- Hardware & Software IT Services

- Malware Analysis Market

Malware Analysis Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Malware Analysis Market by Component (Solutions (Static Analysis, Dynamic Analysis), Services (Training, Consulting and Advisory, Integration and Implementation, Managed SIEM)), by Deployment (On-premise, Cloud), Enterprise Size (Small and Medium-Sized Enterprises, Large Enterprise), Vertical (BFSI, Government and Defense, Healthcare, IT and Telecom, Manufacturing, Research and Academia), and Regional Analysis, 2026 - 2033

Malware Analysis Market Size and Trend Analysis

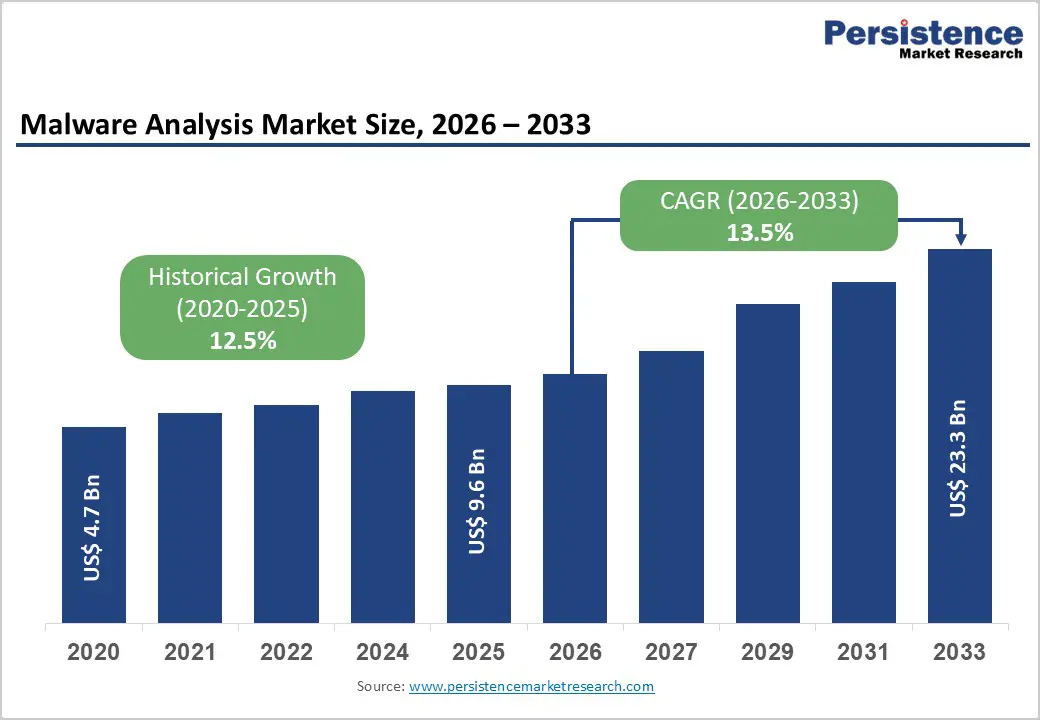

The global malware analysis market size is expected to be valued at US$ 9.6 billion in 2026 and projected to reach US$ 23.3 billion by 2033, growing at a CAGR of 13.5% between 2026 and 2033.

The market is experiencing accelerated growth driven by the exponential increase in sophisticated cyber threats, ransomware attacks, and polymorphic malware variants that evade traditional signature-based detection mechanisms. Organizations across all industry verticals are experiencing unprecedented attack frequencies, with over 3,000 cyberattacks recorded weekly in India alone and global ransomware incidents surging 36% year-over-year through 2025. The integration of artificial intelligence and machine learning capabilities into malware analysis platforms is enabling organizations to detect zero-day exploits, advanced persistent threats, and behavioral anomalies that traditional antivirus solutions fail to identify, compelling enterprises to invest substantially in comprehensive malware analysis solutions and managed security services.

Key Industry Highlights:

- Leading Region: North America holds the largest market share at about 42%, driven by high cybersecurity spending, strong vendor presence, and strict regulatory compliance.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a 16.8% CAGR through 2032 due to rapid digitalization, rising cloud adoption, and surging cyberattacks.

- Dominant Segment: The solutions segment leads the market with around 68% share in 2025 as organizations adopt advanced static, dynamic, and AI-based malware analysis tools.

- Fastest Growing Segment: Cloud deployment is the fastest-growing segment with a 15.8% CAGR through 2032, supported by scalable, subscription-based infrastructure and real-time threat intelligence.

- Key Market Opportunity: The biggest opportunity lies in APT detection for government and defense, where sophisticated nation-state threats require specialized high-security malware analysis capabilities.

| Key Insights | Details |

|---|---|

|

Malware Analysis Market Size (2026E) |

US$ 9.6 billion |

|

Market Value Forecast (2033F) |

US$ 23.3 billion |

|

Projected Growth CAGR (2026-2033) |

13.5% |

|

Historical Market Growth (2020-2025) |

12.5% |

Market Dynamics

Drivers- Accelerating Frequency and Sophistication of Ransomware and Polymorphic Malware Attacks

The global ransomware landscape has undergone a fundamental transformation, with organized cybercriminal groups deploying increasingly sophisticated attack toolkits including Rust-based encryptors, polymorphic payload capabilities, and advanced runtime controls targeting multiple operating systems simultaneously. Healthcare organizations experienced a 30% surge in ransomware attacks targeting vendors and service providers in 2025, with average ransom demands reaching US$514,000 per incident. Meanwhile, confirmed healthcare provider attacks resulted in breaches of over 7.4 million records.

The proliferation of Ransomware-as-a-Service (RaaS) platforms has democratized attack capabilities, enabling less-skilled threat actors to launch enterprise-grade campaigns, compelling organizations to adopt advanced malware analysis solutions combining static analysis, dynamic analysis, and behavioral monitoring. Leading ransomware strains, including Qilin, Play, and Akira, are aggressively expanding, with Qilin alone accounting for 14.1% of reported ransomware incidents, underscoring sustained demand for organizations to deploy comprehensive malware analysis capabilities.

Integration of Artificial Intelligence and Machine Learning in Dynamic Malware Analysis Capabilities

Malware analysis platforms that incorporate AI-driven behavioral analysis and machine learning algorithms trained on over 600 million samples enable security teams to identify previously unknown threats with unprecedented accuracy and speed. Organizations implementing AI-powered malware analysis solutions are achieving 63% improvements in attack detection accuracy, with the capability to identify zero-day variants and evasion techniques that traditional signature-based approaches consistently miss.

Leading vendors, including Palo Alto Networks WildFire, Cisco Threat Grid, and Zscaler Cloud Sandbox, are demonstrating the commercial viability of AI-enhanced malware analysis through substantial revenue growth, with Palo Alto Networks reporting 35% year-over-year SASE segment growth where malware analysis functionality represents a critical component. The AI integration into malware sandboxing solutions enables automated threat classification, reduces false positives, and integrates seamlessly with SIEM and SOAR platforms, reducing mean time to detection and response for security operations centers.

Restraints - Challenges Associated with Malware Evasion and Sandbox Detection Avoidance Techniques

Advanced malware authors have developed sophisticated techniques to detect and evade cloud-based malware analysis sandboxes, including detection of virtualized environments, hypervisor identification, and conditional execution triggering only under specific environmental conditions. Organizations report that approximately 99% of cloud misconfigurations go undetected during initial implementation, creating security blind spots in which malicious files can bypass analysis platforms through sandbox evasion. The continuous arms race between malware developers implementing evasion mechanisms and security vendors deploying countermeasures creates sustained operational challenges requiring continuous platform updates, algorithm refinement, and infrastructure enhancements that increase the total cost of ownership for malware analysis solutions.

Complexity of Multi-Cloud and Hybrid Environment Malware Analysis and Detection Coordination

Organizations maintaining hybrid and multi-cloud infrastructures face significant challenges in coordinating malware analysis across disparate platforms, including on-premises systems, private clouds, and multiple public cloud environments with distinct security policies and isolation boundaries. Integration complexity compounds when organizations maintain legacy on-premise systems that require air-gapped security architectures incompatible with internet-dependent cloud sandbox services, necessitating expensive hybrid malware analysis solutions that support both on-premise and cloud analysis. The operational overhead associated with managing multiple malware analysis platforms, integrating threat intelligence feeds, correlating findings across heterogeneous environments, and maintaining compliance with diverse regulatory frameworks creates organizational friction, limiting adoption among resource-constrained enterprises.

Opportunity - Expansion of Malware Analysis Services in Small and Medium-Sized Enterprise Segment Addressing Security Maturity Gap

Small and medium-sized enterprises represent the fastest-growing market segment for malware analysis solutions, driven by 73% of SMBs experiencing data breaches or cyberattacks in 2023, with average incident costs reaching US$ 3.31 million for organizations employing fewer than 500 people. SMEs historically lacked access to enterprise-grade malware analysis solutions due to complexity and cost barriers, but subscription-based SaaS models and managed security service provider offerings are democratizing access to sophisticated threat analysis capabilities.

Cloud-based malware analysis platforms are enabling SMBs to achieve enhanced threat detection without requiring dedicated security expertise or on-premise infrastructure investments, with research indicating that 56-59% of SMBs have experienced increased attack volume and complexity necessitating professional managed detection and response services incorporating advanced malware analysis functionality.

Government and Defense Sector Demand for Advanced Persistent Threat Detection and Attribution Capabilities

Government agencies and defense contractors face persistent targeting by nation-state advanced persistent threat groups, with documented attacks including APT33 targeting the Defense Industrial Base with FalseFront backdoor malware, Cl0p ransomware targeting over 169 organizations, including US Department of Defense entities, and targeted campaigns against satellite, defense, pharmaceutical, and research organizations across multiple countries.

Government cybersecurity spending is accelerating, with agencies implementing Zero Trust architecture, EDR/XDR solutions, and sophisticated malware analysis capabilities that enable threat attribution and forensic investigation of state-sponsored attacks. The Cybersecurity and Infrastructure Security Agency (CISA) and international government agencies are establishing shared threat intelligence platforms that require integration with malware analysis solutions, creating sustained demand for government-grade malware analysis offerings that incorporate classified threat intelligence feeds and specialized analysis capabilities unavailable in commercial solutions.

Category-wise Analysis

Component Insights

Solutions emerge as the dominant component in the malware analysis market, commanding approximately 68% of market share in 2025, driven by organizational emphasis on deploying advanced static, dynamic, and hybrid analysis capabilities for comprehensive threat detection. Solutions encompassing behavioral-based detection, signature-less analysis, and AI-powered threat classification enable organizations to identify polymorphic malware, zero-day exploits, and sophisticated evasion techniques that traditional solutions fail to detect.

The proliferation of cloud-native sandboxing solutions offering real-time analysis, unlimited latency-free inspection, and instant AI-driven verdicts is establishing Solutions as the foundational malware analysis capability, with research indicating that organizations maintaining fewer than 50 cybersecurity solutions demonstrate recovery times exceeding four hours, compared to organizations consolidating solutions demonstrating recovery within one hour.

Deployment Insights

Cloud-based deployment leads the segment with approximately 58% market share in 2025, reflecting organizational preference for subscription-based, scalable infrastructure that eliminates capital expenditure requirements and reduces operational maintenance overhead. Cloud deployment enables organizations to leverage unlimited processing capacity, instant threat intelligence updates, and seamless integration with distributed security architectures spanning multiple geographies and cloud service providers.

Enterprise Size Insights

Large Enterprises dominate the enterprise-size segment, commanding approximately 68% market share in 2025, reflecting a significantly larger attack surface, greater financial capacity to invest in comprehensive security infrastructure, and regulatory requirements necessitating advanced malware analysis capabilities across distributed enterprise environments. Large enterprises maintain an estimated 350 million endpoints requiring coordinated malware analysis and threat intelligence, creating substantial revenue opportunities for vendors offering enterprise-scale platforms supporting thousands of simultaneous analyses.

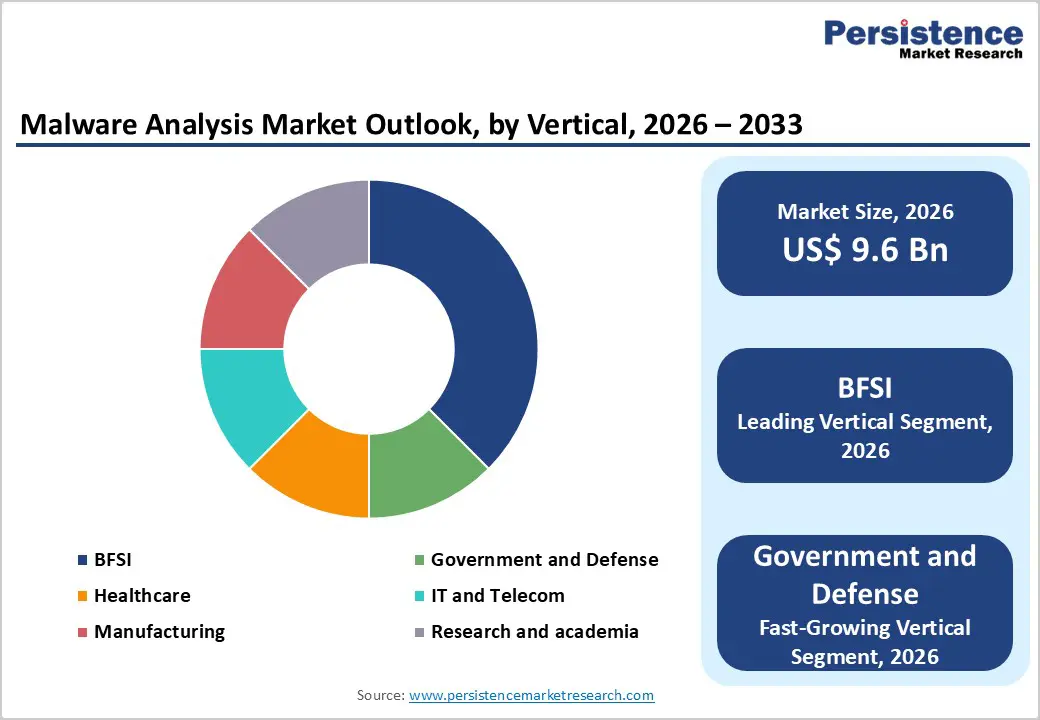

Vertical Insights

The Banking, Financial Services, and Insurance (BFSI) vertical leads with approximately 31% market share in 2025, reflecting substantial regulatory compliance requirements under frameworks such as PCI-DSS and HIPAA, as well as emerging standards mandating advanced threat detection and forensic capabilities. Financial institutions are experiencing escalating attack sophistication with ransomware attacks increasing 13-fold in 2023, average breach costs reaching US$ 5.9 million, and sophisticated supply chain attacks, including MOVEit transfer hacks, compromising financial institution supply chains.

However, Government and Defense represent the fastest-growing vertical with an estimated 18.5% CAGR through 2032, driven by persistent targeting by nation-state APT groups, government spending initiatives on cybersecurity infrastructure, and classified threat intelligence requirements necessitating specialized malware analysis platforms incorporating government-specific threat feeds and analysis capabilities unavailable in commercial offerings.

Regional Insights

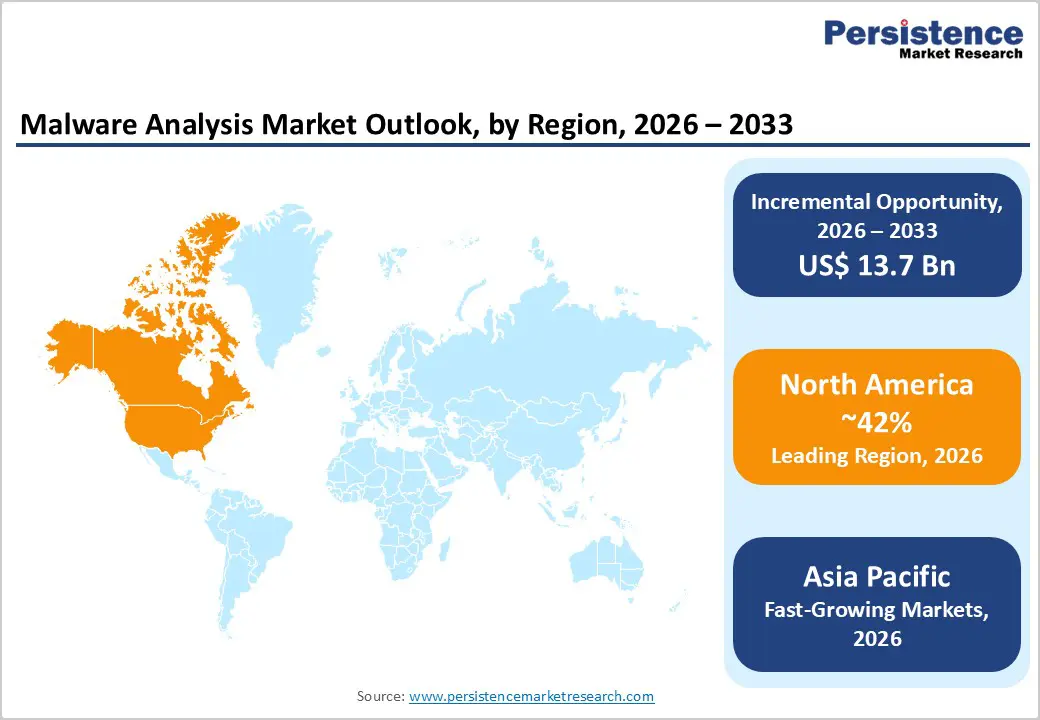

North America Malware Analysis Market Trends and Insights

North America maintains the dominant regional position, accounting for approximately 42% of the global malware analysis market share in 2025, driven by the presence of leading cybersecurity vendors, including Cisco Systems, Palo Alto Networks, FireEye, Symantec Corporation, Fortinet, and Check Point Software Technologies, alongside substantial enterprise IT spending and mature security procurement processes. North American organizations demonstrate aggressive investment in malware analysis infrastructure, reflecting 14.3% growth from 2023, driven primarily by investments in ransomware prevention and malware analysis capabilities.

The North American regulatory environment, including HIPAA, PCI-DSS, SOX, and state-level data protection mandates, establishes a compliance baseline driving the adoption of advanced malware analysis solutions across regulated industries, including healthcare, finance, and government. The region’s robust cybersecurity ecosystem, venture capital funding for security startups, and established managed security service provider market create competitive dynamics driving innovation in behavioral analysis, AI-powered threat detection, and integration of malware analysis with security orchestration platforms.

Europe Malware Analysis Market Trends and Insights

Europe represents the second-largest regional market, commanding approximately 28% of the global malware analysis market share while experiencing sustained growth driven by stringent General Data Protection Regulation (GDPR) requirements, industry-specific regulations, and a cyber threat landscape intensity comparable to North America. European organizations face significant regulatory pressure to demonstrate advanced threat detection and forensic investigation capabilities, with GDPR Article 32 mandating technical and organizational measures to ensure the security of personal data, compelling the adoption of sophisticated malware analysis solutions to support incident investigation and breach notification requirements.

Major European technology hubs, including Germany, the United Kingdom, and France, are experiencing accelerated malware analysis adoption driven by sophisticated supply chain attacks, government cybersecurity initiatives, and substantial enterprise IT investments. Germany specifically operates under stringent German IT Security Act (IT-Sicherheitsgesetz) and sector-specific regulations requiring continuous threat monitoring and advanced incident investigation capabilities, establishing sustained demand for malware analysis platforms with European data residency compliance and localized threat intelligence feeds.

Asia Pacific Malware Analysis Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market, expected to expand at an estimated 16.8% CAGR through 2032, driven by rapid digital transformation, explosive growth in cloud adoption, and accelerating sophistication of cyberattacks targeting the region. India alone experiences over 3,000 cyberattacks weekly, with ransomware groups expanding aggressively and deploying increasingly sophisticated attack toolkits, creating urgent demand for advanced malware analysis solutions and managed security services.

China, Japan, and India represent critical growth markets in the Asia Pacific, and the India Digital Threat Report 2024 highlights essential vulnerabilities in the BFSI sector and government systems that require advanced malware analysis capabilities. Japan and South Korea maintain substantial cybersecurity spending driven by government digitalization initiatives and concern regarding state-sponsored attacks, while India’s rapidly expanding digital economy, cryptocurrency trading platforms, and government services digitalization create an expanding attack surface necessitating widespread adoption of malware analysis solutions across enterprise and government organizations.

Competitive Landscape

The global malware analysis market exhibits moderate to high concentration, with dominant positions held by established cybersecurity leaders, including FireEye, Cisco Systems, Palo Alto Networks, Symantec Corporation, Kaspersky Lab, Fortinet, and Check Point Software Technologies, commanding significant market share through comprehensive security portfolios and extensive customer bases. These established vendors leverage substantial research and development investments, vertical integration of threat intelligence capabilities, and strategic acquisitions of specialized malware-analysis startups to maintain their competitive positioning. The market also features agile specialized vendors focusing on emerging technologies including behavioral analysis, machine learning-powered threat detection, and cloud-native sandboxing capabilities, with newer entrants including Intezer, Joe Security, VMRay, and Proofpoint challenging incumbents through innovation in specific malware analysis domains. Market differentiation increasingly centers on AI integration, threat intelligence breadth, ease of integration with existing security infrastructure, and ability to detect zero-day exploits and evasion techniques rather than basic malware analysis functionality.

Key Market Developments:

- January 2025: Cisco completes acquisition of SnapAttack, a threat detection and defense firm, to bolster Splunk's security innovations and enhance SOC capabilities for advanced threat hunting.

- May 2025: Check Point launches an AI/ML-powered automated threat intelligence platform in Singapore, integrating threat intelligence, dark web tracking, SaaS/email protection, and remediation to enable proactive enterprise threat detection and Zero Trust compliance.

Companies Covered in Malware Analysis Market

- FireEye Inc.

- Cisco Systems Inc

- Palo Alto Networks

- Sophos Ltd

- Symantec Corporation

- Kaspersky Lab

- Fortinet Inc.

- Check Point Software Technologies

- Qualys Inc.

- MCAFEE LLC

- Broadcom Inc.

- Juniper Networks Inc.

- Trend Micro Incorporated

- CrowdStrike Holdings Inc.

- Microsoft Corporation

- Proofpoint Inc.

- Intezer Labs

- VMRay

- Joe Security

- Malwarebytes

Frequently Asked Questions

The malware analysis market is expected to reach around US$ 9.6 billion by 2026.

Rising ransomware incidents, growth in polymorphic malware, and adoption of AI-driven analysis tools are the key demand drivers.

North America leads the market with the highest share due to strong cybersecurity spending and strict compliance norms.

The biggest opportunity lies in advanced persistent threat (APT) detection and investigation solutions for defense and government.

Leading market players include cybersecurity giants FireEye, Cisco Systems, Palo Alto Networks, Symantec Corporation, Kaspersky Lab, Fortinet, and Check Point Software Technologies.