- Smart Packaging

- Magnetic Closure Boxes Market

Magnetic Closure Boxes Market Size, Share, and Growth Forecast, 2026 - 2033

Magnetic Closure Boxes Market by Material Type (Cardboard, Plastic, Others), End-use Industry (Retail Packaging, Luxury Goods Packaging, Others), Closure Mechanism, and Regional Analysis for 2026 - 2033

Magnetic Closure Boxes Market Size and Trends Analysis

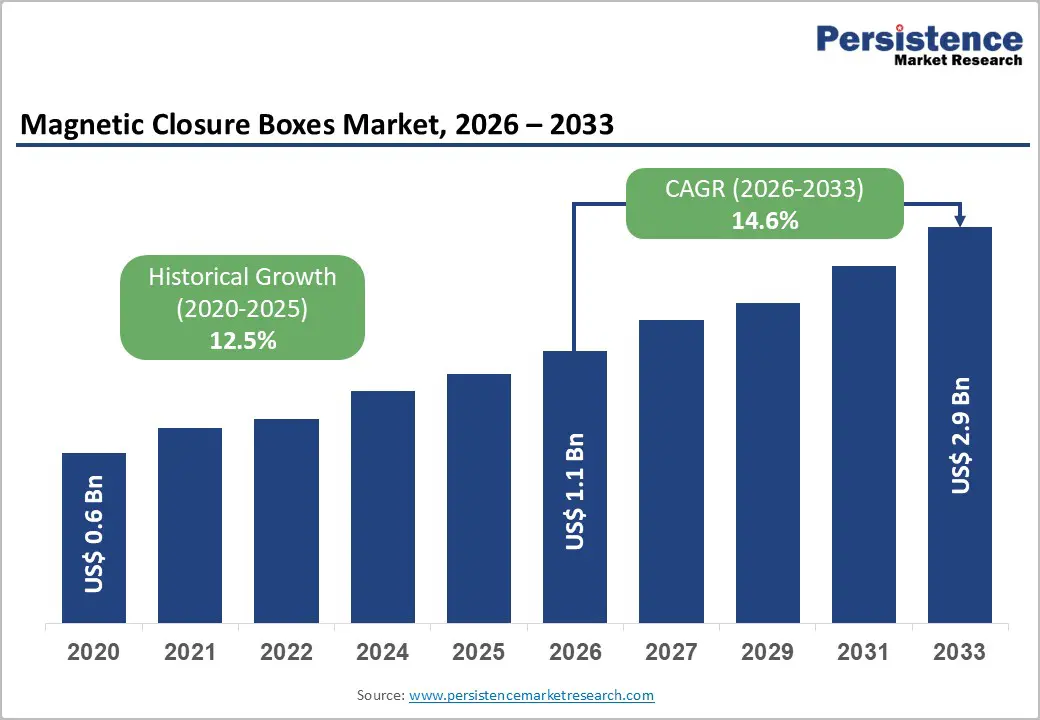

The global magnetic closure boxes market size is likely to be valued at US$1.1 billion in 2026 and is expected to reach US$2.9 billion by 2033, growing at a CAGR of 14.6% between 2026 and 2033, driven by a structural shift toward premium, reusable, and brand-centric packaging formats, particularly across retail, luxury goods, cosmetics, and consumer electronics.

Rising e-commerce penetration, heightened focus on unboxing experiences, and regulatory pressure to adopt recyclable rigid packaging are accelerating adoption.

Key Industry Highlights

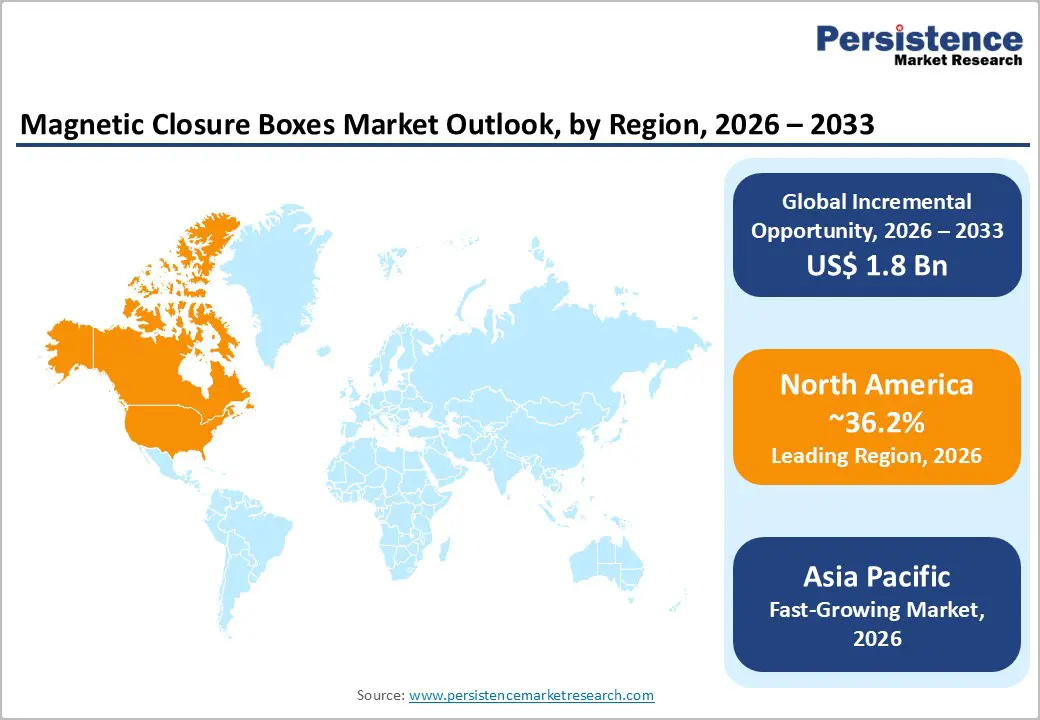

- Leading Region: North America is projected to lead the market, accounting for approximately 36.2% of total market share, supported by the U.S.’s advanced retail ecosystem, strong luxury consumption, and high adoption of premium, reusable rigid packaging across e-commerce, cosmetics, and branded gifting applications.

- Fastest-Growing Region: Asia Pacific represents the fastest-growing regional market, driven by large-scale manufacturing capacity in China and India, rising middle-class consumption, and increasing export-oriented production for global luxury and electronics brands.

- Investment Plans: Industry investment is increasingly focused on sustainable rigid packaging innovation, automation, and capacity expansion in Asia Pacific and Eastern Europe, with leading players allocating capital toward recyclable paperboard structures, detachable magnetic closures, and digitally enabled customization to meet regulatory and brand requirements.

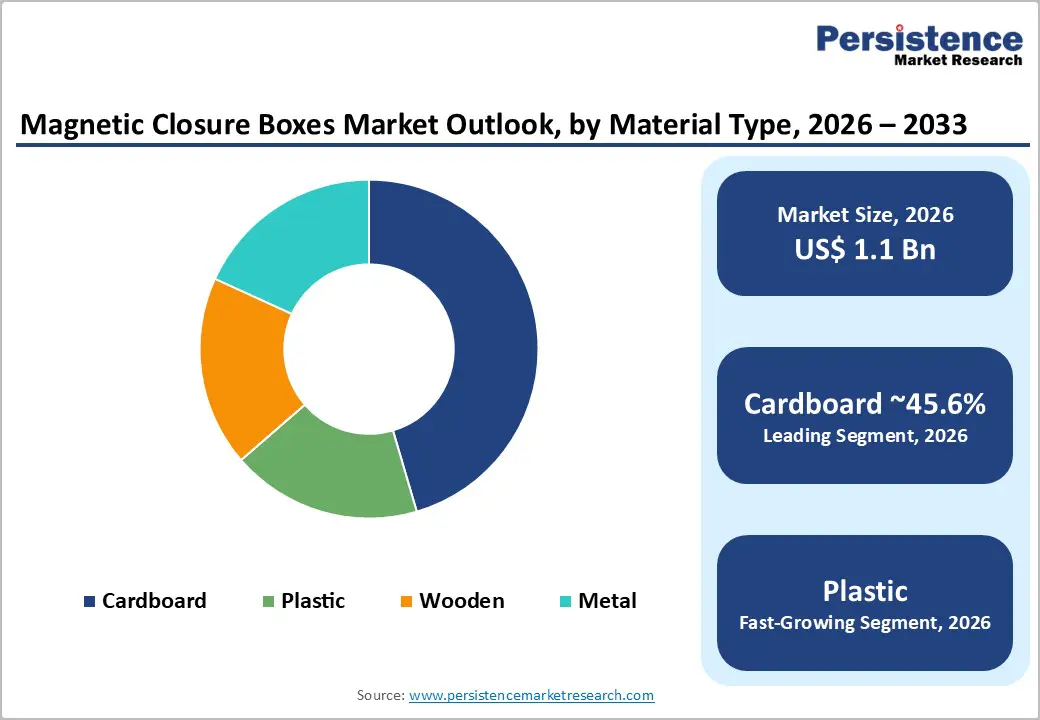

- Dominant Material Type: The cardboard segment is anticipated to be the dominant material type, accounting for approximately 45.6% of the market share in 2026, owing to its recyclability, cost-efficiency, regulatory compliance, and suitability for premium finishes across retail and cosmetics packaging.

- Leading End-use Industry: Retail packaging is expected to lead, holding around 54.3% of market demand in 2026, driven by sustained growth in e-commerce, direct-to-consumer channels, and brand emphasis on enhanced unboxing experiences and product protection.

| Key Insights | Details |

|---|---|

| Magnetic Closure Boxes Market Size (2026E) | US$1.1 Bn |

| Market Value Forecast (2033F) | US$2.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Expansion of Premium and Experience-Driven Retail Packaging

Premiumization in consumer goods has emerged as a core demand driver for magnetic closure boxes. According to data from McKinsey & Company and Euromonitor, over 35% of global consumers indicate that packaging quality influences brand perception and repeat purchase behavior, particularly in the luxury and cosmetics segments. Magnetic closure boxes provide tactile value, structural rigidity, and reusability, aligning with this shift.

E-commerce growth further amplifies demand. The U.S. Census Bureau reports consistent double-digit growth in online retail sales, increasing brand reliance on packaging that protects products while enhancing visual appeal. Magnetic closure boxes reduce secondary packaging needs, improving cost efficiency across logistics and returns management.

Sustainability Regulations and Material Innovation

Government regulations targeting single-use plastics and non-recyclable packaging are materially influencing packaging choices. The European Commission’s Packaging and Packaging Waste Directive (PPWD) and similar frameworks in Canada and India emphasize recyclability and extended producer responsibility.

Cardboard-based magnetic closure boxes, which account for 45.6% of material usage, meet these compliance standards while maintaining premium aesthetics. Advances in water-based adhesives, biodegradable coatings, and recyclable magnets are lowering environmental impact. Industry associations such as FEFCO and American Forest & Paper Association (AF&PA) confirm rising investments in rigid paperboard innovation, directly benefiting this market.

Growth in High-Value Consumer Electronics and Cosmetics

Global cosmetics and personal care revenues exceeded US$500 billion in 2024, according to L’Oréal and Estée Lauder annual filings, while consumer electronics shipments continue to rise in Asia Pacific. These sectors demand tamper-resistant, premium packaging that supports brand differentiation.

Magnetic closure boxes, particularly double-magnet formats, provide enhanced security and repeated usability. Their ability to integrate inserts, foam linings, and branding elements supports higher average selling prices, driving manufacturer margins and long-term adoption.

Barrier Analysis - Higher Unit Costs Compared to Conventional Folding Cartons

Magnetic closure boxes incur 20-35% higher production costs than standard rigid or folding cartons, driven by magnet integration, manual assembly, and premium finishing processes. For price-sensitive markets, particularly in mass retail and food packaging, this cost differential limits penetration.

Small and mid-sized brands face margin pressure, especially during periods of raw material volatility. Data from World Bank commodity indices show persistent fluctuations in paperboard and metal inputs, creating procurement uncertainty for packaging converters.

Recycling Complexity and Magnet Separation Challenges

While cardboard components are recyclable, embedded magnets introduce separation challenges within conventional recycling streams. According to WRAP UK and EPA packaging guidelines, improper separation reduces recycling efficiency and raises contamination risks.

Regulatory scrutiny is increasing, particularly in Europe, where recyclability scoring systems influence packaging approvals. Manufacturers must invest in detachable magnet designs or certified recycling processes, increasing compliance costs and lengthening product development cycles.

Opportunity Analysis - Rapid Growth in Asia Pacific Luxury and Retail Packaging

Asia Pacific represents the fastest-growing regional market, supported by rising disposable incomes and luxury consumption in China, India, and Southeast Asia. According to World Bank income distribution data, the region adds over 70 million middle-income consumers annually.

Magnetic closure boxes are increasingly adopted by premium apparel, gifting, and electronics brands. The addressable opportunity in Asia Pacific is estimated to exceed US$900 million by 2033, supported by localized manufacturing and export-oriented packaging hubs.

Customization and Smart Packaging Integration

Brands are investing in customized structural packaging, including embossing, foil stamping, and NFC-enabled authentication. Magnetic closure boxes provide ideal platforms for such integration. Industry reports from Deloitte and BCG indicate that smart packaging adoption can increase consumer engagement rates by 20-30%. This creates incremental revenue opportunities for converters offering value-added services, expanding profit pools beyond commoditized packaging formats.

Corporate Gifting and Subscription Box Expansion

The corporate gifting and subscription box market continues to grow at over 12% annually, driven by B2B branding and DTC models. Magnetic closure boxes offer durability and reusability, aligning with these applications.

As enterprises seek differentiated packaging for employee engagement and customer retention, demand for medium-volume, high-design packaging formats is accelerating, opening new mid-market revenue streams.

Category-wise Insights

Material Type Insights

Cardboard-based magnetic closure boxes are expected to lead the market, representing around 45.6% of the total revenue, owing to their cost-effectiveness, recyclability, and versatile structural design suitable for both premium and semi-premium applications. Rigid paperboard allows for sophisticated finishing options, including embossing, foil stamping, matte lamination, and UV coating, making these boxes ideal for retail gifting, cosmetics, and branded promotional packaging. From a regulatory standpoint, cardboard meets sustainability standards outlined in frameworks such as the EU Packaging and Packaging Waste Directive and extended producer responsibility (EPR) regulations in North America. Retailers and cosmetics brands favor cardboard magnetic boxes for their ease of customization and scalable production, especially in e-commerce-driven markets. For instance, premium skincare and apparel brands are increasingly adopting rigid cardboard magnetic boxes for seasonal releases and subscription kits, achieving a balance between premium presentation, regulatory compliance, and recyclability.

Plastic magnetic closure boxes are likely to be the fastest-growing material segment, driven primarily by superior durability, moisture resistance, and impact protection. These attributes are particularly valuable in cosmetics, personal care, and consumer electronics packaging, where product integrity during storage and transit is critical. High-gloss finishes and transparent or hybrid plastic designs also enhance shelf appeal in duty-free and specialty retail environments. Sustainability concerns are being addressed through recyclable polymers, reduced material thickness, and cardboard-plastic hybrid structures, especially within Asia Pacific manufacturing ecosystems. For instance, electronics accessory brands in China and South Korea increasingly use plastic magnetic boxes for premium earbuds and wearable devices, where durability and presentation outweigh single-material packaging constraints.

End-use Industry Insights

Retail packaging is anticipated to be the largest end-use segment, holding approximately 54.3% of the global revenue share, supported by the continued expansion of e-commerce, direct-to-consumer (DTC) models, and experiential branding strategies. Magnetic closure boxes enhance the unboxing experience, improve brand recall, and reduce product damage during last-mile delivery, making them a preferred choice for premium retail offerings. Online apparel, lifestyle, and gifting brands increasingly deploy magnetic closure boxes for limited editions, festive packaging, and influencer kits. For example, mid- to high-end fashion retailers and curated gift platforms use magnetic boxes to differentiate brand positioning while maintaining packaging durability across fulfillment networks.

Luxury goods packaging is emerging as the fastest-growing end-use segment as brands intensify focus on premium tactile experiences, reusability, and long-term brand association. Magnetic closure boxes reinforce exclusivity and craftsmanship, aligning closely with luxury brand values. High-end fashion houses, jewelry brands, and premium spirits manufacturers increasingly adopt magnetic closures for watches, fragrances, and limited-edition liquor packaging. For instance, luxury perfume and jewelry brands use multi-layered magnetic boxes with custom inserts to enhance perceived value and support reuse, strengthening customer retention and brand storytelling.

Regional Insights

North America Magnetic Closure Boxes Market Trends - Luxury Branding, DTC Expansion, and Recyclable Rigid Packaging

North America is projected to represent the largest regional market, accounting for an estimated 36.2% of market share, driven primarily by the mature retail infrastructure, strong luxury consumption, and advanced branding ecosystem in the U.S. High per-capita spending on premium goods, coupled with the widespread adoption of direct-to-consumer (DTC) and omnichannel retail models, has elevated demand for rigid, experience-oriented packaging formats. Magnetic closure boxes are increasingly positioned as a value-adding packaging solution rather than a cost center, particularly within apparel, cosmetics, electronics, accessories, and corporate gifting.

Regulatory clarity around sustainable packaging also supports market stability. Frameworks such as U.S. state-level extended producer responsibility (EPR) programs, including those implemented in California, Oregon, and Colorado, are encouraging the use of recyclable paperboard-based magnetic boxes over complex plastic alternatives. In response, companies such as WestRock and International Paper have expanded investments in recyclable rigid box solutions, integrating detachable magnets and fiber-based substrates to improve compliance without compromising premium aesthetics.

From a brand perspective, North American luxury and beauty companies are actively influencing packaging demand. Estée Lauder Companies and LVMH’s U.S. operations have increased their use of reusable magnetic rigid boxes for holiday gift sets and limited-edition launches, reinforcing brand storytelling and sustainability narratives. Automation investments are also reshaping competitive dynamics, with U.S. packaging converters adopting robotic box assembly and digital finishing to manage rising labor costs while maintaining customization flexibility.

Europe Magnetic Closure Boxes Market Trends - Regulation-Compliant Premium Design for High-Value Applications

Europe remains a mature yet innovation-led market, characterized by strong regulatory alignment, premium brand density, and advanced sustainability standards. Germany, the U.K., and France collectively account for the majority of regional demand, supported by robust luxury goods, cosmetics, and premium spirits industries. Magnetic closure boxes in Europe are primarily adopted in high-value, low-volume applications, where packaging quality directly influences brand equity and consumer perception.

Regulatory harmonization under the EU Packaging and Packaging Waste Directive (PPWD) and the upcoming Packaging and Packaging Waste Regulation (PPWR) has accelerated the adoption of recyclable and mono-material rigid packaging formats. European converters such as Smurfit Kappa, DS Smith, and Stora Enso have responded by developing paper-based magnetic closure boxes with reduced material weight and improved recyclability scores, enabling brand owners to meet compliance requirements without sacrificing design complexity.

Luxury and premium consumer brands play a decisive role in shaping regional demand. For example, Diageo and Pernod Ricard have increasingly adopted magnetic rigid boxes for limited-edition whisky and cognac packaging in Western Europe, using premium closures to support gifting and collector-oriented consumption. European cosmetics brands, including those under L’Oréal Group, have expanded the use of magnetic boxes in high-end skincare and fragrance launches, reinforcing Europe’s position as a design-driven and regulation-compliant packaging market.

Asia Pacific Magnetic Closure Boxes Market Trends - Export-Oriented Manufacturing and Rising Premium Consumption

Asia Pacific is likely to be the fastest-growing regional market, supported by manufacturing scale, cost efficiency, expanding middle-class populations, and rising premium consumption. China and India dominate production due to their well-established packaging manufacturing ecosystems, while consumption growth is accelerating across Southeast Asia, Japan, and South Korea. The region’s growth is underpinned by both domestic demand and export-oriented packaging production for global luxury and retail brands.

China remains the primary manufacturing hub for magnetic closure boxes, with companies in Guangdong and Zhejiang supplying premium rigid packaging to North American and European brands. Chinese packaging firms increasingly invest in automation, quality control, and sustainable materials to meet international compliance standards. At the same time, Indian packaging manufacturers are expanding rigid box capabilities to serve domestic luxury, cosmetics, and gifting markets, supported by rising disposable incomes and organized retail expansion.

Brand activity is a key catalyst in the region. Global luxury brands such as Louis Vuitton, Chanel, and Apple rely heavily on Asia Pacific manufacturing partners for premium rigid packaging, indirectly stimulating regional technology upgrades and capacity expansion. In Southeast Asia, e-commerce-driven gifting platforms and premium confectionery brands are adopting magnetic closure boxes to differentiate offerings, particularly during festive seasons. Collectively, these trends position Asia Pacific as the most dynamic growth engine for the magnetic closure boxes market over the forecast period.

Competitive Landscape

The global magnetic closure boxes market is moderately fragmented, with the top 10 players accounting for approximately 45-50% of global revenue. Regional converters compete on customization, while global players focus on innovation and multinational contracts. Large, integrated packaging companies such as Smurfit Kappa, DS Smith, WestRock, Mondi Group, and International Paper compete primarily through innovation, sustainability compliance, and multinational customer relationships.

These players leverage vertically integrated supply chains, advanced material science expertise, and global production footprints to serve multinational luxury, retail, and cosmetics brands. Their scale enables consistent quality, regulatory alignment across regions, and long-term supply agreements with global brand owners.

In contrast, regional and specialty converters differentiate through short lead times, high design flexibility, and bespoke finishing capabilities. These players are particularly competitive in luxury goods, gifting, and promotional packaging, where low-to-medium volumes and high aesthetic complexity favor customization over cost efficiency. Many regional firms maintain close relationships with local fashion houses, cosmetics brands, and e-commerce retailers, allowing rapid response to seasonal demand and limited-edition product launches.

Key Industry Developments

- In March 2025, Mondi Group announced the acquisition of BoxPak’s premium packaging operations to expand its magnetic-closure box manufacturing capacity and strengthen its global footprint in high-end packaging solutions.

- In January 2025, WestRock Company launched a new magnetic-closure packaging line, ‘MagnetiBox Elite,’ aimed at the premium consumer electronics and cosmetics sectors to capture rising demand for durable, brand-enhancing packaging formats.

Companies Covered in Magnetic Closure Boxes Market

- WestRock Company

- Smurfit Kappa Group

- International Paper Company

- DS Smith Plc

- Mondi Group

- Stora Enso Oyj

- Packaging Corporation of America

- Georgia-Pacific LLC

- Oji Holdings Corporation

- Graphic Packaging International

- Cascades Inc.

- Amcor Plc

- Sonoco Products Company

- PakFactory

- Sunrise Packaging

- Blue Box Packaging

- Emenac Packaging

- Claws Custom Boxes

Frequently Asked Questions

The magnetic closure boxes market is estimated at US$1.1 billion in 2026.

The magnetic closure boxes market is forecast to reach US$2.9 billion by 2033.

Key trends include premium retail packaging demand, sustainability-focused materials, enhanced unboxing experiences, and growing use in luxury and cosmetics packaging.

Retail packaging leads the magnetic closure boxes market, accounting for around 54.3% of total demand.

The magnetic closure boxes market is projected to grow at a 14.6% CAGR from 2026 to 2033.

Major players include Smurfit Kappa, DS Smith, WestRock, Mondi Group, and International Paper.