- Pharmaceuticals

- Macular Degeneration Treatment Market

Macular Degeneration Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Macular Degeneration Treatment Market by Treatment (Drugs, Medical Devices, and Surgery), by Disease (Dry Age-Related Macular Degeneration, and Wet Age-Related Macular Degeneration), by Route of Administration (Intravitreal, Suprachoroidal, and Intravenous) by End User (Hospitals, Specialty Clinics, and Ambulatory Surgical Centers), and Regional Analysis from 2026 to 2033

Macular Degeneration Treatment Market Share and Trend Analysis

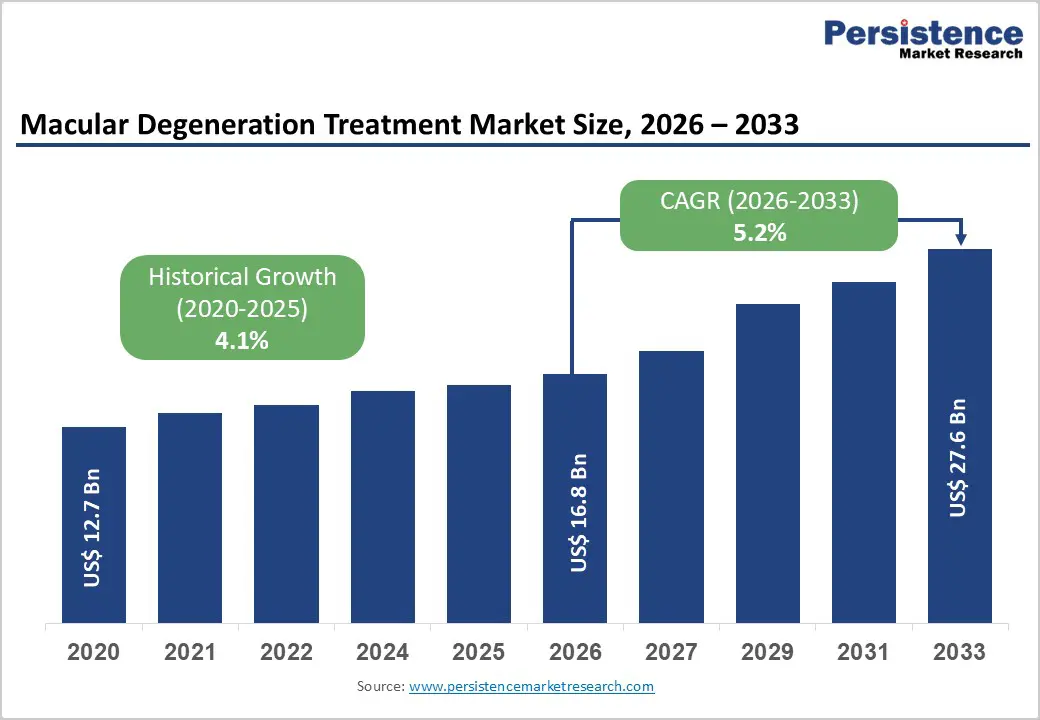

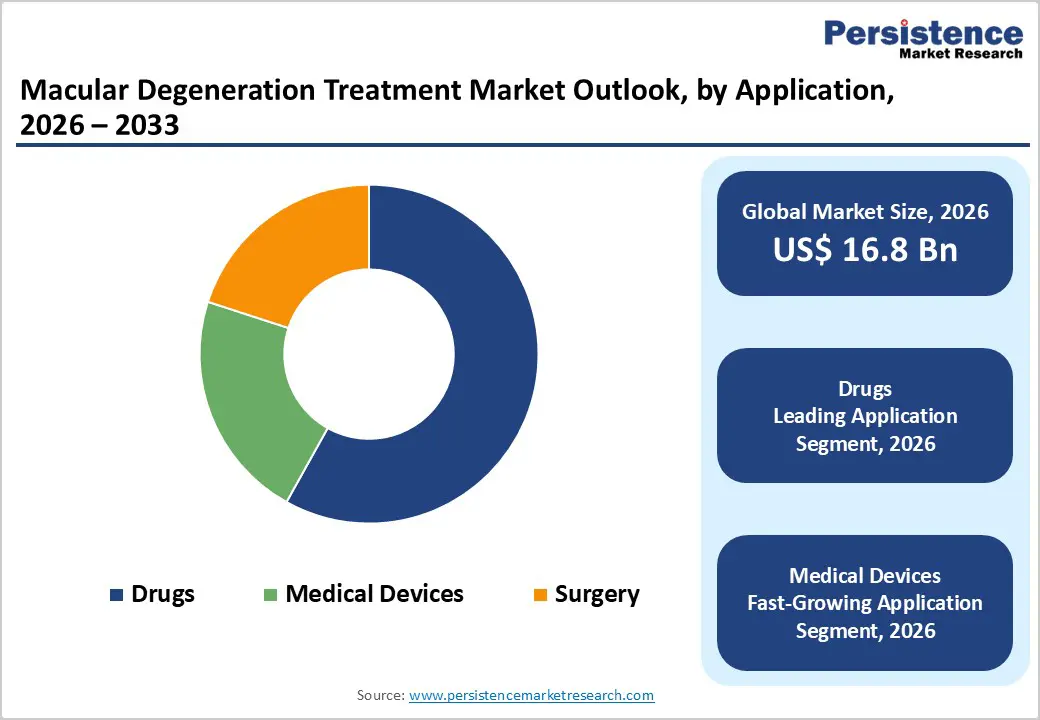

The global macular degeneration treatment market size is estimated to grow from US$ 16.8 Bn in 2026 to US$ 27.6 Bn by 2033. The market is projected to record a CAGR of 5.2% during the forecast period from 2026 to 2033.

Global demand for treatments for macular degeneration is increasing steadily, driven by the rising prevalence of age-related macular degeneration (AMD), growing patient awareness of vision preservation, and expanding access to advanced ophthalmic therapies. Increasing use of anti-VEGF biologics, combination therapies, sustained-release implants, and intravitreal injections across hospitals, specialty clinics, and ambulatory surgical centers is supporting sustained market growth. Higher volumes of wet AMD treatments, growing adoption of early diagnostic imaging such as OCT, and increasing treatment adherence, coupled with rising healthcare expenditure and improved access to specialized ophthalmic care, are further accelerating demand. Continuous innovation in drug delivery systems, minimally invasive injection techniques, and gene therapy pipelines is improving treatment efficacy, patient comfort, and long-term clinical outcomes. Additionally, the growing focus on home-based monitoring, teleophthalmology, and digitally integrated patient care pathways is further propelling the global macular degeneration treatment market.

Key Industry Highlights

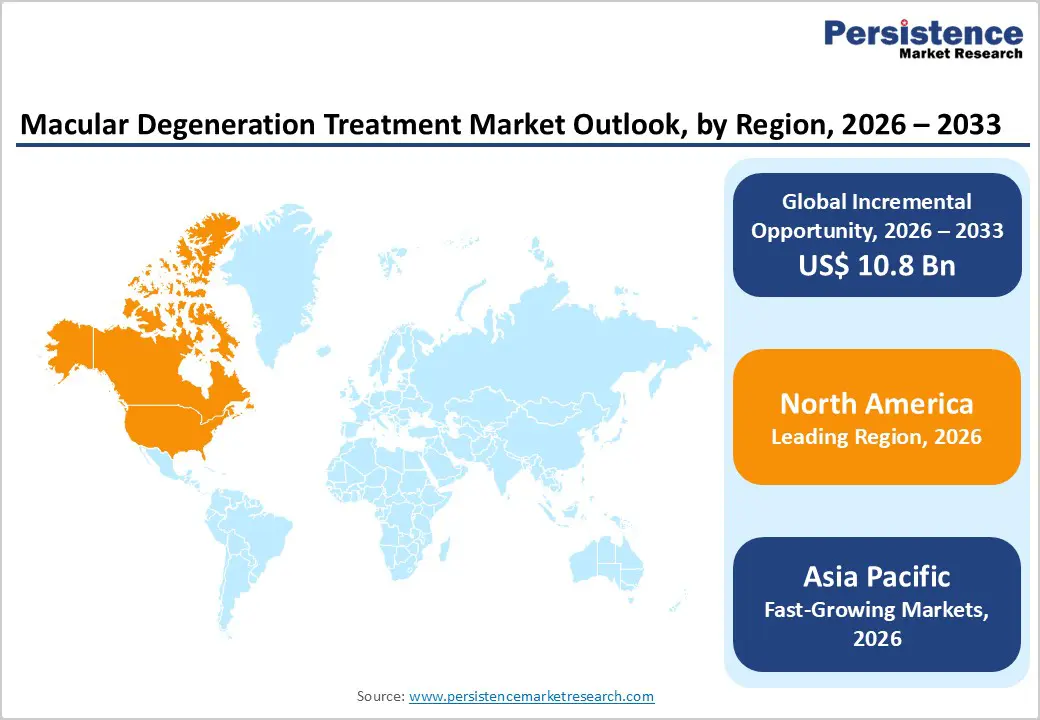

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, high adoption of intravitreal therapies, early uptake of long-acting biologics and home-based ophthalmic care, and strong presence of leading pharmaceutical companies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large AMD patient population, rapid growth in diagnostic and treatment centers, improving healthcare infrastructure, and rising investments in teleophthalmology and home-based eye care.

- Leading Treatment Segment: Drugs dominate the market due to their broad applicability across wet and dry AMD, intravitreal therapy, and sustained-release drug delivery applications.

- Fastest-Growing Treatment Segment: Medical devices are expanding rapidly as adoption of surgical interventions, retinal implants, and advanced diagnostic imaging systems increases.

- Leading Disease Segment: Wet age-related macular degeneration remains the top application, driven by widespread use of intravitreal therapies and high clinical intervention volumes.

- Fastest-Growing Disease Segment: Dry age-related macular degeneration is scaling quickly as demand rises for emerging therapies, early intervention programs, and preventive ophthalmic care.

| Global Market Attributes | Key Insights |

|---|---|

| Macular Degeneration Treatment Market Size (2026E) | US$ 16.8 Bn |

| Market Value Forecast (2033F) | US$ 27.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver - Rising Prevalence of Age-Related Macular Degeneration Coupled with Advancements in Therapeutics and Delivery Technologies

The market is strongly driven by the rising prevalence of age-related macular degeneration (AMD), particularly among aging populations worldwide. As life expectancy increases globally, the number of individuals affected by dry and wet AMD continues to rise, creating significant demand for effective treatments. Wet AMD, being more severe and vision-threatening, contributes heavily to clinical intervention volumes, driving the need for repeated pharmacologic therapy and intravitreal administration. Concurrently, advances in anti-VEGF biologics, combination therapies, sustained-release drug delivery systems, and emerging gene therapies are enhancing treatment efficacy and patient adherence.

The increasing adoption of routine ophthalmic screening, including optical coherence tomography (OCT) and fundus imaging, supports early diagnosis, thereby further elevating treatment volumes. Technological innovations in drug formulation, such as longer-acting biologics, biodegradable implants, and minimally invasive injection systems, are reducing dosing frequency, improving patient comfort, and expanding the eligible treatment population. Greater awareness among patients and clinicians about vision preservation, combined with healthcare system initiatives for early intervention, is reinforcing the dominance of pharmacological and intravitreal treatment approaches. Collectively, the demographic shift toward older populations, coupled with rapid therapeutic innovation, is sustaining robust growth for the global macular degeneration treatment market.

Restraints - High Treatment Costs, Procedural Burden, and Safety Concerns

High costs associated with advanced pharmacological therapies, surgical interventions, and specialized intravitreal devices represent a major restraint limiting broader market adoption. Branded anti-VEGF biologics and novel gene therapy candidates carry premium pricing, making recurring treatment financially burdensome for patients and healthcare providers, particularly in emerging and price-sensitive markets. Repeated intravitreal injections require trained ophthalmologists, sterile clinical environments, and careful patient monitoring, increasing procedural complexity and operational costs.

Safety concerns also pose challenges, including risks of ocular infection, endophthalmitis, intraocular inflammation, and injection-related complications. Patient compliance may be affected by discomfort during procedures, fear of repeated injections, or difficulty accessing specialized clinics. Additionally, reimbursement policies for AMD therapies vary widely across regions, with some countries providing partial coverage for high-cost biologics or advanced implants, limiting equitable access. Limited availability of specialized retinal care in rural or underdeveloped regions further restricts treatment penetration. Collectively, these economic, logistical, and clinical factors act as moderating influences on the adoption of advanced therapies for advanced macular degeneration, potentially slowing uptake despite the growing clinical need.

Opportunity - Expansion of Home-Based, Long-Acting, and Digitally Integrated Therapeutic Solutions

The market presents significant opportunities through the development of long-acting therapies, sustained-release drug delivery systems, and digitally integrated treatment approaches. Advances in biologics with extended dosing intervals and biodegradable intravitreal implants are reducing the frequency of clinical visits, improving patient adherence, and enhancing overall treatment outcomes. Integration of digital platforms for remote monitoring, patient reminders, and adherence tracking is enabling more personalized care and improving long-term vision management.

The expansion of home-based ophthalmic care models, particularly for elderly and mobility-limited patients, is further accelerating the adoption of these innovations. Gene therapy and combination therapeutics targeting both dry and wet AMD subtypes offer opportunities to address previously untreatable conditions, creating a new market segment. Teleophthalmology and AI-driven retinal imaging systems are enhancing early detection, facilitating timely intervention, and supporting population-level screening programs. Emerging markets with increasing healthcare accessibility and awareness of vision preservation present high growth potential, especially when paired with cost-effective or biosimilar therapies. As healthcare systems worldwide shift toward preventive and value-based care, manufacturers that provide integrated, long-acting, and digitally enabled treatment solutions are positioned to capture substantial long-term market share.

Category-wise Analysis

By Treatment, Drugs Dominate Owing to High Adoption of Anti-VEGF and Long-Term Pharmacotherapy

The drugs segment is projected to dominate the global macular degeneration treatment market in 2026, accounting for 58.10% of revenue. This dominance is primarily driven by the widespread and recurring use of anti-VEGF therapies for the management of wet age-related macular degeneration, which remains the most severe and vision-threatening form of the disease. Pharmacological treatments are preferred due to their proven clinical efficacy, ability to slow disease progression, and suitability for long-term disease management. The increasing availability of branded biologics, biosimilars, and next-generation therapeutics with extended dosing intervals further supports segment leadership. In addition, rising diagnosis rates, improved patient awareness, and expanding access to ophthalmic care are increasing treatment volumes globally. Continuous pipeline activity focused on disease-modifying drugs for dry AMD, including complement inhibitors and gene-based therapies, is further strengthening the long-term growth outlook for the drugs segment.

By Route of Administration, Intravitreal Leads Due to Established Clinical Standard of Care

The intravitreal route of administration is projected to dominate the global macular degeneration treatment market in 2026, accounting for 59.70% of revenue. This leadership is driven by its status as the gold standard for the delivery of anti-VEGF therapies used in wet AMD treatment. Intravitreal injections enable direct drug delivery to the retina, ensuring high bioavailability, rapid therapeutic action, and improved clinical outcomes. Ophthalmologists globally rely on this route due to its well-established safety profile, predictable dosing, and compatibility with most approved biologics. High treatment adherence, repeat dosing requirements, and increasing patient volumes contribute to sustained utilization. Furthermore, technological advancements in injection techniques, needle design, and sustained-release intravitreal implants are enhancing patient comfort and procedural efficiency. As most late-stage and pipeline therapies continue to be designed for intravitreal delivery, this route remains central to clinical practice and market revenue generation.

By End User, Hospitals Lead Due to Advanced Ophthalmic Infrastructure and High Treatment Volumes

The hospitals segment is projected to dominate the global macular degeneration treatment market in 2026, accounting for 53.60% of revenue. Hospitals serve as the primary centers for AMD diagnosis, treatment initiation, and management of complex cases, particularly those requiring repeated intravitreal injections or surgical intervention. Availability of specialized ophthalmology departments, retinal imaging systems, and trained retinal specialists supports high patient throughput. Hospitals are also better equipped to manage elderly patients with comorbidities, which are common in AMD populations. In addition, hospitals benefit from structured reimbursement mechanisms, bulk drug procurement, and long-term supplier agreements with pharmaceutical manufacturers. Rising hospital admissions for vision-related disorders, increasing use of advanced imaging technologies such as OCT, and growing emphasis on early diagnosis are further reinforcing hospital dominance. Adoption of newer therapies and participation in clinical trials also contribute significantly to revenue concentration within hospital settings.

Region-wise Insights

North America Macular Degeneration Treatment Market Trends

North America is expected to dominate the global macular degeneration treatment market, with a 46.7% share in 2026, led primarily by the United States. The region benefits from a highly developed healthcare system, strong ophthalmology infrastructure, and widespread access to advanced diagnostic and therapeutic technologies. High prevalence of age-related macular degeneration, driven by an aging population and lifestyle-related risk factors, sustains consistent treatment demand. Early diagnosis through routine eye examinations and broad adoption of optical coherence tomography (OCT) enable timely treatment initiation. Favorable reimbursement policies for intravitreal injections and biologic therapies support high utilization of premium anti-VEGF drugs.

North America also demonstrates rapid uptake of innovative therapies, including long-acting formulations and next-generation biologics. The strong presence of leading pharmaceutical companies, an active clinical research environment, and early regulatory approvals further enhance market penetration. The growing adoption of home-based vision-monitoring tools and digital ophthalmology platforms is also supporting long-term market growth.

Europe Macular Degeneration Treatment Market Trends

The Europe macular degeneration treatment market is expected to grow steadily, supported by an expanding elderly population and increasing prevalence of chronic eye disorders. Countries such as Germany, the U.K., France, Italy, and the Nordic nations exhibit strong demand due to well-established public healthcare systems and broad access to ophthalmic services. Routine screening programs and increasing awareness of early vision loss are driving timely diagnosis and treatment initiation. Europe shows high adoption of anti-VEGF therapies, supported by national reimbursement schemes and standardized treatment protocols.

The region is also witnessing growing interest in biosimilars, which are improving treatment affordability and expanding patient access. Advancements in retinal imaging, coupled with the increasing availability of specialized retinal clinics, are strengthening treatment capacity. Regulatory support for innovative ophthalmic drugs and ongoing clinical research further contribute to market expansion. Additionally, gradual growth in outpatient and specialty eye clinics is supporting decentralized care delivery across the region.

Asia Pacific Macular Degeneration Treatment Market Trends

The Asia Pacific macular degeneration treatment market is expected to register a relatively high CAGR of around 8.7% between 2026 and 2033, driven by the rapid development of healthcare infrastructure and an aging population. Countries such as China, India, Japan, and South Korea are witnessing rising prevalence of AMD due to increased life expectancy and lifestyle transitions. Improving access to ophthalmic diagnostics, expanding private healthcare facilities, and rising awareness of vision-related disorders are accelerating diagnosis rates.

Government initiatives aimed at strengthening eye care services, increasing insurance coverage, and upgrading hospital infrastructure are further supporting market growth. Cost-sensitive markets are driving demand for affordable treatment options, including biosimilars and locally manufactured therapies. Increasing adoption of teleophthalmology, mobile screening units, and community-based eye care programs is expanding reach in underserved areas. Strategic expansion by global pharmaceutical companies and increased clinician training are strengthening long-term growth prospects across Asia Pacific.

Market Competitive Landscape

The global macular degeneration treatment market is highly competitive, with strong participation from companies such as F. Hoffmann-La Roche Ltd, Novartis AG, Regeneron Pharmaceuticals Inc., Bayer AG, and Bausch Health Companies Inc. These players leverage extensive global commercialization networks, strong brand equity, and sustained innovation across anti-VEGF biologics, combination therapies, drug-delivery platforms, and surgical solutions to address diverse clinical needs across dry and wet age-related macular degeneration.

Rising disease prevalence among the aging population, increasing treatment adherence, and growing demand for long-acting and less-frequent dosing regimens are driving portfolio expansion and pipeline activity. Market participants are increasingly prioritizing next-generation biologics, sustained-release delivery systems, gene therapies, and minimally invasive treatment approaches. Strategic focus areas include strengthening ophthalmology clinic and hospital partnerships, expanding access in emerging markets, and accelerating R&D investments to improve treatment durability, patient outcomes, and long-term market positioning.

Key Industry Developments:

- In January 2026, Ocugen, Inc. (NASDAQ: OCGN), a biotechnology leader in gene therapies for blindness, reported positive preliminary 12-month results (~50% patient data) from its Phase 2 ArMaDa trial of OCU410 (AAV5-RORA), a novel modifier gene therapy targeting geographic atrophy (GA) secondary to dry age-related macular degeneration (dAMD). Globally, dAMD affects 266 million people, with GA, its advanced stage, impacting roughly 2-3 million individuals in the U.S. and Europe.

- In July 2025, the U.S. FDA granted fast-track designation to SAR446597, a one-time intravitreal gene therapy for treating geographic atrophy (GA) caused by age-related macular degeneration (AMD). This designation is intended to accelerate the development and review of therapies for serious conditions with unmet medical needs, enabling patients to access promising new treatments sooner.

Companies Covered in Macular Degeneration Treatment Market

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Regeneron Pharmaceuticals Inc.

- Bayer AG

- Bausch Health Companies Inc.

- Alcon Inc.

- Apellis Pharmaceuticals Inc.

- Astellas Pharma Inc. (Iveric Bio)

- Samsung Bioepis

- REGENXBIO Inc.

- 4D Molecular Therapeutics

- Adverum Biotechnologies

- Ocular Therapeutix Inc.

- Others

Frequently Asked Questions

The global macular degeneration treatment market is projected to be valued at US$ 16.8 Bn in 2026.

The market is primarily driven by the rising prevalence of age-related macular degeneration due to global population ageing, increased healthcare expenditure, and continuous innovation in effective therapies and diagnostics.

The global macular degeneration treatment market is poised to witness a CAGR of 5.2% between 2026 and 2033.

Key opportunities include expansion into emerging markets with growing healthcare access, and development of long-acting therapies, advanced drug delivery systems, gene therapies, and personalized treatment solutions.

F. Hoffmann-La Roche Ltd, Novartis AG, Regeneron Pharmaceuticals Inc., Bayer AG, and Bausch Health Companies Inc are some of the key players in the macular degeneration treatment market.