- Medical Devices

- Lung Biopsy Systems Market

Lung Biopsy Systems Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Lung Biopsy Systems Market by Product (Core Needle Biopsy Devices, Fine Needle Aspiration Biopsy Devices, Surgical Biopsy Devices, and Vacuum-Assisted Biopsy Devices), by Procedure Type (Needle Biopsy, Thoracoscopic Biopsy, Transbronchial Biopsy, and Open Biopsy), by Application (Diagnosis of Lung Cancer, Assessment of Interstitial Lung Disease (ILD), Evaluation of Lung Infections, Assessment of Pulmonary Nodules & Masses, and Others) by End User (Hospitals, Cancer Research Centers, Specialty Clinics, and Others), and Regional Analysis from 2026 to 2033

Lung Biopsy Systems Market Share and Trends Analysis

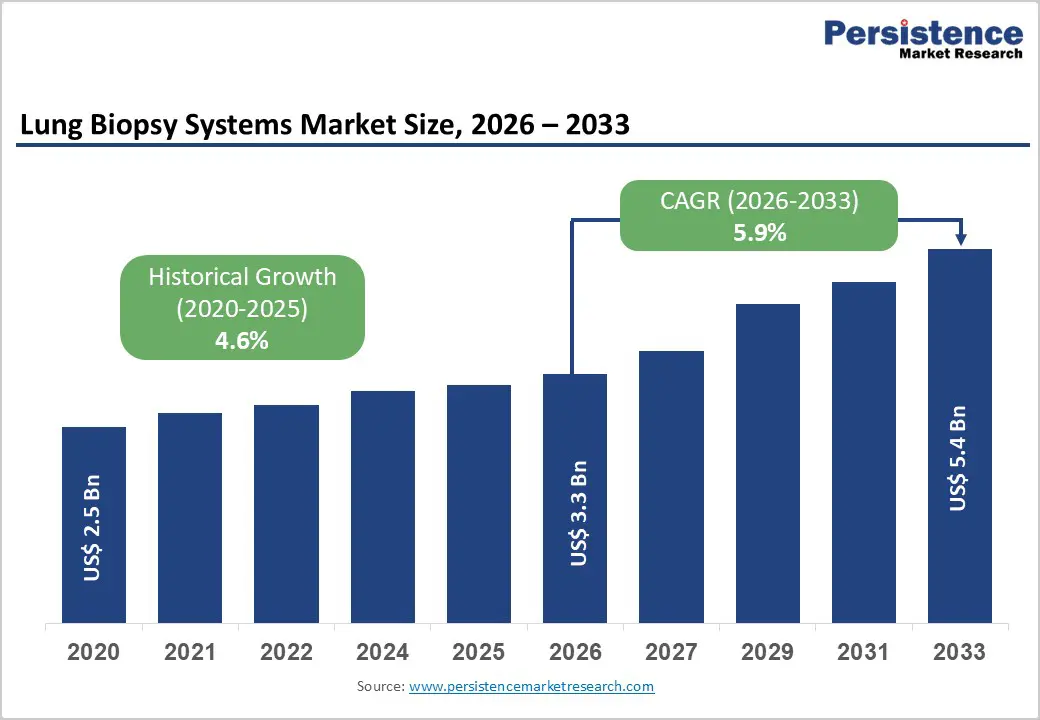

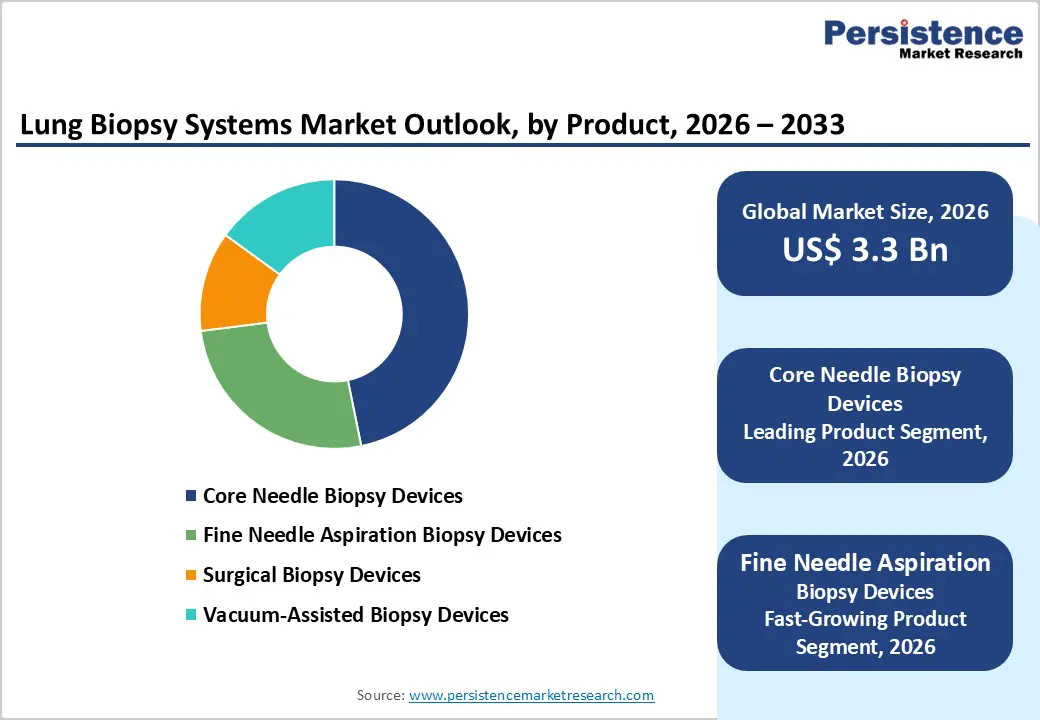

The global lung biopsy systems market size is estimated to grow from US$ 3.3 Bn in 2026 to US$ 5.4 Bn by 2033. The market is projected to record a CAGR of 5.9% during the forecast period from 2026 to 2033.

Global demand for lung biopsy systems is rising steadily, driven by the increasing incidence of pulmonary disorders such as lung cancer, interstitial lung disease, pulmonary infections, and undiagnosed lung nodules, along with a growing clinical shift toward minimally invasive and image-guided diagnostic procedures. Expanding use of lung biopsy systems across hospitals, specialty clinics, diagnostic centers, and ambulatory care settings is supporting sustained market growth. Higher volumes of screening-led diagnostic procedures, improved clinician awareness regarding early tissue confirmation, and rising patient preference for less invasive biopsy techniques are further accelerating adoption.

In addition, increasing healthcare expenditure and broader access to advanced imaging-guided biopsy technologies are enabling wider deployment across both developed and emerging markets. Continuous innovation in needle design, imaging integration, navigation accuracy, and procedural ergonomics is improving diagnostic yield, procedural safety, and workflow efficiency. The growing emphasis on outpatient-based diagnostics, point-of-care interventions, and digitally integrated clinical pathways is further propelling global demand for lung biopsy systems.

Key Industry Highlights

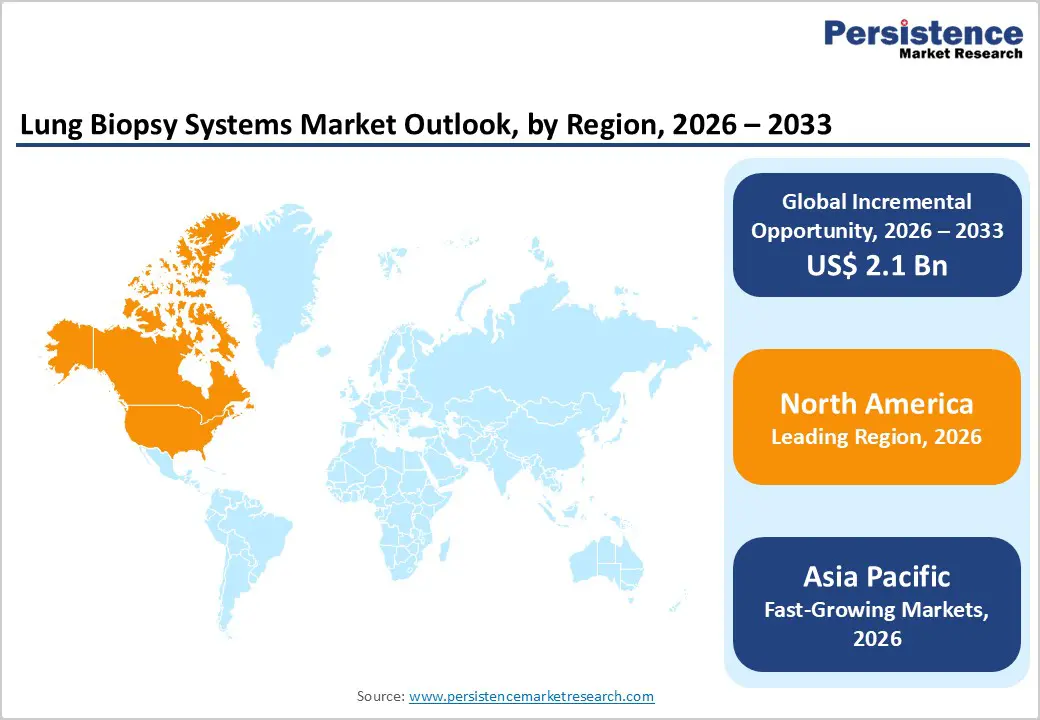

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, strong uptake of minimally invasive lung diagnostics, early adoption of image-guided and navigation-assisted biopsy technologies, and the presence of major medical device manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to large undiagnosed pulmonary patient populations, rapid growth of diagnostic and specialty centers, improving healthcare access, and increasing investments in outpatient and early cancer detection services.

- Leading Product Segment: Core needle biopsy devices dominate the market due to their high diagnostic accuracy, compatibility with image-guided procedures, and widespread use in routine and complex lung tissue sampling.

- Fastest-Growing Product Segment: Fine needle aspiration biopsy devices are expanding rapidly as demand grows for minimally invasive, point-of-care diagnostic solutions and outpatient-based pulmonary evaluations.

- Leading Application Segment: Diagnosis of lung cancer remains the top application, driven by high global disease prevalence and the critical role of biopsy in confirmation, staging, and treatment planning.

- Fastest-Growing Application Segment: Assessment of pulmonary nodules & masses is scaling quickly as lung cancer screening programs expand and clinicians increasingly rely on biopsy systems for early and accurate lesion characterization.

| Global Market Attributes | Key Insights |

|---|---|

| Lung Biopsy Systems Market Size (2026E) | US$ 3.3 Bn |

| Market Value Forecast (2033F) | US$ 5.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver - Rising Diagnostic Demand for Pulmonary Diseases and Shift Toward Less Invasive Tissue Sampling

Escalating incidence of pulmonary disorders is a major catalyst accelerating adoption of lung biopsy systems worldwide. Lung cancer, interstitial lung disease, pulmonary nodules, and chronic infections are being diagnosed at higher rates due to aging populations, smoking prevalence, air pollution, and improved screening programs. As clinical emphasis shifts toward early and accurate diagnosis, tissue confirmation has become essential for disease staging, treatment selection, and molecular profiling. Clinicians increasingly prefer minimally invasive biopsy techniques, such as image-guided core needle and transbronchial biopsies, due to reduced complication risk, faster recovery, and improved patient tolerance compared with open surgical approaches.

Advancements in imaging technologies, including CT, fluoroscopy, and ultrasound guidance, have significantly improved procedural accuracy and safety, encouraging wider clinical adoption. Improved needle designs, enhanced cutting mechanisms, and better lesion access enable higher diagnostic yield with fewer repeat procedures. Growing use of outpatient and same-day diagnostic workflows further supports demand, as minimally invasive lung biopsies reduce hospital stays and procedural burden. Increasing physician awareness, expanding lung cancer screening initiatives, and integration of biopsy procedures into standardized diagnostic algorithms continue to reinforce sustained growth in lung biopsy system utilization across healthcare settings.

Restraints - Cost Sensitivity, Technical Complexity, and Procedural Risk Considerations

The adoption of lung biopsy systems is constrained by economic and operational challenges. Advanced biopsy devices, particularly those compatible with high-end imaging platforms or robotic navigation systems, involve substantial upfront investment. This cost burden can limit procurement in smaller hospitals, ambulatory centers, and facilities in price-sensitive markets. In addition to capital costs, recurring expenses related to disposable biopsy needles, accessories, and imaging consumables increase the overall procedural cost, impacting budget allocation decisions.

Procedural complexity also remains a limiting factor. Lung biopsy requires skilled operators with expertise in imaging interpretation, lesion targeting, and complication management. Risks such as pneumothorax, bleeding, or inadequate tissue sampling necessitate careful patient selection and procedural planning. Limited availability of trained interventional pulmonologists or radiologists in certain regions restricts routine use, particularly outside tertiary care centers. Variability in reimbursement policies and lack of uniform coverage for advanced biopsy techniques further dampen adoption. In some healthcare systems, conservative clinical practices and preference for imaging surveillance over invasive confirmation delay biopsy utilization. These combined financial, technical, and regulatory barriers moderate market expansion despite rising diagnostic demand.

Opportunity - Growth of Image-Guided, Robotic, and Outpatient Lung Biopsy Solutions

Evolving diagnostic pathways are creating strong growth opportunities for lung biopsy systems. Increasing reliance on image-guided and navigation-assisted biopsy techniques enables accurate sampling of small, peripheral, and hard-to-reach lung lesions, expanding clinical applicability. Robotic-assisted and electromagnetic navigation platforms are gaining attention for their ability to improve reach, precision, and diagnostic confidence, particularly in early-stage lung cancer detection. Outpatient and ambulatory care expansion further enhances opportunity potential. Minimally invasive biopsy procedures that can be performed on a same-day basis align well with cost-containment strategies and patient-centric care models.

Growing adoption of lung cancer screening programs is generating higher volumes of indeterminate nodules, increasing demand for efficient biopsy confirmation. Emerging markets present untapped potential as healthcare infrastructure improves and access to advanced diagnostics expands. Technological innovation offers additional upside, with developments in needle flexibility, real-time imaging feedback, AI-assisted lesion targeting, and digital workflow integration improving procedural outcomes. Government initiatives supporting early cancer diagnosis, preventive healthcare, and minimally invasive interventions further strengthen the opportunity landscape. As clinicians prioritize precision diagnostics with reduced patient burden, advanced, efficient, and scalable lung biopsy solutions are well positioned for long-term growth.

Category-wise Analysis

By Product, Core Needle Biopsy Devices Lead Due to High Diagnostic Accuracy and Broad Clinical Adoption

The core needle biopsy devices segment is projected to dominate the global lung biopsy systems market in 2026, capturing a revenue share of 46.8%. This leadership is primarily driven by the high diagnostic yield and tissue adequacy offered by core needle biopsies, making them the preferred choice for definitive lung cancer diagnosis and histopathological evaluation. These devices are widely used across hospitals, specialty clinics, and diagnostic centers for both routine and complex pulmonary lesion sampling. Core needle systems enable precise tissue extraction under CT or ultrasound guidance, supporting accurate tumor typing and molecular testing. Their compatibility with minimally invasive, image-guided procedures enhances clinician confidence while reducing patient trauma and recovery time. Rising demand for early and accurate lung cancer detection, growth in outpatient diagnostic procedures, and increasing reliance on image-guided interventions further reinforce adoption. Continuous innovation in needle design, cutting mechanisms, ergonomic handling, and compatibility with advanced imaging platforms continues to support sustained leadership of this segment in global clinical practice.

By Application, Lung Cancer Diagnosis Dominates Due to High Disease Burden and Screening Uptake

The diagnosis of lung cancer segment is expected to lead the global lung biopsy systems market in 2026, accounting for a 48.0% revenue share. This dominance is driven by the high global incidence of lung cancer and the growing emphasis on early and accurate tissue diagnosis. Lung biopsy systems play a critical role in confirming malignancy, staging disease, and enabling biomarker and molecular testing for targeted therapies. Increased implementation of lung cancer screening programs, particularly among high-risk populations such as smokers and elderly patients, has significantly increased biopsy volumes. Image-guided core needle and transbronchial biopsy procedures are routinely used to evaluate pulmonary nodules and suspicious lesions detected during screening. Rising awareness among clinicians regarding precision oncology, along with advancements in minimally invasive biopsy techniques, has improved procedural safety and diagnostic confidence. Additionally, integration of biopsy workflows with digital pathology and oncology platforms supports faster clinical decision-making, reinforcing lung cancer diagnosis as the largest and most consistent application segment globally.

By End User, Hospitals Lead Due to Advanced Infrastructure and High Procedural Volumes

The hospitals segment is projected to dominate the global lung biopsy systems market in 2026, capturing a 49.6% revenue share. Hospitals remain the primary setting for lung biopsy procedures due to their access to advanced imaging infrastructure, multidisciplinary pulmonary teams, and trained interventional specialists. High patient inflow for suspected lung cancer, pulmonary nodules, and complex respiratory conditions results in consistently high procedure volumes. Hospitals are equipped to perform a full spectrum of biopsy techniques, including CT-guided, bronchoscopic, and surgical biopsies, supporting comprehensive diagnostic workflows. Long-term procurement contracts and centralized purchasing systems drive recurring demand for biopsy devices and consumables. Adoption is further strengthened by standardized clinical protocols, infection control policies, and the ability to manage procedure-related complications. Increasing hospital admissions for respiratory diseases, expansion of oncology departments, and growing investments in minimally invasive diagnostic technologies ensure hospitals maintain a dominant role in end-user adoption globally.

Region-wise Insights

North America Lung Biopsy Systems Market Trends

North America is expected to dominate the global lung biopsy systems market in 2026, accounting for a 46.7% value share, largely driven by the United States. The region benefits from a mature healthcare infrastructure, high concentration of pulmonologists and interventional radiologists, and widespread adoption of advanced diagnostic technologies. Strong emphasis on early cancer detection, supported by established lung cancer screening programs, significantly increases biopsy procedure volumes. Hospitals and diagnostic centers routinely utilize image-guided core needle and bronchoscopic biopsy systems for accurate tissue sampling and molecular testing. Favorable reimbursement policies for minimally invasive diagnostic procedures further encourage adoption across both inpatient and outpatient settings.

The presence of leading medical device manufacturers supports rapid commercialization of technologically advanced biopsy systems with improved precision and safety. Additionally, early adoption of digital pathology, AI-assisted imaging, and integrated diagnostic workflows enhances clinical efficiency. Ongoing clinician training programs, regulatory rigor, and continued investments in diagnostic innovation collectively sustain North America’s market leadership.

Europe Lung Biopsy Systems Market Trends

Europe’s lung biopsy systems market is expected to grow steadily in 2026, supported by rising prevalence of lung cancer, aging populations, and increasing focus on early diagnosis. Countries such as Germany, the U.K., France, Italy, and the Nordic region demonstrate strong adoption due to well-established healthcare systems and widespread access to advanced diagnostic services. Hospitals and specialty respiratory centers routinely perform lung biopsies for cancer diagnosis, interstitial lung disease evaluation, and pulmonary nodule assessment. Regulatory emphasis on patient safety and minimally invasive procedures supports the use of image-guided biopsy systems with lower complication rates. Europe is also witnessing gradual adoption of portable and workflow-efficient biopsy technologies that improve procedural turnaround times.

Technological advancements in imaging resolution, needle stability, and digital data integration enhance diagnostic confidence. Supportive reimbursement frameworks, standardized treatment guidelines, and expanding outpatient diagnostic services further facilitate market growth. Continuous investments in clinician education and diagnostic infrastructure reinforce stable and sustained adoption across the region.

Asia Pacific Lung Biopsy Systems Market Trends

The Asia Pacific lung biopsy systems market is projected to register a higher CAGR of around 8.0% between 2026 and 2033, driven by rapid expansion of healthcare infrastructure and rising diagnostic demand. Large patient populations in China, India, Japan, and South Korea, combined with increasing incidence of lung cancer and pulmonary disorders, are significantly boosting biopsy procedure volumes. Improved access to hospital-based diagnostics, expansion of private healthcare facilities, and growing awareness of early disease detection are accelerating adoption of minimally invasive lung biopsy systems.

Government initiatives aimed at strengthening healthcare delivery, expanding insurance coverage, and upgrading diagnostic capabilities further support market growth. Cost-sensitive markets are encouraging demand for affordable, portable, and efficient biopsy devices suitable for high-volume settings. Strategic expansion by global manufacturers, localization of production, and increased clinician training programs are improving device availability and expertise. Ongoing technological improvements in imaging guidance, procedural accuracy, and digital integration continue to enhance adoption across the region.

Market Competitive Landscape

The global lung biopsy systems market is highly competitive, with strong participation from FUJIFILM Corporation, DTR Medical Ltd, BD, Olympus Corporation, and Medtronic. These players leverage extensive global distribution networks, strong brand equity, and continuous innovation in biopsy needles, bronchoscopic platforms, imaging integration, navigation accuracy, and device ergonomics to address a wide range of pulmonary diagnostic applications.

Rising demand for minimally invasive diagnostic procedures, increasing prevalence of lung cancer and chronic respiratory disorders, and the shift toward early and precise tissue diagnosis are driving innovation. Manufacturers are focusing on advanced image-guided and robotic-assisted biopsy systems, improved sample yield, enhanced procedural safety, and digital workflow integration, while strengthening hospital collaborations, expanding in emerging markets, and sustaining R&D investments for accurate, efficient, and clinician-friendly biopsy solutions.

Key Industry Developments:

- In January 2026, Leadoptik, a developer of miniaturized imaging platforms for minimally invasive surgical applications, announced it had received FDA 510(k) clearance for its Last Inch Assessment (LIA) technology, an advanced imaging device designed to support lung biopsy procedures.

- In July 2025, Selio Medical, a Dublin-based EIT Health-supported start-up, received U.S. Food and Drug Administration (FDA) clearance for its novel device designed to enhance the safety of lung cancer diagnosis, with its Pre-B. Seal Lung Biopsy Plug System becoming the first FDA-cleared solution specifically indicated to reduce lung biopsy associated pneumothorax through a prophylactic pre-sealing approach.

- In October 2024, the U.S. Food and Drug Administration (FDA) granted Breakthrough Device designation to an AI-powered clinical decision support tool designed to assist lung cancer biopsy procedures. The designation recognizes the technology’s potential to significantly improve biopsy accuracy, lesion targeting, and procedural efficiency by leveraging advanced algorithms to support clinician decision-making during lung tissue sampling.

Companies Covered in Lung Biopsy Systems Market

- FUJIFILM Corporation

- DTR Medical Ltd

- BD

- Olympus Corporation

- Medtronic

- Hologic, Inc.

- B. Braun SE

- Cardinal Health

- Argon Medical Devices

- Cook

- Zimmer Biomet

- Teleflex Incorporated

- Johnson & Johnson

- Others

Frequently Asked Questions

The global lung biopsy systems market is projected to be valued at US$ 3.3 Bn in 2026.

Rising lung cancer incidence and growing adoption of minimally invasive, image-guided biopsy techniques are driving demand for lung biopsy systems.

The global lung biopsy systems market is poised to witness a CAGR of 5.9%between 2026 and 2033.

Expansion of robotic and AI-enabled biopsy technologies alongside growing adoption in emerging healthcare markets.

FUJIFILM Corporation, DTR Medical Ltd, BD, Olympus Corporation, and Medtronic are some of the key players in the lung biopsy systems market.