- Automotive Components & Materials

- Lightweight Automotive Body Panels Market

Lightweight Automotive Body Panels Market Size, Share, Trends, Regional Forecasts 2025 - 2032

Lightweight Automotive Body Panels Market By Material (Metal, Polymers & Composites), Composite (Bumper, Roof, Doors), Vehicle (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle), and Regional Analysis 2025 - 2032

Lightweight Automotive Body Panels Market Share and Trends Analysis

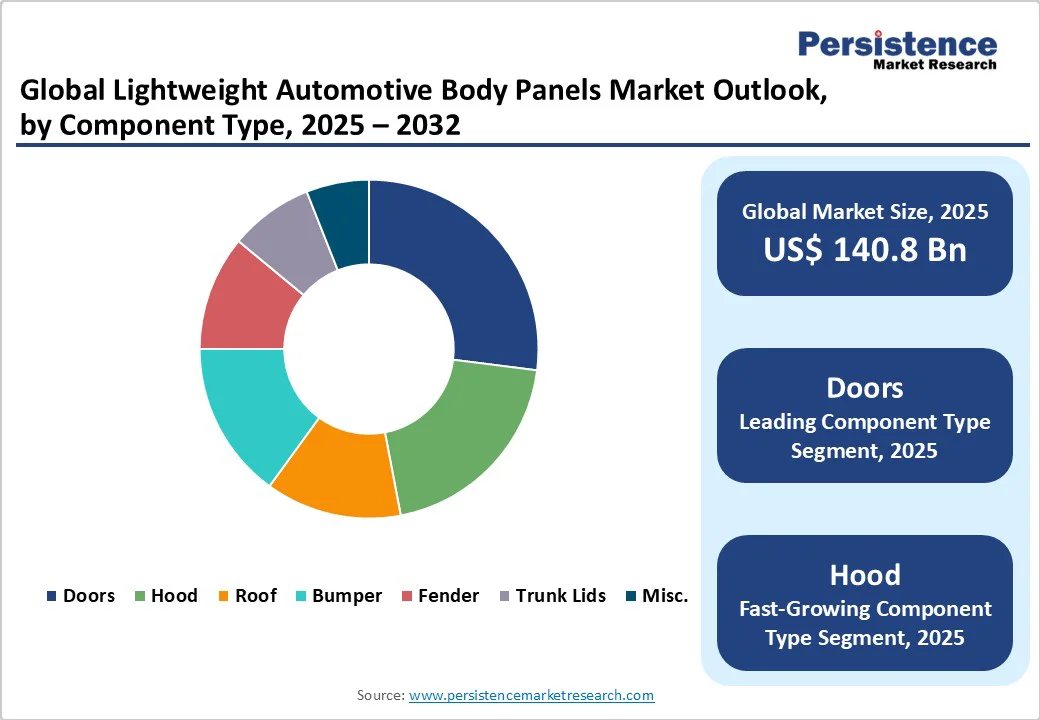

The global lightweight automotive body panels market size is likely to be valued at US$140.8 billion in 2025 and is projected to reach US$197.3 billion by 2032, growing at a CAGR of 4.9% between 2025 and 2032.

The market expansion is driven by stringent emission regulations compelling automakers to reduce vehicle weight for improved fuel efficiency. Rising electric vehicle adoption necessitates lightweight solutions to offset battery weight and extend driving range.

Advanced materials, including aluminum alloys, carbon fiber composites, and high-strength steel, enable manufacturers to achieve substantial weight reduction while maintaining structural integrity and safety standards.

Key Highlights Summary

- Leading Material Segment: Metals dominate with a 73% market share, driven by the adoption of aluminum; polymers & composites are the fastest-growing at a 5.2% CAGR.

- Vehicle Categories: Passenger vehicles lead with 56% market share; electric vehicles fastest-growing at 7.8% CAGR from battery weight offset requirements

- Component Leadership: Doors segment dominates with 27% share; hood segment fastest-growing at 5.9% CAGR from aerodynamic optimization needs

- Regional Distribution: Asia Pacific dominates with 41% market share; Europe shows a significant 5.2% CAGR; North America holds 21% share

- Regulatory Impact: EU CO2 emission targets require 15% reduction from 2025; US CAFE standards drive 6-8% fuel economy improvement from 10% weight reduction

- Strategic Developments: Major partnerships between OEMs and material suppliers; Gestamp revenue exceeds €10 billion; Plastic Omnium revenues exceed €8 billion.

| Key Insights | Details |

|---|---|

| Lightweight Automotive Body Panel Market Size (2025E) | US$140.8 billion |

| Market Value Forecast (2032F) | US$197.3 billion |

| Projected Growth CAGR (2025 - 2032) | 4.9% |

| Historical Market Growth (2019-2024) | 4.3% |

Market Dynamics Analysis

Drivers - Stringent Emission Regulations and Fuel Efficiency Standards

Government regulations worldwide are increasingly implementing stringent emission standards, compelling automakers to develop fuel-efficient and lightweight vehicles that comply with these regulations. The Corporate Average Fuel Economy (CAFE) standards and Euro 6 regulations have significantly boosted demand for lightweight body panels as manufacturers seek to meet prescribed emission targets.

According to the U.S. Department of Energy, a 10% reduction in vehicle weight can result in a 6%-8% fuel economy improvement, making lightweight panels crucial for achieving compliance with fuel efficiency mandates.

The European Union has set definitive targets to reduce CO2 emissions by 15% from 2025 onwards for cars and light commercial vehicles, with additional reductions required from 2035. These regulatory frameworks create compelling business cases for the adoption of lightweight materials, as manufacturers face substantial penalties for non-compliance with emission standards.

Rapid Electric Vehicle Market Growth and Battery Weight Offsetting

The global electric vehicle market's expansion represents a primary catalyst for the adoption of lightweight body panels, with over 13.7 million electric cars sold in 2023, marking a 33% increase from the previous year's 10.3 million units. Electric vehicles rely on heavy battery packs that add considerable weight, making weight reduction crucial for optimizing range and efficiency through the use of lightweight body panels.

Leading EV manufacturers, such as BYD and NIO, have incorporated aluminum-intensive platforms to improve energy efficiency and extend driving range. At the same time, Tesla utilizes carbon fiber components in its premium models. The necessity for lightweight solutions in EVs creates substantial market opportunities as battery technology continues to advance and EV adoption accelerates globally.

Restraints - High Material Costs and Manufacturing Complexity

The substantial costs associated with advanced lightweight materials pose significant barriers to market adoption, particularly for budget-conscious manufacturers and mainstream vehicle segments. Carbon fiber and aluminum materials command premium prices compared to traditional steel, with fluctuating raw material costs creating profitability challenges for manufacturers.

The high cost of research, development, and manufacturing of advanced lightweight panels requires substantial capital investments that many smaller manufacturers cannot afford. Integration complexities arising from the use of multiple lightweight materials from different suppliers can create potential compatibility issues and manufacturing challenges.

The specialized manufacturing processes required for advanced composites and aluminum components demand skilled labor and sophisticated equipment, increasing operational expenses.

Supply Chain Disruptions and Raw Material Volatility

The lightweight materials sector faces significant challenges from raw material price volatility affecting carbon fiber, magnesium, and aluminum, which compromises cost-effectiveness and discourages adoption among price-sensitive manufacturers. Supply chain disruptions caused by geopolitical tensions, trade restrictions, and raw material shortages impact manufacturing timelines and increase production costs.

Limited availability of certain high-strength materials restricts production capacities and hinders market growth, particularly in emerging markets where supply chains are less established. The complexity of lightweight material supply chains necessitates careful coordination among multiple suppliers, which can create potential bottlenecks and quality control challenges.

Counterfeit lightweight materials entering developing markets pose quality and safety risks that can undermine overall market development and consumer confidence.

Opportunities - Emerging Markets Expansion and Localized Manufacturing

Asia Pacific’s rapid industrialization and growing automotive production present substantial opportunities for lightweight body panel manufacturers to establish localized operations and capture market share. China's "Made in China 2025" initiative includes significant investment in advanced materials development, creating opportunities for lightweight material suppliers to participate in domestic manufacturing expansion.

India's Department of Science and Technology has launched collaborative projects to commercialize lightweight bio-composites derived from local materials such as jute and flax fibers, offering cost-effective alternatives for regional automakers.

The expansion of shared mobility services in the Asia Pacific markets creates demand for lightweight solutions that improve operational efficiency and reduce maintenance costs for fleet operators. Emerging markets offer opportunities for manufacturers to develop specialized lightweight solutions tailored to regional requirements and cost structures.

Advanced Materials Development and Sustainable Solutions

The development of bio-based polymers and recycled aluminum creates opportunities for manufacturers to address sustainability requirements while maintaining lightweight performance characteristics. Advancements in lightweight composite materials, including graphene-based nanomaterials, offer revolutionary potential for automotive structures, enabling unprecedented strength-to-weight ratios.

The integration of smart manufacturing technologies, including artificial intelligence and automation in lightweight panel production, enables cost optimization and quality improvements. 3D printing applications for lightweight automotive components offer opportunities for mass customization and reduced tooling costs, particularly for low-volume specialty vehicles.

The focus on circular economy principles creates market opportunities for developing recyclable, lightweight materials that align with the automotive industry's sustainability goals.

Electric and Autonomous Vehicle Integration Opportunities

The convergence of electric and autonomous vehicle technologies creates specialized opportunities for lightweight body panels that integrate sensors, communication equipment, and aerodynamic optimization features. Connected vehicle technologies require lightweight housing solutions for electronic components, creating new market segments for specialized lightweight panels.

The development of vehicle-to-vehicle communication systems necessitates lightweight antenna integration and electromagnetic shielding solutions built into body panels. Autonomous vehicle platforms require lightweight structural solutions that accommodate advanced sensor arrays while maintaining crash safety performance.

The expansion of mobility-as-a-service platforms creates demand for durable, lightweight solutions designed for high-utilization commercial applications.

Segmentation Analysis

Material Type Analysis

The metals segment dominates the lightweight automotive body panels market with a 73% market share in 2025, driven by aluminum's proven performance characteristics, established manufacturing infrastructure, and cost-effectiveness compared to advanced composites.

Aluminum alloys offer superior strength-to-weight ratios, corrosion resistance, and recyclability, making them attractive for high-volume automotive applications, including body panels, chassis components, and engine blocks. The automotive industry's average aluminum content per vehicle continues growing steadily as manufacturers leverage aluminum's lightweight benefits while maintaining structural integrity and crash safety performance.

The polymers and composites segment represents the fastest-growing category, with a CAGR of 5.2%, driven by technological advancements in carbon fiber-reinforced plastics (CFRP) and glass fiber-reinforced plastics (GFRP), which offer exceptional strength-to-weight performance.

Carbon fiber composites provide five times the strength of steel while weighing significantly less, making them increasingly viable for premium and performance vehicle applications. The segment benefits from declining production costs, improved manufacturing processes, and expanding applications in electric vehicles, where weight reduction directly impacts battery efficiency and driving range.

Vehicle Type Analysis

The passenger vehicle segment maintains market leadership with a 56% share in 2025, supported by large production volumes, consumer demand for fuel efficiency, and regulatory compliance requirements driving lightweight panel adoption across mainstream automotive categories.

The segment encompasses compact cars, midsize sedans, SUVs, and luxury vehicles, each with specific lightweight requirements driven by performance expectations and regulatory standards. Major automotive manufacturers, including Toyota, Honda, and Volkswagen, have accelerated the integration of lightweight panels across passenger vehicle platforms to meet stringent emission regulations and consumer expectations for efficiency.

The electric vehicle segment exhibits a positive CAGR, driven by the critical need to offset heavy battery pack weight and maximize driving range through comprehensive weight reduction strategies. Electric vehicle manufacturers extensively utilize lightweight body panels to counterbalance battery weight, with leading companies such as Tesla, BYD, and NIO incorporating aluminum-intensive platforms and carbon fiber components.

The segment benefits from rapid expansion of the EV market, government incentives promoting electric mobility, and technological advancements in battery technology, which increase the importance of vehicle weight optimization.

Component Type Analysis

The doors segment dominates the component type category with a 27% share in 2025, driven by the large surface area, structural importance, and safety requirements that make doors prime candidates for lightweight material integration.

Door panels offer substantial weight reduction opportunities through the substitution of aluminum and composite materials, while maintaining crash safety performance and integrating advanced features such as window regulators and locking mechanisms. The segment benefits from established manufacturing processes, proven safety performance, and cost-effective integration into existing vehicle platforms.

The hood segment represents the fast-growing component category, driven by aerodynamic optimization requirements, engine bay heat management, and pedestrian protection regulations that favor lightweight construction.

Hood applications offer ideal opportunities for the adoption of lightweight materials due to non-structural requirements that prioritize weight reduction over load-bearing capacity. The segment benefits from aesthetic design flexibility, easier manufacturing integration, and consumer acceptance of premium lightweight materials in visible exterior components.

Regional Market Insights

North America Lightweight Body Panels Market Trends

North America maintains a significant market position with a 21% share of the global lightweight automotive body panels market, driven by stringent CAFE standards, established automotive manufacturing infrastructure, and strong research and development capabilities. The United States market is projected to grow significantly, with a dominant presence in North America, supported by increasing fuel efficiency regulations and the adoption of electric vehicles.

Regional growth drivers include the prevalence of pickup trucks and SUVs, which benefit significantly from weight reduction; government initiatives promoting clean vehicle technologies; and the strong presence of leading automotive manufacturers and suppliers. The region's mature automotive industry offers established supply chains and manufacturing expertise for integrating lightweight materials.

Major automotive OEMs, including Ford, General Motors, and Stellantis, are utilizing lightweight body panels to meet Corporate Average Fuel Economy (CAFE) standards while preserving vehicle performance and safety characteristics. The region benefits from advanced manufacturing technologies, established aluminum and composite material supply chains, and consumer acceptance of premium lightweight solutions in high-value vehicle segments.

Europe Lightweight Body Panels Market Trends

Europe demonstrates significant market importance with a robust CAGR of 5.2%, driven by the European Union's stringent CO2 emission targets requiring a 15% reduction from 2025 onwards and additional reductions from 2035 for passenger cars and light commercial vehicles.

The region's advanced automotive manufacturing capabilities in Germany, France, and the United Kingdom support the integration of sophisticated lightweight materials across both premium and volume vehicle segments. European automakers, including BMW, Mercedes-Benz, Audi, and Volkswagen Group, lead global lightweight technology development through extensive research and development investments and strategic partnerships with material suppliers.

Regional competitive advantages include established relationships between automotive OEMs and lightweight material suppliers, supportive government policies promoting sustainable mobility, and consumer willingness to pay premiums for advanced lightweight technologies. The region's focus on premium vehicle segments drives demand for sophisticated lightweight solutions, including carbon fiber and advanced aluminum alloys.

Asia Pacific Lightweight Body Panels Market Trends

Asia Pacific dominates the global market with the largest 41% market share, driven by massive automotive production volumes in China, Japan, South Korea, and India, combined with rapid electric vehicle adoption and government support for clean mobility initiatives.

China leads regional growth with a 38.5% share of Asia Pacific demand, supported by over 9 million electric vehicles produced in 2023 and substantial government investments in advanced materials research through initiatives like "Made in China 2025". The region benefits from cost-effective manufacturing capabilities, large consumer markets, and established supply chains for lightweight materials, including aluminum and composites.

India demonstrates strong growth potential with a 6.3% CAGR, driven by expanding vehicle manufacturing, export growth, and the localization of lightweight material supply chains to support domestic automotive production.

Regional manufacturers, including BYD, NIO, and traditional automakers such as Toyota and Honda, are accelerating the integration of lightweight panels to meet emission regulations and enhance vehicle competitiveness in global markets. The region's competitive advantages include manufacturing cost efficiency, technological innovation capabilities, and proximity to raw material sources for the production of lightweight materials.

Competitive Landscape

The global lightweight automotive body panels market is moderately consolidated, with key players such as Magna International, Gestamp, Plastic Omnium, ThyssenKrupp AG, and Alcoa Corporation holding significant market shares. These companies leverage comprehensive product portfolios, advanced manufacturing capabilities, and strategic partnerships with OEMs.

The competitive landscape comprises both traditional suppliers and specialized firms that specialize in lightweight materials, driving dynamic competition. Market leaders leverage robust R&D capabilities and established OEM relationships to sustain their competitive edge.

Strategic Developments

Magna International has enhanced its lightweight body panel capabilities through acquisitions and partnerships, focusing on aluminum and composites for electric vehicles in 2024. Plastic Omnium reported over €8 billion in revenues, investing in sustainable manufacturing for lightweight components. Gestamp surpassed €10 billion in annual sales by developing specialized lightweight solutions for EV platforms.

Strategic collaborations between OEMs and material suppliers have accelerated the development of innovative lightweight solutions. Teijin Limited and Toray Industries have expanded their positions in carbon fiber composites through investments in automotive applications. Additionally, advanced manufacturing partnerships in 3D printing are enabling efficient panel fabrication for specialized uses.

Key Developments

- In April 2024, Toray Industries and Hyundai Motor Group announced a long-term strategic partnership for joint R&D of lightweight carbon-fiber and composite materials. The alliance targets advanced, high-strength components for next-generation EVs (from chassis and body panels to battery and motor structures), combining Toray’s composite expertise with Hyundai’s vehicle design.

- In August 2022, Plastic Omnium finalized the €52.5 million acquisition of ACTIA Group’s Power division (100% stake), bolstering its energy-management portfolio and enhancing its EV body-panel integration capabilities.

- In February 2022, Teijin Automotive Technologies began commercial operation of a new 39,000 m² composites plant in Changzhou (Jiangsu, China). They announced construction of a third plant in Shenyang to dramatically expand its production of lightweight composite panels and EV components for Chinese automakers.

Companies Covered in Lightweight Automotive Body Panels Market

- Magna International Inc.

- Gestamp

- Plastic Omnium

- ThyssenKrupp AG

- Alcoa Corporation

- Gordon Auto Body Parts Co. Ltd

- Austem Company Ltd

- Flex-N-Gate Corporation

- KUANTE Auto Parts Manufacture

- Changshu Huiyi Mechanical & Electrical

- ABC Group Inc

- Hwashin

- Stick Industry Co. Ltd

- Teijin Limited

- Toray Industries

Frequently Asked Questions

The lightweight automotive body panels market is set to reach US$ 140.8 Bn in 2025.

The growth is driven by strict emission regulations, increasing electric vehicle adoption for weight reduction, and advancements in materials science for better performance and efficiency.

The industry is estimated to rise at a CAGR of 4.9% from 2025 to 2032.

Key market opportunities exist in emerging markets with localized manufacturing, innovations in sustainable materials such as bio-based polymers, and the integration of lightweight panels in electric and autonomous vehicle platforms.

The major players dominating the global Lightweight Automotive Body Panels Market are Magna International Inc., Gestamp, Plastic Omnium, ThyssenKrupp AG, Alcoa Corporation, Gordon Auto Body Parts Co., Ltd.