- Processed Food

- Ketchup Market

Ketchup Market Size, Share, and Growth Forecast, 2025 - 2032

Ketchup Market By Product Type (Regular, Flavored), Nature (Organic, Conventional), Packaging (PET/Glass Bottles, Pouch and Sachet), Distribution Channel (On Trade, Off Trade), and Regional Analysis for 2025 - 2032

Ketchup Market Size and Trends Analysis

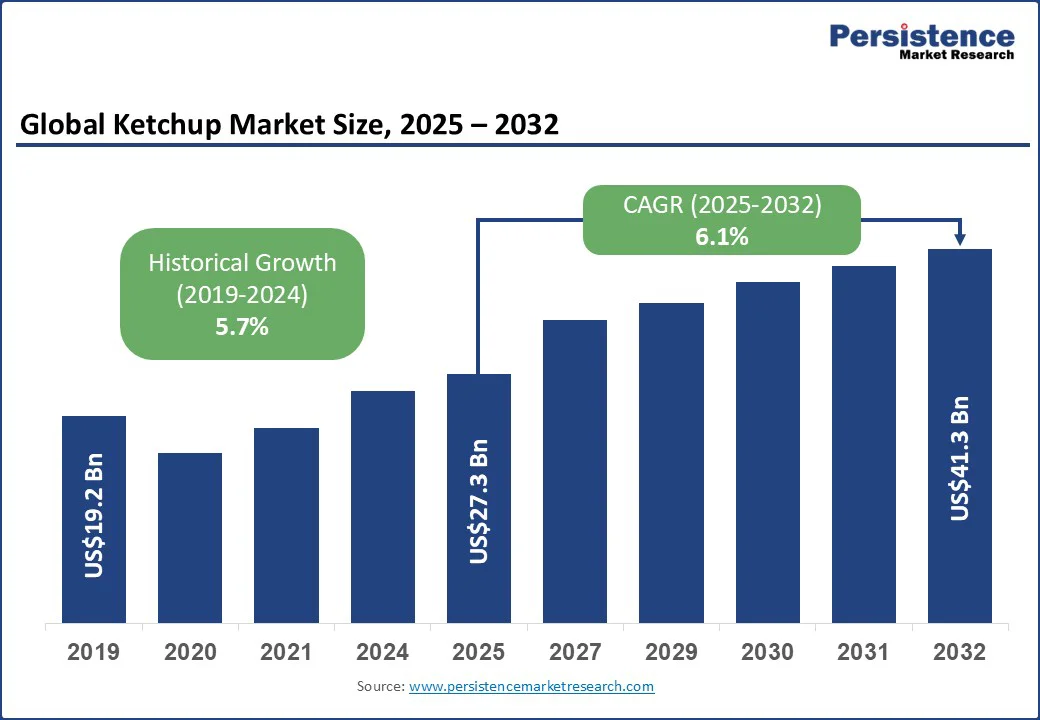

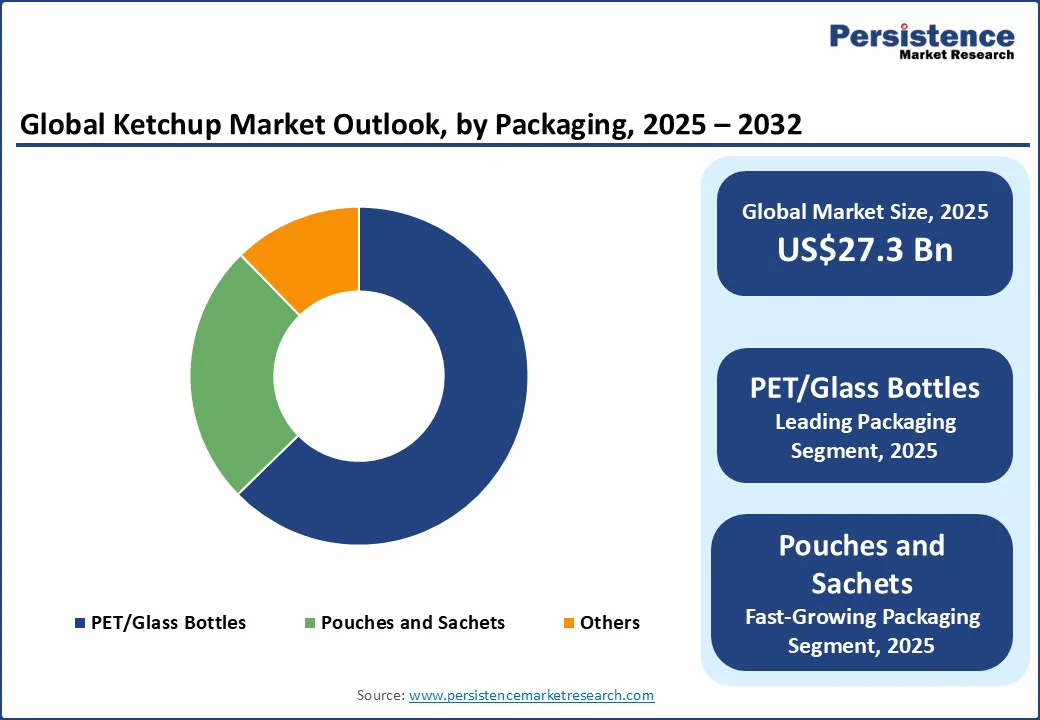

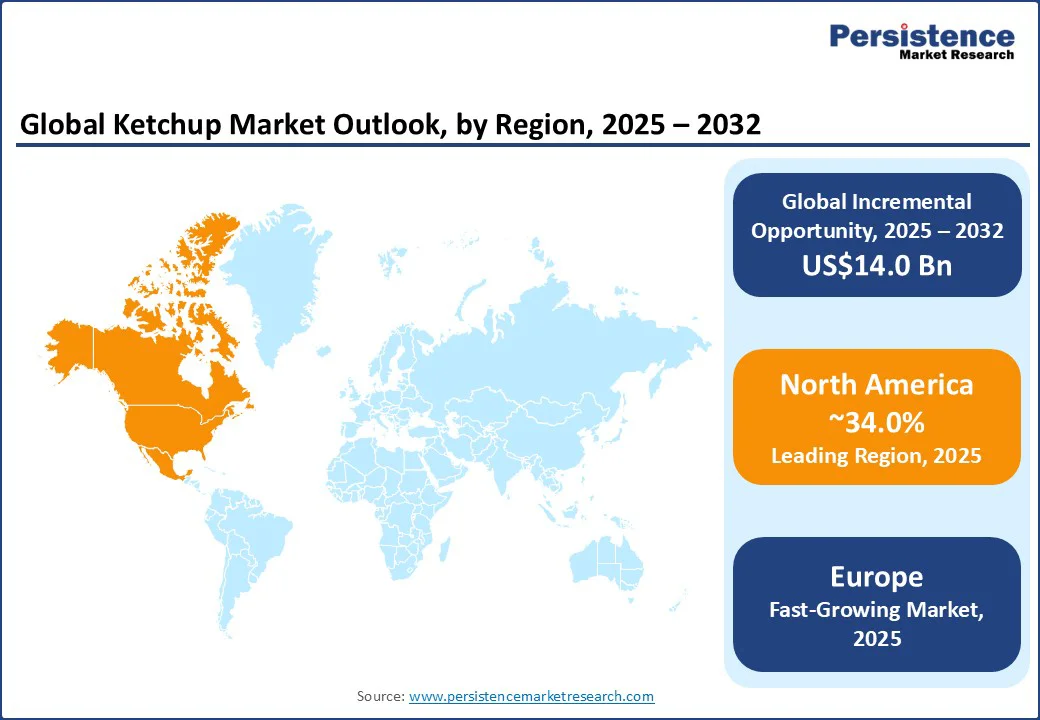

The global ketchup market size is likely to be valued at US$ 27.3 Bn in 2025 and is estimated to reach US$ 41.3 Bn in 2032, growing at a CAGR of 6.1% during the forecast period 2025 - 2032, fueled by increasing consumption of processed and convenience food, rising penetration of flavored condiments, and surging demand for sustainable packaging formats worldwide.

Key Industry Highlights:

- New Product Launch: Granos launched Granos Better Ketchup in April 2025. It is a sugar-free ketchup sweetened with jaggery. It exhibits the company’s commitment to providing healthy and preservative-free products that appeal to the evolving requirements of health-conscious consumers.

- Leading Product Type: Regular ketchup holds nearly 72.5% share in 2025, owing to its familiar taste, affordability, and wide availability.

- Key Nature: Conventional, with around 84.2% share in 2025, spurred by established consumer trust, low price points, and mass retail presence.

- Dominant Packaging: PET/glass bottles, approximately 62.7% of the ketchup market share in 2025, backed by their ability to provide squeezability and premium appeal.

- Leading Region: North America, with about 34.0% share in 2025, due to high per capita consumption and a well-established fast-food culture.

- Fastest-growing Region: Europe, approximately 29.0% share in 2025, boosted by rising preference for clean-label and locally sourced condiments.

| Key Insights | Details |

|---|---|

| Ketchup Market Size (2025E) | US$27.3 Bn |

| Market Value Forecast (2032F) | US$41.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Convenience Food Items

The global consumption of packaged and ready-to-eat meals has increased substantially. According to Johns Hopkins Bloomberg School of Public Health, in the U.S., ultra-processed food comprised more than half of all calories consumed at home, rising from 51% in 2003 to 54% in 2018. About one-third of all calories were consumed outside the home.

The proportion of total calories from minimally processed food fell nearly five percentage points from 33.2% in 2003 to 28.5% in 2018.

Ketchup, being a versatile condiment, benefits directly from this shift. As per the Agricultural Marketing Resource Center, per capita processed tomato consumption was 73.3 pounds in 2023, highlighting ketchup’s role in fast food and home-cooked meals. This trend ensures sustained demand for regular ketchup, particularly through fast-food chains and Quick Service Restaurants (QSRs).

Ongoing Shift toward Health-conscious and Organic Products

The International Federation of Organic Agriculture Movements (IFOAM) reported that global organic food and drink sales reached approximately €136.4 Bn in 2023. While some national markets, such as the U.S. and parts of Europe, reported growth rates above 7% annually, the total global market growth rate was lower and varied by region.

Organic ketchup is increasingly popular among health-conscious consumers who are avoiding synthetic additives and high fructose corn syrup. According to Statistics Denmark, Denmark's organic market share of retail trade was 11.6% in 2024, a figure consistently among the highest in Europe. It is driving premiumization in ketchup ranges. This structural trend supports the growth of the organic ketchup segment, though conventional ketchup retains market dominance.

Packaging Developments Propelling Retail Penetration

Consumer preferences for easy-to-use, resealable, and lightweight packaging are influencing ketchup sales. Pouches and sachets are among the fastest-growing packaging formats in the global sauces, dressings, and condiments market, with pouches capturing approximately 45% of the flexible packaging segment in 2024.

The sachet/pouch format is gaining impetus in single-serve, foodservice, and takeaway channels. This is attributed to surging consumer preference for convenience and portion control. Similarly, PET bottles dominate due to durability and recyclability. These developments improve shelf visibility and consumer convenience, directly contributing to wide adoption across both off-trade and on-trade channels.

Volatility in Raw Material Prices

Tomatoes account for nearly 80% of ketchup’s raw material costs. Climate change-induced supply disruptions have resulted in fluctuations in tomato production, with the World Tomato Processing Council (WTPC) predicting a 14% year-on-year decline in Europe's processing tomato output for 2022, due to adverse weather conditions. This volatility increases input costs, pressuring margins and retail prices.

Prolonged disruptions are anticipated to limit affordability and restrain demand in price-sensitive markets.

Regulatory and Health Concerns over Sugar Content

The World Health Organization (WHO) recommends limiting added sugar intake to less than 10% of daily calories. However, traditional ketchup formulations often contain 20 to 25% sugar content. Several governments, including the U.K. and Mexico, have introduced sugar taxes on processed food since 2020. Such measures directly impact ketchup producers, compelling reformulation and increasing compliance costs.

Expansion in Emerging Economies

Asia Pacific’s rising middle-class population is influencing condiment consumption. A World Economic Forum report from 2021 projected that more than 1 billion Asians would join the global middle class by 2030, pushed by China and India.

Increasing QSR penetration in India, where the fast-food industry is expanding at 15% annually, creates high demand for ketchup. This represents an opportunity exceeding US$5 Bn in incremental sales by 2032 across the region.

Flavored and Premium Product Launches

Global consumers are diversifying their palates, favoring flavored ketchups infused with chili, garlic, and exotic spices. A new study reported that flavored condiments grew 11% year-over-year in 2023, outpacing regular variants.

Premiumization is specifically strong in Europe, where gourmet sauces represent 18% of condiment revenues. Ketchup manufacturers launching regional flavors stand to capture younger, urban consumers and extend beyond traditional use cases.

Sustainability and Eco-friendly Packaging

Consumers increasingly prioritize sustainable packaging, with a 2023 survey noting that 55% of global consumers are willing to pay more for eco-friendly packaging. Companies adopting recyclable PET bottles, biodegradable sachets, and refill packs can help brands differentiate themselves in competitive markets. This shift presents opportunities for ketchup producers to comply with retailer sustainability commitments and regulatory mandates in Europe and North America.

Category-wise Analysis

Product Type Insights

Regular ketchup dominates the category with nearly 72.5% market share in 2025. Its widespread use in households, QSRs, and institutional food services strengthens its leadership. Regular ketchup remains a low-cost condiment, catering to mass consumers and fast-food operators worldwide.

Flavored ketchup is the fastest-growing segment, expanding at over 7.3% CAGR from 2025 to 2032. Growth stems from rising consumer experimentation, particularly in Asia Pacific and Europe, where chili-infused and spice-based variants are gaining popularity. Premium positioning and limited-edition launches further boost segment traction.

Nature Insights

Conventional ketchup holds approximately 84.2% share in 2025, spurred by cost competitiveness and established retail distribution. The category benefits from bulk demand in institutional kitchens and fast-food chains, where price sensitivity outweighs organic preferences.

Conversely, organic ketchup is poised to record the fastest CAGR of 8.4% during the forecast period. Rising health awareness and regulatory pushes for reduced chemical use in agriculture encourage organic adoption. The segment is mainly growing in Europe and North America, where clean-label trends dominate consumer choices.

Packaging Insights

PET and glass bottles remain the leading packaging format with about 62.7% share in 2025. Their durability, recyclability, and convenience make them the preferred choice for households and retail shelves. Glass bottles, while premium, dominate traditional markets in Europe.

Pouches and sachets are projected to rise at a 7.6% CAGR through 2032, driven by affordability and portability. Single-serve sachets are widely adopted in QSRs, airlines, and institutional catering, primarily in Asia Pacific and Africa. This format also complies with the trend toward portion control and reduced food waste.

Regional Insights

North America Ketchup Market Trends - Strong Fast-food Culture and Sustainable Packaging Investments Propel Growth

North America accounts for nearly 34.0% of the ketchup market in 2025, led by the U.S. Robust fast-food penetration, high per-capita consumption, and development in reduced-sugar formulations propel demand. Regulatory frameworks, including the Food and Drug Administration’s (FDA) labeling mandates, ensure transparency in nutritional information.

Investments in recyclable PET packaging are skyrocketing, with companies such as Kraft Heinz committing US$100 Mn for sustainable packaging development since 2023. Canada’s rising preference for organic ketchup adds further momentum. The region’s consolidated market structure favors large multinational players.

Europe Ketchup Market Trends - Sugar Tax-driven Reformulations and Premium Organic Focus Boost Sales

Europe represents 29.0% of global ketchup revenues in 2025, with Germany, the U.K., and France leading consumption. Regulatory harmonization under the EU Food Safety Authority supports market stability, while sugar tax regimes in the U.K. and Spain encourage reformulation.

Development in organic and gourmet ketchups is rising, reflecting Europe’s premiumization trend. Investments in eco-friendly glass packaging also cater to EU circular economy goals. Local players in Italy and Spain emphasize tomato authenticity, strengthening regional identity. Europe, hence remains the global leader in organic ketchup adoption.

Asia Pacific Ketchup Market Trends - Expansion of QSRs and Affordable Sachet Packaging Augment Demand

Asia Pacific is the fastest-growing regional market, expanding at around 7.4% CAGR from 2025 to 2032. Rising disposable income, urbanization, and a surge in QSRs across China, India, and ASEAN countries are propelling ketchup demand. China dominates regional consumption, while India is witnessing growing ketchup adoption in Tier-2 and Tier-3 cities.

Regulatory reforms promoting food safety standards and local tomato cultivation further support industry scalability. Packaging innovations such as low-cost sachets ensure affordability in rural areas. The region is emerging as a manufacturing hub due to low-cost tomato production and expanding supply chain infrastructure.

Competitive Landscape

The global ketchup market is moderately consolidated, with global leaders such as Kraft Heinz, Unilever, and Nestlé accounting for over 45% of global revenues in 2025. Regional and private-label players maintain a strong presence in price-sensitive markets, including India and Latin America. Competitive positioning revolves around product development, brand equity, and distribution reach.

Key Industry Developments

- In June 2025, Heinz launched a new tomato ketchup with no added sugar or salt in the U.K. The latest Tomato Ketchup Zero includes 35% more tomato than the original product and was made to cater to the rising demand for healthy options in the country.

- In May 2025, Thomas Biotech & Cytobacts Center for Biosciences (OPC) Pvt. Ltd. developed Papchup, a new papaya-based ketchup to help papaya farmers get better prices for their crop. Papchup contains 50% papaya pulp, compared to many tomato ketchups on the market, which contain around 12% to 18% tomato paste.

Business Strategies

Leading companies emphasize innovation in flavors, sustainable packaging, and regional expansion. Differentiation is achieved through clean-label positioning, cost leadership in conventional segments, and premiumization in developed markets. Private-label penetration intensifies price competition.

Companies Covered in Ketchup Market

- The Kraft Heinz Company

- Del Monte Foods Holdings Ltd.

- Conagra Brands Inc.

- Nestle S.A.

- Unilever PLC

- McCormick & Company Inc.

- Wingreens Farms Pvt. Ltd.

- General Mills Inc.

- Campbell Soup Company

- Kagome Co., Ltd.

- The Foraging Fox Ltd.

- Mars Inc.

- Organicville Foods

- Mutti S.p.A.

- Premier Foods plc

- Masan Group

- Tata Consumer Products

- Hain Celestial Group Inc.

Frequently Asked Questions

The ketchup market is projected to reach US$27.3 Bn in 2025.

Rising demand for ready-to-use condiments and fast-food expansion globally are the key market drivers.

The ketchup market is poised to witness a CAGR of 6.1% from 2025 to 2032.

Emergence of plant-based formulations and high demand for gourmet ketchup lines are the key market opportunities.

The Kraft Heinz Company, Del Monte Foods Holdings Ltd., and Conagra Brands Inc. are a few key market players.