- Home Care & Utilities

- Jewelry Boxes & Organizers Market

Jewelry Boxes & Organizers Market Size, Share and Growth Forecast, 2026-2033

Jewelry Boxes & Organizers Market by Product Type (Jewelry Boxes, Jewelry Organizers, Travel & Portable Cases, Watch Boxes & Cases, Wall-Mounted Organizers, Display & Retail Cases, Others), Material (Wood, Leather, Metal, Glass, Plastic, Fabric & Textile, Eco & Sustainable Materials, Composite), Distribution Channel (Online E-Commerce, Specialty Stores & Boutiques, Hypermarkets, Omni-Channel, B2B), and Regional Analysis for 2026-2033

Jewelry Boxes & Organizers Market Share and Trends Analysis

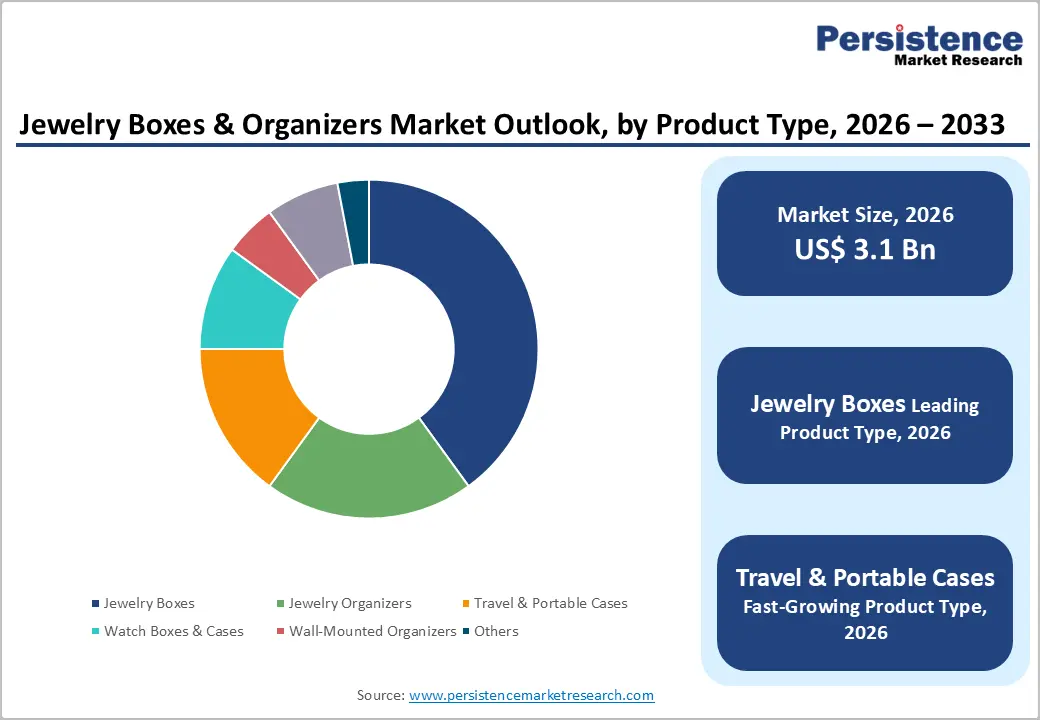

The global jewelry boxes & organizers market size is likely to be valued at US$ 3.1 billion in 2026, and is projected to reach US$ 4.6 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026-2033. Market growth is being supported by rising global jewelry ownership, increasing focus on urban household storage optimization, and sustained demand from premium gifting, fashion accessories, and organized retail channels. The continued expansion of e-commerce platforms for furniture and home organization is strengthening product accessibility and assortment depth, while the premiumization of lifestyle storage solutions is steadily raising average selling prices across mass premium and luxury tiers.

From a demand perspective, favorable demographic shifts are continuing to shape purchasing behavior, particularly among working women, urban millennials, and luxury watch collectors who are prioritizing aesthetics, functionality, and product durability. Sustainability is increasingly influencing material selection, with manufacturers adopting responsibly sourced wood, recycled composites, and low-impact packaging to align with evolving consumer expectations. At the same time, modular and customizable design formats are gaining traction as buyers seek flexible storage solutions that adapt to growing collections and limited living spaces.

Key Industry Highlights

- Dominant Product: Jewelry boxes are expected to lead with 40% market share in 2026, supported by gifting and premium household demand, while travel & portable cases are projected to grow fastest at a 7.5% CAGR through 2033, driven by mobility and urban living trends.

- Leading Material: Wood and leather are anticipated to dominate with a 42% share in 2026, reflecting premium appeal and durability, whereas eco-friendly materials are set to be the fastest-growing at an 8.2% CAGR through 2033, supported by sustainability regulations and consumer preferences.

- Dominant Distribution Channel: Specialty stores and boutiques are likely to hold a 36% share in 2026 due to the strength of experiential retail, while online e-commerce is expected to expand the fastest through 2033, driven by the growing adoption of direct-to-business (D2C) models.

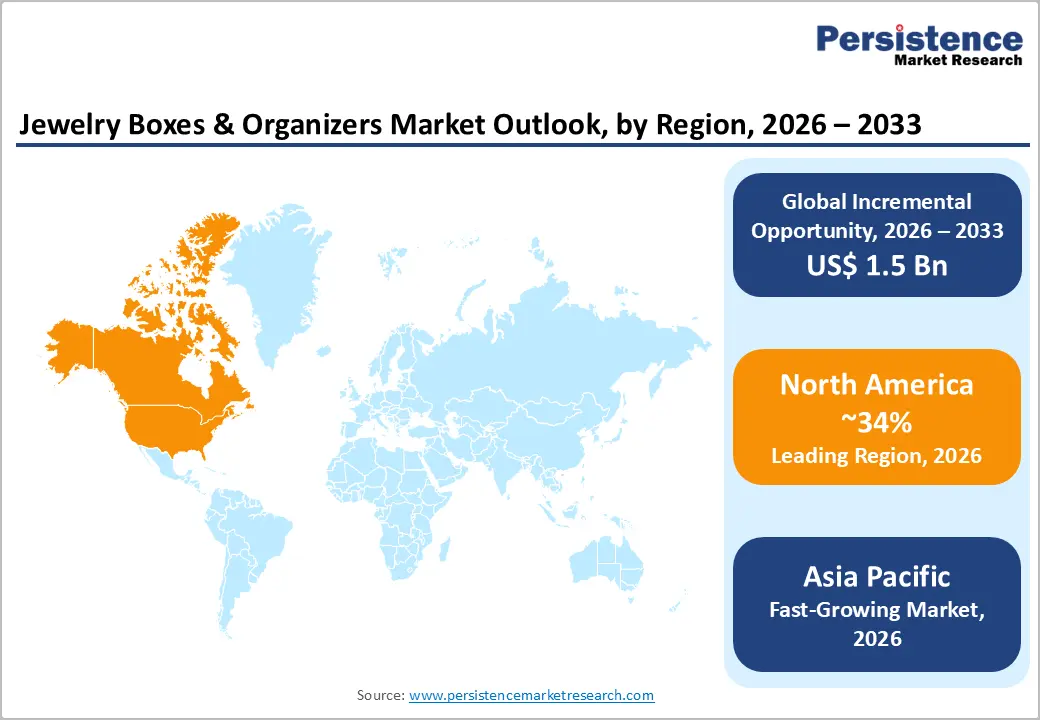

- Regional Leadership: North America is expected to lead with about 34% share in 2026, owing to premium spending capacity, while Asia Pacific is projected to be the fastest-growing market at 7% CAGR through 2033, fueled by a strong cultural alignment with jewelry ownership.

- Competitive Environment: Competitive dynamics are shaped by premiumization and sustainability, with players focusing on certified materials, modular designs, and omni-channel strategies to enhance margins and market reach.

| Key Insights | Details |

|---|---|

| Jewelry Boxes & Organizers Market Size (2026E) | US$ 3.1 Bn |

| Market Value Forecast (2033F) | US$ 4.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Jewelry Ownership and Digital-Led Lifestyle Storage Adoption

Jewelry consumption worldwide continues to expand, supported by income growth, enduring bridal jewelry traditions, and increasing penetration of fashion and everyday-wear jewelry. According to the World Gold Council, jewelry remains the dominant use of gold worldwide, while UN Comtrade data shows consistent growth in jewelry trade values over the last decade. As household jewelry volumes rise, consumers increasingly seek organized, protective, and display-oriented storage solutions to manage and safeguard their collections. This trend is especially pronounced in urban households, where space constraints and asset protection needs directly support higher replacement and upgrade cycles for jewelry boxes and organizers.

The structural expansion of home organization and lifestyle storage categories is reinforcing market demand. Smaller living spaces and rising home improvement spending have elevated jewelry storage from a functional product to a lifestyle accessory with aesthetic value. Premium finishes, modular compartmentalization, and furniture-integrated designs are driving higher average selling prices. According to OECD e-commerce statistics, online retail penetration continues to rise across both developed and emerging economies, further accelerating visibility, customization, and direct-to-consumer engagement for jewelry storage products, and strengthening long-term demand momentum.

Pricing Pressure and Rising Input Compliance Costs

Pricing pressure is clearly visible among established branded manufacturers such as IKEA, Muji, Stackers, and Mele & Co., which operate across both premium and mid-range jewelry storage categories. These brands increasingly compete with low-priced, unbranded jewelry organizers sold via e-commerce marketplaces, particularly from manufacturers based in China and Southeast Asia. In highly commoditized segments such as plastic trays, fabric organizers, and travel cases, aggressive pricing by unbranded sellers has constrained the ability of branded players to raise prices, even as logistics, labor, and packaging costs increase. As a result, branded manufacturers are often forced to absorb cost increases or rationalize product portfolios to protect market share.

The branded suppliers serving Europe and North America face rising compliance-driven input costs. Companies using wood and leather, such as IKEA, Stackers, and Wolf 1834, must comply with European Union (EU) environmental directives, FSC-certified wood sourcing requirements, and leather traceability standards, which increase procurement, auditing, and certification expenses. These compliance requirements also lengthen lead times and reduce sourcing flexibility, thereby increasing operational complexity. While such measures strengthen sustainability credentials and brand trust, intense price competition has limited cost pass-through, resulting in margin pressure and reinforcing pricing and compliance costs as a structural restraint on market profitability.

Premium, Sustainable, and B2B-Driven Jewelry Storage Demand

Urban consumers and affluent buyers are increasingly opting for premium and customized jewelry boxes, watch cases, and modular organizers that match their collections and personal style. Brands such as Stackers and Mele & Co. are offering personalization options, including engraved names, interchangeable compartments, and bespoke layouts, which command higher per-unit revenue and reinforce brand loyalty. These products are often purchased as gifts or lifestyle accessories. Demand is strongest in metropolitan areas, where space-efficient, aesthetically integrated organizers are preferred. The expansion of online platforms enables consumers to access these tailored products easily, boosting sales conversion and enabling higher profit margins for manufacturers targeting the premium segment.

The sustainability and institutional demand present additional revenue streams. Eco-friendly materials such as bamboo, recycled plastics, and FSC-certified wood are gaining traction in Europe and North America, where consumers increasingly factor environmental responsibility into purchase decisions. On the B2B front, luxury retailers, jewelry chains, hotels, and corporate gifting programs are sourcing display cases and bulk organizers for stores and events, creating stable, contract-driven revenues. By combining premiumization, eco-conscious materials, and institutional procurement, manufacturers can capture higher margins in the consumer segment while securing predictable volume sales through B2B channels.

Category-wise Analysis

Product Type Insights

Jewelry boxes are expected to be the leading product type, expected to account for approximately 40% of the market revenue in 2026, driven by their universal applicability in households, gifting demand, and versatility across price points, designs, and materials. Traditional boxes perform strongly in bridal gifting, premium home décor, and luxury accessories channels, while modular designs cater to urban households seeking functional aesthetics. Pottery Barn launched a modular jewelry box collection with integrated LED lighting, reflecting the growing trend of combining style and utility. Consumer preference for organized, protective storage continues to reinforce leadership in this segment. The segment benefits from repeat purchases and brand loyalty, particularly in premium urban markets. Higher disposable incomes and the gifting culture in North America and Europe further sustain dominance.

The fastest-growing product type is travel & portable cases, projected to grow at a CAGR of 7.5% through 2033, driven by rising travel activity, compact urban living, and multifunctional designs. The popular products include Stackers Travel Jewellery Box, Lyrovo Travel Jewelry Organizer Pouch, and VASCO Travel Jewelry Organizer Roll, which cater to consumers seeking portable yet protective storage on the go. These products combine lightweight design with multiple compartments for rings, necklaces, and earrings, aligning with the needs of frequent travelers and urban professionals. The emphasis on compactness and ease-of-packing continues to accelerate adoption. Digital marketplaces and influencer-driven social shopping further boost visibility and conversion. The rising travel frequency post-pandemic and increased disposable income in key regions are strengthening this segment’s growth trajectory.

Material Insights

Wood and leather are expected to be the leading materials, likely to hold around 42% of the jewelry boxes & organizers market revenue share in 2026, driven by premium appeal, durability, and suitability for heirloom-quality jewelry. Brands such as Wolf Designs and Mele & Co. offer wooden and leather boxes with detailed finishes and protective linings, reinforcing consumer preference. These materials are especially favored in gifting and high-value collections. Urban households prioritize functional and decorative storage, and premium retailers leverage in-store and e-commerce visibility. Repeat purchases and brand loyalty support sustained market share. Product quality, craftsmanship, and aesthetic appeal remain key purchase drivers. Thus, wood and leather maintain a stronghold in both traditional and premium segments.

Eco- and sustainable materials are projected to be the fastest-growing segment, with a forecast CAGR of roughly 8.2% through 2033, driven by rising consumer awareness and environmental sustainability initiatives. Bamboo, recycled composites, and FSC-certified wood are increasingly used by brands targeting eco-conscious buyers. Examples include Stackers’ recycled material modular organizers and ethically sourced wooden boxes. Adoption is strongest in Europe and North America, where eco-conscious purchasing is high. Millennials and Gen Z are key consumers for sustainable storage. Retailers highlighting eco-credentials see higher engagement and repeat purchases. This segment offers both differentiation and premiumization opportunities for manufacturers.

Distribution Channel Insights

Specialty stores & boutiques are expected to dominate, with an estimated 36% share of the jewelry boxes & organizers market in 2026, benefiting from curated assortments, experiential retail, and personalized service. Brands such as Wolf Designs, Stackers, and Umbra leverage boutique placements to showcase premium finishes and limited editions. Physical touchpoints enable consumers to assess material, design, and compartment layout, particularly for high-value products. Retailers also capitalize on gifting occasions and seasonal promotions. High-end channels drive repeat purchases and reinforce brand storytelling. Premium collections continue to rely on in-store presence. Boutique channels remain essential for consumer trust and experiential engagement.

The online e-commerce is anticipated to be the fastest-growing channel, projected to grow at a 9.0% CAGR from 2026 to 2033, driven by convenience, global reach, and digital customization tools. Verified products include SNMMIFER Portable Travel Jewellery Box, Krishyam Travel Jewelry Case, and Carlton London Jewelry Travel Case, highlighting online-first access to diverse designs. Omni-channel strategies enhance offline experiences, while social commerce and influencer-led marketing boost engagement. Internet penetration and logistics efficiency in the Asia Pacific and North America accelerate growth. Bundled offers and product visuals improve conversions.

Regional Insights

North America Jewelry Boxes & Organizers Market Trends

North America is expected to capture around 35% of the market share in 2026, driven by high consumer spending on premium lifestyle and home décor storage solutions. Brands such as Wolf Designs and Umbra dominate premium wooden and leather jewelry boxes, while Pottery Barn integrates curated accessory collections for gifting occasions. Department stores such as Macy’s and Nordstrom reinforce visibility for high-end organizers and seasonal assortments. E-commerce platforms expand reach beyond urban hubs, providing digital customization options and flexible delivery. Consumers prioritize both functionality and aesthetics in home organization. Seasonal peaks, such as holidays, drive promotional campaigns and product upgrades. Strong IP protection, advanced logistics, and mature retail infrastructure support stable market leadership. High disposable income and lifestyle-focused consumers further bolster premium product adoption.

Premium and multifunctional organizers, modular compartments, anti-tarnish finishes, and space-efficient layouts are expected to gain traction in the upcoming years. Online-first retail strategies paired with boutique in-store experiences help brands capture both everyday and luxury buyers. Collaborations between home décor and lifestyle brands further boost category visibility and brand awareness. Retailer’s segment offerings to meet both premium and mid-range demand. Affluent urban households prioritize style, practicality, and long-term product durability. Omnichannel strategies support discovery, trial, and conversion of purchases. Seasonal gifting and cultural events enhance revenue peaks.

Europe Jewelry Boxes & Organizers Market Trends

The European market is predicted to showcase stable growth, led by Germany, the U.K., and France, with a strong focus on craftsmanship, minimalism, and premium design aesthetics. Brands such as Stackers and Friedrich Lederwaren dominate modular and leather-crafted organizers, while boutique retailers showcase curated assortments in flagship locations. Department stores such as Selfridges and high-end design outlets in Paris and Berlin integrate jewelry storage solutions into lifestyle displays. Consumers increasingly demand sustainable materials, including recycled composites and ethically sourced wood. E-commerce expands access to high-end and customizable options, complementing physical retail. Urban households favor compact, functional designs that fit modern living spaces. European buyers value quality, aesthetics, and responsible sourcing, sustaining market relevance. High discretionary spending and premium home décor trends further support steady adoption.

The eco-conscious and multifunctional organizers have grown in popularity, particularly in Scandinavia and Benelux countries. Retailers emphasize recycled fabrics, bamboo, and FSC-certified wood for premium collections. Seasonal promotions, design fairs, and cross-brand partnerships enhance consumer engagement and brand loyalty. Omnichannel strategies allow online reach while maintaining boutique experiences. Urbanization and smaller apartments increase demand for wall-mounted and modular storage solutions. Consumers reward brands with sustainability credentials and high-quality finishes. Demand is particularly strong among younger, eco-aware buyers.

Asia Pacific Jewelry Boxes & Organizers Market Trends

Asia Pacific is projected to be the fastest-growing regional market for jewelry boxes & organizers, projected to expand at approximately 7% CAGR between 2026 and 2033, driven by rising disposable incomes, jewelry gifting traditions, and rapid e-commerce adoption. China, India, and ASEAN economies lead growth, supported by local and regional brands such as Foshan Huiyi Packaging and lifestyle-focused Indian retailers. Japanese manufacturers offer elegant, compact designs for dense urban households. E-commerce marketplaces broaden access to both global and regional organizers while enabling digital customization and competitive pricing. Young urban professionals drive demand for style, practicality, and multi-functionality. Festivals, weddings, and cultural gifting occasions amplify seasonal demand. Digital payment innovations, efficient logistics, and marketplace promotions further accelerate growth. Expanding middle-class incomes and lifestyle-conscious consumers support strong long-term adoption.

The social commerce, influencer marketing, and marketplace promotions are accelerating adoption in Asia Pacific. Regional manufacturers focus on culturally relevant designs at affordable price points for local consumers. International brands such as Stackers have expanded presence through local e-commerce channels, offering modular and eco-friendly options. Urbanization and growing middle-class wealth increase baseline demand for jewelry organizers. Seasonal gifting peaks during weddings and festivals drive sales velocity and retailer promotions. Compact, multifunctional organizers gain traction in small living spaces. Localized designs and culturally themed products enhance engagement.

Competitive Landscape

The global jewelry boxes & organizers market structure is moderately consolidated, with leading players such as Wolf Designs, Stackers, Umbra, and Friedrich Lederwaren collectively controlling more than 40% of market revenue in 2026. These established brands leverage strong retail networks, premium brand positioning, and extensive product portfolios spanning wooden, leather, and modular organizers. They invest in design innovation, material differentiation, and curated lifestyle assortments to maintain market leadership.

The regional and niche players such as Foshan Huiyi Packaging (China), local Indian lifestyle brands, and small European boutique manufacturers focus on specialized consumer segments, eco-friendly materials, and culturally tailored designs. Market entry is constrained by brand recognition requirements, design differentiation, and premium material sourcing, but e-commerce platforms and social commerce enable smaller firms to reach a wider audience. Market consolidation is expected to rise gradually as global leaders form strategic partnerships, acquire boutique or regional brands, and expand omnichannel presence, while digital tools and online personalization allow software-enabled customization to gain traction.

Key Industry Developments

- In October 2025, Richpack introduced its "2026 Jewelry Packaging Blueprint," offering 200+ certified eco-friendly and premium materials, AI-assisted design tools, and sustainable manufacturing processes. The initiative enables rapid prototyping, personalized packaging, and storytelling experiences for jewelry brands. Production includes fast-turnaround options, low-carbon logistics, and localized warehousing in New York.

- In May 2025, Pottery Barn Teen launched its first home collection in collaboration with designer Kendra Scott, integrating jewelry-inspired aesthetics into dorm and teen bedroom décor. Offerings included gem-shaped vanity mirrors doubling as jewelry organizers, coordinated storage solutions, and lifestyle accessories. Products combined signature gemstone motifs with functional design, with the collection highlighting vibrant colors, brass detailing, and no-nails décor options.

- In March 2025, WOLF inaugurated its California facility, featuring a dedicated showroom and event space for partners, retailers, and designers. The opening hosted the first U.S. edition of the "Leaders in Conversation" panel series. The facility functions as a hub for design, finance, customer service, and operations. The expansion strengthens WOLF’s presence in the key Americas market. The restored 1952 building blends heritage with modern infrastructure. It positions the 190-year-old British brand for long-term growth in North America.

Companies Covered in Jewelry Boxes & Organizers Market

- Wolf 1834

- Stackers

- Songmics

- Mele & Co.

- Pottery Barn

- IKEA

- Umbra

- Zara Home

- Muji

- Amazon Basics

- Williams-Sonoma

- Godinger

Frequently Asked Questions

The global jewelry boxes & organizers market is projected to reach US$ 3.1 billion in 2026.

Rising jewelry ownership, high demand for premium, multifunctional, and eco-friendly organizers, and online personalization and curated retail experiences are supporting market growth.

The market is expected to witness a CAGR of 5.8% from 2026 to 2033.

Prime opportunities include customizable premium storage in urban markets, adoption of sustainable materials, and increasing B2B demand from hotels, retailers, and corporate gifting programs.

Wolf Designs, Stackers, Umbra, Friedrich Lederwaren, and Foshan Huiyi are a few among the leading players.