- Smart Packaging

- Fragrance Jewelry Pods Market

Fragrance Jewelry Pods Market Size, Share, and Growth Forecast, 2026 - 2033

Fragrance Jewelry Pods Market by Product Type (Necklaces, Bracelets, Others), Fragrance Type (Floral, Fruity, Others), End-user, Distribution Channel, and Regional Analysis for 2026 - 2033

Fragrance Jewelry Pods Market Size and Trends Analysis

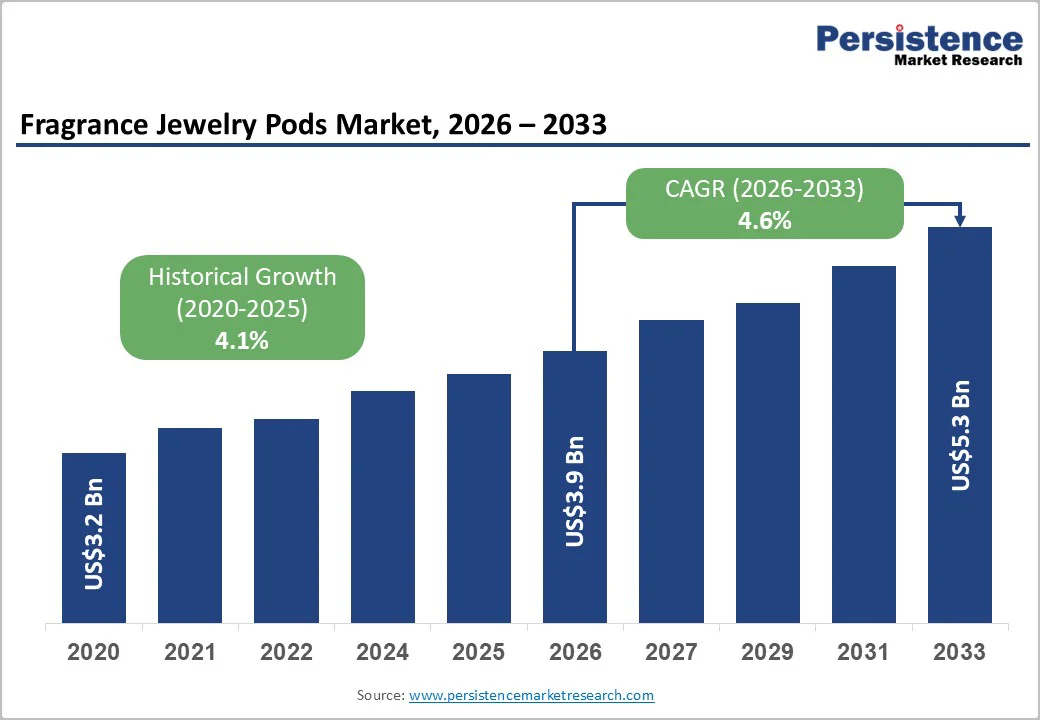

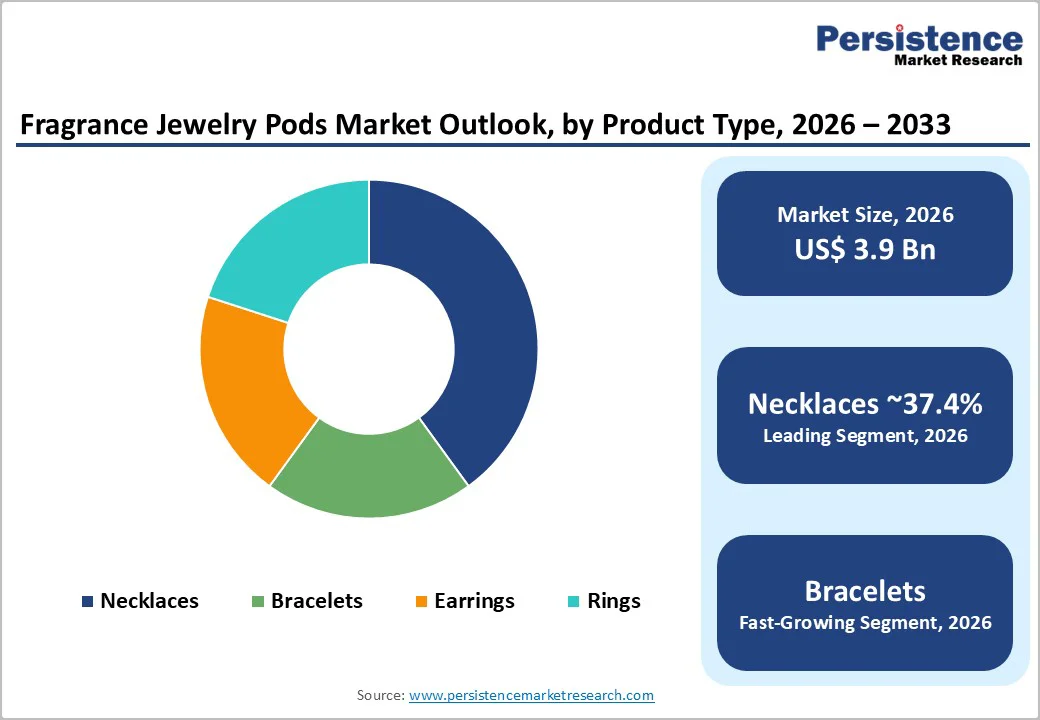

The global fragrance jewelry pods market size is likely to be valued at US$3.9 billion in 2026 and is expected to reach US$5.3 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033, driven by the convergence of fragrance personalization with wearable accessories, sustained consumer spending on lifestyle and gifting products, and the continued rise of direct-to-consumer and omnichannel retail models.

Product innovations, such as refillable pods and compatibility with essential oils, are redefining design standards and influencing consumer purchasing decisions. Although the market is still anchored in fashion jewelry, it is gradually gaining ground from the wellness and personal-care sector as fragrance becomes integrated into everyday self-care habits.

Key Industry Highlights

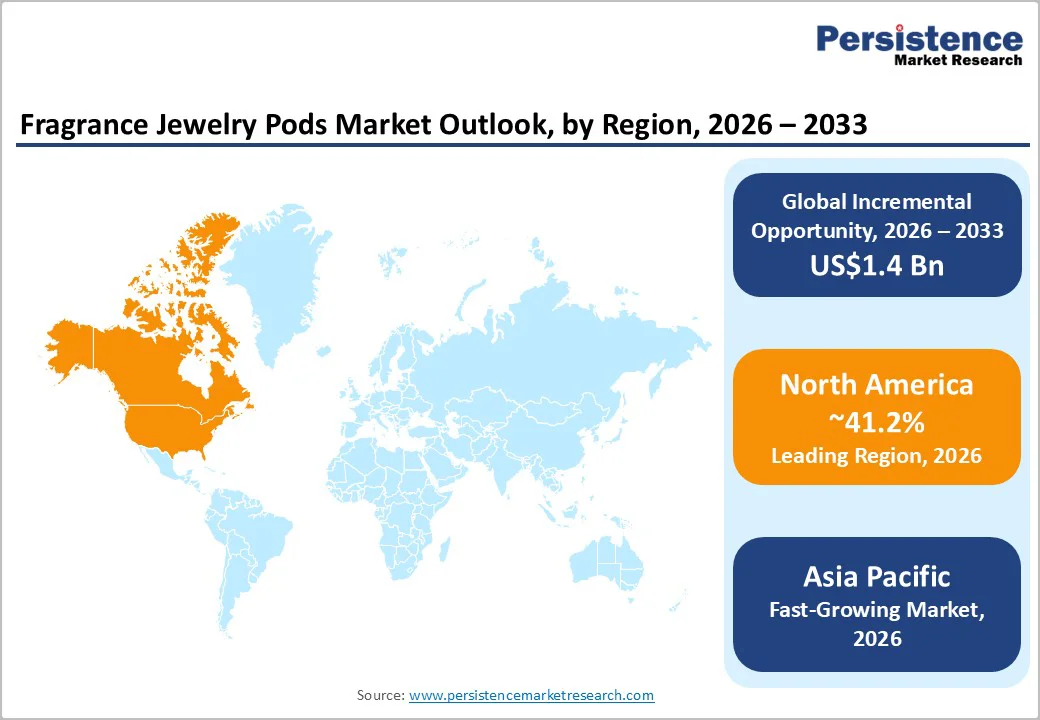

- Leading Region: North America is projected to account for 41.2% of the market, supported by strong U.S. consumer spending on lifestyle accessories, advanced omnichannel retail penetration, and a well-established refill-based purchasing ecosystem.

- Fastest-growing Region: Asia Pacific, recording the highest growth momentum due to expanding middle-class populations, cultural affinity for jewelry, rapid e-commerce adoption, and cost-efficient manufacturing of modular fragrance pod systems.

- Investment Plans: Capital deployment is increasingly focused on digitally native, direct-to-consumer brands with scalable supply chains and recurring refill revenue models, particularly in North America and export-oriented manufacturing hubs in the Asia Pacific.

- Dominant Product Type: Necklaces are anticipated to hold a 37.4% market share, driven by structural compatibility with fragrance pods, higher average selling prices, and strong gifting relevance.

- Leading Fragrance Type: Floral fragrances are estimated to account for 32.7% of market share, supported by broad demographic appeal, gifting associations, and positioning as core signature scents in refill assortments.

| Key Insights | Details |

|---|---|

| Fragrance Jewelry Pods Market Size (2026E) | US$3.9 Bn |

| Market Value Forecast (2033F) | US$5.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Convergence of Fashion Accessories and Wellness Consumption

Consumers increasingly perceive fragrance as an extension of personal identity and emotional well-being. Fragrance jewelry pods capitalize on this shift by integrating scent delivery into necklaces, bracelets, rings, and earrings, enabling fragrance use beyond traditional sprays and roll-ons. The broader fragrance and jewelry markets have demonstrated stable mid-single-digit growth in recent years, providing a favorable macroeconomic environment for hybrid products. Personalized, portable scent solutions continue to gain relevance among consumers seeking differentiated lifestyle accessories.

Channel Evolution through E-Commerce and Direct-To-Consumer Models

The expansion of online retail has reduced distribution barriers for niche and emerging fragrance jewelry brands. Digital channels enable rapid product launches, subscription-based refill programs, and data-driven personalization strategies that are difficult to replicate in traditional retail environments. Online jewelry sales penetration continues to increase, supporting faster adoption of novel accessory categories. Digital-first brands benefit from lower fixed retail costs, shorter feedback loops, and the ability to test limited-edition fragrance variants efficiently. This channel shift has also increased repeat purchase frequency by simplifying refill access, directly supporting long-term revenue stability and higher customer lifetime value.

Ingredient Regulation and Allergen Disclosure Requirements

Fragrance-related regulatory frameworks impose limitations on ingredient selection, labeling, and product claims. Compliance with safety standards and allergen disclosure requirements increases formulation complexity and documentation costs, particularly for brands lacking in-house regulatory expertise. Reformulation, stability testing, and compliance validation can add approximately 1.5% to 4.0% to the cost of goods sold for fragrance-integrated jewelry products in regulated markets. These incremental costs put pressure on margins, especially in lower-priced fashion jewelry segments, where price elasticity is high.

Barrier Analysis - Concerns over Durability and Scent Longevity

Consumers expect fragrance jewelry to deliver both aesthetic durability and consistent scent diffusion. Products with inadequate sealing systems or low-quality materials often have higher return rates and negative reviews, which can limit brand credibility. To mitigate this risk, manufacturers must invest in engineering solutions such as advanced sealing mechanisms, hypoallergenic metals, and standardized refill systems. These investments increase upfront development costs and raise minimum order quantities, creating structural barriers for small-scale designers and limiting rapid market entry.

Opportunity Analysis - Premiumization and Refill-Based Recurring Revenue Models

Refillable fragrance pod systems offer a pathway to recurring revenue and margin expansion. Even modest adoption of refill subscriptions among existing fragrance jewelry users can materially expand the addressable market. Bundling jewelry with consumable refills enhances customer retention while shifting revenue mix toward higher-margin consumables, improving long-term profitability.

Expansion in Emerging Markets and Gifting-Driven Demand

Emerging markets in the Asia Pacific and select Latin American countries demonstrate strong demand for occasion-led gifting and novelty accessories. Rising disposable incomes among millennials and Gen Z consumers support higher spending on personalized lifestyle products. A 5-7% increase in penetration within fast-adopting demographics could accelerate regional growth beyond baseline projections. Manufacturers with cost-efficient production capabilities and localized product assortments are well-positioned to capture this incremental demand through seasonal collections and entry-level pricing strategies.

Category-wise Analysis

Product Type Insights

Necklaces are anticipated to hold a 37.4% market share in 2026, primarily due to their structural suitability for housing fragrance pods and their prominence as visible fashion accessories. Pendant-style designs allow manufacturers to integrate refillable capsules, absorbent beads, or wick-based inserts while maintaining visual appeal and functional durability. Necklaces generate higher revenue per unit than bracelets or earrings, supported by premium materials, intricate designs, and longer product lifecycles.

Necklaces also benefit from strong gifting relevance, particularly during festive and celebratory occasions, where consumers associate pendants with higher perceived value. Brands such as Aroma Jewelry, Zenned Out, and Soulmate Jewelry have successfully positioned locket-style diffuser necklaces as customizable gifting products by offering interchangeable scent pods and engraved pendants. These features enhance repeat-purchase behavior through refill sales, contributing to margin stability and recurring-revenue models for manufacturers and retailers.

Bracelets are likely to be the fastest-growing product type, driven by increasing demand for lightweight, everyday wearable accessories that align with casual fashion and wellness-oriented lifestyles. Stackable bracelet formats, compatibility with athleisure and office wear, and lower average price points support wider consumer adoption, particularly among first-time buyers. Compared to necklaces, bracelets offer greater ease of use and less sensitivity to visibility-related issues, encouraging frequent wear and repeated scent experimentation. Product innovation has played a crucial role in accelerating the adoption of bracelets.

Compact fragrance capsules, magnetic or silicone-based closures, and skin-safe metal alloys enable scalable production and durability. Companies such as Scentchips Jewelry and Essential Oil Bracelet Co. have expanded bracelet portfolios through modular designs compatible with multiple scent inserts. These products perform strongly on direct-to-consumer e-commerce platforms, where affordability and customization drive higher conversion rates and support rapid volume growth.

Fragrance Type

Floral fragrances are estimated to remain the dominant scent category in the market, accounting for 32.7% of market share in 2026. Their broad cross-demographic appeal and strong association with gifting, personal care, and emotional well-being position floral scents as default options for both first-time and repeat buyers. Notes such as lavender, rose, jasmine, and lily are widely recognized and culturally accepted across regions, supporting consistent global demand.

From a commercial perspective, floral fragrances are often positioned as core or signature scents within refill assortments. This strategy simplifies inventory management and reduces consumer decision fatigue, improving sell-through efficiency. Brands including Bloom Diffuser Jewelry and Aromatherapy Jewelry Company commonly bundle floral pods with initial jewelry purchases, reinforcing their role as entry-point fragrances. Their perceived sophistication and versatility also enable premium pricing, strengthening revenue contribution within the overall fragrance mix.

Fruity fragrance types are likely to grow fastest, particularly among younger consumers and lifestyle-driven buyers seeking energetic, mood-enhancing scent profiles. Notes such as citrus, berry, apple, and tropical blends align with wellness trends that emphasize emotional uplift and personalization. Unlike traditional floral scents, fruity fragrances are frequently marketed as seasonal or situational, encouraging repeat purchases and collection-based consumption.

Growth in this segment is supported by advancements in micro-concentrate formulation technologies, enabling high scent intensity in compact pod formats. Digital customization tools and online configurators enable consumers to create personalized fruity blends, increasing average order value. Brands such as My Mood Jewelry and Scentique Pods have leveraged limited-edition fruity collections tied to summer or festive themes, driving engagement and accelerating adoption. These dynamics position fruity fragrances as a key growth engine within the evolving fragrance jewelry ecosystem.

Regional Insights

North America Fragrance jewelry Pods Market Trends - U.S.-Led Omnichannel Growth and Refill-Driven Revenue Dominance

North America is projected to lead with a 41.2% market share in 2026, driven primarily by sustained demand in the U.S. High discretionary spending on lifestyle accessories, a strong gifting culture, and advanced omnichannel retail ecosystems underpin regional leadership. Subscription-style refill sales and seasonal scent launches contribute meaningfully to recurring revenue across direct-to-consumer channels.

The U.S. market benefits from the presence of digitally native brands such as Zenned Out, Aroma Jewelry, and Essential Oil Bracelet Co., which have scaled through platforms including Shopify, Amazon, and Etsy. These brands leverage influencer-led discovery, wellness positioning, and personalized scent offerings to drive customer acquisition. From a regulatory standpoint, oversight by the U.S. Food and Drug Administration (FDA) and adherence to IFRA fragrance safety standards have increased labeling and formulation compliance costs.

These measures also enhance consumer trust and reduce product risk, favoring established players with quality control capabilities. Venture and private equity investment activity increasingly targets brands with data-driven inventory planning, vertically integrated sourcing, and predictable refill repurchase behavior, reinforcing North America’s leadership position.

Europe Fragrance Jewelry Pods Market Trends - Design-Centric Expansion Shaped by EU Regulatory Rigor and Licensing Models

Europe represents a mature yet innovation-led market for fragrance jewelry pods, with strong demand concentrated in Germany, the U.K., France, and Spain. Consumer preference in the region leans toward design-led products that combine fragrance functionality with established jewelry aesthetics. Designer collaborations and licensing partnerships play a central role, enabling fashion and accessories brands to enter the fragrance jewelry category without building proprietary scent infrastructure. This approach has been particularly visible among boutique jewelry houses and concept stores across Western Europe.

The regulatory environment significantly shapes market dynamics. Compliance with EU Cosmetics Regulation (EC) No 1223/2009, mandatory allergen disclosure, and IFRA guidelines increases product development timelines and costs but strengthens transparency and consumer safety. These requirements favor players with regulatory expertise and standardized sourcing. Brands operating within the EU increasingly emphasize hypoallergenic materials, traceable fragrance ingredients, and refill sustainability claims.

Investment activity in Europe centers on premium positioning, with fragrance jewelry frequently marketed through department stores, museum shops, and curated lifestyle retailers. Licensing agreements enable established fashion brands to test demand for fragrance and jewelry while minimizing operational complexity, supporting steady yet controlled market expansion.

Asia Pacific Fragrance Jewelry Pods Market Trends - Manufacturing-Led Scale and E-Commerce-Accelerated Adoption across Asia Pacific

Asia Pacific is the fastest-growing regional market, supported by strong cultural affinity for jewelry, expanding middle-class populations, and competitive manufacturing advantages. China and India dominate the volume demand, driven by affordability-focused designs and gifting traditions, while Japan emphasizes minimalist aesthetics, craftsmanship, and subtle fragrance profiles. The region benefits from a well-established jewelry supply chain ecosystem, enabling cost-efficient production of modular pod systems and refill components at scale.

Growth acceleration is closely tied to the expansion of digital commerce platforms such as Tmall, JD.com, Flipkart, and Rakuten, which enable small and mid-sized brands to reach national and cross-border audiences efficiently. Several Asia-based manufacturers operate as original equipment manufacturers (OEMs) for Western fragrance jewelry brands, aligning production with IFRA standards to support exports to North America and Europe.

Indian and Chinese suppliers specializing in stainless steel, brass, and hypoallergenic alloys have gained relevance as global brands seek supply chain diversification. This manufacturing and export orientation positions Asia Pacific as both a high-growth consumption market and a strategic production hub, reinforcing its long-term importance within the global fragrance jewelry pods market.

Competitive Landscape

The global fragrance jewelry pods market is moderately fragmented. Premium segments are influenced by established jewelry brands and fragrance licensors, while value segments are populated by numerous independent designers and digital-native brands. Brand equity, distribution access, and engineering quality drive competitive differentiation at the high end, while price sensitivity and design novelty dominate lower tiers.

Recent developments include licensing partnerships between jewelry brands and fragrance specialists, limited-edition scented jewelry launches emphasizing wellness positioning, and ongoing updates to fragrance ingredient standards. These developments highlight the market’s transition toward formalized product architectures, higher compliance thresholds, and deeper integration between fashion and fragrance value chains.

Key strategies include innovation in refill systems, partnerships with fragrance formulators, and expansion of subscription-based models. Market leaders emphasize brand heritage and product reliability, while emerging players focus on affordability, rapid design cycles, and social-commerce engagement.

Key Industry Developments

- In May 2025, Belgian jewelry brand Wouters & Hendrix collaborated with model and wellness advocate Hannelore Knuts to launch L’Issence, a scented ring that embeds a discreet refillable scent wick infused with a custom essential-oil blend, illustrating the fusion of fine jewelry craftsmanship with wearable scent functionality.

- In May 2025, Toronto-based designer label Nidolio introduced the world’s first aroma-infused fine jewelry line, blending handcrafted sculptural pieces with essential-oil fragrances that diffuse scent as wearable wellness accessories, marking a notable innovation in scent-integrated jewelry.

Companies Covered in Fragrance Jewelry Pods Market

- Aroma Jewelry

- Zenned Out

- Scentchips Jewelry

- Essential Oil Bracelet Co.

- Aromatherapy Jewelry Company

- Soulmate Jewelry

- Bloom Diffuser Jewelry

- My Mood Jewelry

- Scentique Pods

- Diffuser World

- Vivi Bella Designs

- Simply Earth Jewelry

- Bali Jewelry Diffusers

- Tranquil Aroma Jewelry

- Nirvana Diffuser Jewelry

- AromaLuxe Accessories

- Pure Essence Jewelry

- ScentWear Collective

- ZenStyle Diffuser Jewelry

Frequently Asked Questions

The global fragrance jewelry pods market is valued at US$3.9 billion in 2026.

By 2033, the fragrance jewelry pods market is projected to reach US$5.3 billion.

Key trends include growth in refillable and modular jewelry designs, increasing demand for personalized fragrance pods, rising integration of wellness and aromatherapy concepts, and expanding direct-to-consumer and e-commerce distribution channels.

Necklaces are the leading product segment, accounting for 37.4% of market share, due to their structural suitability for fragrance pods and strong gifting appeal.

The fragrance jewelry pods market is expected to grow at a CAGR of 4.6% between 2026 and 2033.

Major players include Aroma Jewelry, Zenned Out, Scentchips Jewelry, Essential Oil Bracelet Co., and Aromatherapy Jewelry Company.