- Medical Devices

- Intermittent Catheters Market

Intermittent Catheters Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Intermittent Catheters Market by Product (Coated Intermittent Catheters and Uncoated Intermittent Catheters), by Type (Male Length Catheter, Female Length Catheter, and Pediatric Length Catheter) by Material (Latex, Rubber, Silicone, and Polyvinylchloride (PVC)), by Application (Urinary Incontinence, Urinary Retention, Prostate Gland Surgery, Spinal Cord Injury, and Others), by End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Home Care Settings) and Regional Analysis from 2026 to 2033

Intermittent Catheters Market Share and Trend Analysis

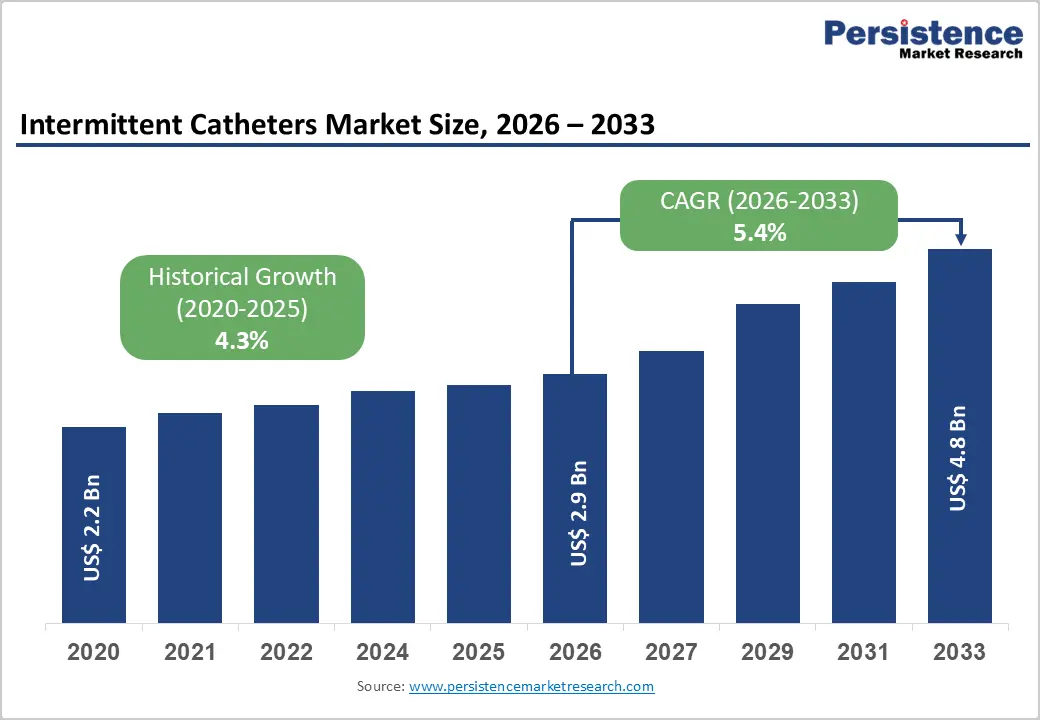

The global intermittent catheters market size is estimated to grow from US$ 2.9 Bn in 2026 to US$ 4.8 Bn by 2033. The market is projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033.

Global demand for intermittent catheter solutions is increasing steadily, driven by the rising prevalence of urinary incontinence, urinary retention, neurogenic bladder disorders, spinal cord injuries, and post-surgical urinary complications. Aging populations, increasing incidence of diabetes and prostate-related conditions, and higher survival rates following neurological trauma have significantly expanded the patient pool requiring long-term bladder management. Growing clinical awareness and adoption of clean intermittent self-catheterization are improving patient independence while reducing the risk of complications associated with indwelling catheters.

Advancements in catheter technology, including hydrophilic coatings, pre-lubricated designs, and single-use sterile products, are enhancing comfort, safety, and adherence. Intermittent catheters are widely used across hospitals, specialty clinics, ambulatory surgical centers, and home-care settings to support effective bladder emptying and reduce infection risk. Rising healthcare expenditure, expansion of advanced hospital infrastructure, and improved access to urology care in emerging markets are reinforcing long-term demand. Additionally, favorable reimbursement frameworks in developed regions, expanding patient education programs, and continuous product innovation continue to support sustained global market growth.

Key Industry Highlights

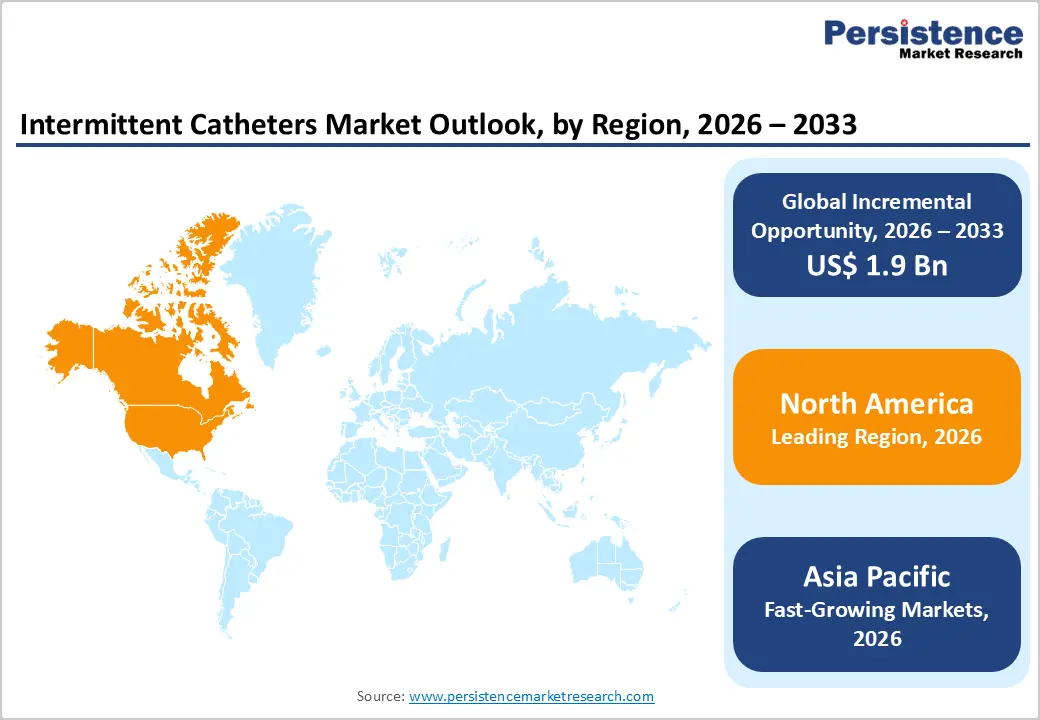

- Leading Region: North America holds the largest share at 47.3%, supported by advanced healthcare infrastructure, high awareness of urological disorders, early adoption of coated intermittent catheters, strong reimbursement coverage, and the presence of leading medical device companies.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rising healthcare expenditure, improving access to urology care, growing elderly and post-surgical populations, rapid hospital expansion, and increasing adoption of patient-friendly intermittent catheter solutions.

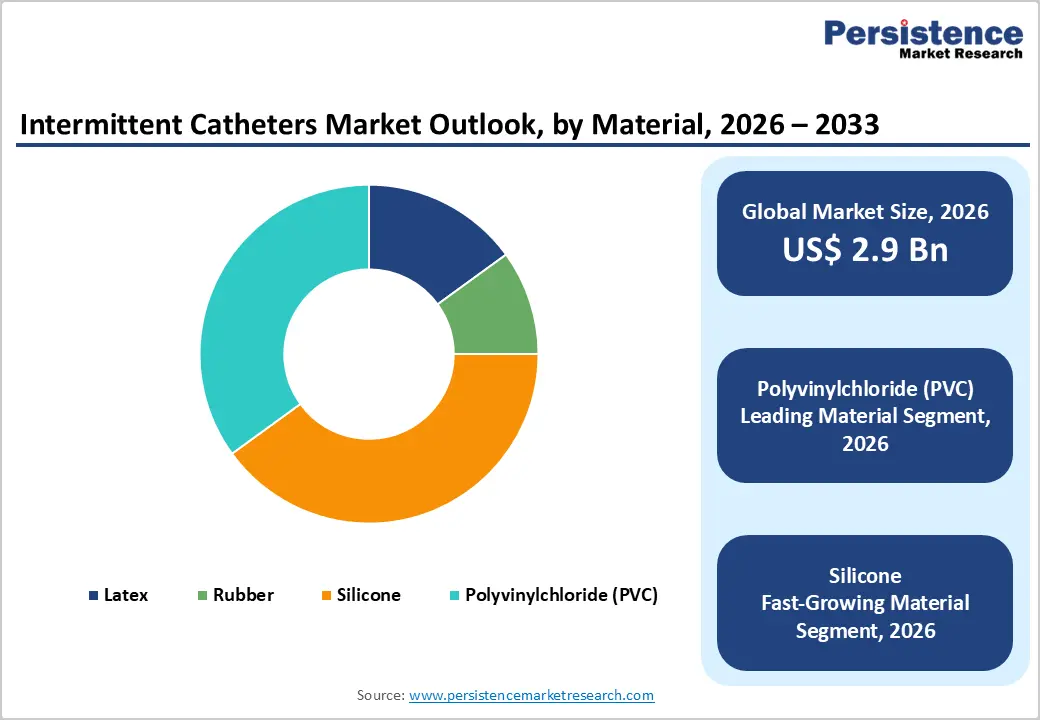

- Leading Material Segment: Polyvinylchloride (PVC) dominates the market due to its cost-effectiveness, widespread clinical usage, ease of manufacturing, and broad availability across hospital and home-care settings.

- Fastest-Growing Material Segment: Silicone is growing steadily due to its superior biocompatibility, reduced allergy risk, and increasing preference for long-term and frequent catheterization applications.

- Leading Application Segment: Urinary incontinence remains the top segment, driven by high disease prevalence, standardized clinical management protocols, and consistent utilization across care settings.

- Fastest-Growing Application Segment: Prostate gland surgery is witnessing renewed growth due to rising surgical volumes, aging male populations, and increased need for short-term post-operative bladder management in hospital and ambulatory settings.

| Global Market Attributes | Key Insights |

|---|---|

| Intermittent Catheters Market Size (2026E) | US$ 2.9 Bn |

| Market Value Forecast (2033F) | US$ 4.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver – Rising Prevalence of Urological Disorders and Shift Toward Intermittent Self-Catheterization

Growth is primarily driven by the increasing global prevalence of urinary incontinence, urinary retention, neurogenic bladder dysfunction, and spinal cord injuries, which necessitate effective bladder management solutions. Aging populations, rising incidence of diabetes, prostate disorders, and post-surgical complications are significantly expanding the patient pool requiring intermittent catheterization. Clinically, intermittent catheters are increasingly preferred over indwelling catheters due to lower risks of infection, improved bladder health, and better long-term outcomes. Growing awareness among physicians and patients regarding the benefits of clean intermittent self-catheterization has accelerated adoption, particularly in home-care settings.

Technological advancements such as hydrophilic coatings, pre-lubricated designs, compact packaging, and single-use sterile products enhance ease of use, comfort, and patient compliance. These innovations are especially valuable for patients with limited dexterity or chronic conditions requiring frequent catheterization. Favorable reimbursement policies in developed markets, coupled with strong clinical guidelines supporting intermittent catheter use, further support demand. In addition, increasing hospital admissions, surgical procedures, and rehabilitation programs continue to drive consistent utilization across acute and long-term care settings, sustaining market growth globally.

Restraints – Cost Barriers, Infection Risks, and Limited Access in Developing Regions

The market faces notable constraints related to the higher cost of advanced intermittent catheters, particularly coated and single-use products, which may limit adoption in cost-sensitive healthcare systems. In low- and middle-income regions, patients often rely on reusable or uncoated catheters due to affordability concerns, increasing the risk of complications and limiting market penetration of premium products. Reimbursement variability across countries further affects purchasing decisions, especially for home-care patients who may bear out-of-pocket expenses.

Improper catheterization techniques, lack of patient training, and inconsistent hygiene practices contribute to catheter-associated urinary tract infections, which can deter long-term usage and negatively impact clinical outcomes. Limited access to trained healthcare professionals and patient education programs in rural or underserved areas restricts effective adoption of self-catheterization. Additionally, regulatory complexity, stringent product approval requirements, and compliance with international quality standards increase development and manufacturing costs for suppliers. Supply chain disruptions and dependency on imported medical devices in certain regions further constrain availability. Collectively, these financial, clinical, and infrastructure-related challenges moderate market growth and highlight the need for affordable solutions and broader education initiatives.

Opportunity – Product Innovation, Home-Care Expansion, and Growth in Emerging Economies

Significant opportunities are emerging from continuous innovation in catheter design, including ultra-low friction coatings, antimicrobial surfaces, compact travel-friendly formats, and environmentally sustainable materials. These advancements improve patient comfort, reduce infection risk, and support long-term adherence, particularly among chronic users. The rapid expansion of home healthcare services presents a major growth avenue, as patients increasingly prefer independent bladder management supported by discreet and easy-to-use catheter solutions. Integration of digital health tools, remote monitoring, and patient training platforms further enhances self-catheterization outcomes.

Emerging markets across Asia Pacific, Latin America, and parts of Africa offer substantial untapped potential due to improving healthcare infrastructure, rising healthcare expenditure, and growing awareness of urological health. Government investments in hospital expansion, aging population growth, and increasing surgical volumes are expected to boost demand. Local manufacturing, cost-optimized product lines, and public-private partnerships are improving affordability and access. Additionally, collaborations between medical device companies, healthcare providers, and rehabilitation centers are accelerating adoption. As awareness, accessibility, and innovation converge, these opportunities are expected to drive sustained long-term growth.

Category-wise Analysis

By Product, Coated Intermittent Catheters Lead Due to Superior Patient Comfort and Lower Infection Risk

Coated intermittent catheters are projected to dominate the global intermittent catheters market in 2026, accounting for a revenue share of 64.5%. This leadership is primarily driven by increasing adoption of hydrophilic and pre-lubricated coatings that significantly reduce friction, discomfort, and urethral trauma during catheterization. These advantages are particularly critical for patients requiring long-term or frequent self-catheterization, such as those with spinal cord injuries, neurogenic bladder, or chronic urinary retention.

Growing clinical emphasis on reducing catheter-associated urinary tract infections (CAUTIs) further supports the shift toward coated products. Additionally, improved ease of use, discreet packaging, and enhanced portability make coated catheters more suitable for home-care settings. Favorable reimbursement policies in developed markets, along with rising patient awareness and physician preference for safer catheterization options, continue to reinforce the dominance of coated intermittent catheters throughout the forecast period.

By Application, Urinary Incontinence Leads Due to High Disease Prevalence and Standardized Care Pathways

The urinary incontinence segment is expected to lead the intermittent catheters market in 2026, capturing a revenue share of 35.0%. This dominance is attributed to the high and growing prevalence of urinary incontinence, particularly among the aging population, post-surgical patients, and individuals with neurological disorders. Intermittent catheterization remains a preferred bladder management approach due to its effectiveness in maintaining continence, reducing bladder pressure, and minimizing long-term complications.

Standardized clinical guidelines and physician recommendations support widespread adoption across hospitals, specialty clinics, and home-care settings. Increasing awareness, early diagnosis, and proactive management strategies are expanding the treated patient population. Furthermore, patient-centric catheter designs that enhance comfort, discretion, and independence are driving consistent utilization. These factors collectively sustain urinary incontinence as the leading application segment in terms of revenue contribution.

By End User, Hospitals Lead Due to High Procedure Volumes and Acute Care Demand

Hospitals are projected to dominate the global intermittent catheters market in 2026, accounting for a revenue share of 44.4%. This leadership is driven by the high volume of catheterization procedures performed in hospital settings, particularly for acute urinary retention, post-operative care, trauma cases, and neurological conditions. Hospitals serve as the primary point of diagnosis and treatment initiation, where intermittent catheterization is commonly prescribed during inpatient stays.

The presence of trained healthcare professionals ensures proper catheter selection, patient education, and infection control. Additionally, hospital pharmacies benefit from structured procurement systems, favorable reimbursement frameworks, and government healthcare funding. Large tertiary and teaching hospitals also play a key role in early adoption of advanced catheter technologies and clinical best practices. As surgical volumes and chronic disease management needs continue to rise, hospitals are expected to remain the leading end-user segment.

Region-wise Insights

North America Intermittent Catheters Market Trends

North America is expected to dominate the global intermittent catheters market with a value share of 47.7% in 2026, led primarily by the United States. The region benefits from a well-established healthcare infrastructure, high awareness of urinary disorders, and early adoption of advanced medical devices. Strong clinical emphasis on patient safety and infection prevention has accelerated the shift toward coated intermittent catheters. High prevalence of urinary incontinence, spinal cord injuries, and neurogenic bladder conditions further drives demand.

Favorable reimbursement policies under Medicare, Medicaid, and private insurers support widespread product accessibility across hospital and home-care settings. The presence of leading medical device manufacturers, continuous product innovation, and robust distribution networks contribute to strong market penetration. Additionally, extensive patient education programs, trained healthcare professionals, and growing preference for self-catheterization enhance long-term adoption. These factors collectively sustain North America’s leadership throughout the forecast period.

Europe Intermittent Catheters Market Trends

The European intermittent catheters market is projected to grow steadily, supported by strong public healthcare systems, well-established hospital networks, and increasing focus on long-term bladder management. Countries such as Germany, the U.K., France, Italy, and Spain lead adoption due to structured urology care pathways and national reimbursement coverage for catheterization products. Rising awareness of urinary incontinence and neurogenic bladder disorders, particularly among the elderly population, is driving consistent demand. Public healthcare funding ensures access to both coated and uncoated intermittent catheters, supporting patient compliance and continuity of care.

Stringent regulatory standards across the region ensure high-quality products and standardized clinical practices. In addition, growing adoption of home-care models and patient self-management solutions is expanding usage beyond hospital settings. Continuous training of healthcare professionals and focus on infection prevention further contribute to sustained market growth across Europe.

Asia Pacific Intermittent Catheters Market Trends

The Asia Pacific intermittent catheters market is expected to register a higher CAGR of around 7.9% between 2026 and 2033, driven by improving healthcare infrastructure, rising awareness of urological disorders, and expanding access to medical devices. Countries such as China, India, Japan, South Korea, and Australia are witnessing increasing diagnosis rates of urinary incontinence and neurogenic bladder conditions. Government investments in hospital expansion, aging population growth, and rising surgical volumes are fueling demand for intermittent catheters. Urban hospitals are increasingly adopting standardized catheterization protocols, while domestic manufacturers improve affordability and product availability.

Expansion of home healthcare services and patient education initiatives is further supporting self-catheterization adoption. Growing reimbursement coverage, public-private partnerships, and physician training programs enhance clinical outcomes. Collectively, these factors position Asia Pacific as the fastest-growing regional market during the forecast period.

Market Competitive Landscape

The global intermittent catheters market is highly competitive, with strong participation from companies such as Boston Scientific Corporation, Medtronic, Hollister Incorporated, B. Braun SE, Coloplast Corp, BD, and Teleflex Incorporation. These players leverage extensive global distribution networks, strong brand recognition, and diversified medical device portfolios to address the rising demand for effective urinary management solutions.

Their product offerings emphasize coated and uncoated intermittent catheters, user-friendly designs, and materials aimed at improving patient comfort, reducing infection risk, and supporting long-term self-catheterization. Continuous innovation in product design, regulatory approvals, clinical safety, infection prevention, and compliance with international quality and manufacturing standards remains critical for maintaining competitive positioning in the global intermittent catheters market.

Key Industry Developments:

- In April 2023, Coloplast reported positive results from its first pivotal clinical study of Luja, a next-generation intermittent male catheter featuring more than 80 micro-holes. The study demonstrated complete bladder emptying in a single free flow in 90% of catheterisations, highlighting Luja’s ability to minimize residual urine and reduce bladder microtrauma, thereby lowering the risk of urinary tract infections.

- In July 2022, Otsuka Pharmaceutical Factory, Inc. announced the launch of the OT-Balloon Catheter®, an intermittent urological catheter introduced on August 22, 2022. The reusable device is designed for patients with difficulty urinating spontaneously and features an inflatable balloon at the catheter tip that allows temporary placement in the bladder during nighttime or outings. This design reduces the need for repeated self-catheterization while in use, enabling flexible, lifestyle-oriented bladder management.

Companies Covered in Intermittent Catheters Market

- Boston Scientific Corporation

- Medtronic

- Hollister Incorporated

- B. Braun SE

- Coloplast Corp

- BD

- Teleflex Incorporation

- Cook

- Optimum Medical Limited

- Ivor Shaw T/A Pennine Healthcare

- Medline Industries LP

- Flexicare (Group) Limited

- Convatec Inc.

- Others

Frequently Asked Questions

The global intermittent catheters market is projected to be valued at US$ 2.9 Bn in 2026.

Rising prevalence of urinary disorders, an expanding elderly population, and growing adoption of coated, self-catheterization solutions drive the global intermittent catheters market.

The global intermittent catheters market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Key opportunities lie in expanding home-care usage, penetration in emerging markets, and innovation in advanced, user-friendly, and sustainable catheter technologies.

Boston Scientific Corporation, Medtronic, Hollister Incorporated, B. Braun SE, Coloplast Corp, BD, and Teleflex Incorporation are some of the key players in the intermittent catheters market.