- Biotechnology

- Influenza Diagnostics Market

Influenza Diagnostics Market Size, Share, and Growth Forecast, 2026 - 2033

Influenza Diagnostics Market by Drug Class (ACE Inhibitors, Angiotensin Receptor Blockers, Others), Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, Others), and Regional Analysis for 2026 - 2033

Influenza Diagnostics Market Size and Trends Analysis

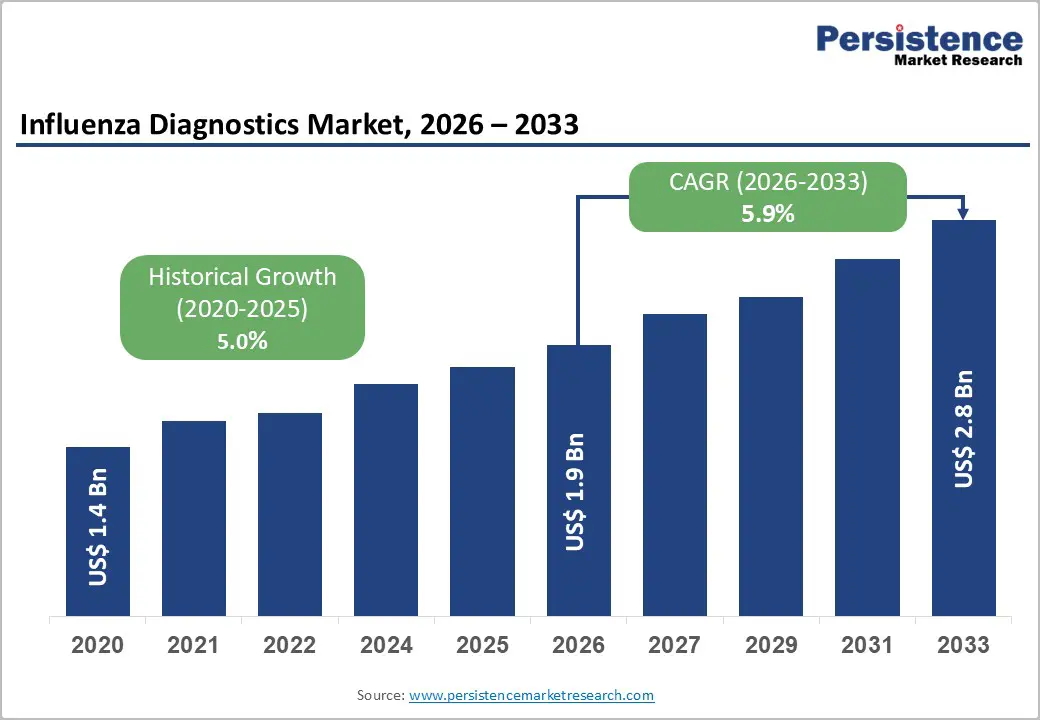

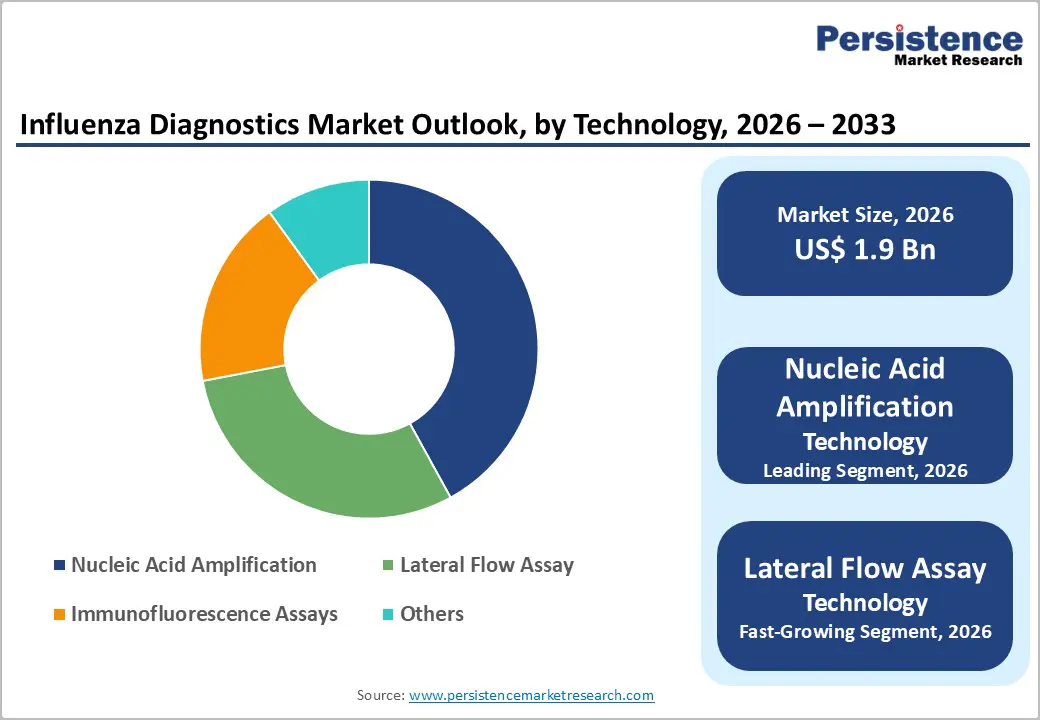

The global influenza diagnostics market size is likely to be valued at US$1.9 billion in 2026, and is expected to reach US$2.8 billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033, driven by the rising prevalence of seasonal influenza outbreaks and increasing awareness about early disease detection.

Growing demand for rapid and accurate diagnostic tests in hospitals, clinics, and laboratories has further accelerated market growth. Technological advancements in molecular diagnostics and point-of-care testing have improved testing efficiency and reliability.

Key Industry Highlights:

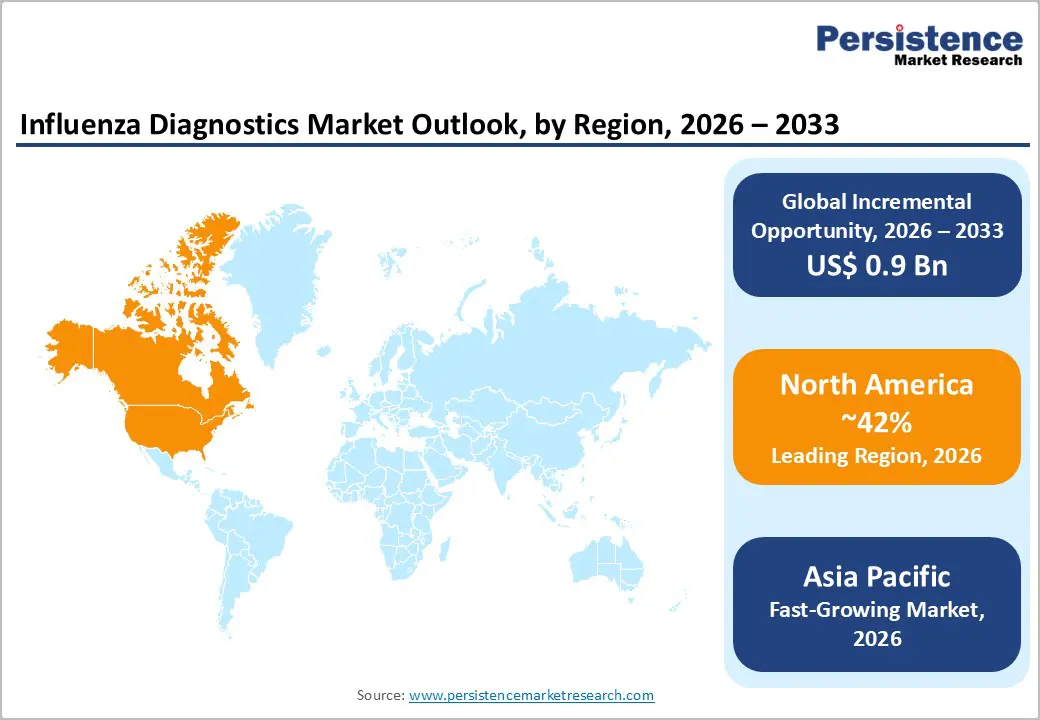

- Dominant Region: North America is expected to dominate the market with an estimated 42% revenue share in 2026, supported by strong CDC surveillance mandates and robust hospital diagnostic procurement.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing regional market, driven by healthcare infrastructure expansion in China, India, and Southeast Asia.

- Leading Product Type: Kits & reagents are anticipated to dominate the product segment with 72% share, reflecting the high-volume, repeat-purchase consumable demand inherent to diagnostic testing workflows.

- Dominant Technology: Nucleic acid amplification (NAA) technology is expected to hold 45% of the market share, underpinned by superior accuracy standards required in hospital and reference laboratory settings.

DRO Analysis

Driver - Rising Global Influenza Disease Burden and Pandemic Preparedness Spending

The rising global burden of influenza has become a major public health concern, driving increased investments in pandemic preparedness and diagnostic infrastructure. Seasonal influenza outbreaks affect millions of people every year, leading to significant hospitalizations, economic losses, and deaths, particularly among children, older adults, and immunocompromised individuals. The growing frequency of viral mutations and the emergence of new influenza strains have heightened the risk of pandemics, encouraging governments and healthcare organizations to strengthen surveillance and response systems.

In response, countries are allocating larger healthcare budgets toward pandemic preparedness initiatives, including vaccine development, stockpiling antiviral drugs, expanding laboratory capacities, and improving rapid diagnostic technologies. International organizations are also promoting early disease detection and coordinated outbreak management to reduce transmission risks. The lessons learned from the COVID-19 pandemic have accelerated awareness regarding the importance of preparedness against respiratory infections such as influenza.

Restraint - Sensitivity Limitations of Rapid Antigen Tests

Rapid influenza diagnostic tests (RIDTs) based on lateral flow assay technology, while widely accessible, carry a significant clinical limitation: their sensitivity ranges from 50%-70% compared to RT-PCR gold standards, according to CDC guidance. This means a substantial proportion of true influenza cases may yield false-negative results, particularly during early infection or in immunocompromised patients.

Healthcare providers who remain aware of this diagnostic gap often revert to confirmatory molecular testing, adding costs and turnaround time. This dual-test dynamic constrains RIDT adoption in high-acuity settings and limits market substitution of lower-cost rapid tests for more precise molecular assays.

Opportunity - Multiplex Respiratory Panel Testing and AI-Driven Diagnostics

Multiplex respiratory panel testing and AI-driven diagnostics are transforming the influenza diagnostics landscape by enabling faster, more accurate, and comprehensive disease detection. Multiplex respiratory panel tests allow healthcare professionals to simultaneously identify multiple respiratory pathogens, including influenza viruses, COVID-19, respiratory syncytial virus (RSV), and other infections, using a single patient sample. This approach reduces diagnostic time, improves clinical decision-making, and supports timely treatment initiation, especially during peak flu seasons and respiratory outbreaks.

The integration of artificial intelligence into diagnostic systems further enhances testing efficiency by improving data interpretation, predictive analytics, and outbreak monitoring. AI-powered platforms can analyze complex diagnostic patterns, detect infection trends, and assist laboratories in minimizing human errors. These technologies also support automated reporting and real-time surveillance, enabling healthcare providers and public health agencies to respond more effectively to emerging influenza threats.

Category-wise Analysis

Product Type Insights

Kits & reagents are projected to dominate, accounting for an estimated 72% share of total revenue in 2026. This segment's leadership reflects the consumable, repeat-purchase nature of diagnostic reagents; every test run requires fresh reagent kits, generating predictable recurring revenue. Roche's cobas Influenza A/B assay kit exemplifies how premium molecular reagent offerings command both clinical uptake and pricing power in hospital-based laboratories.

Instruments represent the fastest-growing product segment, propelled by capital investments in automated, high-throughput platforms. BD's Veritor Plus Analyzer and bioMérieux's VIDAS platform illustrate how instrument upgrades, particularly those enabling multiplex detection, are creating new revenue streams as healthcare facilities modernize their diagnostic infrastructure.

Technology Insights

Nucleic acid amplification (NAA) technologies are estimated to dominate, approximately 45% of the share in 2026. RT-PCR and isothermal amplification methods deliver the highest diagnostic accuracy, making them the preferred choice in hospitals and reference laboratories for influenza A and B detection and subtyping. Roche's cobas Liat Influenza A/B & RSV assay is a market-leading example of NAA-based near-patient testing integration.

Lateral flow assay (LFA) technology is the fastest-growing segment, benefiting from its low cost, no-instrumentation design, and suitability for POC environments. Quidel's Sofia 2 Influenza A+B FIA test exemplifies how next-generation LFA readers are narrowing the accuracy gap with molecular methods while maintaining the speed and accessibility advantages that drive mass adoption.

End-user Insights

Hospitals and Clinics constitute the leading end-user segment, capturing an estimated 55%-60% of the market revenue in 2026. Their high patient volumes, access to reimbursement frameworks, and need for rapid diagnostic decisions to guide antiviral therapy drive consistent and large-volume procurement. Academic medical centers running FDA Emergency Use Authorization influenza protocols during outbreak seasons exemplify the depth of hospital-based demand.

Clinical Laboratories are the fastest-growing end-user category, driven by centralized testing efficiency, economies of scale in reagent procurement, and growing demand for batch molecular testing of respiratory specimens. Quest Diagnostics and LabCorp-affiliated facilities in the U.S. represent this segment's commercial profile, increasingly processing multiplex panels that include influenza alongside COVID-19 and RSV.

Regional Insights

North America Influenza Diagnostics Market Trends

North America regional market is projected to dominate, holding a 42% revenue share in 2026. The region benefits from strong reimbursement frameworks, high influenza testing awareness, and the presence of leading market players.

U.S. Influenza Diagnostics Market Insights

The U.S. represents the dominant national market in North America, driven by CDC-mandated influenza surveillance programs, CLIA-waived POC test proliferation, and robust hospital diagnostics procurement. The 2022-2023 flu season, one of the earliest and most severe in a decade, accelerated rapid influenza test adoption across urgent care and emergency department settings, reinforcing demand momentum.

Canada Influenza Diagnostics Market Insights

Canada's market growth is supported by provincial public health laboratory networks investing in molecular influenza surveillance. Health Canada's regulatory alignment with international diagnostic standards is easing market entry for innovative platforms, particularly multiplex PCR panels.

Europe Influenza Diagnostics Market Trends

Europe shows steady growth, driven by ECDC-coordinated surveillance initiatives, EU health emergency preparedness frameworks, and high hospital diagnostic standards.

Germany Influenza Diagnostics Market Trends

Germany's market is fueled by its extensive statutory health insurance reimbursement system and a dense network of clinical laboratories running automated molecular diagnostics. German hospitals have rapidly adopted multiplex respiratory panels post-COVID, boosting influenza diagnostic volumes.

U.K. Influenza Diagnostics Market Trends

The NHS seasonal flu surveillance program, in partnership with Public Health England (now UKHSA), generates structured annual demand for both rapid antigen tests and RT-PCR-based confirmatory assays. The U.K.'s accelerated IVDR adoption trajectory is also shaping procurement preferences toward higher-accuracy platforms.

Asia Pacific Influenza Diagnostics Market Trends

Asia Pacific is likely to be the fastest-growing regional market, propelled by expanding healthcare infrastructure, rising infectious disease surveillance investment, and large unmet testing needs across high-population nations. The region is expected to gain market share incrementally as molecular platform costs decline.

China Influenza Diagnostics Market Trends

China’s market is witnessing steady growth due to rising seasonal influenza cases, increasing awareness of early disease detection, and stronger government focus on pandemic preparedness. Rapid influenza diagnostic tests (RIDTs), RT-PCR assays, and point-of-care testing solutions are gaining significant adoption across hospitals and laboratories.

India Influenza Diagnostics Market Trends

India represents one of the highest-potential influenza diagnostics markets globally, given its 1.4 billion population, seasonal influenza peaks, and the National Health Mission's emphasis on diagnostic capacity building at district hospital levels. Adoption of rapid antigen tests at primary health centers is accelerating.

Competitive Landscape

The global influenza diagnostics market is moderately consolidated, with Hoffmann-La Roche Ltd, BD, bioMérieux SA, Quidel Corporation, Sekisui Diagnostics, and GenMark Diagnostics, Inc. collectively shaping competitive dynamics through continuous product innovation, strategic acquisitions, and regional expansion. Roche maintains a leadership position through its molecular diagnostics portfolio, leveraging the cobas and Liat platforms to capture premium hospital and reference laboratory segments globally. BD's BioGX reagents and Veritor platform drive POC market penetration, while bioMérieux's VIDAS and FilmArray systems address both clinical and emergency medicine workflows.

Competitive differentiation increasingly turns on software integration, connectivity, and data interoperability. GenMark Diagnostics has focused on syndromic panel testing with its ePlex platform, while Quidel, now part of QuidelOrtho, is expanding its Sofia rapid testing ecosystem into new geographies. Sekisui Diagnostics maintains a competitive niche in immunoassay-based rapid testing for resource-constrained settings.

Key Industry Developments:

- In March 2026, Roche launched the cobas ePlex Respiratory Pathogen Panel 3 (RP3), a diagnostic test that detected multiple viruses and bacteria responsible for respiratory illnesses. The company made the test available in countries that accepted the CE mark.

- In September 2025, QuidelOrtho Corporation expanded its QUICKVUE portfolio by launching the QUICKVUE Influenza + SARS Test, a CLIA-waived and 510(k)-cleared rapid immunoassay for professional use. The company designed the easy-to-use test for physician office labs, urgent care centers, emergency departments, pharmacies, and decentralized hospital laboratories.

Companies Covered in Influenza Diagnostics Market

- Hoffmann-La Roche Ltd

- BD

- bioMérieux SA

- Quidel Corporation

- SEquis Diagnostics

- GenMark Diagnostics, Inc.

Frequently Asked Questions

The global influenza diagnostics market is projected to reach US$1.9 billion in 2026.

Key growth drivers include the rising global influenza disease burden, with the WHO reporting 290,000-650,000 annual respiratory deaths, and the rapid expansion of point-of-care testing infrastructure enabled by CLIA-waived rapid diagnostic devices. Pandemic preparedness investments and government surveillance programs further accelerate market demand.

The influenza diagnostics market is poised to witness a CAGR of 5.9% from 2026 to 2033.

The most significant market opportunities are the adoption of multiplex respiratory panel testing combined with AI-driven diagnostics, and the expansion into emerging markets, particularly Asia Pacific and Latin America, through government-funded infectious disease surveillance programs and national health infrastructure investments.

Key players include Hoffmann-La Roche Ltd, BD, bioMérieux SA, Quidel Corporation (QuidelOrtho), Sekisui Diagnostics, and GenMark Diagnostics, Inc.