- Animal Health

- Canine Influenza Testing Market

Canine Influenza Testing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Canine Influenza Testing Market by Testing Methods (Molecular Testing, Traditional Testing methods), Indication (Flu, Type A influenza, Cough and cold), End User (Institutional Sales, Veterinary Diagnostic center, Veterinary Clinics, Research Institutes, Veterinary store), and Regional Analysis from 2026 to 2033.

Canine Influenza Testing Market Outlook

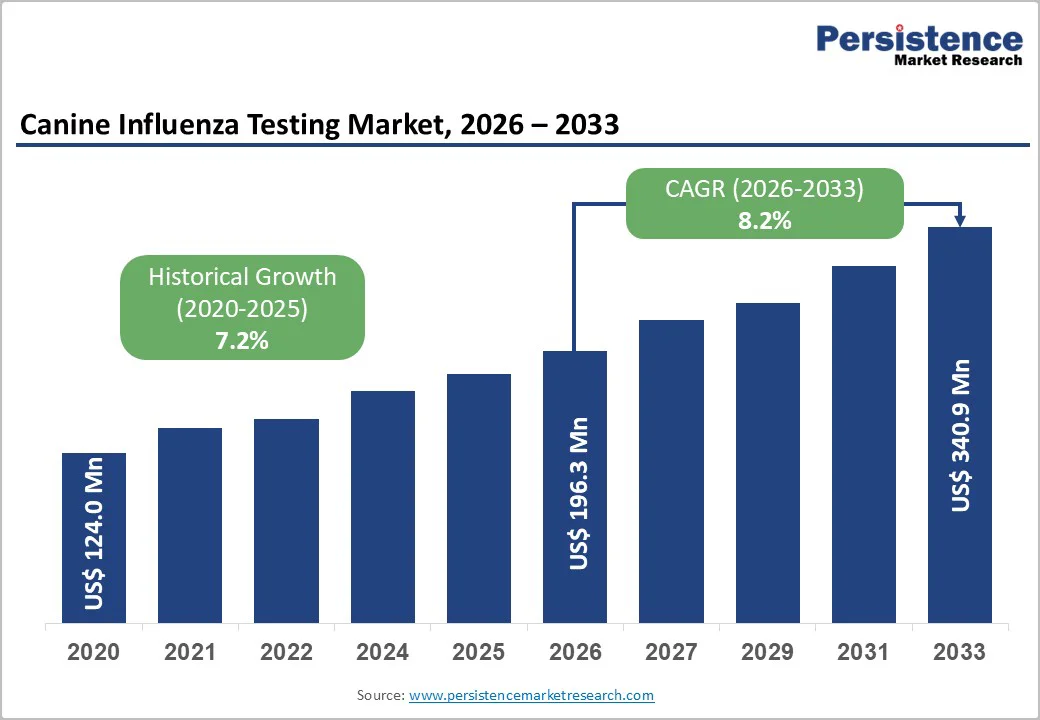

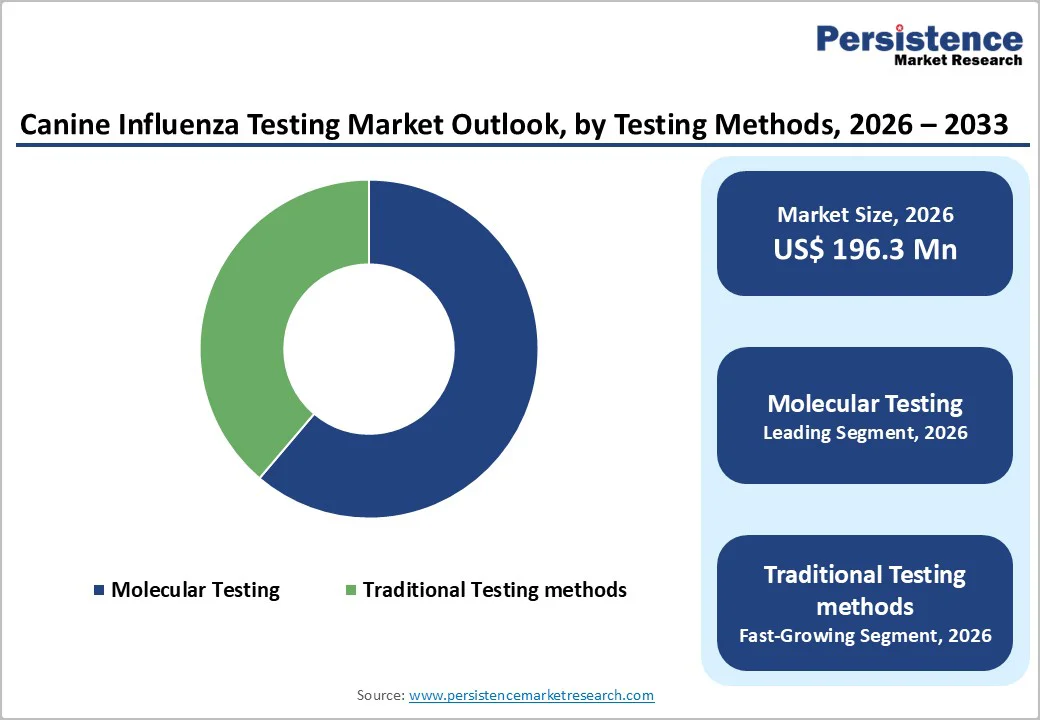

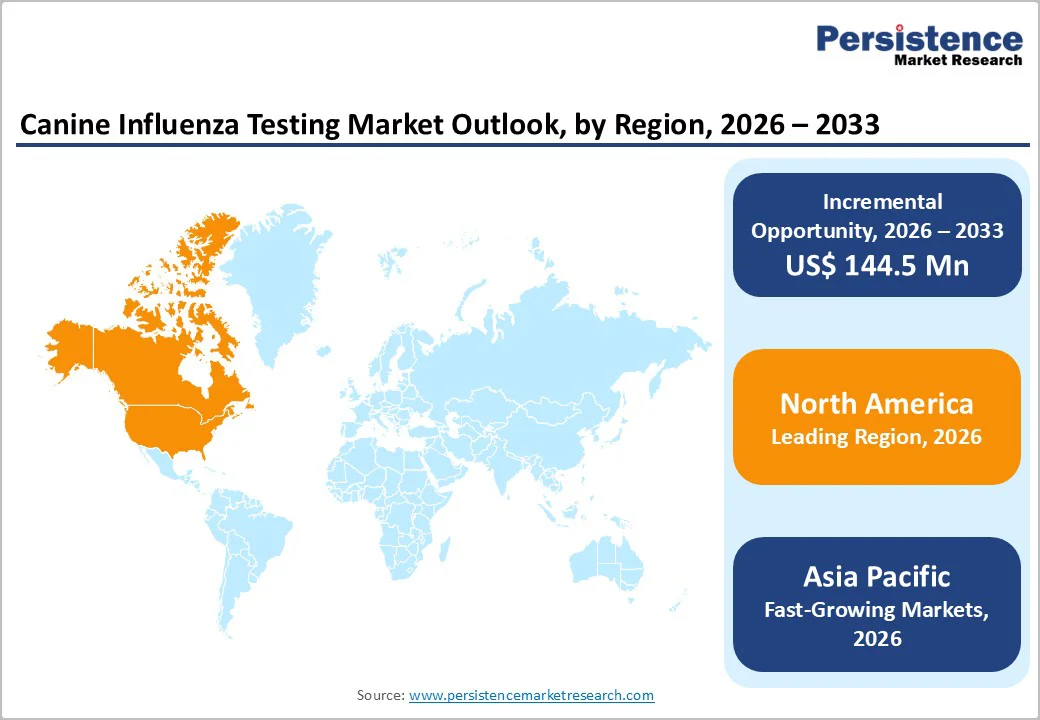

The global Canine Influenza Testing Market is estimated to grow from US$ 196.3 Mn in 2026 to US$ 340.9 Mn by 2033. The market is projected to record a CAGR of 8.2% during the forecast period from 2026 to 2033.

The Canine Influenza Testing Market is growing steadily, driven by rising pet ownership, increased awareness of canine influenza, and demand for accurate diagnostics. North America leads, supported by advanced veterinary infrastructure and funding, while Asia-Pacific grows rapidly due to expanding veterinary services, increasing pet adoption, and rising use of molecular and rapid influenza tests, improving detection and outcomes.

Key Industry Highlights

- Dominant Segment: Molecular testing methods lead the market with 61.2% share in 2025, valued for their high sensitivity, rapid detection of canine influenza virus, and ability to guide timely clinical decisions. They enable accurate diagnosis, support outbreak management, and are widely adopted in veterinary clinics, diagnostic labs, and research facilities.

- Dominant Region: North America holds the largest market share, supported by advanced veterinary infrastructure, widespread pet ownership, and strong funding for animal health research. Asia-Pacific is the fastest-growing region, driven by expanding veterinary services, rising adoption of molecular and rapid tests, and increasing awareness of canine influenza among pet owners.

- Market Drivers: Growth is fueled by rising prevalence of canine influenza outbreaks, increasing demand for accurate and rapid diagnostic tests, expansion of veterinary clinics and diagnostic labs, and adoption of molecular and point-of-care testing technologies.

- Market Opportunity: Key opportunities include the development of multiplex and AI-enabled diagnostic kits, integration with telehealth and veterinary health monitoring platforms, expansion into emerging pet care markets, collaborations with research institutions, and broader applications in preventive veterinary care and epidemiological surveillance.

| Key Insights | Details |

|---|---|

| Global Canine Influenza Testing Market Size (2026E) | US$ 196.3 Mn |

| Market Value Forecast (2033F) | US$ 340.9 Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.2% |

| Historical Market Growth (CAGR 2020 to 2025) | 7.2% |

Market Dynamics

Driver – Rising prevalence of canine influenza outbreaks in pets globally

Rising prevalence and documented outbreaks of canine influenza have increased demand for diagnostic testing, driving market growth. Canine influenza is a respiratory disease caused primarily by influenza A viruses, notably H3N2 and formerly H3N8, which have circulated across dog populations in multiple countries. Meta analyses show influenza A H3N2 prevalence in dogs reaching up to 17.8% in sampled populations, with seroprevalence of approximately 7.44% for H3N2 and 7.96% for H3N8 worldwide, indicating notable viral presence among dogs globally. This persistent circulation, particularly of H3N2, underscores ongoing infection risk and surveillance need.

Outbreak history further illustrates this trend: in the United States, the H3N2 canine influenza virus caused localized outbreaks beginning in 2015, with cases reported across multiple regions and continuing circulation in dog populations. The Centers for Disease Control and Prevention (CDC) notes that H3N2 remains present in dogs, especially in environments such as kennels and shelters, where transmission is facilitated. This documented spread reinforces the need for reliable diagnostics; veterinary clinics and labs increasingly adopt testing to confirm influenza infection, manage cases, and prevent further spread among susceptible canine populations.

Restraints – High cost of advanced molecular and multiplex diagnostic tests

The high cost of advanced molecular diagnostics, such as PCR and multiplex assays, limits adoption in veterinary practice and restrains the canine influenza testing market. Molecular tests require specialized instrumentation, cold-chain reagent handling, and trained technical staff, making them significantly more expensive than traditional methods such as rapid antigen or culture tests. For example, diagnostic labs list PCR-based respiratory panels (analogous to influenza tests) at a fee of around USD 101 per panel. In contrast, basic tests such as ELISAs or individual serology are much cheaper. These elevated prices create barriers for smaller clinics and owners with limited budgets, reducing routine testing uptake.

Government and veterinary lab fee schedules show the inherent cost disparity between molecular and traditional diagnostics, reinforcing this restraint. Many PCR tests for infectious agents in companion animals, including canine respiratory viruses, routinely cost USD 35–$101 per test at university diagnostic labs, reflecting inherent higher costs for molecular assays. At the same time, government laboratory fees for traditional serology and immunoassays are often markedly lower. In broader infectious disease diagnostics, costs for molecular panels are often reported as 3–5 times those of conventional diagnostics, further deterring routine use in cost-sensitive regions. The need for expensive infrastructure also disproportionately affects rural or resource-limited clinics.

Opportunity – Development of rapid, multiplex, and AI-enabled diagnostic kits

The development of rapid and multiplex diagnostic kits presents a significant opportunity by enhancing diagnostic efficiency and expanding testing capabilities. In veterinary infectious disease diagnostics, more than 30 multiplex PCR panels and over 200 rapid immunodiagnostic kits were introduced globally between 2023 and 2025, allowing simultaneous detection of multiple pathogens, including respiratory viruses, in a single assay. Multiplex real-time PCR assays have been developed to detect canine influenza alongside other respiratory pathogens with high sensitivity and specificity, thereby improving surveillance and differential diagnosis in clinical settings. These innovations reduce time to result and operational complexity, encouraging broader adoption in veterinary practices.

AI-enabled diagnostic interpretation and point-of-care molecular platforms further expand the opportunity landscape by increasing accuracy and decentralizing testing. In human influenza diagnostics, the CDC has highlighted rapid molecular assays that deliver results in 15–30 minutes and multiplex assays that detect multiple viruses simultaneously, illustrating the potential translation of such technology to veterinary contexts. Additionally, research shows AI augmented systems can interpret lateral flow assays in 1–2 minutes with accuracy above 96%, significantly reducing human error and enhancing field applicability. These technological trends can be harnessed for canine influenza diagnostics, offering faster, more reliable testing and supporting surveillance and outbreak management.

Category-wise Analysis

By Testing Method, Molecular Testing Dominates the Canine Influenza Testing Market

Molecular testing dominates with a 61.2% share in 2025, as it offers superior sensitivity and specificity compared with traditional diagnostic methods. PCR and RT PCR assays detect viral RNA even at low concentrations, enabling early and accurate identification of canine influenza infections, which is critical for timely intervention and outbreak control. The CDC notes that molecular influenza assays provide more reliable results than antigen detection or culture, with turnaround times ranging from 15 to 90 minutes, making them ideal for clinical and shelter environments. Veterinary diagnostic labs, including university centers like Cornell’s AHDC, emphasize PCR as the gold standard because it differentiates influenza from other respiratory pathogens, ensures precise diagnosis, and informs effective treatment, driving its widespread adoption across veterinary clinics and research facilities.

By Application, Flu dominates due to high contagion, targeted detection, early diagnosis, and outbreak prevention.

Flu dominates the canine influenza testing Market because canine influenza is a highly contagious respiratory disease caused by specific influenza A viruses (H3N2 and H3N8), requiring targeted diagnostic testing. According to the CDC, outbreaks occur rapidly in settings such as kennels, shelters, and veterinary clinics, causing symptoms ranging from cough and fever to severe respiratory distress, making accurate influenza testing critical for disease control. Epidemiological studies indicate a pooled prevalence of influenza A in dogs of around 12%, with PCR and serology confirming active infections globally. Consequently, veterinarians prioritize influenza testing over general respiratory diagnostics to ensure early detection, guide treatment, implement isolation, and prevent outbreaks, establishing flu as the dominant application segment.

Regional Insights

North America Canine Influenza Testing Market Trends

North America dominates the Canine Influenza Testing Market with 45.5% share in 2025, because of high companion dog ownership and well-established veterinary care practices. In the United States, approximately 66% of households own pets, with about 65.1 million households owning at least one dog, reflecting a large base of animals that routinely receive veterinary care, including infectious disease diagnostics. Routine veterinary visits, preventive care guidance, and robust public awareness about pet health encourage influenza testing as part of respiratory disease management. Additionally, North America’s advanced diagnostic infrastructure, widespread availability of PCR and laboratory services, and proactive animal health practices lead to more frequent influenza testing than in regions with lower dog ownership or limited veterinary services.

Europe Canine Influenza Testing Market Trends

Europe is an important region in the Canine Influenza Testing Market due to high pet ownership and extensive veterinary healthcare infrastructure. As of 2023, an estimated 139 million European households (49%) owned one or more pets, with over 106 million dogs across the region, reflecting a substantial canine population requiring healthcare services. This growing dog population drives demand for diagnostic testing, including influenza screening, as owners pursue preventive and disease-specific care. Veterinary services in Europe are well developed, with strong institutional support, standardized animal health regulations, and expanding diagnostic capabilities in countries like Germany, France, and the UK, facilitating routine infectious disease testing. This combination of a large dog population and structured veterinary care makes Europe a key region for canine influenza diagnostics.

Asia-Pacific Canine Influenza Testing Market Trends

Asia Pacific is the fastest-growing region in the canine influenza testing market, driven by rising pet ownership, increasing disposable incomes, and expanding veterinary services. Across key Asia-Pacific countries such as China and India, the pet population has grown substantially, with China alone home to over 58 million dogs, and broader regional ownership is increasing as urban households adopt pets for companionship and family roles. This surge in pet numbers drives demand for enhanced veterinary healthcare, including diagnostics for infectious diseases like canine influenza, supported by greater awareness of animal health and preventive care. There is also growing investment in veterinary infrastructure and diagnostic technologies, especially in urban centers, enabling more comprehensive testing availability and uptake

Market Competitive Landscape

Leading applications in the canine influenza testing market focus on accurate influenza detection, outbreak management, and timely clinical intervention. Rapid and molecular diagnostics enable early virus identification, support treatment decisions, and improve infection control. High adoption in veterinary clinics, shelters, and diagnostic labs enhances disease surveillance, drives market growth, and increases acceptance of advanced testing methods globally.

Key Industry Developments:

- In October 2024, QIAGEN received FDA clearance for its QIAstat-Dx Mini Panel, aiming to enhance precision in outpatient respiratory diagnostics. The approval allows healthcare providers to quickly and accurately detect multiple respiratory pathogens, supporting timely and targeted treatment decisions.

- In June 2024, The USDA approved Merck Animal Health’s NOBIVAC® NXT Canine Flu H3N2, marking it as the first and only RNA-particle technology vaccine for canine influenza. The authorization allows veterinarians to use this innovative vaccine to protect dogs against H3N2 influenza virus, offering enhanced immune response and improved disease prevention.

Companies Covered in Canine Influenza Testing Market

- Qiagen

- Merck&Co

- Abaxis

- ThermoFisher Scientific

- Rapigen

- Neogen Dutch Diagnostics

- Fassisi

- Zoetis

- EUROFINSTECHNOLOGIES

- iNtRON Biotechnology

- Biopanda Reagents

- Heska Corporation

- Ubio Biotechnology Systems

- Idexx Laboratories

- Abbott

- Roche

- Coris Bioconcept

- Life Bioscience

- Others

Frequently Asked Questions

The global Canine Influenza Testing Market is projected to be valued at US$ 196.3 Mn in 2026.

Rising canine influenza prevalence, increased pet ownership, advanced diagnostics, veterinary awareness, and demand for rapid testing.

The global Canine Influenza Testing Market is poised to witness a CAGR of 8.2% between 2026 and 2033.

Development of rapid, multiplex, AI-enabled tests, emerging markets expansion, preventive care, and veterinary research collaborations.

Qiagen, Merck&Co., Abaxis, Thermo Fisher Scientific, Rapigen, NeogenDutch Diagnostics/