- Nutraceuticals & Functional Foods

- Hydration Supplement Market

Hydration Supplement Market Size, Share, and Growth Forecast, 2026 - 2033

Hydration Supplement Market by Form (Powders, RTD Liquids, Tablets, Concentrates & Syrups, ORS, Gels & Chews), Application (Sports & Performance, Clinical/Medical, Everyday Wellness, Travel/Heat Exposure, Pediatrics & Geriatrics), Ingredient System (Electrolytes-Only, Electrolytes + Carbohydrates, Electrolytes + Amino Acids, Electrolytes + Vitamins/Minerals, Natural-Source Hydration, Personalized Blends), and Regional Analysis for 2026 - 2033

Hydration Supplement Market Share and Trends Analysis

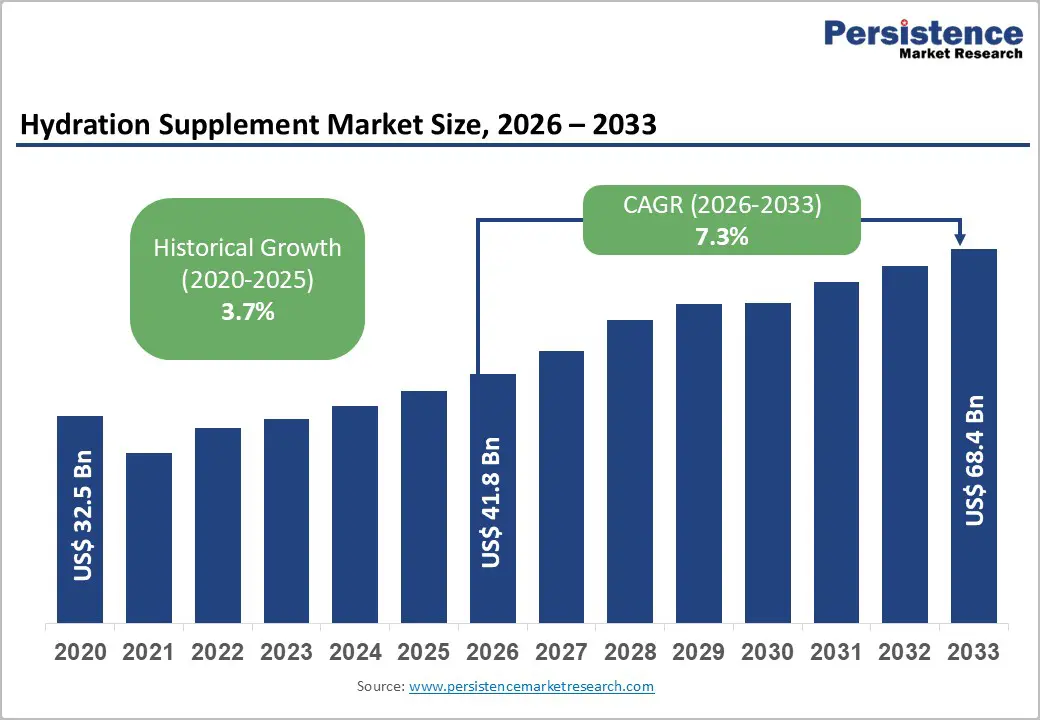

The global hydration supplement market size is likely to be valued at US$ 41.8 billion in 2026, and is estimated to reach US$ 68.4 billion by 2033, growing at a CAGR of 7.3% during the forecast period 2026 - 2033. The market has been expanding steadily as heat exposure has risen, physical activity participation has grown, and clinical awareness of dehydration risks have increased.

Electrolyte beverages and oral rehydration solutions (ORS) have experienced sales growth from 2020 to 2024, while large beverage multinationals have reported mid-single-digit annual revenue growth in their functional hydration portfolios. The World Health Organization (WHO) has highlighted diarrheal diseases as a key driver of dehydration-related mortality worldwide, which sustains baseline ORS demand. Meanwhile, the Centers for Disease Control and Prevention (CDC) has noted increases in sports participation and heat-related illnesses in the United States. Real income recovery across major economies has supported discretionary wellness spending since post-2022 inflationary pressures eased, per International Monetary Fund (IMF) data.

Companies such as PepsiCo and The Coca-Cola Company continue to allocate capital toward functional beverages, including hydration brands such as Gatorade and Powerade, according to their U.S. Securities and Exchange Commission (SEC) filings. Regulatory authorities, including the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), have been enforcing labeling standards that shape formulations and compliance costs. As hydration supplements shift from sports-focused use to everyday wellness routines, clinical demand will remain stable in developing markets. Demographic changes, urbanization, and climate volatility will further drive growth, with investments targeting premium clean-label products and e-commerce channels.

Key Industry Highlights

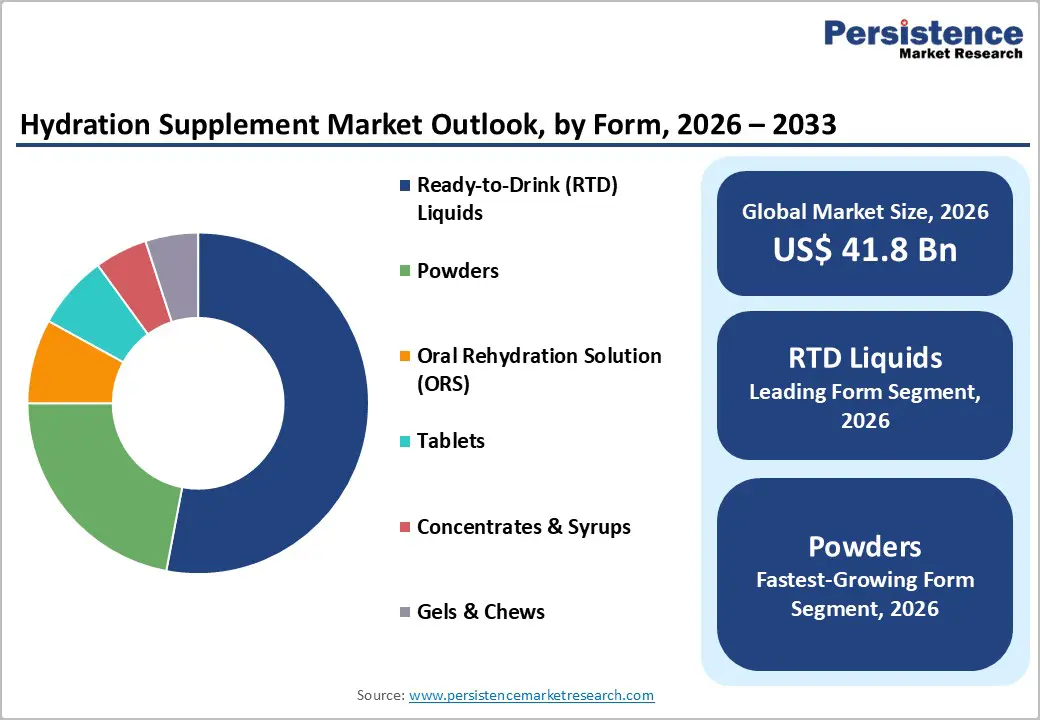

- Leading Form: Ready-to-drink (RTD) liquids are expected to lead with roughly 53% revenue share in 2026, supported by strong retail penetration across supermarkets and convenience channels.

- Top Application: Sports and performance hydration supplements are projected to dominate with an estimated 41.5% revenue share in 2026, reflecting established athlete-focused brand ecosystems and sponsorship-driven demand.

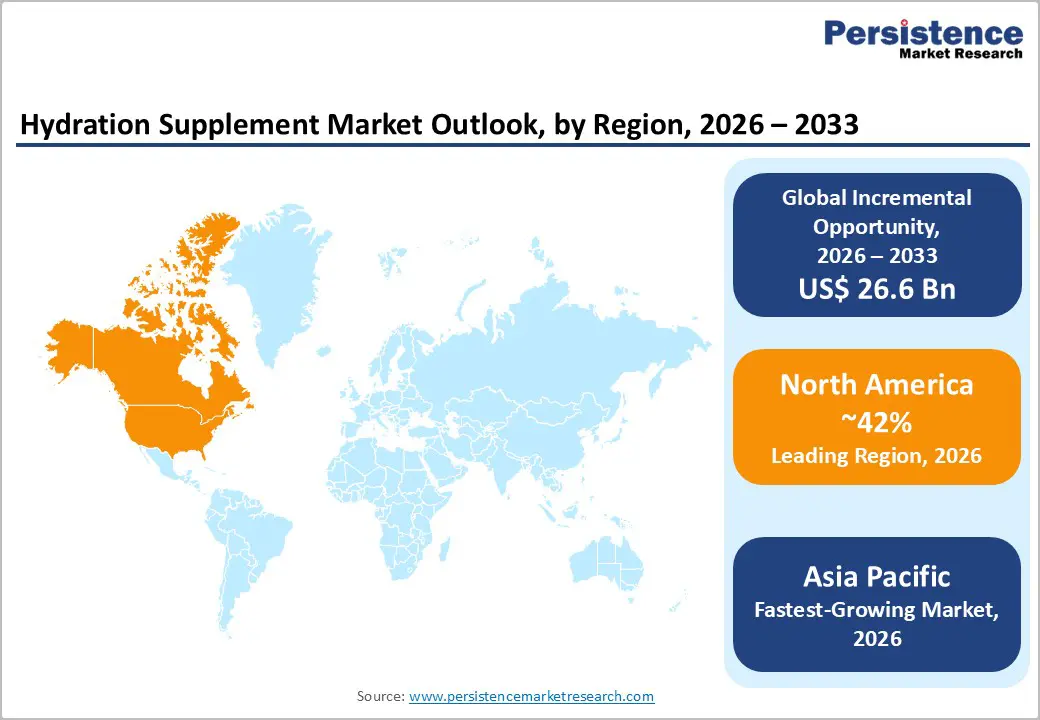

- Dominant Region: North America is projected to account for nearly 42% of the market in 2026, supported by high per-capita functional beverage consumption and advanced retail infrastructure.

- Fastest-Growing Application: Everyday wellness hydration is projected to deliver a 2026 - 2033 CAGR of roughly 8%, driven by consumers repositioning electrolyte products as part of preventive health routines.

- July 2025: Liquid Death rolled out a new energy drink line called Liquid Death Sparkling Energy, expanding beyond its core canned water offerings.

| Key Insights | Details |

|---|---|

| Hydration Supplement Market Size (2026E) | US$ 41.8 Bn |

| Market Value Forecast (2033F) | US$ 68.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Heat Exposure and Climate-Linked Dehydration Risk

The WHO reported a sustained increase in the frequency and severity of heatwaves worldwide. The World Meteorological Organization (WMO) has confirmed that recent years are ranking among the warmest on record, and temperature irregularities are continuing across multiple regions. The CDC has observed a rise in emergency department visits linked to heat stress in the United States. These developments are indicating that heat exposure is becoming a structural public health concern rather than a seasonal anomaly. Urbanization is accelerating, particularly in Asia and Africa, and a growing share of the workforce is operating in outdoor environments such as construction, logistics, and agriculture. As a result, dehydration risk is increasing across both developed and emerging economies. Public authorities are issuing more frequent heat advisories, and employers are strengthening workplace hydration protocols. This environment is steadily reinforcing demand for electrolyte replenishment solutions across retail, pharmacy, and institutional supply chains.

Climate variability is reshaping how consumers and organizations are perceiving hydration. Instead of associating electrolyte supplements solely with athletic recovery, buyers are viewing them as preventive health tools that support cognitive clarity, physical endurance, and safety in high-temperature settings. Construction companies, defense departments, and emergency response agencies are expanding procurement volumes to mitigate operational risk. Corporate wellness programs are also integrating hydration support into occupational health strategies. Manufacturers are responding by refining their product portfolios toward rapid absorption, clean-label positioning, and natural-ingredient sourcing. Brands that align convenience with transparent formulation standards will strengthen credibility as regulators continue to monitor product claims under frameworks such as those of the U.S. FDA and EFSA. Companies that anticipate sustained heat exposure and embed hydration into broader preventive care strategies will have positioned themselves effectively for long-term demand resilience.

Shift toward Preventive Wellness Consumption

Data from the International Monetary Fund (IMF) indicate that disposable income levels across North America and Europe are stabilizing after pandemic-related disruption. As household finances recover, consumers are reallocating budgets toward preventive health and functional nutrition categories. Public filings submitted to the SEC show that PepsiCo is reporting consistent performance across its hydration brands such as Gatorade and Propel. Unilever PLC has also disclosed expansion within its hydration supplement portfolio following the acquisition of Liquid I.V. These disclosures confirm that leading corporations are treating functional hydration as a strategic growth vertical rather than a peripheral product line. Capital allocation toward marketing, distribution, and product innovation is reinforcing this positioning.

Consumer perception is evolving alongside income recovery. Buyers are associating hydration with mental focus, physical restoration, and sustained daily efficiency rather than limiting usage to sports participation. This shift is broadening total addressable demand and supporting higher purchase frequency. Regulatory authorities such as the U.S. FDA and the EFSA are actively regulating health claims, which is prompting companies to reformulate with compliant levels of vitamins, minerals, and electrolytes. Manufacturers are embedding hydration products into structured wellness routines, and subscription-based purchasing models are increasing retention and lifetime value. Organizations that align product development with compliant fortification strategies and evidence-based positioning will strengthen trust while capturing incremental demand from non-athletic consumers.

Regulatory Claim Restrictions and Labeling Scrutiny

The U.S. FDA strictly regulates electrolyte beverages under federal food labeling laws and restricts disease-treatment claims unless products meet the standards applied to ORS. The EFSA also conducts rigorous scientific assessments before approving nutrient and health claims within the European Union (EU). Companies must substantiate statements about hydration, recovery, or physiological benefits using compliant language and approved nutrient thresholds. Products that suggest medical efficacy without proper classification are attracting regulatory scrutiny. Enforcement actions are resulting in warning letters, product relabeling, and potential market withdrawal. As oversight is intensifying, manufacturers are revising packaging language and reformulating ingredient compositions to align with permissible claims frameworks.

Compliance requirements are increasing operational complexity, particularly for smaller firms that lack dedicated regulatory teams. Labeling audits, scientific substantiation reviews, and documentation management are raising fixed costs and extending product development timelines. Ingredient sourcing is also under closer scrutiny, particularly for micronutrients and functional additives that trigger claim validation. These obligations are raising entry barriers and slowing the pace at which new brands can scale distribution. Retailers are prioritizing suppliers with strong compliance records to mitigate reputational and legal exposure.

Input Cost Volatility and Supply Chain Exposure

The Food and Agriculture Organization (FAO) Food Price Index indicates sustained volatility in sugar and other agricultural inputs between 2021 and 2024. Fluctuations in crop yields, energy prices, and trade policies continue to affect raw material costs. Electrolyte minerals such as magnesium and potassium rely on mining output and global logistics networks, which are exposed to geopolitical disruption and transportation bottlenecks. The concentration of supply in specific producing countries increases vulnerability to export restrictions and freight delays. These factors are creating procurement uncertainty and limiting the predictability of input pricing for hydration supplement manufacturers. Companies are diversifying supplier bases and negotiating longer-term contracts to stabilize sourcing conditions.

Packaging expenditure remains above pre-2020 benchmarks. Polyethylene terephthalate (PET) resin prices are responding to crude oil movements, which are introducing variability into bottle manufacturing costs. Transportation and energy expenses are adding further pressure across distribution chains. In price-sensitive markets, consumers are responding to higher retail prices by shifting toward private-label alternatives. Supermarket chains are expanding store-brand electrolyte offerings, intensifying competitive dynamics. Manufacturers are adjusting cost pass-through strategies carefully to avoid demand erosion. Firms that are strengthening supply chain resilience, improving production efficiency, and exploring lightweight packaging innovations will better protect margins while sustaining market presence.

Emerging Market Clinical Hydration Penetration

The WHO recognizes oral rehydration therapy as a critical intervention for reducing child mortality linked to diarrheal disease when timely access is ensured. The United Nations Children’s Fund (UNICEF) has been scaling ORS distribution programs across Sub-Saharan Africa and South Asia to strengthen community-level treatment coverage. Public health agencies are integrating ORS into essential medicine lists and primary care protocols, which is reinforcing baseline demand. At the same time, rapid urbanization in countries such as India, Indonesia, and Nigeria is expanding pharmacy networks and organized retail healthcare outlets. Governments are investing in broader dehydration prevention campaigns and maternal-child health initiatives, thereby increasing awareness and access to rehydration products.

As healthcare infrastructure improves and urban consumers gain greater access to formal retail channels, commercial ORS brands are entering mainstream pharmacy shelves alongside institutional supplies. The hospital and public procurement channels remain stable due to continued government and donor funding. However, privately branded over-the-counter (OTC) ORS products are gaining visibility in urban markets where consumers are seeking convenient, ready-to-use formats. Manufacturers are differentiating through flavored formulations, improved packaging, and clearer dosage guidance while remaining aligned with regulatory standards. Companies that are combining clinical credibility with retail accessibility will strengthen penetration in emerging economies where public health policy and consumer demand are converging.

Digital Direct-to-Consumer Expansion

Global e-commerce adoption is expanding steadily as digital infrastructure improves across both developed and emerging economies. The World Bank reports rising internet penetration rates in developing regions, which is broadening access to online retail platforms. As connectivity improves, consumers are becoming more comfortable purchasing health and nutrition products through digital channels. In North America and Europe, subscription-based hydration supplement programs are gaining traction as buyers seek convenience and predictable replenishment cycles. Companies are integrating data analytics tools to monitor purchasing behavior, optimize inventory planning, and design personalized electrolyte blends tailored to lifestyle profiles. This digital integration is strengthening customer insight and enabling faster product iteration.

D2C distribution models are reducing dependence on traditional retail intermediaries and improving gross margin structures. Digital marketing strategies are allowing brands to target specific consumer segments such as endurance athletes, remote workers, and preventive wellness adopters through performance-based advertising. Customer acquisition costs are becoming more measurable, and retention strategies are relying on automated reorder systems and loyalty incentives. As repeat purchase frequency increases, firms are enhancing lifetime customer value while stabilizing revenue streams. Organizations that are investing in secure payment systems, responsive logistics networks, and compliant online health communication will strengthen competitive positioning in an increasingly digital marketplace.

Category-Wise Analysis

Form Insights

Ready-to-drink liquids are likely to lead with an estimated 53% of the hydration supplement market revenue share in 2026. SEC filing data confirm that RTD hydration beverages are the largest revenue-generating products within functional drink portfolios of several top brands. This format benefits from immediate consumption, standardized dosing, and strong in-store visibility across supermarkets, hypermarkets, and convenience outlets. Retailers are allocating prominent shelf placement to established RTD brands because of high turnover rates and brand recognition. Cold-chain distribution capabilities in developed markets are further reinforcing RTD dominance. Companies are continuing to invest in packaging innovation and low-sugar reformulation to maintain compliance with regulatory guidance while preserving consumer appeal.

Powdered hydration supplements are set to be the fastest-growing form from 2026 to 2033. Online sales performance and corporate disclosures indicate rising adoption of single-serve stick packs and bulk powder containers due to portability and lower unit costs. Powders are significantly reducing transportation weight and warehousing requirements, which is improving contribution margins under D2C distribution models. Subscription-based purchasing structures are encouraging repeat consumption and predictable revenue streams. Manufacturers are expanding flavor portfolios and clean-label formulations to attract wellness-oriented buyers. Brands that are aligning digital distribution capabilities with lightweight packaging and personalized electrolyte blends will likely sustain accelerated growth in this segment over the coming years.

Form Insights

Ready-to-drink liquids are likely to lead with an estimated 53% of the hydration supplement market revenue share in 2026. SEC filing data confirm that RTD hydration beverages are the largest revenue-generating products within functional drink portfolios of several top brands. This format benefits from immediate consumption, standardized dosing, and strong in-store visibility across supermarkets, hypermarkets, and convenience outlets. Retailers are allocating prominent shelf placement to established RTD brands because of high turnover rates and brand recognition. Cold-chain distribution capabilities in developed markets are further reinforcing RTD dominance. Companies continue to invest in packaging innovation and low-sugar reformulation to maintain regulatory compliance while preserving consumer appeal.

Powdered hydration supplements are set to be the fastest-growing form from 2026 to 2033. Online sales performance and corporate disclosures indicate rising adoption of single-serve stick packs and bulk powder containers due to portability and lower unit costs. Powders are significantly reducing transportation weight and warehousing requirements, which is improving contribution margins under D2C distribution models. Subscription-based purchasing models encourage repeat purchases and provide predictable revenue streams. Manufacturers are expanding flavor portfolios and clean-label formulations to attract wellness-oriented buyers. Brands that are aligning digital distribution capabilities with lightweight packaging and personalized electrolyte blends will likely sustain accelerated growth in this segment over the coming years.

Application Insights

Sports and performance applications are poised to dominate in 2026, commanding approximately 41.5% of the hydration supplement market share. Data from the CDC and Eurostat indicate sustained participation in organized sports, recreational fitness, and endurance events across major economies. This consistent engagement is reinforcing baseline consumption of electrolyte beverages and recovery formulations. Large beverage corporations are maintaining investment in athlete endorsements, sports league partnerships, and event sponsorships to preserve brand visibility and loyalty. These marketing strategies are strengthening the association between hydration products and physical performance outcomes. Retail distribution networks are also aligning promotions with sporting calendars, which is supporting recurring seasonal demand.

Everyday wellness is projected to be the fastest-growing application area over the 2026-2033 forecast period, with a CAGR of nearly 8%. Brands are repositioning hydration supplements to appeal to office professionals, frequent travelers, and health-conscious consumers who are prioritizing daily energy and cognitive clarity. Companies are introducing low-sugar and micronutrient-fortified variants that align with routine health maintenance rather than competitive athletics. This broader positioning is expanding the addressable consumer base and encouraging more frequent usage occasions. Market players that are integrating hydration into general wellness narratives and preventive health strategies will likely capture incremental demand outside core athletic segments.

Sports and performance applications are poised to dominate in 2026, commanding approximately 41.5% of the hydration supplement market share. Data from the CDC and Eurostat indicate sustained participation in organized sports, recreational fitness, and endurance events across major economies. This consistent engagement is reinforcing baseline consumption of electrolyte beverages and recovery formulations. Large beverage corporations are maintaining investment in athlete endorsements, sports league partnerships, and event sponsorships to preserve brand visibility and loyalty. These marketing strategies are strengthening the association between hydration products and physical performance outcomes. Retail distribution networks are also aligning promotions with sporting calendars, which is supporting recurring seasonal demand.

Everyday wellness is projected to be the fastest-growing application area over the 2026-2033 forecast period, with a CAGR of nearly 8%. Brands are repositioning hydration supplements to appeal to office professionals, frequent travelers, and health-conscious consumers who are prioritizing daily energy and cognitive clarity. Companies are introducing low-sugar and micronutrient-fortified variants that align with routine health maintenance rather than competitive athletics. This broader positioning is expanding the addressable consumer base and encouraging more frequent usage occasions. Market players that integrate hydration into broader wellness narratives and preventive health strategies will likely capture incremental demand beyond core athletic segments.

Regional Insights

North America Hydration Supplement Market Trends

North America is slated to remain the largest regional market for hydration supplements through 2033, forecasted to capture a share of roughly 42% in 2026 and supported by the concentration of leading beverage manufacturers and established retail networks. Global giants such as The Coca-Cola Company report that a substantial portion of hydration-related revenue is originating from the United States. The region benefits from widespread participation in organized sports, fitness programs, and outdoor recreational activities. Advanced supermarket chains, convenience outlets, and specialty nutrition stores are ensuring strong product visibility and rapid inventory turnover. Premiumization trends are influencing consumer preferences, with buyers demonstrating willingness to pay higher prices for clean-label formulations and functional enhancements.

Regulatory oversight from the U.S. FDA is shaping product labeling, health claims, and formulation standards, which is reinforcing compliance discipline across the industry. Direct-to-consumer channels are expanding as brands strengthen digital storefronts and subscription models. Investment activity is continuing across marketing partnerships, research and development initiatives, and distribution optimization. Venture funding and corporate acquisitions are supporting portfolio diversification and innovation. Companies that are aligning regulatory compliance with omnichannel distribution strategies and premium positioning will continue consolidating leadership within the North American hydration supplement landscape.

Europe Hydration Supplement Market Trends

In Europe, market dynamics for hydration supplements is undergoing significant evolutions as companies respond to guidance from the EFSA and broader public health initiatives targeting sugar reduction. Regulatory evaluation of nutrient and health claims is shaping ingredient selection and marketing language across hydration supplements. In the United Kingdom, fiscal measures such as sugar levies are influencing innovation strategies, prompting manufacturers to reduce added sugars and introduce low-calorie electrolyte formulations. These policy interventions are encouraging research and development investment in alternative sweeteners and balanced micronutrient profiles. As governments continue prioritizing obesity prevention and chronic disease management, hydration brands are aligning portfolios with compliance-driven reformulation standards.

Retail consolidation across European markets is strengthening the bargaining power of major supermarket chains. Private-label electrolyte beverages and hydration powders are expanding shelf presence, intensifying price competition. Established brands are responding through differentiated positioning based on ingredient transparency, clinical validation, and sustainable packaging. Although demand for functional hydration is remaining stable, regulatory oversight and pricing pressure are moderating expansion rates compared to less regulated regions. Companies that are coupling compliant formulation practices with strong retailer partnerships and value-added product attributes will sustain competitive resilience within the European hydration supplement market.

Asia Pacific Hydration Supplement Market Trends

The market in Asia Pacific is anticipated to register the highest 2026-2033 CAGR of approximately 8.7%, fueled by rapid urban expansion and rising exposure to high temperatures, which are increasing awareness of dehydration risks. The WHO provides robust support for dehydration prevention initiatives across South Asia through public health campaigns and community-level access to ORS. Surging population density in metropolitan centers is elevating demand for convenient electrolyte products that support daily mobility and outdoor activity. Governments are strengthening healthcare outreach and maternal-child health programs, which are reinforcing baseline rehydration awareness. Climate variability is further contributing to sustained demand across both institutional procurement and consumer retail channels.

Retail pharmacy networks are expanding in countries such as India, Indonesia, and Vietnam, improving access to distribution for commercial hydration supplements. At the same time, digital commerce platforms are gaining scale as internet penetration increases across the region. Rising middle-class income levels are enabling greater discretionary spending on preventive health products. Consumers are increasingly viewing electrolyte supplements as part of routine wellness management rather than episodic treatment. Manufacturers that combine affordable pricing strategies with locally adapted formulations and strong digital engagement will capture long-term growth opportunities in the Asia-Pacific hydration supplement market.

Competitive Landscape

The global hydration supplement market structure is exhibiting moderate concentration among leading multinational corporations. PepsiCo and The Coca-Cola Company control a significant share of the RTD liquid space through established brands and extensive distribution systems. Their scale advantages in procurement, marketing investment, and retail partnerships are reinforcing category leadership. Unilever PLC is strengthening its position through the expansion of Liquid I.V., which is benefiting from direct-to-consumer penetration and premium pricing strategies. These firms are leveraging global supply chains and brand equity to defend shelf space and negotiate favorable retail terms. Market leadership is therefore depending not only on product formulation but also on distribution reach and marketing intensity.

Private-label electrolyte beverages and powders are also gaining traction across Europe and North America. Large retail chains are introducing competitively priced alternatives that appeal to cost-conscious consumers. Although entry barriers are not prohibitive, new entrants must invest significantly in brand development, regulatory compliance, and logistics capabilities to achieve scale. Innovation efforts are concentrating on sugar reduction, natural ingredient sourcing, and transparent labeling to meet evolving consumer expectations and regulatory scrutiny.

Key Industry Developments

- In October 2025, PepsiCo expanded its sports-nutrition lineup by enhancing its Protein portfolio with new innovations under Muscle Milk and Propel brands, aiming to strengthen position in both recovery and performance segments. The company is also introducing co-branded products with Starbucks to broaden distribution and meet growing consumer demand for functional protein and hydration options.

- In August 2025, Liquid I.V. launched a new sugar-free version of its Hydration Multiplier electrolyte powder in Canada, introducing a White Peach-flavored option formulated to deliver enhanced hydration without sugar to meet local consumer demand. The product is rolling out in retail outlets such as Costco and will soon be available online, marking a notable expansion of the brand’s Canadian portfolio.

- In July 2025, Otsuka Pharmaceutical launched the sale of POCARI SWEAT, a balanced electrolyte beverage formulated to replenish fluids and ions lost through perspiration, in India to support hydration and everyday health. The product will be distributed through local retail channels and is backed by Otsuka’s global expertise in fluid and electrolyte science.

Companies Covered in Hydration Supplement Market

- PepsiCo, Inc.

- The Coca-Cola Company

- Unilever PLC

- Abbott Laboratories

- GlaxoSmithKline plc

- Nestlé S.A.

- Danone S.A.

- Herbalife Ltd.

- Otsuka Holdings Co., Ltd.

- Amway Corp.

- Prestige Consumer Healthcare Inc.

- Church & Dwight Co., Inc.

- The Kraft Heinz Company

- Suntory Holdings Limited

Frequently Asked Questions

The global hydration supplement market is projected to reach US$ 41.8 billion in 2026.

Increasing mortality caused by diarrheal diseases, rise in sports participation, and growing incidence of heat-related illnesses are driving the market.

The market is poised to witness a CAGR of 7.3% from 2026 to 2033.

Widening allocation of capital by large companies toward functional beverages, strict enforcement of labeling standards by regulatory authorities, and shift of hydration supplements from sports-focused use to everyday wellness routines are creating new market opportunities.

PepsiCo, Inc., The Coca-Cola Company, Unilever PLC, and Abbott Laboratories are some of the key players in the market.