- Renewable Energy

- Off-grid Hybrid Power System Market

Off-grid Hybrid Power System Market Size, Share, and Growth Forecast 2026 – 2033

Off-grid Hybrid Power System by Component (Solar PV, Wind Turbine), by System Configuration (Solar-Diesel, Solar-Wind-Diesel, Wind-Diesel), by Application (Residential, Commercial, Industrial), and Regional Analysis 2026 – 2033

Off-grid Hybrid Power System Market Size and Trends Analysis

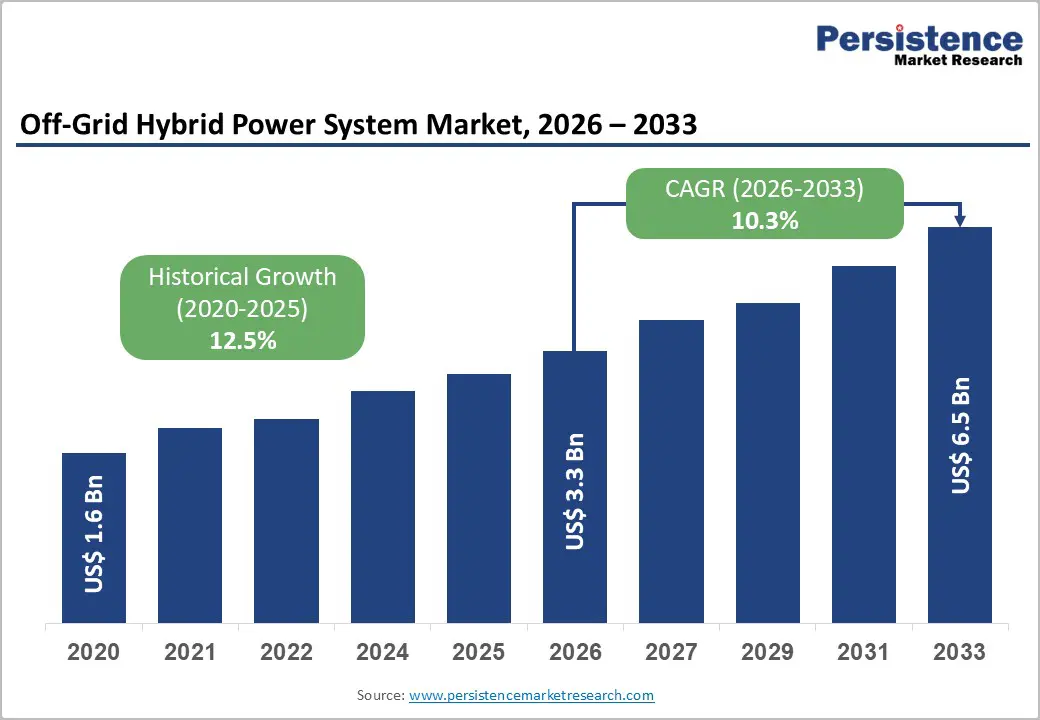

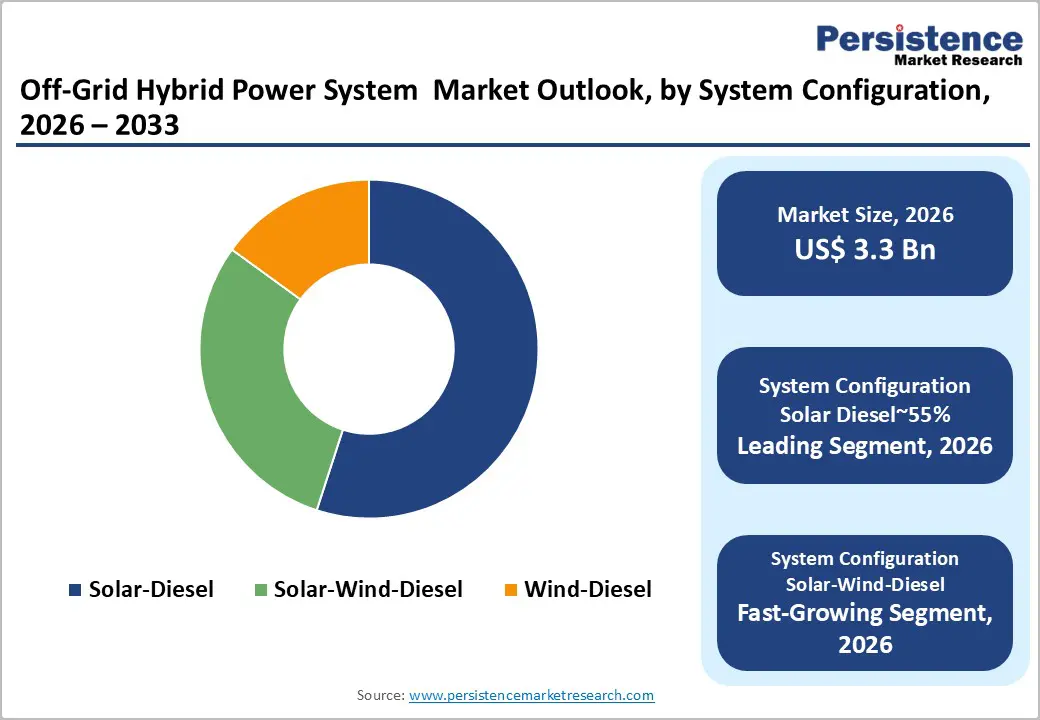

The global off-grid hybrid power system market is expected to be valued at US$3.3 billion in 2026 and is projected to reach US$6.5 billion by 2033, reflecting a CAGR of 10.3% during the forecast period from 2026 to 2033, driven by decreasing costs of renewable energy, increasing rural electrification initiatives, and advancements in energy storage technologies that improve both system reliability and operational efficiency.

The market outlook is presented in present-future terms and is positioned within a broad, neutral global scope without application or regional narrowing.

Key Industry Highlights:

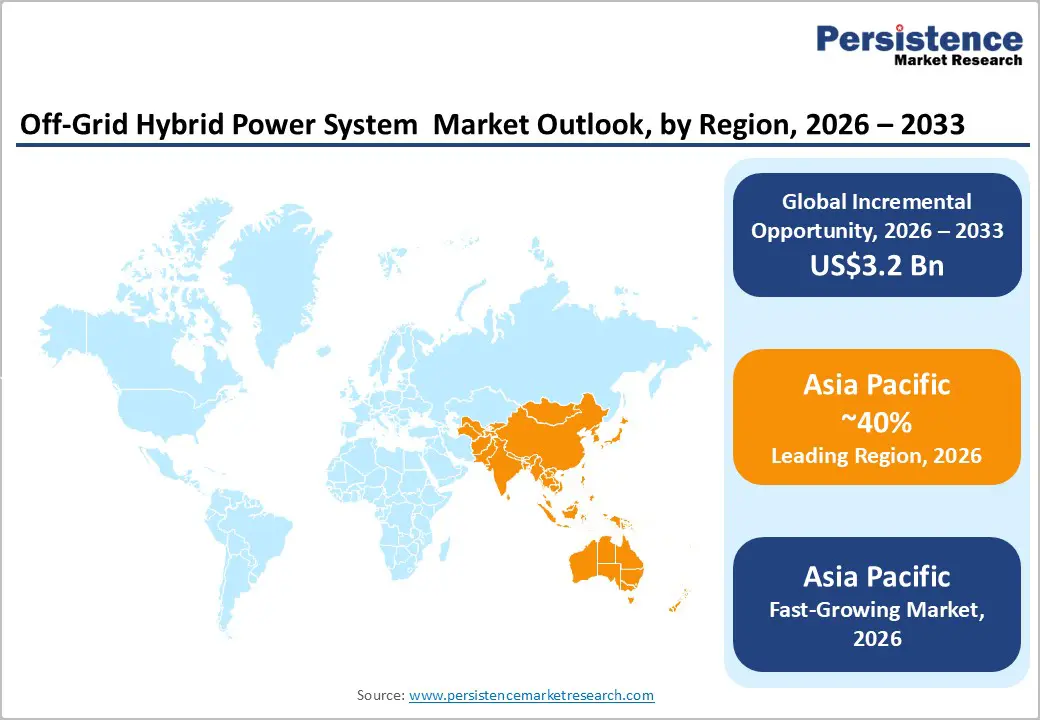

- Leading and Fastest-growing Region : Asia Pacific, with approximately 40% share of the global market, due to rapid expansion in rural electrification, industrial infrastructure, and island microgrid projects, technology adoption, and ecosystem advantages .

- Leading System Configuration: Solar-diesel hybrid systems are projected to dominate for simplicity, cost, adoption, and functional use across key sectors with approximately 55% market share.

- Leading Application: Commercial applications are projected to dominate due to versatility, cost-efficiency, and suitability across use-cases, with approximately 41% market share.

- Key Industry Developments: Policy-led renewable energy mandates and large-scale project announcements are projected to shape industry activity.

| Key Insights | Details |

|---|---|

| Off-grid Hybrid Power System Market Size (2026E) | US$ 3.3 Bn |

| Market Value Forecast (2033F) | US$ 6.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 10.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 12.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Technological Advancements and Falling Costs

Declining technology costs across solar, wind, and energy storage systems continue to drive the economic feasibility of Off-grid hybrid power deployment. Lower component pricing reduces upfront capital requirements, which improves affordability across remote and price-sensitive installations. Cost compression at the equipment level also shortens payback periods, supporting broader project financing acceptance. As capital barriers ease, system integrators increasingly standardize hybrid configurations to manage procurement and installation complexity more efficiently.

At the same time, advancements in lithium-ion battery performance increase system reliability and operational flexibility. Higher energy density and longer cycle life reduce replacement frequency, which lowers lifecycle maintenance costs. Improved storage performance enables smoother load balancing and reduced fuel dependency, limiting exposure to price volatility. These operational efficiencies support continuous power availability, reinforcing hybrid systems as a practical solution for sustained Off-grid energy supply.

Policy Inconsistencies and Regulatory Uncertainty

Policy inconsistency and regulatory uncertainty continue to constrain planning and capital deployment across the off-grid hybrid power project. Fragmented regulatory frameworks complicate compliance requirements, increasing administrative overhead and approval timelines. Unclear subsidy structures and variable tariff regimes elevate financial modelling risk, which limits long-term contract visibility. These conditions raise project development costs and slow investment decisions, particularly for multi-site or cross-jurisdictional deployments.

Recent regulatory resets illustrate this constraint in practice. In Vietnam, the issuance of Decree 57/2025/ND-CP in March 2025 restructured renewable energy governance and direct power purchase agreement mechanisms. While intended to streamline oversight, the transition period introduced interpretive ambiguity for developers and offtakes. Project pipelines faced reassessment as permitting rules and contractual frameworks adjusted. Such regulatory shifts increase execution risk, reinforcing policy stability as a critical constraint on scalable Off-grid hybrid system deployment.

Microgrid Technology Advancements and Distributed Energy Resources Integration

Advancements in microgrid architectures and distributed energy resource integration continue to create scope for more flexible Off-grid hybrid power deployments. Modular microgrid designs support localized generation, storage, and load management, which reduces reliance on centralized coordination. This configuration enables phased capacity additions, lowering scaling risk for operators managing uncertain demand profiles. As deployment models mature, microgrids increasingly support standardized project execution across remote and industrial settings.

At the system level, the integration of digital energy management platforms enables real-time monitoring and automated dispatch across generation sources. Embedded analytics improve load forecasting accuracy, which reduces fuel dependency and limits unplanned downtime. Containerized and pre-integrated system formats further reduce installation complexity, supporting faster commissioning cycles. These mechanisms create opportunities for technology providers to support repeatable deployment models that balance cost control, operational resilience, and long-term system performance.

Category–wise Analysis

System Configuration Insights

The solar-diesel hybrid segment is projected to lead with approximately 55% market share in 2026, underpinned by its entrenched role in remote industrial power, rental fleets, and critical infrastructure where uptime is non-negotiable. Adoption remains anchored by fuel-risk mitigation, dispatch reliability, and retrofit compatibility, with operators prioritizing standardized controllers, AC-coupled microgrids, and rapid deployment in high-utilization environments. Ongoing platform evolution, including active hybridization, zero-load operation, modular power skids, and remote monitoring, continues to reinforce replacement cycles and utilization intensity. Vendors such as Caterpillar, Cummins, Kohler, SMA, Victron Energy, and Schneider Electric are expanding portfolios with integrated controllers and containerized systems to lock in enterprise workflows and long-term service contracts.

The solar-wind-diesel hybrid segment is likely to be the fastest-growing segment, driven by performance limits of solar-only hybrids across extreme climates, island grids, and 24/7 industrial sites. Growth is being catalyzed by DC-coupled HVDC microgrids, grid-forming inverters, and maintainable VAWT integration, which materially improve round-trip efficiency, resource complementarity, and asset utilization. Accelerating adoption is supported by digital twins, AI-driven dispatch, and advanced planning tools that reduce battery oversizing and operational friction for first-time adopters. Companies including Wärtsilä, Siemens Gamesa, GE Vernova, ABB, Schneider Electric, and Danfoss are scaling integrated platforms to capture early-cycle demand and embed switching costs.

Application Insights

Commercial application is projected to dominate, accounting for approximately 41% share in 2026, underpinned by entrenched deployment across malls, hospitals, data centers, telecom infrastructure, and urban weak-grid commercial estates where continuity and tariff exposure materially shape energy strategy. Adoption remains anchored by peak shaving, demand-charge avoidance, and business continuity planning, with enterprises prioritizing behind-the-meter optimization, thermal energy storage for HVAC load shifting, and VPP-ready architectures in high-utilization environments. Ongoing platform evolution, including AI-managed load shedding, second-life battery integration, and pre-engineered containerized microgrids, continues to reinforce replacement cycles and utilization intensity. Vendors such as Schneider Electric, Siemens, Eaton, Tesla Energy, Sungrow, Huawei, BayWa r.e., and Enel X are expanding integrated platforms and energy management ecosystems to lock in enterprise workflows and long-term service contracts. This combination of mature infrastructure, regulatory alignment, and predictable demand sustains commercial leadership within structured deployment models.

The industrial segment is likely to be the fastest-growing application within the hybrid power systems market, driven by grid infrastructure lag, decarbonization mandates across global supply chains, and reliability constraints at remote mining, processing, and heavy manufacturing sites. Growth is being catalyzed by megawatt-scale E-Houses, high C-rate battery systems, synchronous condenser integration, and bifacial tracker-based generation, which materially improve grid stability, surge handling, and energy yield under continuous load profiles. Accelerating adoption is supported by digital twins, predictive maintenance, and remote diagnostics that reduce downtime risk and commissioning friction for first-time adopters. Companies including Wärtsilä, Rolls-Royce MTU, Caterpillar, ABB, Siemens, Rockwell Automation, Saft, BYD, and Tesla are scaling industrial-grade platforms to capture early-cycle demand and embed switching costs.

Regional Insights

Asia Pacific Off-grid Hybrid Power System Market Trends

Asia Pacific is expected to lead the global hybrid and off-grid power systems market, commanding an estimated 40% share while also being the fastest-growing regional segment. The region’s dominance is underpinned by a combination of unique geographical challenges, rapid industrialization, and aggressive technological adoption. Island nations such as Indonesia and the Philippines require off-grid hybrid solutions to overcome the logistical impossibility of connecting remote islands to centralized grids, while rural industrial hubs in India and Australia are increasingly turning to modular solar-wind-diesel or solar-wind-hydrogen systems to reduce reliance on diesel and cut operational costs. Huawei dominates the telecom hybrid segment with advanced digital power converters, Sungrow Power Supply provides large-scale hybrid inverters for industrial applications, and Adani Power is actively expanding rural microgrid deployment in India.

SMA Solar Technology offers high-end off-grid inverters for the Australian Outback, while Delta Electronics supplies modular power solutions for remote industrial sites. Technological advances such as AI-driven Energy Management Systems, bifacial solar integration, and Vehicle-to-Grid compatibility are increasingly standard in APAC deployments, allowing systems to optimize energy draw, predict load demand, and integrate electric vehicle batteries as supplementary storage.

Pilot projects in Japan and South Korea are also testing hydrogen integration for long-term renewable storage, complementing the existing solar-wind infrastructure. Standardization of mini-grid technical requirements across ASEAN nations is facilitating mass production rather than custom builds, further consolidating APAC’s position. The combination of high demand, innovative technology adoption, supportive policies, and the presence of leading brands ensures Asia Pacific remains the global leader and fastest-growing market for hybrid and off-grid power systems.

North America Off-grid Hybrid Power System Market Trends

North America is expected to remain a stable regional market for hybrid and off-grid energy systems, supported by institutional maturity and replacement-driven demand cycles. The region is projected to sustain steady deployment momentum as industrial users, utilities, and infrastructure operators prioritize resilience-oriented energy architectures. Capacity additions in remote and off-grid applications are expected to expand distributed solar and storage installations, while hybrid solar and battery deployments are expected to scale across commercial and utility-linked microgrid projects. Business models are expected to shift toward service-oriented energy provisioning, with Power as a Service structures enabling predictable operating expenditure for transport corridors, logistics hubs, and industrial facilities. Market development is expected to align with grid hardening strategies, climate adaptation planning, and corporate decarbonization roadmaps, positioning North America as a structurally resilient but maturity-constrained growth market.

The U.S. is expected to anchor regional demand as grid resilience priorities, rural electrification gaps, and climate-driven disruption risks accelerate decentralized energy adoption. Federal and state-level fiscal incentives are expected to reduce upfront capital barriers, while safety and electrical compliance frameworks are expected to formalize technical standards across off-grid and hybrid system deployments. Technology roadmaps are expected to prioritize AI-enabled energy management, modular microgrid architectures, and advanced battery chemistries optimized for harsh operating environments. Military, telecommunications, and remote industrial operations are expected to sustain demand for tactical, rapidly deployable hybrid systems, reinforcing North America’s positioning as a stability-driven, resilience-focused regional market.

Europe Off-grid Hybrid Power System Market Trends

Europe represents a mature and highly structured market for off-grid hybrid power systems, characterized by a focus on flexibility, storage integration, and fossil fuel replacement in niche industrial and mobile applications. Unlike rapidly expanding regions, growth in Europe is driven by corrective and efficiency-oriented measures rather than new capacity build-outs. Energy security and independence remain key motivators, as enterprises and households adopt hybrids to mitigate grid volatility.

Industrial adoption is increasingly centered on green hydrogen and battery-hybrid solutions, with companies such as Siemens Energy delivering renewable-powered electrolysis systems and Instagrid deploying mobile hybrid units for construction, events, and emergency services. Residential trends are shifting toward hybridization of existing solar assets, plug-in balcony systems, and smart hybrids capable of managing negative price periods, reflecting a market that prioritizes optimization and resilience over volume expansion.

Technological advancement reinforces Europe’s mature status, with AI-driven Energy Management Systems, battery energy storage as core infrastructure, and aggregation into Virtual Power Plants becoming standard practice. Leading hubs include Germany, with its research-driven hybrid deployments; the Netherlands, home to the Haring Vliet Energy Park integrating wind, solar, and storage; and the U.K., dominating merchant-driven BESS capacity. Major players such as Siemens Energy, SMA Solar Technology, Schneider Electric, Vestas, Wartsila, and Instagrid exemplify the region’s focus on high-quality, technologically sophisticated solutions. Overall, Europe’s market remains disciplined, emphasizing operational efficiency, regulatory compliance, and advanced integration rather than aggressive expansion.

Competitive Landscape

The global off-grid hybrid power system market is fragmented, composed of a mix of multinational corporations, specialized regional developers, and emerging technology startups. Leading companies such as Schneider Electric, Siemens Energy, Tesla, Honeywell, Johnson Controls, and Hitachi exert a strong influence through comprehensive portfolios covering generation, storage, control, and energy management platforms. The competitive advantage stems from AI-driven energy optimization, predictive analytics, turnkey deployment capabilities, and global service infrastructure, allowing them to deliver cost-efficient, reliable systems.

Regional developers and niche innovators remain relevant by leveraging localized expertise, customer relationships, and specialized technology solutions, maintaining pockets of competitiveness. Market differentiation emphasizes system modularity, digital connectivity, renewable integration, and lifecycle services, while strategic partnerships and acquisitions are gradually consolidating advanced technology segments. Emerging players and solar-integrated firms such as Jinko Solar, Trina Solar, JA Solar, Winch Energy, and BoxPower highlight innovation in storage, modular microgrids, and software optimization, signaling continued evolution. Industry behavior indicates increasing focus on hybrid system intelligence, grid integration, and turnkey energy solutions, suggesting competitive pressure will intensify across both global and regional players.

Key Industry Highlights:

- In June 2025, ‘Partners Group agreed to acquire the utility-scale developer Power Transitions from EnCap Investments, committing US$450 million to scale its hybrid power portfolio.

- In December 2024, Google’s renewable energy division, TPG Rise Climate, and Intersect Power formed a US$20 billion partnership to develop co-located data centers.

- In June 2024, SolarEdge Technologies unveiled its next-generation high-power residential hybrid inverter and modular battery system.

Companies Covered in Off-grid Hybrid Power System Market

- ABB Group

- General Electric (GE)

- Schneider Electric

- Siemens Energy

- Wärtsilä

- SMA Solar Technology AG

- Eaton

- Huawei Technologies Co., Ltd.

- Tata Power Renewable Energy

- Tesla Inc.

- Honeywell International

- Johnson Controls International

- Hitachi Ltd.

- Panasonic Corporation

- Winch Energy

- BoxPower

Frequently Asked Questions

The global off-grid hybrid power system market is valued at US$3.3 billion in 2026 and is projected to reach US$6.5 billion by 2033.

Declining renewable energy costs, expanding rural electrification initiatives, and advancing energy storage technologies are the primary drivers of market growth.

The off-grid hybrid power system market is expected to grow at a CAGR of 10.3% between 2026 and 2033, reflecting steady demand expansion.

Key opportunities include hybrid microgrid deployment in underserved regions, advancements in digital energy management platforms, and the integration of modular and pre-integrated system formats for faster deployment.

Major players include Schneider Electric, Siemens Energy, Tesla, Honeywell, Johnson Controls, Hitachi, ABB, General Electric, SMA Solar Technology, Huawei, Tata Power Renewable Energy, and emerging innovators such as Winch Energy and BoxPower.