- Smart Packaging

- Horizontal Form Fill Seal (HFFS) Machines Market

Horizontal Form Fill Seal (HFFS) Machines Market Size, Share, and Growth Forecast, 2026 - 2033

Horizontal Form Fill Seal (HFFS) Machines Market by Capacity (151-350 Packets Per Minute, Less than 150 Packets Per Minute, Others), Product Type (Stand Alone Wrapper, Fully Automated System, Others), Pack Style, Application, and Regional Analysis for 2026 - 2033

Horizontal Form Fill Seal (HFFS) Machines Market Size and Trends Analysis

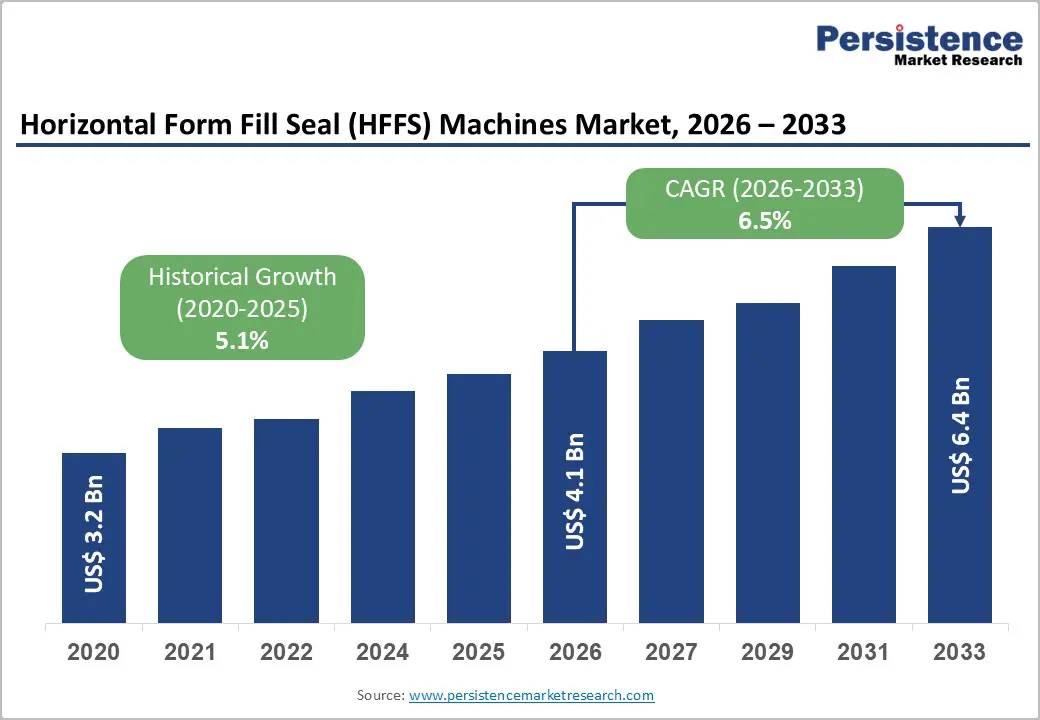

The global horizontal form fill seal (HFFS) machines market size is likely to be valued at US$4.1 billion in 2026 and is expected to reach US$6.4 billion by 2033, growing at a CAGR of 6.5% between 2026 and 2033, driven by expanding food & beverage packaging demand, particularly in confectionery, snack bars, and bakery applications, combined with rising automation investments in developed economies.

Manufacturers are prioritizing modular, servo-driven HFFS platforms that reduce changeover time, improve sealing precision, and enable predictive maintenance. Emerging economies are contributing incremental demand through compact, low-waste packaging formats. Regulatory emphasis on hygienic, traceable packaging in pharmaceuticals and personal care further strengthens adoption of advanced horizontal pouch and flow-wrap systems.

Key Industry Highlights:

- Leading Region: North America is projected to lead the market, accounting for approximately 30.7% market share, driven by high packaged food consumption and strong automation adoption across the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing regional market, supported by expanding processed food production in China and India and rising automation investments across Southeast Asia.

- Investment Plans: Manufacturers are increasing capital investment in fully automated and digitally integrated HFFS lines, with modernization and sustainability-driven upgrades contributing to steady annual growth aligned with the projected 5.2% CAGR (2026 - 2033).

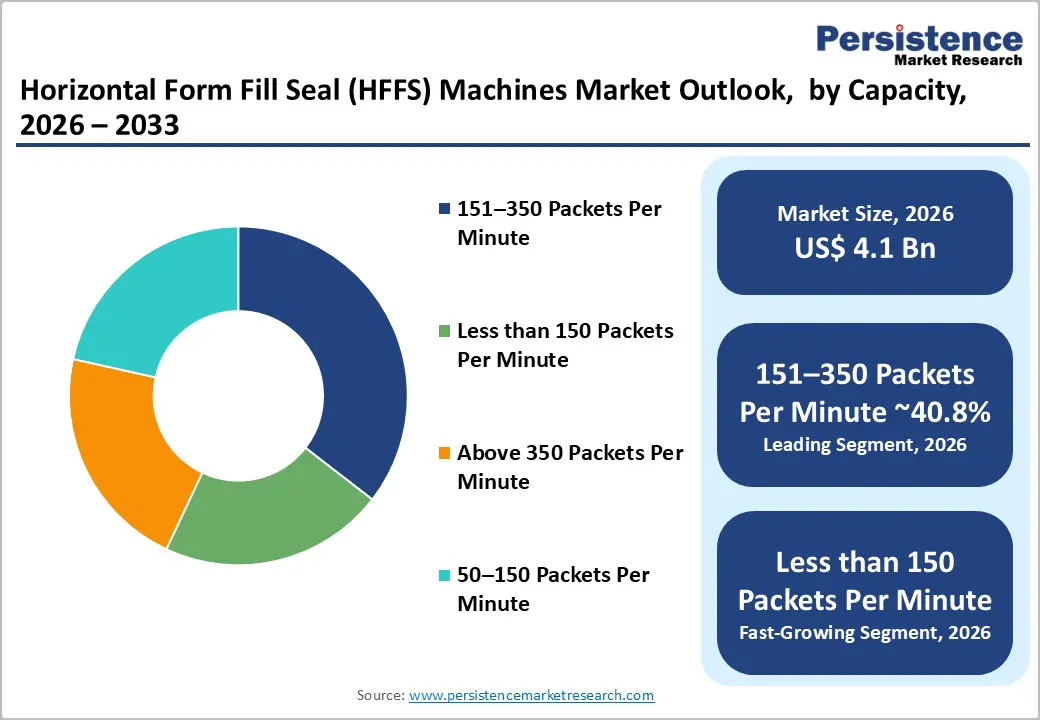

- Dominant Capacity: The 151-350 ppm segment is anticipated to dominate the market with 32.6% share, owing to its optimal balance between throughput efficiency and capital cost.

- Leading Product Type: Stand alone wrappers are estimated to hold the leading position, accounting for 40.8% of the market, supported by their cost-efficiency, modular design, and broad application across snack and bakery packaging.

| Key Insights | Details |

|---|---|

| Horizontal Form Fill Seal (HFFS) Machines Market Size (2026E) | US$4.1 Bn |

| Market Value Forecast (2033F) | US$6.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automation and Labor Productivity Gains

Rising labor costs and persistent workforce shortages are accelerating the shift from manual and semi-automatic packaging lines toward fully automated HFFS systems. Companies increasingly evaluate capital expenditure through productivity metrics such as throughput per hour, overall equipment effectiveness (OEE), and downtime reduction. Mid- to high-speed systems (151-350 packets per minute and above) frequently demonstrate measurable efficiency improvements, including double-digit gains in output consistency and lower labor dependency. Automation also enhances sealing precision, reduces product waste, and improves quality assurance compliance. As a result, equipment purchases are increasingly justified not only by throughput gains but also by lower long-term operating costs. This dynamic supports higher average selling prices while expanding aftermarket revenue streams through service agreements, spare parts, and digital upgrades.

Flexible Packaging and Sustainability Requirements

Sustainability policies and retailer requirements for lightweight, recyclable packaging are reshaping equipment specifications. Brand owners are transitioning toward mono-material films, reduced laminate structures, and recyclable flexible formats that are compatible with advanced HFFS platforms. Modern machines incorporate enhanced sealing technology, film tension control, and compatibility with resealable features such as zippers and tear notches. Regulatory initiatives focused on packaging waste reduction and extended producer responsibility are increasing demand for machinery capable of processing next-generation materials. Older systems often require retrofits to accommodate recyclable films, creating incremental equipment demand. Consequently, sustainability initiatives are not only influencing material selection but also driving both new equipment investment and installed-base modernization.

Product Portioning and E-Commerce Packaging

Growth in single-serve, snack-size, and multipack configurations has expanded the role of HFFS equipment in flexible retail packaging. Consumer demand for convenience, portion control, and on-the-go consumption is particularly evident in snack bars, confectionery, and ready-to-eat bakery items. Horizontal flow-wrap systems offer efficient production of such formats while preserving product integrity. E-commerce growth has also altered packaging requirements. Retail-ready, durable, and visually appealing packaging formats are essential for reducing transit damage and improving shelf presentation. This shift supports demand across both lower-capacity (<150 ppm) machines for agile brands and mid-speed equipment for large-scale manufacturers managing multiple SKUs. Investments in quick-change tooling and digital recipe management are rising as product portfolios expand.

Barrier Analysis - High Capital Intensity and Extended Payback Periods

Fully automated HFFS systems require significant capital outlays, including integration, installation, and validation costs. For small and mid-sized manufacturers, payback periods can extend from two to five years depending on production volume and utilization rates. Financing availability and interest rate cycles materially influence purchasing decisions. A substantial proportion of smaller enterprises cite total cost of ownership and system integration complexity as barriers to modernization. This cost sensitivity sustains demand for semi-automatic systems and retrofit solutions while moderating conversion rates to fully automated lines.

Supply Chain and Component Constraints

HFFS machines rely on servo motors, programmable logic controllers, precision tooling, and electronic components that are susceptible to global supply chain volatility. Extended procurement timelines can delay commissioning schedules and affect revenue recognition for OEMs. Lead times for high-end systems have fluctuated considerably in recent years, with component price increases contributing to overall system cost escalation. These constraints increase inventory management complexity and may temporarily defer capital investment decisions, particularly in price-sensitive markets.

Opportunity Analysis - Retrofit and Lifecycle Service Expansion

A substantial installed base of legacy HFFS systems presents significant opportunities for modernization. Upgrades, including servo retrofits, control panel replacements, robotic infeed integration, and digital monitoring systems, enhance machine performance without full equipment replacement. Service contracts and performance-based maintenance agreements provide recurring revenue streams for OEMs. Lifecycle services typically generate higher margins than new equipment sales. By bundling predictive maintenance tools and upgrade kits, suppliers can reduce customer downtime while strengthening long-term relationships. This strategy expands addressable revenue without requiring proportional increases in manufacturing capacity.

Emerging Markets and Localized Manufacturing

Rapid expansion of food processing and FMCG production in Southeast Asia, India, and Latin America is driving demand for mid-range HFFS systems tailored to regional price expectations. Local assembly operations and regional service hubs reduce total acquisition costs and lead times. This localization strategy improves competitiveness and accelerates adoption among regional processors. Smaller snack and confectionery brands in emerging economies increasingly seek automation to improve hygiene standards and meet export requirements. Vendors that combine localized production with financing solutions and operator training programs are well positioned to capture high-growth opportunities.

Industry 4.0 and Digital Integration

Digital transformation is reshaping packaging operations. Remote diagnostics, real-time performance monitoring, and predictive maintenance tools reduce downtime and optimize throughput. Integration with plant-level manufacturing execution systems enables data-driven production planning and quality assurance. Early adopters report measurable improvements in uptime and maintenance efficiency. As digital infrastructure becomes standard across processing facilities, HFFS machines equipped with open communication protocols and cloud-based analytics will gain competitive advantage. Software subscriptions and analytics services represent incremental revenue opportunities beyond traditional equipment sales.

Category-wise Analysis

Capacity Insights

The 151-350 packets per minute (ppm) segment is anticipated to account for 32.6% of market share in 2026. This capacity range offers an optimal balance between throughput and capital investment, making it highly suitable for mid- to large-scale snack, bakery, and confectionery producers. Equipment within this band typically integrates servo-driven motion control, automated feeding systems, and flexible tooling configurations that support multi-SKU production. These features allow manufacturers to manage diverse product portfolios without sacrificing efficiency. Producers value this segment for its adaptability to seasonal product fluctuations and moderate production volumes. Modular capabilities, including resealable closures, multi-lane feeding, and synchronized case packing, enhance operational flexibility while maintaining consistent output quality. The ability to scale production without requiring extensive infrastructure expansion makes this capacity range especially attractive. As a result, machines operating between 151-350 ppm remain the core revenue generator for many original equipment manufacturers, supported by strong aftermarket service and upgrade demand.

Machines operating at below 150 ppm represent the fastest-growing capacity category. Growth in this segment is driven by increasing demand for trial-sized pouches, artisanal food brands, specialty health products, and direct-to-consumer packaging models. Smaller systems require lower upfront capital expenditure and occupy minimal floor space, making them accessible to start-ups and emerging manufacturers. This cost advantage lowers entry barriers for companies transitioning from manual or semi-automatic packaging operations. Frequent product innovation and shorter production runs further strengthen demand for agile equipment capable of rapid format changeovers. Compact HFFS systems often feature user-friendly interfaces, simplified tooling adjustments, and flexible film compatibility to support diverse packaging formats. Leasing and flexible financing options also encourage adoption, allowing smaller firms to automate incrementally without significant capital strain. This shift reflects broader market dynamics favoring customization, smaller batch production, and faster product launches.

Product Type Insights

Stand alone wrappers is estimated to account for 40.8% of the market in 2026, making them the dominant product type. These systems provide cost-efficient flow-wrapping solutions for individual products such as snack bars, biscuits, bakery items, and confectionery goods. Their modular design enables seamless integration with existing upstream processing and downstream packaging equipment, reducing operational complexity. This compatibility allows manufacturers to upgrade packaging efficiency without overhauling entire production lines. Producers favor stand alone wrappers for their mechanical reliability, ease of maintenance, and operational simplicity. The machines accommodate a wide range of product shapes and sizes, supporting diverse applications across food and non-food sectors. A substantial installed base strengthens the aftermarket ecosystem, generating recurring revenue through spare parts, maintenance contracts, and performance upgrades. This established infrastructure reinforces the segment’s leading position and long-term stability.

Fully automated systems represent the fastest-growing product type within the HFFS market. These integrated lines combine feeding, grouping, wrapping, inspection, and case packing into a unified automated process. By minimizing manual handling, fully automated systems enhance hygiene control, reduce contamination risks, and improve production consistency. Labor cost pressures and workforce shortages continue to accelerate demand for such solutions among large brand owners and pharmaceutical manufacturers. Demand for fully automated systems is strongest in regions characterized by higher labor costs and stringent regulatory requirements. Advanced features such as real-time performance monitoring, digital traceability, and predictive maintenance further strengthen their value proposition. Turnkey system integration, including performance validation and guaranteed output levels, encourages long-term capital investment. As manufacturers prioritize productivity optimization and regulatory compliance, fully automated HFFS solutions are positioned to capture an increasing share of future market growth.

Regional Insights

North America Horizontal Form Fill Seal (HFFS) Machines Market Trends - Automated HFFS Expansion Driven by Labor Shortages

North America is projected to account for approximately 30.7% of the market share in 2026, with the U.S. representing the largest national contributor. Strong demand stems from high consumption of packaged food in ready-to-eat meals, snacks, frozen foods, and pet food. Major food manufacturers such as Nestlé, PepsiCo, and General Mills continue to expand automated packaging capacity across U.S. facilities to enhance throughput and reduce labor dependency. Persistent labor shortages in manufacturing have accelerated investment in fully automated HFFS lines integrated with robotics and digital controls.

Equipment suppliers are strengthening their regional footprint through innovation and acquisitions. For instance, ProMach has expanded its North American flexible packaging portfolio through strategic acquisitions and the integration of end-of-line automation solutions, enabling turnkey packaging lines for food and healthcare clients. Similarly, Barry-Wehmiller continues to enhance digital performance monitoring and lifecycle services via its packaging divisions.

Stringent regulations enforced by the U.S. Food and Drug Administration and traceability requirements under the Food Safety Modernization Act (FSMA) influence machine design, promoting hygienic stainless-steel construction, washdown compatibility, and real-time data logging. Private-label expansion among retailers such as Walmart and Costco is increasing contract packaging demand, prompting co-packers to invest in high-speed HFFS systems with quick-changeover capability. Investors increasingly favor vertically integrated OEM-service models that bundle machinery, spare parts, and predictive maintenance solutions, strengthening long-term equipment demand stability across the region.

Europe Horizontal Form Fill Seal (HFFS) Machines Trends- Sustainable, High-Precision HFFS with Modular Design

Europe maintains a strong HFFS market presence, supported by engineering excellence, regulatory harmonization, and sustainability-driven innovation. Germany, Italy, France, Spain, and the U.K. represent core demand centers. European OEMs such as Syntegon and IMA Group continue to lead in high-precision, servo-driven HFFS systems tailored for food, confectionery, and pharmaceutical applications. These companies emphasize modular machine architectures and Industry 4.0 connectivity, enabling remote diagnostics and performance analytics. Sustainability mandates under the European Union’s Packaging and Packaging Waste Directive (PPWD) are reshaping machine specifications. Equipment must accommodate recyclable mono-material films, paper-based laminates, and compostable substrates. As a result, OEMs are developing advanced sealing technologies capable of handling thinner, heat-sensitive materials without compromising pack integrity.

For example, MULTIVAC has introduced energy-efficient thermoforming and flow-wrapping systems optimized for recyclable films, supporting retailers transitioning toward circular packaging models. Major European food brands such as Unilever and Danone are piloting recyclable flexible packaging initiatives across multiple product lines. This shift stimulates retrofit demand, as existing HFFS equipment requires sealing upgrades and software adjustments to process new substrates. Lifecycle service agreements and modernization projects therefore, represent a significant revenue stream for regional OEMs. Investment in automation also addresses high labor costs across Western Europe, reinforcing long-term market resilience.

Asia Pacific Horizontal Form Fill Seal (HFFS) Machines Market Trends - Fastest-Growing HFFS Market with Cost Efficiency

Asia Pacific is the fastest-growing regional market, driven by rapid industrialization, urbanization, and rising processed food consumption. China and India are the primary demand centers, supported by expanding middle-class populations and increased penetration of packaged snacks, dairy products, and convenience foods. Domestic food manufacturers and multinational companies such as ITC Limited and Tingyi Holding Corp. are scaling up automated packaging capacity to meet volume growth and export standards.

In China, local equipment manufacturers compete aggressively on cost while global suppliers strengthen partnerships and local assembly operations to reduce price barriers. Companies such as SACMI have expanded their Asian service and manufacturing footprint to support beverage and food packaging lines, improving lead times and aftermarket support. In India, policy initiatives promoting domestic food processing and export competitiveness are accelerating automation investments in mid-speed, cost-effective HFFS systems suitable for regional brands.

Japan represents a technologically advanced sub-market emphasizing high-precision automated systems. Firms such as Fuji Machinery Co., Ltd. focus on premium flow-wrapping and HFFS equipment with advanced servo control and compact footprints, catering to confectionery and pharmaceutical sectors. Across Southeast Asia, export-oriented production in countries such as Thailand and Vietnam encourages adoption of traceable, hygienic systems aligned with international food safety standards. Localized manufacturing, expanded regional service networks, and rising private-label exports collectively reinforce Asia Pacific’s position as the fastest-growing HFFS market globally.

Competitive Landscape

The global horizontal form fill seal (HFFS) machines market is moderately concentrated. Several global OEMs command significant shares in premium and mid-speed segments, while regional manufacturers compete on cost and localized service. Aftermarket services, spare parts, and digital upgrades are central to competitive differentiation. Service capabilities increasingly influence purchasing decisions alongside machine performance.

Market leaders emphasize automation innovation, lifecycle service monetization, localized manufacturing, and digital integration. Competitive advantages include rapid changeover capability, hygienic design compliance, and Industry 4.0 connectivity. Financing models and equipment-as-a-service approaches are emerging to broaden market access.

Key Industry Developments:

- In August 2025, HMC Products showcased its IMTN5 Pouchmaster horizontal form-fill-seal machine at PACK EXPO Las Vegas, demonstrating enhanced packaging performance across food, snacks, cosmetics, and healthcare applications.

Companies Covered in Horizontal Form Fill Seal (HFFS) Machines Market

- IMA Group

- Syntegon Technology

- MULTIVAC Group

- ProMach Inc.

- Fuji Machinery Co., Ltd.

- Bosch Packaging Technology

- Barry-Wehmiller Companies, Inc.

- ULMA Packaging

- Coesia Group

- SACMI Group

- Rovema GmbH

- PFM Packaging Machinery S.p.A.

- Marchesini Group

- Omori Machinery Co., Ltd.

- Hayssen Flexible Systems

- Ishida Co., Ltd.

- KHS Group

- Nichrome India Ltd.

Frequently Asked Questions

The global horizontal form fill seal (HFFS) machines market is estimated to be valued at US$4.1 billion in 2026.

The horizontal form fill seal (HFFS) machines market is projected to reach approximately US$6.4 billion by 2033.

Key trends include increasing adoption of fully automated and integrated packaging lines and growing demand for recyclable and mono-material film compatibility

By capacity, the 151-350 ppm segment leads the horizontal form fill seal (HFFS) machines market, accounting for 32.6% share, due to its optimal balance between throughput and capital investment. By product type, Stand alone wrappers dominate with 40.8% market share, supported by cost efficiency and broad application across snack and bakery packaging.

The horizontal form fill seal (HFFS) machines market is projected to grow at a CAGR of 6.5% between 2026 and 2033.

Major players include IMA Group, Syntegon Technology, MULTIVAC Group, ProMach Inc., and Fuji Machinery Co., Ltd.