- Off-Road Equipment & Machinery

- Horizontal Grinder Market

Horizontal Grinder Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Horizontal Grinder Market by Power Source (Diesel-Powered Horizontal Grinders and Electric-Powered Horizontal Grinders), Grinding Capacity (< 400 HP, 400-700 HP, 700-900 HP, and> 900 HP), Application, Wood Recycling and Processing, Land Clearing and Forestry Operations, Biomass and Energy Production, Construction and Demolition Waste Processing), and Regional Analysis for 2025 - 2032

Horizontal Grinder Market Size and Trends Analysis

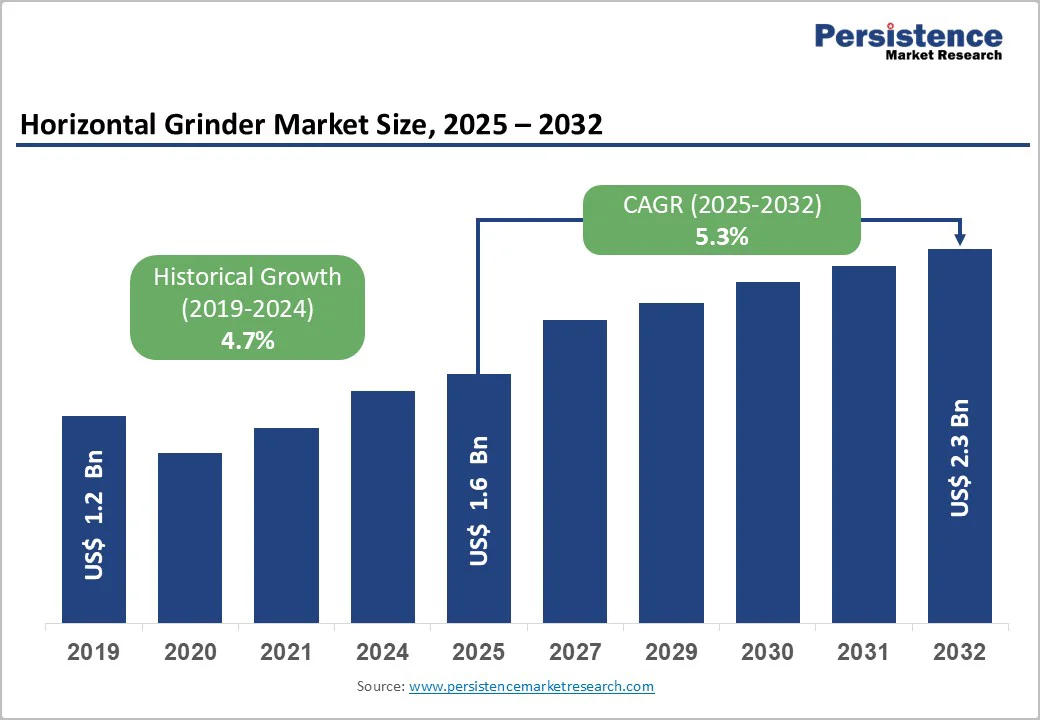

The global horizontal grinder market size is valued at US$1.6 billion in 2025 and is projected to reach US$2.3 billion by 2032, reflecting a CAGR of 5.3% during the forecast period 2025 to 2032.

Three macroeconomic forces primarily drive the market expansion: tightening global regulations on construction and demolition (C&D) waste management, rising adoption of biomass as a renewable energy source, and ongoing technological advancements that enhance operational efficiency.

Demand remains strong across wood recycling, land clearing, C&D waste processing, biomass production, and organics recycling, all of which require high-capacity material reduction equipment.

Key Industry Highlights:

- Power Source Leadership: Diesel-powered grinders command a 60%+ revenue share, while the electric-powered segment is the fastest-growing due to environmental regulations and operational cost advantages.

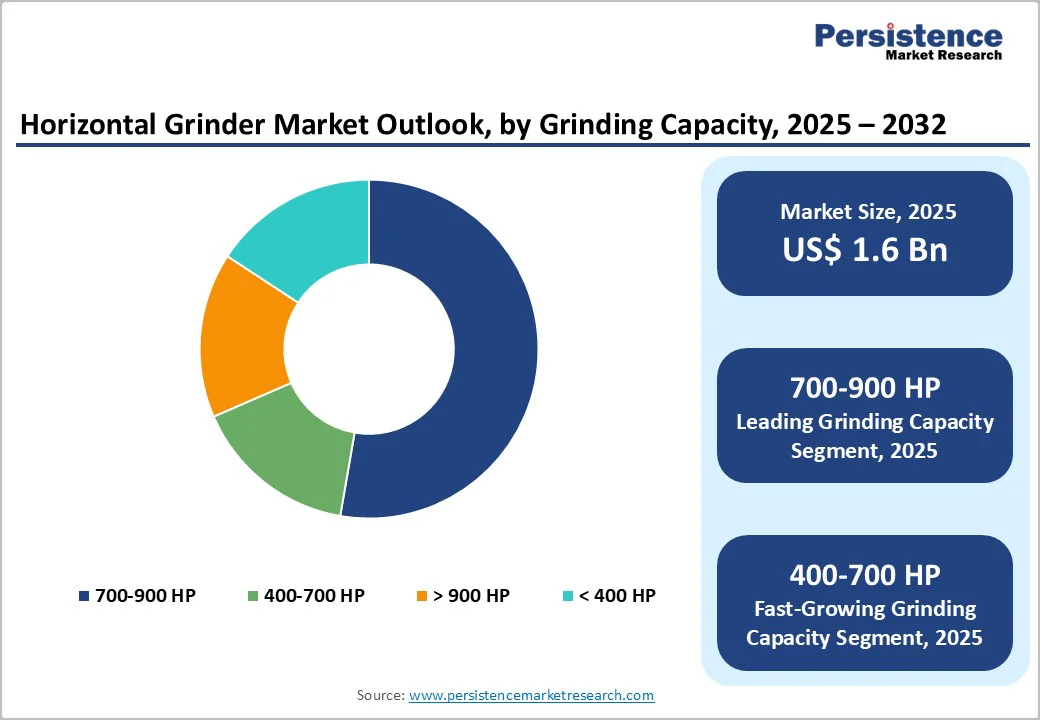

- Capacity Market Leader: The 700-900 HP category dominates with a 40%+ revenue share; the 400-700 HP segment is the fastest-growing, aligned with specialized application expansion and distributed processing facility development.

- Application Dynamics: Wood recycling and processing maintains 20%+ revenue share; land clearing and forestry operations experience fastest growth at 6.8-7.4% CAGR driven by infrastructure development and climate-related land management requirements.

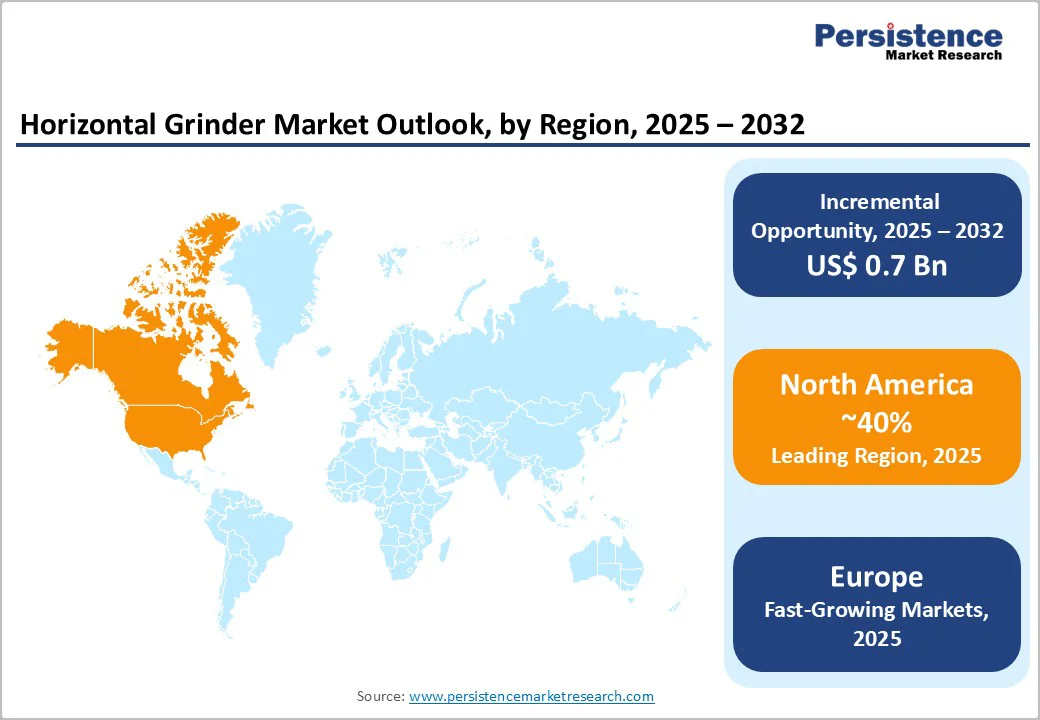

- Regional Market Performance: North America maintains 40% global market share (US$640 million); Asia-Pacific represents the fastest-growing region at 6.1% CAGR.

- Strategic Developments: Product line expansion by CBI (2024), Bandit Industries market entry (2024), and electric technology commercialization by WSM indicate intensifying competition and technology-driven market differentiation strategies reshaping competitive positioning.

| Key Insights | Details |

|---|---|

| Horizontal Grinder Market Size (2025E) | US$ 1.6 Bn |

| Market Value Forecast (2032F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Dynamics

Drivers - Stringent Regulatory Framework and Waste Diversion Mandates

Regulatory bodies globally have implemented increasingly rigorous requirements for construction and demolition waste management.

The U.S. Environmental Protection Agency (EPA) mandates waste diversion targets of 75-95% for C&D materials, with major municipalities, including Denver, implementing "Waste No More" ordinances (approved by 70% of voters in November 2022) requiring detailed recycling plans for all demolition projects. These regulations specifically address concrete, asphalt, wood, metals, and gypsum processing areas where horizontal grinders provide critical functionality.

The 2023 EPA report documented that proper recycling can recover up to 70% of demolition waste for beneficial reuse. The regulatory landscape extends internationally, with the European Union promoting circular economy principles through stringent landfill diversion regulations and developing nations increasingly adopting similar frameworks.

Market impact: Regulatory compliance requirements create consistent demand for equipment, with waste management facilities investing in horizontal grinders to meet or exceed mandated diversion thresholds. This regulatory tailwind supports projected market growth of 5.3% CAGR through 2032.

Technological Advancement in Automation and Remote Monitoring Systems

Modern horizontal grinders incorporate advanced technological systems that fundamentally enhance operational economics. Remote monitoring capabilities, programmable logic controllers (PLCs), smart sensor integration, and load-sensing technology enable real-time performance optimization and predictive maintenance.

Telematics systems provide fleet management visibility, reducing unscheduled downtime and improving the total cost of ownership. Electrification represents a transformative technology trend, with electric-powered grinders offering 50-70% lower emissions profiles and substantially reduced operational noise, creating market opportunities in urban recycling centers and regulated industrial zones.

Advanced rotor designs with interchangeable screens, variable-speed drives, and automated feed-rate adjustments enable equipment versatility across multiple material types and processing scenarios.

Technology integration commands 15-20% equipment cost premiums but delivers proportionally higher operational efficiency gains, enabling waste-processing companies to increase throughput while reducing energy consumption and maintenance expenditures. This technology adoption cycle supports sustained market expansion across both developed and emerging markets.

Market Restraining Factors

High Initial Capital Investment and Equipment Costs

Horizontal grinder systems represent significant capital expenditures, with entry-level models ranging from US$300,000-US$500,000 and high-capacity systems exceeding US$1.2 million.

These capital requirements create accessibility barriers for smaller waste management operators, particularly in developing regions with limited access to equipment financing. Additional infrastructure costs (concrete pads, feed systems, screening equipment, and disposal logistics) increase the total project investment requirements.

Equipment financing options remain limited in emerging markets, with interest rates often exceeding 12-15% annually, substantially elevating customer acquisition costs. Quantified risk: Capital constraints limit market penetration in regions where waste management facilities operate at lower scales or with compressed profit margins. This restraint particularly impacts small municipalities and private operators in the Asia Pacific and Latin American markets.

Opportunity - Electric-Powered Grinder Technology Expansion in Urban Markets

Electric horizontal grinders represent a high-growth opportunity segment currently capturing emerging market share in urban recycling centers, industrial facilities, and regulated emission zones.

Electrification eliminates the need for diesel engines, reducing operational noise by 50-70% and emissions by 60-80%, enabling facility placement in proximity-sensitive areas and compliance with increasingly stringent urban environmental regulations. The fastest-growing power source segment, electric grinders reduce operational costs through simplified maintenance (no oil changes, filter replacements, or fuel management) and longer equipment availability cycles.

Municipal waste processing facilities implementing zero-emission operational targets create specific market demand for electric solutions. Opportunity sizing: Electrification could capture 25-35% of the market (representing US$575-US$805 million in incremental equipment sales) within the 2025-2032 forecast period, particularly in European, North American, and developed Asia-Pacific markets that implement strict emissions regulations.

Category-wise Analysis

Power Source Insights

Diesel-powered horizontal grinders dominate the market with over 60% revenue share. Their leadership is supported by mature manufacturing ecosystems, operator familiarity, and strong suitability for high-capacity outdoor operations.

Diesel engines provide superior torque for processing dense materials such as stumps, construction debris, and contaminated wood, while also offering unmatched mobility and operational independence critical for forestry, land clearing, and remote-site applications. Despite their dominance, the segment faces growing pressure from tightening emission standards, fuel price volatility, and faster depreciation relative to newer electric models.

Still, diesel equipment remains essential for maximum throughput requirements and non-electrified environments, sustaining a projected 5.9% CAGR through 2032. In contrast, electric-powered grinders represent the fastest-growing segment, driven by urban sustainability mandates, modernization of municipal waste facilities, and lower lifetime operating costs.

Electric grinders eliminate fuel costs entirely, reduce maintenance needs by 40-60%, and comply with noise and emission restrictions in urban and industrial zones. Manufacturers such as West Salem Machinery are expanding electric portfolios, supported by incentives across North America and Europe.

Grinding Capacity Insights

The 700-900 HP horizontal grinder segment leads the market with over 40% revenue share, driven by its ability to deliver an optimal balance between high processing capacity and cost-efficient operation. Machines in this range typically handle 80-150 tons per hour, making them ideally suited for municipal solid waste (MSW) facilities, mid-scale commercial processors, and multi-stream waste reduction environments.

Models such as the CBI Magnum Force 6400CT and Peterson 6700D dominate this category, supported by key market drivers including throughput alignment with municipal requirements, enhanced mobility through tracked or wheeled platforms, and improved operational economics that strengthen profitability for mid-size waste processors.

The segment further benefits from advanced automation, telematics, and remote monitoring, which improve efficiency and reduce downtime, making it the preferred choice for operators seeking high-volume capabilities at manageable capital costs.

In contrast, the 400-700 HP segment represents the fastest-growing category, expanding at 6.1% CAGR through 2032. Its growth is fueled by rising demand from land clearing, selective demolition, and distributed waste collection systems, combined with lower equipment acquisition costs, rising municipal investment in secondary processing infrastructure, growing adoption of automation in smaller operations, and rental or EaaS models that support project-based usage.

Application Insights

The horizontal grinder market is strongly shaped by two major application segments, with wood recycling and processing remaining the clear market leader and land clearing and forestry operations emerging as the fastest-growing category.

Wood recycling and processing accounts for over 20% of total revenues (approximately US$320 million in 2025), supported by extensive use in pallet disposal, recovery of construction lumber, reduction of demolition waste, and processing of industrial wood residue.

This segment benefits from mature recycling ecosystems in the United States, Germany, China, and Europe’s EPR-driven regulatory structure, enabling consistent demand for mulch, biomass fuel, and animal bedding derived from processed wood. With established recycling networks and documented value creation through material recovery and cost savings, this segment maintains a stable 4.8% CAGR through 2032.

In contrast, land clearing and forestry operations represent the fastest-growing application, driven by expanding infrastructure projects, forest health programs, agricultural land consolidation, and climate-linked storm recovery needs.

Activities such as whole-tree grinding, stump removal, wildfire salvage, and orchard clearing increasingly rely on high-capacity machines like the CBI Magnum Force 5900T and Peterson 6700D. Supported by rising development activity in Asia-Pacific and Latin America, this segment is projected to register a robust 6.2% CAGR through 2032.

Regional Insights and Trends

North America leads the horizontal grinder market with dominant revenue, advanced infrastructure, and strong regulatory-driven growth.

North America remains the dominant regional market for horizontal grinders, generating nearly US$640 million in 2025 and accounting for over 40% of global revenue. The United States drives this leadership through mature waste management infrastructure, extensive recycling networks, and stringent regulatory frameworks that mandate high construction and demolition (C&D) waste diversion.

The region processes nearly 600 million tons of C&D waste annually, with horizontal grinders supporting 35-40% of material recovery operations. High equipment penetration, advanced technology adoption, and a fleet age of 8-10 years ensure steady replacement cycles.

Growth is underpinned by EPA and state-level mandates targeting 75-95% recovery, expanding municipal policies such as Denver’s “Waste No More,” and a construction sector expected to grow 4-6% annually through 2030. North America also leads in automation, remote monitoring, and electric grinder adoption, supported by the EPA’s Sustainable Materials Management (SMM) framework, which recognizes grinders as essential circular-economy infrastructure.

The competitive landscape is moderately consolidated, with Terex CBI, Peterson (Astec), and Rotochopper holding over 55% combined share. Strong investment trends, US$4-8 billion in annual waste infrastructure investment, and growing equipment-as-a-service usage support procurement demand.

Europe’s Horizontal Grinder Market Grows on Strict Regulations, Advanced Recycling Systems, and Rising Electrification

Europe remains the second-largest regional market for horizontal grinders, led by Germany, the United Kingdom, France, and Spain, supported by advanced waste management systems and strict environmental regulations. The European market is projected to grow at a 6.1% CAGR by the end of 2032.

Germany dominates the region with its highly developed recycling infrastructure, processing 70-75% of construction and demolition (C&D) waste through material recovery facilities that depend heavily on horizontal grinding equipment.

The U.K. showcases strong technological adoption, achieving up to 40% improvements in material recovery through integrated equipment systems. France and Spain continue to expand their waste management capabilities in alignment with EU circular economy mandates, positioning them as accelerating growth markets.

Growth in Europe is primarily driven by regulatory harmonization under EU waste directives, circular economy policies, and EPR frameworks that strengthen the economics of material recovery.

Environmental regulations promoting noise and emission reductions are accelerating the adoption of electric grinders, which already account for 25-30% of European sales, compared with 8-10% globally. Moreover, Europe benefits from strong technology leadership, particularly in contamination removal and automated processing systems.

A stringent regulatory landscape such as the EU’s 70% C&D waste recovery requirement and higher national targets in Germany (95%), the Netherlands (90%), and France (85%) continues to stimulate equipment procurement. The market remains competitive yet premium-priced, with equipment costing 15-20% more than North American systems due to advanced engineering standards.

Competitive Landscape

The global horizontal grinder market is advancing through steady technological innovation and moderate consolidation, with the top four manufacturers collectively holding 50-55% market share.

Major leaders including Terex Corporation (CBI), Astec Industries (Peterson), and Rotochopper dominate high-capacity and premium performance segments, while Bandit Industries, West Salem Machinery, and Bruks-Siwertell maintain strong positions in specialized and regional markets. Competition increasingly centers on automation, electrification, remote monitoring, and contamination-removal efficiency rather than pricing alone.

Recent product launches underscore the industry’s shift toward mobility, power, and intelligent control systems. Vermeer’s HG4000TX, introduced in 2025, enhances jobsite access with a tracked undercarriage and high-performance grinding capabilities.

Rotochopper’s L II grinder and BI’s 5900T highlight rising competition around throughput, durability, and operational reliability. Viably’s Komptech Lacero, designed for the North American wood waste and organics recycling sector, reinforces the move toward high-speed, high-horsepower solutions.

Manufacturers are also adapting to stricter emission regulations by adopting Tier 4F/Stage V engines and integrating productivity monitoring tools. Meanwhile, emerging players in Asia-Pacific and India are capturing cost-sensitive segments through competitively priced, locally manufactured equipment. Overall, innovation-led differentiation continues to define the global horizontal grinder market.

Key Industry Developments

- In August 2025, Vermeer introduced the HG4000TX horizontal grinder, engineered with a tracked undercarriage to maximize jobsite mobility. The model delivers high-performance grinding capabilities and offers optional technologies such as the Vermeer coloring system and productivity monitoring tools. Powered by a 536-hp (399.7-kW) CAT® C13B T4F/Stage V diesel engine and equipped with the Series III duplex drum, the HG4000TX is designed to enhance operational efficiency through advanced system integration.

- In 2025, Rotochopper launched its L II horizontal grinder, showcasing the new model during Demo Day 2025 at its Minnesota headquarters.

- In 2025, BI introduced its 5900T horizontal grinder, a model the company states sets new benchmarks in efficiency, power, and durability for heavy-duty grinding applications.

- In 2024, Viably (formerly Komptech Americas) announced the launch of the Komptech Lacero high-speed horizontal grinder, developed to meet the demanding requirements of North America’s wood waste and organics recycling industries. The Lacero underscores Viably’s commitment to advanced, profit-driven resource recovery technologies. It features a robust, precision-engineered design with a 41-inch diameter downswing drum, powered by a CAT® C18 diesel engine and PT Tech clutch, delivering up to 812 horsepower.

Companies Covered in Horizontal Grinder Market

- Vermeer Corporation

- Bandit Industries, Inc.

- Morbark, LLC

- Peterson Pacific Corporation

- CBI (Continental Biomass Industries)

- Rotochopper, Inc.

- Doppstadt

- Komptech

- Diamond Z

- Husmann Umwelt-Technik

- Vecoplan AG

- Terra Select GmbH

- Other Market Players

Frequently Asked Questions

The Horizontal Grinder market is estimated to be valued at US$ 1.6 Bn in 2025.

The key demand driver for the Horizontal Grinder market is the rapid expansion of construction and demolition (C&D) waste recycling, driven primarily by stringent environmental regulations and increasing global emphasis on circular economy practices.

In 2025, the North America region will dominate the market with an exceeding 40% revenue share in the global Horizontal Grinder market.

Among application, wood recycling and processing have the highest preference, capturing beyond 30% of the market revenue share in 2025, surpassing other applications.

Vermeer Corporation, Bandit Industries, Inc., Morbark, LLC, Peterson Pacific Corporation, CBI (Continental Biomass Industries), and Rotochopper, Inc. are a few leading players in the Horizontal Grinder market.