- Medical Devices

- Holter Monitoring Systems Market

Holter Monitoring Systems Market Size, Trends, Share, Growth, and Regional Forecast, 2025 to 2032

Holter Monitoring Systems Market By Product (Wired Holter Monitoring Systems and Wireless Holter Monitoring Systems), by Indication (Atrial fibrillation, Bradycardia, Tachycardia, and Others), End-user, and Regional Analysis from 2025 to 2032

Holter Monitoring Systems Market Share and Trends Analysis

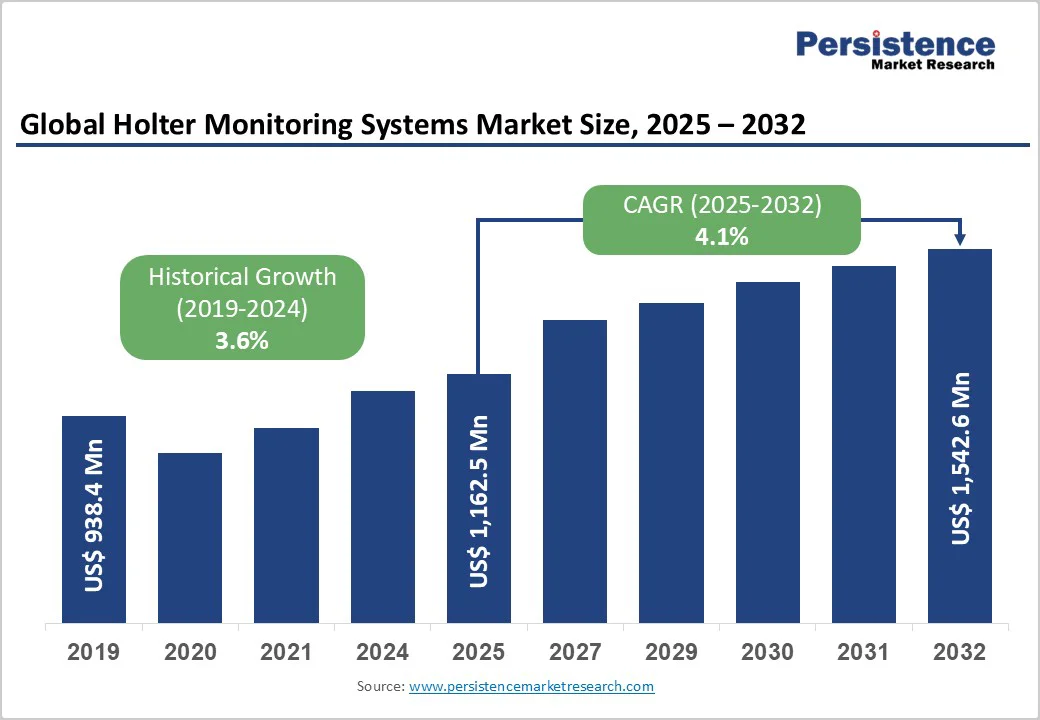

The global holter monitoring systems market size is likely to value US$ 1,162.5 million in 2025 and is projected to reach US$ 1,542.6 million, growing at a CAGR of 4.1% during the forecast period from 2025 to 2032.

The global demand for holter monitoring systems is on the rise due to the increasing prevalence of cardiovascular diseases and arrhythmias, the expansion of hospitals and cardiac specialty clinics, and the growing adoption of remote and home-based cardiac monitoring solutions.

Additionally, technological advancements such as wireless, patch-based, and AI-enabled Holter devices, along with supportive reimbursement frameworks and improved healthcare infrastructure in developing regions, are further driving the market growth.

Key Industry Highlights:

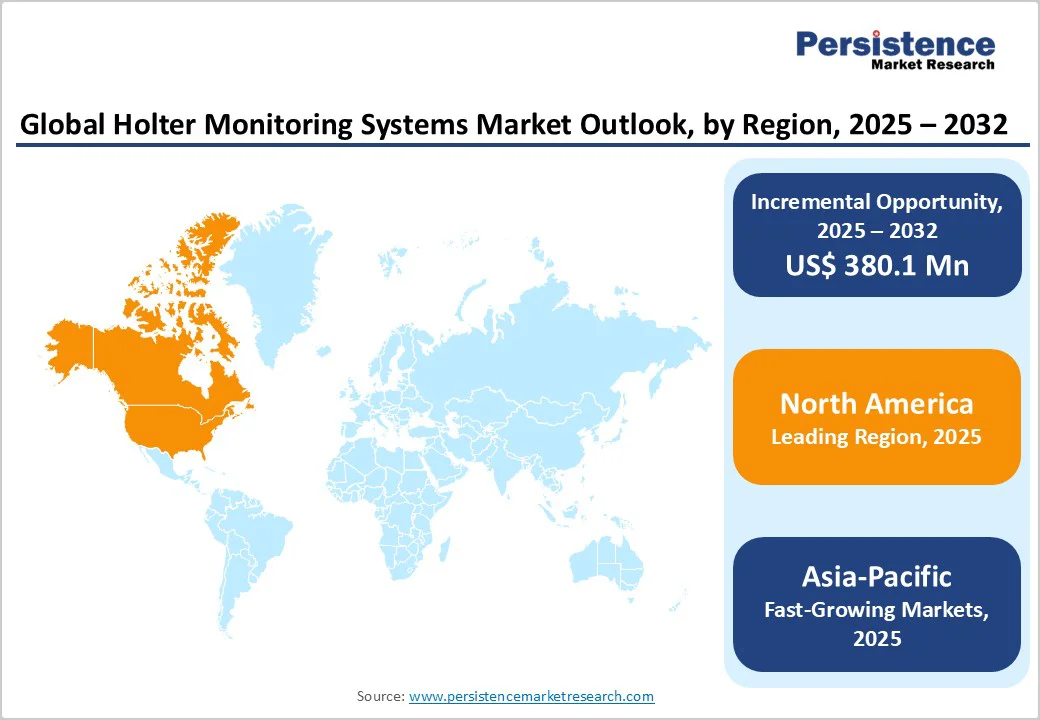

- Leading Region: North America is projected to dominate the global holter monitoring systems market with a revenue share of 39.3% in 2025, driven by the high prevalence of cardiovascular diseases, strong presence of leading medical device manufacturers and advanced healthcare infrastructure.

- Fastest-Growing Region: Asia Pacific is expected to be fastest-growing market for holter monitoring systems with a revenue share of 22.3% in 2025, fueled by the rising burden of cardiovascular disorders, rapid expansion of healthcare infrastructure, increasing adoption of wireless and home-based cardiac monitoring.

- Leading Indication Segment: Atrial fibrillation (AF) is the leading segment, driven by the rising global burden of AF-related complications, increased screening initiatives, and growing adoption of continuous ECG monitoring for early diagnosis and management.

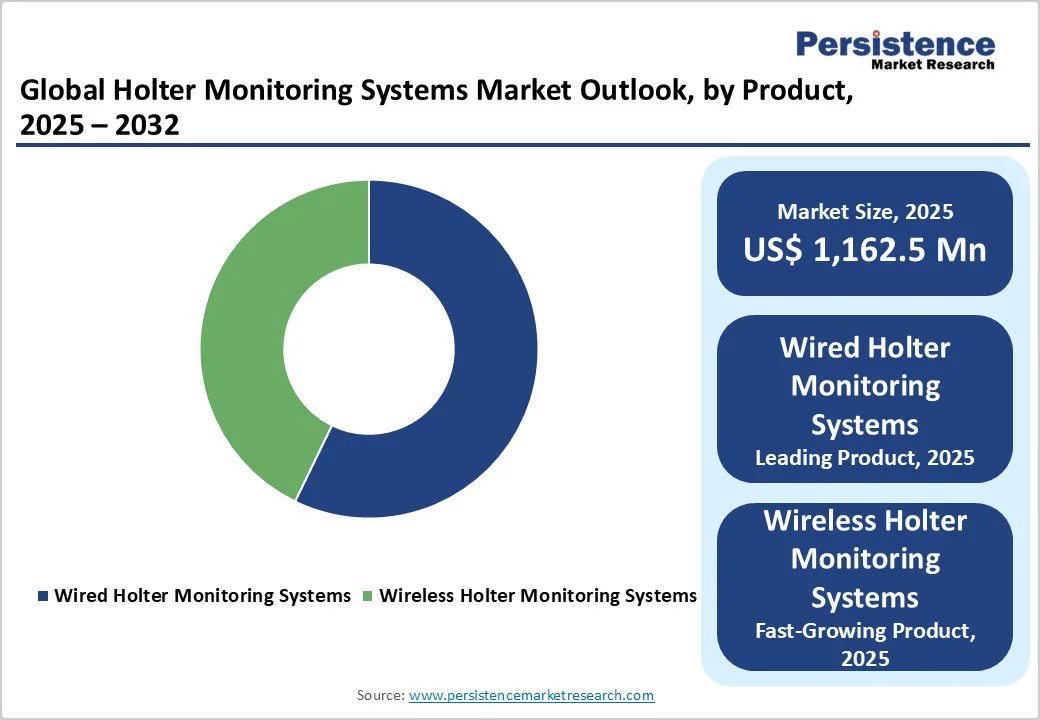

- Wireless Holter monitoring systems are gaining traction due to enhanced convenience and real-time remote monitoring. Their compact design, improved battery life, and seamless data transmission to healthcare providers are driving widespread adoption, particularly in home-based cardiac management.

- Fastest-Growing Indication Segment: Bradycardia is the fastest-growing segment, driven by the increasing prevalence of age-related cardiac rhythm disorders and rising utilization of holter monitoring for accurate detection of slow heart rate abnormalities.

| Key Insights | Details |

|---|---|

| Holter Monitoring Systems Market Size (2025E) | US$ 1,162.5 Mn |

| Market Value Forecast (2032F) | US$ 1,542.6 Mn |

| Projected Growth (CAGR 2025 to 2032) | 4.1% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.6% |

Market Dynamics

Driver - Advancements in Wearable Technology and Rising Cardiovascular Disease Prevalence

Advancements in wearable technology have significantly transformed holter monitoring systems, making them more functional, comfortable, and patient-friendly. Modern devices are now lightweight, compact, and often designed as adhesive patches or small wearable units, allowing patients to carry out their daily activities with minimal disruption.

Extended battery life and low-power electronics enable continuous monitoring for days or even weeks, while wireless connectivity allows real-time data transmission to healthcare providers.

For instance, in April 2025, LifeSignals, Inc., launched the UbiqVue 2AYe Holter System at Heart Rhythm 2025, in partnership with UltraLinQ Healthcare Solutions. The device streamlines cardiac monitoring by securely transmitting ECG data via a patient app, allowing physicians to review interim reports in real time and eliminating the need to mail or retrieve the biosensor.

The growing incidence of cardiovascular conditions, such as arrhythmias, atrial fibrillation, and heart failure, is further driving demand for holter monitoring systems. Continuous cardiac monitoring helps in early diagnosis, timely intervention, and improved patient management, making these devices increasingly essential in both hospitals and remote care settings.

For instance, in 2023, the Centers for Disease Control and Prevention reported that 919,032 people died from cardiovascular disease in the U.S., accounting for roughly one in every three deaths. This highlights the urgent need for reliable, continuous monitoring solutions to reduce morbidity and mortality and improve overall patient outcomes.

Restraints - High Device Costs and Regulatory Barriers Limiting Market Adoption

The high cost of advanced holter monitoring devices, driven by features such as wireless connectivity, extended battery life, and AI-based analysis, significantly limits accessibility, especially in low- and middle-income regions where healthcare budgets are constrained. This cost barrier often restricts adoption in smaller hospitals, clinics, and home-care settings, slowing the overall penetration of these devices in emerging markets.

In addition, regulatory challenges pose substantial obstacles for manufacturers and healthcare providers. Holter monitoring systems must comply with stringent and often varying medical device regulations across different countries, which include extensive documentation, rigorous testing, and clinical validation requirements.

These regulatory complexities lead to lengthy approval timelines, increased development and compliance costs, and delays in product launches, which restrain market growth and limit timely access to advanced cardiac monitoring solutions for patients in need.

Opportunity - AI Integration and Growth in Home-Based Cardiac Monitoring

The rising focus on home-based healthcare is creating significant opportunities for holter monitoring systems. These devices are now being used outside traditional clinical settings, allowing patients to undergo continuous cardiac monitoring from the comfort of their homes. This not only enhances patient convenience and adherence but also enables healthcare providers to track cardiac health remotely, detect irregularities early, and make timely interventions.

Incorporating AI into Holter monitoring systems significantly improves the analysis of continuous ECG data, enabling faster and more accurate detection of arrhythmias and other cardiac abnormalities. AI algorithms help process large volumes of data, identify subtle patterns that are missed by traditional methods, and generate actionable insights for clinicians.

This not only enhances diagnostic accuracy but also supports the development of personalized treatment plans, timely interventions, and better overall patient management.

The integration of AI ultimately transforms Holter monitoring into a smarter, more efficient tool for cardiac care. For instance, in April 2024, a study published in Oxford University Press demonstrated that AI-enabled Holter algorithms could accurately detect ventricular tachycardia and ventricular fibrillation during long-term ECG monitoring.

Trained on large datasets and validated with patient data, these algorithms showed higher sensitivity and specificity than traditional methods, highlighting their potential to enable earlier detection and timely intervention for life-threatening arrhythmias.

Category-wise Analysis

By Product, Wired Holter Monitoring Systems Dominate Globally Due to Their Proven Reliability, Cost-Effectiveness, and Established Clinical Usage

The wired holter monitoring systems segment is projected to dominate the global holter monitoring systems market in 2025, accounting for revenue share of 57.2%. The segment’s strong performance is primarily driven by the high reliability and accuracy in continuous cardiac monitoring, which makes it the preferred choice for hospitals and diagnostic centers.

The systems have a long-standing clinical track record, offering stable performance over extended periods, and are cost-effective compared to advanced wireless alternatives. Additionally, their compatibility with existing hospital infrastructure, easy integration with electronic medical records, and regulatory approvals in major markets further drives the segment’s growth.

By Indication, Atrial Fibrillation Segment Leads the Market Due to High Global Prevalence and Growing Need for Continuous Cardiac Rhythm Monitoring

The atrial fibrillation segment is projected to dominate the global holter monitoring systems market in 2025, with a revenue share of 38.4%. This is due to the high prevalence of atrial fibrillation, growing awareness of its associated stroke and cardiovascular risks, and the critical need for continuous cardiac monitoring for timely diagnosis and management.

Additionally, advancements in holter devices that provide accurate long-term rhythm tracking, coupled with increasing adoption in hospitals and specialty clinics for AF detection and management, further drive this segment’s growth.

By End-user, Hospitals Segment Leads the Market Due to High Patient Volume, Advanced Infrastructure, and the Capability to Manage Complex Cardiac Monitoring

The hospitals segment is projected to dominate the global holter monitoring systems market in 2025, accounting for 52.5% of revenue share. This is due to the high patient volume and the capability to manage complex cardiac cases requiring continuous ECG monitoring in the hospitals.

They also have the infrastructure and trained staff to operate advanced holter systems, analyze data, and integrate findings with electronic medical records. Additionally, hospitals are early adopters of technologically advanced devices, such as wireless and AI-enabled Holter monitors, due to their ability to enhance diagnostic accuracy, improve workflow efficiency, and support advanced cardiac data analytics.

Region-wise Insights

North America Holter Monitoring Systems Market Trends

The North America holter monitoring systems market is projected to dominate the market globally with 39.3% share in 2025 due to the high prevalence of cardiovascular diseases, including arrhythmias and heart failure, which drive demand for continuous cardiac monitoring.

In 2023, the Centers for Disease Control and Prevention (CDC) reported that around 805,000 people in the United States experience a heart attack annually, of which 605,000 are first-time heart attacks and 200,000 occur in individuals with a prior heart attack. This high incidence of cardiovascular events highlights the critical need for continuous cardiac monitoring, driving the adoption of holter monitoring systems.

The region benefits from a well-established healthcare infrastructure with advanced hospitals and cardiac clinics capable of deploying sophisticated Holter monitoring systems. Widespread adoption of wireless and AI-enabled Holter devices, coupled with strong insurance coverage and reimbursement policies for diagnostic cardiac procedures, further supports market growth in the region.

Europe Holter Monitoring Systems Market Trends

Europe holter monitoring systems market is expected to achieve a steady growth, driven by stringent regulatory standards ensuring device quality, increasing geriatric population prone to arrhythmias, and rising investment in outpatient and home-based cardiac monitoring programs.

In March 2025, the British Heart Foundation (BHF) reported that European funders committed over €5 million to research on heart and circulatory diseases, highlighting ongoing investment in cardiovascular health and the growing emphasis on early detection and continuous monitoring of heart conditions, which supports the increasing adoption of holter monitoring systems.

Countries such as Germany, France, and the U.K. are promoting preventive cardiac care through awareness campaigns, For instance, in 2024, on World Heart Day, the European Heart Network (EHN) urged policymakers across Europe to take coordinated action to improve cardiovascular health, emphasizing the need for early detection, prevention, and stronger health systems.

EHN’s seven-year strategic plan aims to reduce premature, preventable cardiovascular deaths by 30% by 2030, reinforcing the growing focus on monitoring and managing heart conditions through technologies such as holter monitoring systems.

Asia Pacific Holter Monitoring Systems Market Trends

Asia Pacific market is projected to reach a CAGR of 5.2% from 2025 to 2032, fueled by the rapidly expanding healthcare infrastructure, rising prevalence of cardiovascular diseases, and increasing awareness of cardiac health.

Growth is further supported by the adoption of advanced wireless holter monitoring systems, government initiatives promoting digital health and remote patient monitoring, and rising disposable incomes, which improve access to diagnostic technologies in countries such as China, India, and Japan.

For instance, in September 2023, on World Heart Day, the Government of India’s Ministry of Health launched a nationwide campaign to raise awareness about hypertension and its link to cardiovascular disease. The initiative promotes active lifestyles, healthy diets, and reduced tobacco and alcohol use, addressing a major public health challenge as over 220 million Indian adults have hypertension, with only 12% under control.

Additionally, the rapid growth of medical tourism and the expansion of private healthcare infrastructure are significantly propelling market growth in the region. Countries such as India, Thailand, and Singapore are emerging as leading medical tourism hubs, attracting international patients seeking affordable yet advanced cardiac diagnostics and treatments, including holter monitoring.

Competitive Landscape

The global holter monitoring systems market is highly competitive, with major players such as Medtronic, Nissha Medical Technologies, Baxter, Koninklijke Philips N.V., iRhythm Inc., GE Healthcare, and LifeSignals are leading the market through continuous product innovation, strategic partnerships, and expansion of their wireless and AI-enabled holter monitoring portfolios.

These companies are also focusing on geographic expansion, mergers and acquisitions, and collaborations with hospitals and home healthcare providers to strengthen their market presence. Additionally, investment in research and development for advanced, patient-friendly monitoring solutions further reinforces their competitive position.

Key Industry Developments:

- In May 2025, iRhythm Technologies, Inc. launched the Zio long-term continuous ECG monitoring (LTCM) system in Japan, branded locally as the Zio ECG Recording and Analysis System. The device offers up to 14 days of uninterrupted ECG monitoring and utilizes a PMDA-approved AI algorithm for advanced arrhythmia detection.

- In May 2024, Ivalink, a digital healthcare solutions provider, launched a new ambulatory cardiac solution for mobile cardiac telemetry (MCT) and Holter monitoring. The solution integrates remote patient monitoring (RPM) technologies with advanced arrhythmia detection algorithms, enabling streamlined deployment and more efficient patient care.

- In May 2024, Royal Philips launched its nationwide ambulatory cardiac monitoring service in Spain, integrating the wearable ePatch with its AI-powered Cardiologs platform. Used by 14 healthcare providers, the solution enhances arrhythmia detection, particularly atrial fibrillation, while improving patient comfort, care access, and clinical outcomes, and reducing costs compared to traditional holter monitors.

Companies Covered in Holter Monitoring Systems Market

- Medtronic

- Nissha Medical Technologies

- Baxter

- iRhythm Inc

- Koninklijke Philips N.V.

- GE Healthcare

- FUKUDA DENSHI

- Spacelabs Healthcare

- AliveCor, Inc

- Cardiac Insight, Inc.

- VitalConnect

- LifeSignals

- Nasiff Associates Inc

- Midmark Corporation

- SCHILLER

- VivaLNK, Inc.

Frequently Asked Questions

The global holter monitoring systems market is projected to be valued at US$ 1,162.5 Mn in 2025.

Rising prevalence of cardiovascular diseases and arrhythmias, growing demand for continuous and remote cardiac monitoring, and increasing adoption of wireless and AI-enabled Holter system are driving market growth.

The global market is poised to witness a CAGR of 4.1% between 2025 and 2032.

Expansion of home-based and ambulatory cardiac monitoring, integration of AI-driven analytics and cloud connectivity, and the development of compact, long-term wearable Holter devices present major growth opportunities in the holter monitoring systems market.

Medtronic, Nissha Medical Technologies, Baxter., Koninklijke Philips N.V., iRhythm Inc., GE Healthcare are some of the key players in the market.