- Smart Packaging

- Holographic Transfer Film Market

Holographic Transfer Film Market Size, Share, and Growth Forecast, 2026 - 2033

Holographic Transfer Film Market By Material Type (PET, BOPP(OPP), Others), Application (Cigarettes & Alcohol, Packaging & Printing, Others), End-Use Industry and Regional Analysis for 2026 - 2033

Holographic Transfer Film Market Size and Trends Analysis

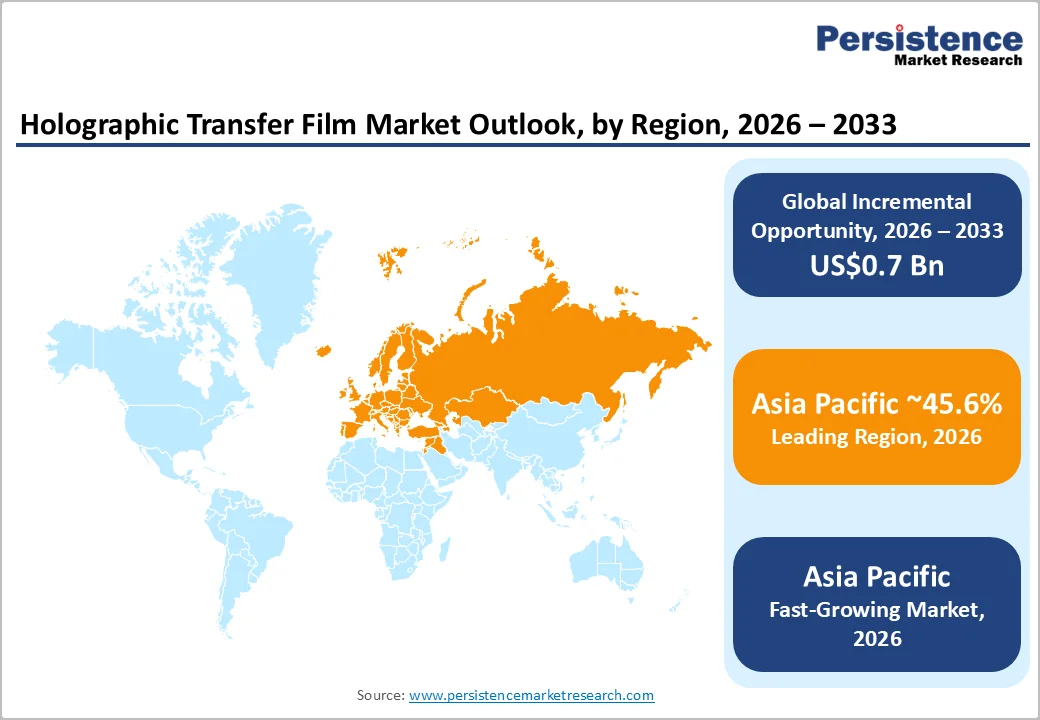

The global holographic transfer film market size is likely to be valued at US$1.8 billion in 2026. It is expected to reach US$2.5 billion by 2033, growing at a CAGR of 4.6% between 2026 and 2033, driven by rising demand for anti-counterfeit solutions and premium packaging aesthetics across regulated and brand-sensitive industries.

Steady demand from cigarette and alcohol labeling, along with growth in security and pharmaceutical track-and-trace applications, continues to support the market. Cost efficiency is improving through manufacturing scale-up and a shift to sustainable films such as BOPP and advanced PET. At the same time, raw material price volatility and regulatory compliance requirements limit short-term growth.

Key Industry Highlights

- Leading Region: Asia Pacific to account for approximately 45.6% of global demand, driven by large-scale cigarette and alcohol packaging, cost-competitive film manufacturing, and dense converting infrastructure across China, India, Japan, and ASEAN.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, supported by expanding consumer markets, rising premiumization in packaging, and increasing adoption of holographic security features, outpacing mature markets in growth momentum.

- Investment Plans: Industry investment is primarily directed toward capacity expansion, digital embossing and converting upgrades, and the development of PVC-free/recyclable holographic film, with sustainability-aligned product lines representing an estimated 25-30% of new capital expenditure among leading suppliers.

- Dominant Material Type: PET is likely to be the dominant material segment, holding approximately 38.7% revenue share in 2026, favored for its superior embossing quality, dimensional stability, and suitability for premium decorative and security applications.

- Leading Application: Cigarettes and alcohol are the leading application segments with roughly 34.3% share, supported by consistent demand for premium visual effects, excise compliance, and anti-counterfeit protection in regulated markets.

| Key Insights | Details |

|---|---|

| Holographic Transfer Film Market Size (2026E) | US$1.8 Bn |

| Market Value Forecast (2033F) | US$2.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Anti-Counterfeit and Security Demand

Escalating global concerns over counterfeiting remain a primary driver of demand for holographic transfer films. These films provide high-value optical security features that are difficult to replicate and are widely deployed across cigarettes, alcohol packaging, pharmaceuticals, and secure documents. Governments and brand owners continue to increase spending on brand protection, particularly in emerging markets where counterfeit risks are higher.

The ability to integrate diffractive and patterned optical elements, along with overt visual cues and covert machine-readable features, positions holographic transfer films as a preferred security substrate. This structurally embedded demand supports stable, mid-single-digit growth through 2033.

Premiumization and Shelf Appeal in FMCG

Brand owners increasingly use holographic effects to enhance shelf differentiation and perceived product value, particularly in premium cigarettes, alcoholic beverages, and cosmetics. Packaging designers are more willing to absorb incremental packaging costs when premium shelf impact supports pricing power and brand positioning.

Adoption is strongest in categories where higher margins offset added packaging expenditure. The expansion of e-commerce and omnichannel retail further increases the importance of visually distinctive packaging. Demand is rising for customized holographic patterns and digitally enabled embellishments that combine tactile finishes with optical diffraction.

Material and Process Innovation

Advances in base film technologies, including embossable PET and high-performance BOPP, along with improved transfer coatings, are enhancing yields and lowering converting costs. Suppliers are launching PVC-free and BOPP-based holographic solutions that align with evolving sustainability requirements and recyclability expectations.

Digital converting technologies and improved cold- and hot-transfer processes reduce setup waste and enable shorter production runs. These innovations are extending the use of holographic film beyond luxury products into broader packaging and printing applications, establishing a long-term pathway for volume growth.

Barrier Analysis - Raw Material Cost Volatility

Holographic transfer films rely heavily on polymer substrates such as PET and BOPP, as well as metallization inputs that are exposed to energy and feedstock price fluctuations. Sudden cost inflation compresses margins and can trigger price pass-throughs that weaken short-term demand.

Smaller converters face greater exposure due to limited hedging capabilities, increasing consolidation pressure within the industry. Historical cost shocks in comparable film sectors have resulted in mid-single-digit margin compression, favoring suppliers with diversified sourcing and long-term supply agreements.

Regulatory and Recycling Constraints

Chemical safety, recyclability, and food-contact regulations restrict certain film formulations and increase compliance costs. Multi-layer holographic laminates can complicate recycling streams, particularly in regions with stringent environmental frameworks.

Compliance often requires reformulation, certification, and capital investment, slowing adoption in sustainability-sensitive FMCG categories. For mid-sized converters, incremental compliance expenditures during regulatory alignment phases can represent several percentage points of annual revenue, affecting near-term profitability.

Opportunity Analysis - PVC-Free and Recyclable Holographic Solutions

The transition from PVC-based films to BOPP or PET alternatives presents a significant growth opportunity where recyclability is mandated. If PVC replacement enables holographic adoption across 10-15% of currently constrained volumes, the incremental addressable opportunity could reach US$100-200 million over the next five to seven years under conservative scenarios.

Suppliers capable of offering certified post-consumer recycled content and mono- and polymeric laminate solutions are well-positioned to capture early demand from sustainability-focused consumer goods brands.

Security Printing and Pharmaceutical Serialization

Holographic transfer films incorporating machine-readable covert features offer cross-selling potential into pharmaceutical serialization and secure document markets. Regulatory pressure to strengthen pharmaceutical supply-chain security is accelerating the adoption of advanced authentication technologies.

Security-grade holographic applications typically command higher revenue per square meter and exhibit stronger customer retention. Growth rates in these applications are expected to exceed decorative uses by one to two percentage points, creating a premium-margin subsegment supported by partnerships between holographic film suppliers and authentication solution providers.

Category-wise Analysis

Material Type Insights

PET is expected to remain the leading material, with a revenue share of 38.7% in 2026, owing to its high mechanical strength, dimensional stability, and superior embossing precision, which are critical for producing consistent diffractive optical effects. Its ability to withstand higher processing temperatures enables deep embossing and fine microstructural definition, making PET the preferred substrate for premium security and decorative applications.

These characteristics are particularly valued in spirits packaging, high-end cosmetics, and luxury labels, where visual clarity and long-term performance are essential. PET-based holographic films are widely used for tamper-evident seals, tax bands, and brand authentication labels in regulated industries.

In premium alcoholic beverages, PET holographic foils are commonly applied to bottle necks and closures to enhance brand differentiation while supporting anti-counterfeit requirements. Similarly, cosmetic brands use PET-based holographic finishes on cartons and labels to convey premium positioning.

While PET continues to dominate by value, its long-term growth trajectory increasingly depends on compatibility with recycling streams, lightweighting initiatives, and the integration of recycled PET content, particularly in regions with stricter environmental regulations.

BOPP (OPP) is the fastest-growing material segment in the holographic transfer film market, driven by its cost efficiency, lower density, and favorable recyclability profile. Compared to PET, BOPP offers material cost advantages and reduced weight, making it attractive for high-volume packaging and price-sensitive applications.

Growth is further supported by PVC replacement initiatives, particularly in regions where regulatory and retailer-led sustainability commitments restrict the use of chlorine-based materials.

Recent advancements in direct-embossable BOPP grades, enhanced surface coatings, and improved metallization techniques have significantly improved optical clarity and embossing depth. These innovations have narrowed the performance gap with PET, enabling BOPP holographic films to be used in mid-tier packaging, promotional labels, daily-sale consumer goods, and retail packaging.

Applications such as personal care packaging, confectionery wraps, and promotional over-labels increasingly utilize BOPP-based holographic films to balance visual impact with cost control. As recycling infrastructure for polyolefin films expands globally, BOPP is expected to gain further share, particularly in mass-market and sustainability-driven packaging formats.

Application Insights

Cigarettes and alcohol are estimated to represent the largest segment, holding a 34.3% revenue share, underpinned by the dual requirements for premium aesthetics and robust anti-counterfeit protection. Holographic elements are widely deployed as tax stamps, excise bands, neck seals, and decorative foils, providing both overt visual authentication and brand differentiation.

These applications are deeply embedded in packaging architectures, resulting in stable and recurring demand.

Regulatory labeling mandates and excise control mechanisms further reinforce the use of holographic transfer films, particularly in markets where illicit trade remains a concern. In the spirits sector, holographic neck labels and closure seals are commonly used to authenticate premium and super-premium brands.

Tobacco packaging relies on holographic tax bands to support traceability and compliance, ensuring consistent consumption volumes despite broader regulatory pressures. The segment’s ability to absorb higher packaging costs, due to relatively high product margins, continues to sustain its leading market position.

Packaging and printing applications are expanding at an accelerated pace as holographic finishes transition from niche decorative uses into mainstream packaging and promotional formats. Improvements in transfer efficiency, compatibility with digital and hybrid printing lines, and reduced minimum order requirements have lowered barriers to adoption.

This has enabled brand owners to deploy holographic effects in short-run campaigns, seasonal packaging, and limited-edition product launches. Holographic transfer films are increasingly used in labels, folding cartons, flexible packaging accents, and point-of-sale materials, where shelf visibility plays a critical role in purchase decisions.

Advancements in sustainability-aligned substrates, including BOPP and lightweight PET variants, support broader use in fast-moving consumer goods. Packaging converters are integrating holographic effects alongside tactile coatings and variable-data printing, enabling brands to combine visual impact with customization. As cost structures continue to improve, packaging and printing applications are expected to remain the primary driver of volume growth in the market.

Regional Insights

North America Holographic Transfer Film Market Trends - Security-Focused Premium Packaging and Digital Embellishment Integration

North America remains a technology-intensive and value-driven market, characterized by high per-unit packaging expenditure in premium cigarettes, spirits, pharmaceuticals, and regulated consumer products.

The U.S. leads regional adoption of advanced holographic security features, particularly in excise-controlled goods and pharmaceutical secondary packaging. Holographic transfer films are widely used for tax bands, tamper-evident seals, and authentication labels, reflecting a strong institutional focus on brand protection and supply-chain integrity.

Investment in digital converting, embellishment, and short-run finishing technologies continues to shape market dynamics. Packaging converters and security printers in the U.S. have expanded capabilities to integrate holographic transfer foils with digital print platforms, enabling customized, variable, and limited-edition packaging.

This has supported increased use of holographic effects in premium spirits, craft beverages, and specialty pharmaceutical packaging. Major brand owners in alcohol and personal care continue to leverage holographic elements to reinforce brand differentiation in highly competitive retail environments.

Regulatory frameworks in North America remain largely sector-specific, offering greater material flexibility than Europe. Sustainability initiatives driven by state-level regulations and large retailers are increasingly influencing material selection. This has encouraged the adoption of PVC-free holographic films, particularly PET and emerging BOPP-based solutions.

Investment activity in the region is focused on equipment upgrades, security-feature integration, and selective acquisitions by packaging groups seeking to expand decorative and authentication capabilities, reinforcing North America’s role as a high-margin, innovation-oriented market.

Europe Holographic Transfer Film Market Trends - Regulation-Led Recyclable and High-Specification Holographic Films

Europe represents a high-value and regulation-driven market for holographic transfer films, underpinned by strong demand from premium packaging, luxury goods, pharmaceuticals, and government-backed anti-counterfeit programs.

Germany, the U.K., France, and Spain collectively account for a substantial share of regional consumption, with applications spanning spirits packaging, cosmetics, secure documents, and branded consumer goods. Regulatory harmonization around chemical safety, recyclability, and packaging waste reduction strongly influences product development and material selection.

European converters and brand owners increasingly favor holographic transfer films that align with mono-material packaging structures, reduced metallization layers, and improved recyclability profiles. This regulatory environment has accelerated innovation in PET-based recyclable holographic foils and lightweight alternatives, while limiting growth prospects for legacy PVC-based solutions.

The region has also seen increased collaboration between material suppliers, converters, and technology developers to accelerate the commercialization of sustainable and security-enhanced holographic products.

Luxury spirits and cosmetics brands headquartered in Europe continue to deploy holographic finishes for brand protection and premium positioning, particularly in export markets vulnerable to counterfeiting. Investment activity is concentrated on advanced security features, eco-designed holographic films, and process optimization, reinforcing Europe’s position as a global reference market for compliant, high-specification holographic applications.

Asia Pacific Holographic Transfer Film Market Trends - High-Volume Tax Band Demand and Cost-Efficient Manufacturing Scale

Asia Pacific leads the global holographic transfer film market with an estimated 45-50% share and is also the fastest-growing region, driven by large consumer populations, extensive cigarette and alcohol packaging volumes, and a dense network of film manufacturers and converters. China, India, Japan, and key ASEAN countries form the core growth engine, benefiting from scale efficiencies, cost-competitive manufacturing, and strong domestic demand.

China and India play a central role as both major consumers and global suppliers of holographic transfer films. The widespread use of holographic tax bands in tobacco and alcohol packaging continues to anchor baseline demand. At the same time, rising consumption of packaged foods, personal care products, and consumer electronics supports diversification into decorative and branding applications.

Japan contributes through high-precision holographic technologies and premium security solutions, particularly for pharmaceuticals, electronics, and export-oriented packaging.

Regulatory environments across the Asia Pacific remain heterogeneous, requiring suppliers to maintain flexible product portfolios that meet both domestic standards and international export requirements. Sustainability initiatives are gaining momentum, especially among multinational brand owners operating in the region, encouraging gradual adoption of recyclable and PVC-free holographic films.

Ongoing capacity expansions, investments in advanced embossing technologies, and launches of sustainability-focused product lines reinforce Asia Pacific’s position as the global volume engine, while steadily improving technical capabilities support movement up the value chain.

Competitive Landscape

The global holographic transfer film market exhibits moderate concentration at the top, with leading global suppliers holding strong positions in technology, intellectual property, and branded security solutions. A long tail of regional and specialist converters supplies price-sensitive and localized demand. Security-focused applications are more concentrated due to certification and IP barriers, while decorative and graphic segments remain fragmented.

Leading companies emphasize innovation in security features, sustainability-driven material development, and vertical integration across film and converting capabilities, and regional capacity expansion. Bundled authentication and certification services are increasingly used to enhance customer lifetime value.

Key Industry Developments

- In March 2025, UFlex Holography reintroduced a specialized premium holographic film for high-impact calendar applications. It unveiled advanced registered transfer metallized board technologies, combining aesthetic appeal with enhanced eco-functionality to support brand promotion and sustainable packaging trends.

- In September 2024, LEONHARD KURZ introduced its “TTR NOVA” thermal-transfer holographic ribbon product line, offering diffractive finishes and dynamic depth effects compatible with flat-head printing systems, thereby enhancing decorative and brand-protection applications.

Companies Covered in Holographic Transfer Film Market

- LEONHARD KURZ GmbH

- Avery Dennison Corporation

- Cosmo Films (Cosmo First)

- Toyo Ink Group (artience)

- Toray Industries

- Taghleef Industries

- Uflex Limited

- SRF Limited

- Jindal Poly Films

- Holostik Group

- Kurz Transfer Products

- Treofan Group

- 3M Company

- Mitsubishi Chemical Group

- ITW (Illinois Tool Works)

- K Laser Technology

- API Group (API Transfer Technologies)

- Polinas

- Light Logics Holography

- Hologram Industries

Frequently Asked Questions

The global holographic transfer film market is estimated to be valued at US$1.8 billion in 2026.

By 2033, the holographic transfer film market is projected to reach US$2.5 billion.

Key trends include rising adoption of anti-counterfeit and security features, increasing use in premium and promotional packaging, material substitution toward PVC-free and recyclable films (PET and BOPP), and growing integration of digital embossing and short-run finishing technologies in packaging and printing applications.

By material type, PET is the leading segment, accounting for approximately 38.7% of total market share, supported by its superior embossing performance, dimensional stability, and suitability for high-value decorative and security applications.

The market is expected to grow at a CAGR of 4.6% between 2026 and 2033.

Major players include LEONHARD KURZ GmbH, Avery Dennison Corporation, Cosmo Films (Cosmo First), Toyo Ink Group (artience), and Toray Industries.