- Pharmaceuticals

- Insomnia Treatment Market

Insomnia Treatment Market Size, Trends, Share, Growth, and Regional Forecast, 2026 - 2033

Insomnia Treatment Market by Treatment Type (Pharmacological Therapies, Non-Pharmacological Therapies), Distribution Channel, and Regional Analysis from 2026 - 2033

Insomnia Treatment Market Share and Trends Analysis

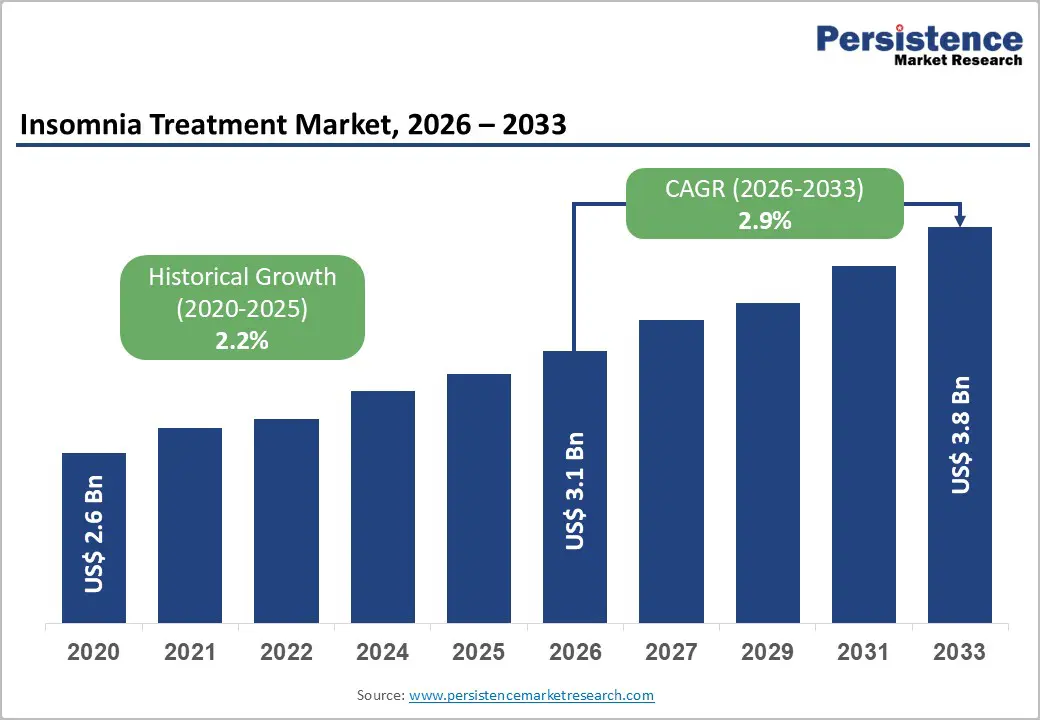

The global insomnia treatment market size is estimated to grow from US$3.1 billion in 2026 to US$3.8 billion by 2033 and is projected to record a CAGR of 2.9% during the forecast period from 2026 to 2033. The market is growing due to rising stress levels, increasing prevalence of sleep disorders, and awareness of mental health care.

Demand is shifting toward safer and longer-acting therapies, including orexin receptor antagonists and melatonin-based drugs. Cognitive Behavioral Therapy for Insomnia (CBT-I) and digital sleep platforms are increasingly preferred as first-line solutions. An aging population, high burden of chronic diseases, and comorbid psychiatric conditions further drive treatment needs. Pharmaceutical advancements, expanding online pharmacy channels, and improved diagnosis at sleep centers support market adoption.

Key Industry Highlights

- Chronic stress, lifestyle imbalance, night-shift work patterns, screen exposure, and high mental health burden are increasing insomnia prevalence globally.

- Digital CBT-I apps, sleep monitoring platforms, and subscription-based sleep improvement programs are expanding rapidly.

- Insomnia in geriatric individuals is rising because of neurological disorders, chronic illness, polypharmacy, and anxiety-related sleep disturbances.

- OTC melatonin products, herbal sleep aids, and soft-dose prescription medications are increasingly sold through online channels.

- Leading Distribution Channel: Retail pharmacies are widely available compared to sleep clinics or digital platforms, increasing reach.

| Key Insights | Details |

|---|---|

|

Insomnia Treatment Market Size (2026E) |

US$3.1 Bn |

|

Market Value Forecast (2033F) |

US$3.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

2.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.2% |

Market Dynamics

Driver - Increasing Adoption of Structured CBT-I in Hospitals

Increasing adoption of structured Cognitive Behavioral Therapy for Insomnia (CBT-I) in hospitals is transforming treatment pathways from medication-centric approaches to evidence-based behavioral models. Hospitals are now developing dedicated behavioral therapy departments, integrating sleep psychologists into care teams, and collaborating with neuropsychiatry specialists to create standardized CBT-I programs. The shift is driven by growing clinical evidence that CBT-I provides longer-lasting benefits, improves sleep hygiene, and reduces relapse rates compared to traditional sedatives. Many multi-specialty hospitals are adopting digital CBT-I modules, mobile apps, video-based therapy, online sleep diaries, and guided cognitive tools to scale accessibility for remote patients. Structured CBT-I is being incorporated into discharge planning for patients with anxiety, chronic stress disorders, and post-treatment insomnia, enabling continuity of care.

Hospitals are linking CBT-I outcomes with sleep monitoring systems to measure improvements in sleep latency, night awakenings, and total sleep duration. This reduces long-term drug dependency, minimizes side effects, and supports safer geriatric treatment. The approach is now recognized as a reimbursable and protocol-based therapy in many healthcare systems, strengthening its adoption across global hospital networks.

Restraints - Off-label Medication Misuse

Off-label medication misuse is a major restraint in the insomnia treatment market, as many patients rely on alternative options such as antidepressants, antipsychotics, muscle relaxants, sedative painkillers, or alcohol to induce sleep rather than seeking clinically validated insomnia treatments. This practice often begins with informal recommendations from family, chemists, or acquaintances, and later becomes habitual because the patient perceives immediate relief without consulting a physician. Such misuse diverts patients away from prescribed insomnia-specific drugs like orexin antagonists or controlled hypnotics, reducing physician-led intervention and limiting the market’s long-term revenue potential.

Additionally, antidepressants and antipsychotics are often available at lower cost or through leftover prescriptions, making them a preferred self-managed solution among young adults, working professionals, and elderly caregivers. Alcohol consumption as a sleep-inducing agent further worsens dependency and increases morning fatigue, leading patients to avoid medical consultations. As symptoms appear manageable through self-medication, individuals delay diagnosis, reducing demand for CBT-I, prescription drugs, and structured treatment pathways. This ultimately suppresses therapy conversion rates, weakens prescription adherence cycles, and increases clinical complications.

Opportunity - Long-Acting Molecules with No Withdrawal Risks

The development of long-acting, extended-release hypnotic molecules presents a significant opportunity in the insomnia treatment market. Traditional sedative-hypnotics, including benzodiazepines and short-acting non-benzodiazepine drugs, often pose challenges such as rebound insomnia, daytime drowsiness, and dependence with long-term use. These limitations lead to poor patient adherence and cautious prescribing by physicians, especially in chronic insomnia cases. By contrast, new long-acting formulations are designed to maintain stable therapeutic levels throughout the night, ensuring uninterrupted sleep while minimizing next-day residual effects.

Importantly, these molecules are engineered to avoid withdrawal symptoms and rebound insomnia, which are common barriers in conventional therapies. This safety profile enhances patient compliance and builds trust with healthcare providers, encouraging broader adoption in both hospital and outpatient settings. Moreover, such drugs can command a premium due to their clinical advantages, improved quality-of-life outcomes, and reduced need for polytherapy or combination therapies. As patient awareness of safe, effective long-term sleep management grows, long-acting, non-addictive hypnotics are well positioned to capture a substantial share and become a preferred choice for insomnia management globally.

Category-wise Analysis

By Treatment Type Insights

Pharmacological therapies dominate the insomnia treatment market because they offer fast, tangible relief from sleep disturbances, which patients highly value for immediate improvement. Prescription drugs such as benzodiazepines, non-benzodiazepine hypnotics, melatonin agonists, and orexin receptor antagonists are widely used across adults and the elderly, who represent the largest patient segments. These therapies are easily accessible through retail and hospital pharmacies, enabling widespread adoption compared to non-pharmacological options like CBT-I, which require trained therapists or digital platforms. Additionally, chronic insomnia patients often rely on medications for long-term symptom control, further increasing usage and market share. Healthcare systems and insurance coverage are also better structured to support pharmacological interventions. While non-pharmacological treatments are gaining attention for their safety and long-term benefits, adoption remains limited due to awareness, patient motivation, and infrastructure constraints, keeping pharmacological therapies as the leading segment in terms of revenue and market penetration.

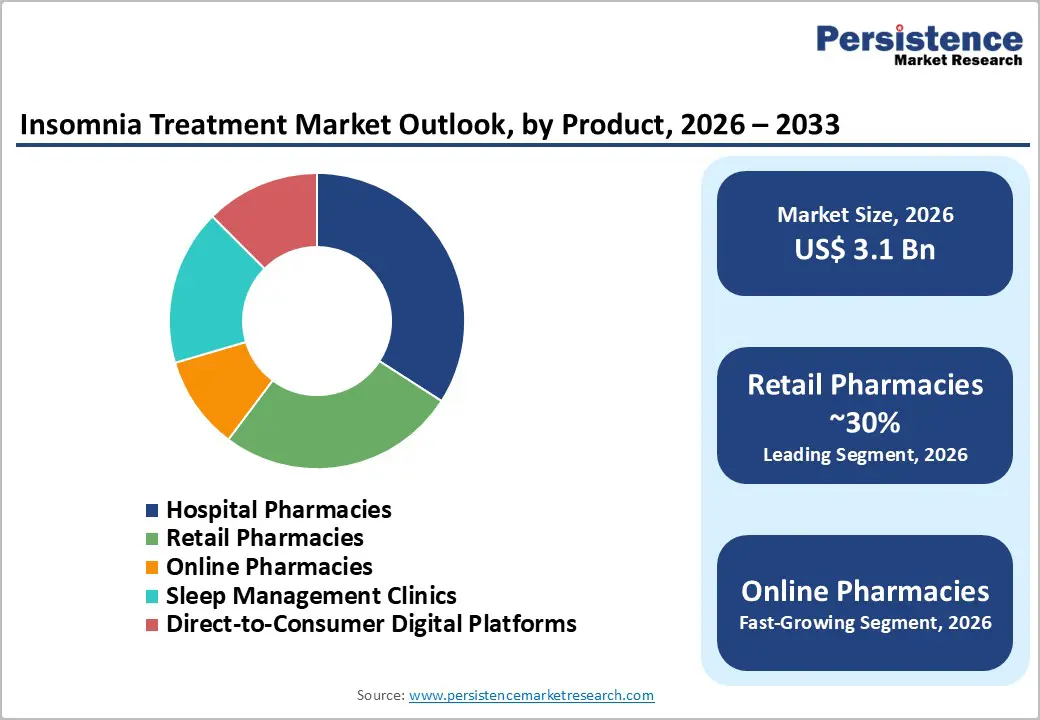

By Distribution Channel Insights

Retail pharmacies lead the insomnia treatment market because they provide convenience, accessibility, and a broad product range for patients. They stock both over-the-counter sleep aids, such as melatonin, herbal supplements, and antihistamines and prescription medications like benzodiazepines, Z-drugs, and orexin receptor antagonists, catering to both casual users and chronic insomnia patients. Chronic users often require frequent refills, and the widespread presence of retail pharmacies in urban, semi-urban, and rural areas makes them the most accessible point.

Many patients also prefer consulting pharmacists for advice on mild sleep disturbances, avoiding the need for hospital visits or specialist appointments. While hospital pharmacies play a key role in initial prescriptions and clinical supervision, their reach is comparatively limited. Emerging channels like online pharmacies and digital platforms are growing rapidly, but still have smaller adoption due to regulatory restrictions, trust issues, and the need for physician prescriptions. This combination of availability, convenience, and comprehensive product offerings ensures that retail pharmacies capture the highest market share.

Region-wise Insights

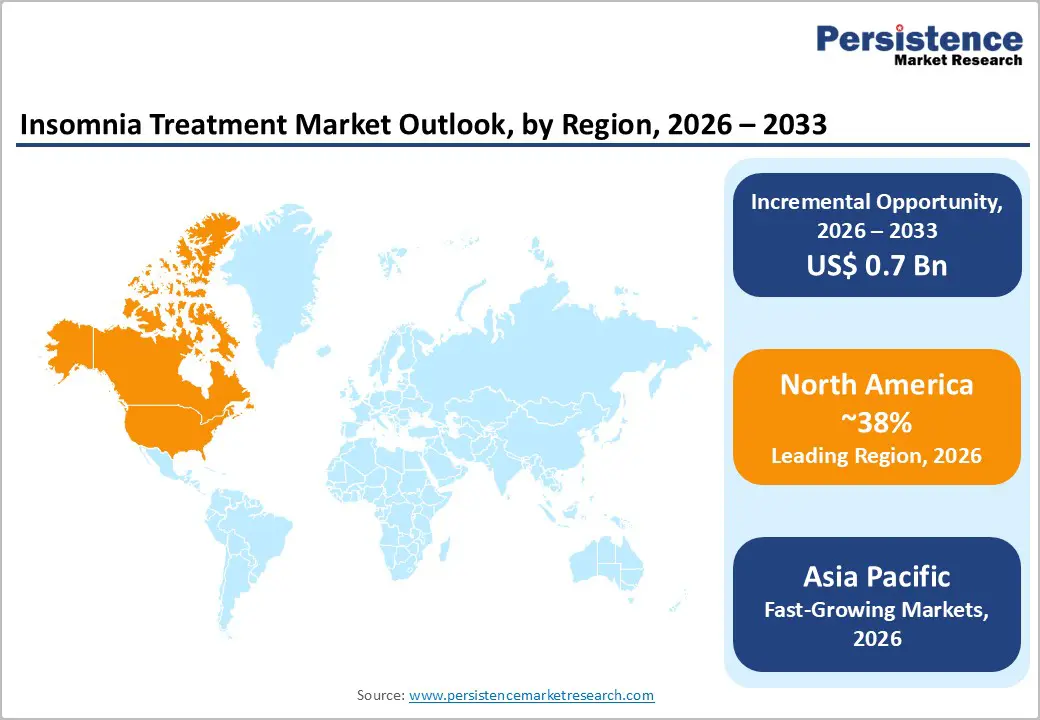

North America Insomnia Treatment Market Trends

North America leads the global insomnia treatment market due to the high prevalence of sleep disorders, strong healthcare infrastructure, and widespread awareness of mental health. In the U.S., rising stress levels, long working hours, and lifestyle-induced sleep disruptions are driving demand for both pharmacological and non-pharmacological treatments. Prescription medications such as benzodiazepines, Z-drugs, melatonin agonists, and orexin receptor antagonists dominate, supported by insurance coverage and easy access through retail and hospital pharmacies.

Cognitive Behavioral Therapy for Insomnia (CBT-I) and digital sleep therapeutics are gaining traction, especially among tech-savvy populations seeking long-term behavioral interventions. The U.S. also shows rapid adoption of digital platforms that integrate AI-guided sleep tracking with therapy, enhancing patient adherence. Research investment, regulatory approvals for new drug classes, and increasing physician awareness of safer long-term options further strengthen market leadership. Combined, these trends make North America the largest and most innovative market for insomnia treatment globally.

Asia Pacific Insomnia Treatment Market Trends

The Asia Pacific region is emerging as a high-growth market for insomnia treatment due to rapid urbanization, lifestyle changes, increasing work-related stress, and growing awareness of sleep health. Countries such as China, Japan, India, and South Korea are witnessing a rising prevalence of sleep disorders, driving demand for both prescription medications and over-the-counter sleep aids. Pharmacological therapies, including benzodiazepines, non-benzodiazepine hypnotics, and melatonin-based drugs, dominate treatment, while non-pharmacological options such as Cognitive Behavioral Therapy for Insomnia (CBT-I) and digital therapeutics are gradually gaining acceptance. Expanding healthcare infrastructure, an increasing number of sleep clinics, and rising digital health adoption are driving market growth. Additionally, online pharmacies and e-commerce platforms are improving access to insomnia treatments in remote areas. Taken together, these trends position the Asia-Pacific as a fast-growing and strategically important market for insomnia therapies.

Competitive Landscape

The insomnia treatment market is highly competitive and fragmented, with players focusing on innovation, drug formulation improvements, and digital therapy solutions. Companies are investing in research and development of safer, long-acting molecules, extended-release formulations, and personalized therapies to differentiate offerings. Strategic partnerships, mergers, and acquisitions are common to expand product portfolios and geographic reach. Market participants also emphasize digital integration, including AI-guided CBT-I platforms and wearable device compatibility, to enhance patient engagement.

Key Industry Developments:

- In December 2025, Boots Online Doctor launched a new insomnia treatment service aimed at adults experiencing chronic sleep difficulties. The service offered expert guidance, personalised treatment plans, and practical advice on sleep hygiene. Patients also had access to prescription medications when deemed appropriate, ensuring a comprehensive approach to managing and improving sleep patterns.

Companies Covered in Insomnia Treatment Market

- Merck & Co., Inc.

- Pfizer Inc.

- Sanofi S.A.

- Eisai Co., Ltd.

- Takeda Pharmaceutical Company Limited

- Teva Pharmaceutical Industries Ltd.

- Vanda Pharmaceuticals Inc.

- Idorsia Ltd

- Johnson & Johnson

- GlaxoSmithKline plc

- Bayer AG

- Others

Frequently Asked Questions

The global insomnia treatment market is projected to be valued at US$3.1 Bn in 2026.

Increasing stress, long working hours, lifestyle changes, and mental health issues are contributing to higher rates of insomnia worldwide.

The global market is poised to witness a CAGR of 2.9% between 2026 and 2033.

Extended-release hypnotics with minimal withdrawal risk can capture chronic patient segments.

Merck & Co., Inc., Pfizer Inc., Sanofi S.A., Eisai Co., Ltd., and others.