- Pharmaceuticals

- Gastrointestinal Stromal Tumor (GIST) Treatment Market

Gastrointestinal Stromal Tumor (GIST) Treatment Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Gastrointestinal Stromal Tumor (GIST) Treatment Market by Drugs (Imatinib, Ripretinib, Crenolanib, Regorafenib, Avapritinib, Sunitinib, Others), Treatment Type, Distribution Channel, and Regional Analysis from 2026 to 2033

Gastrointestinal Stromal Tumor (GIST) Treatment Market Share and Trends Analysis

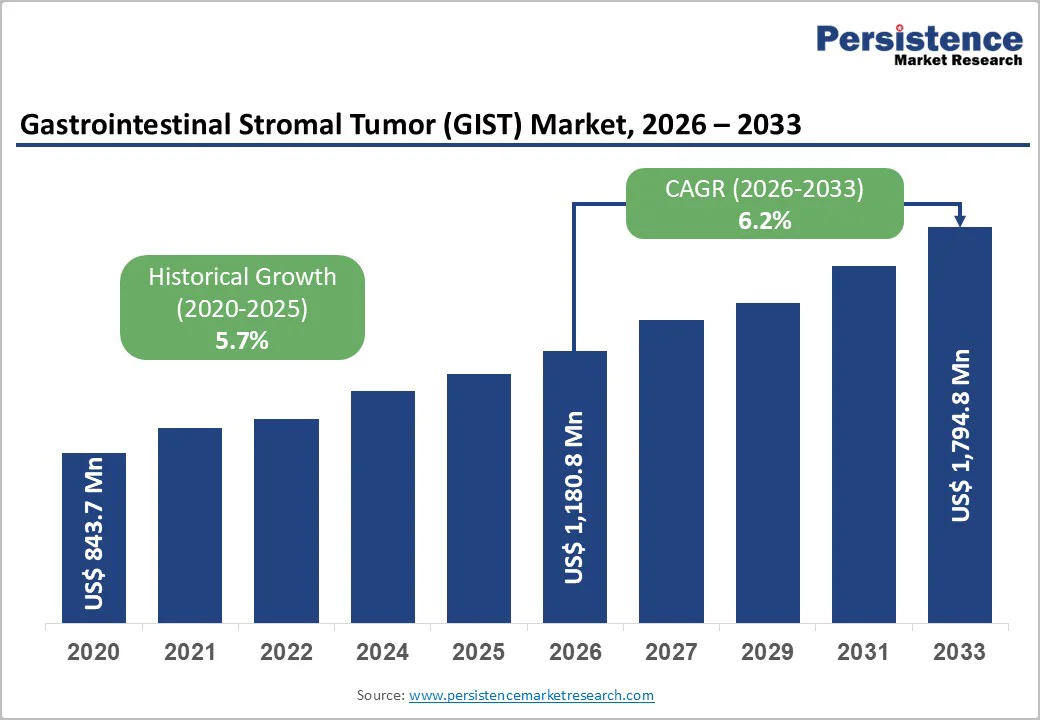

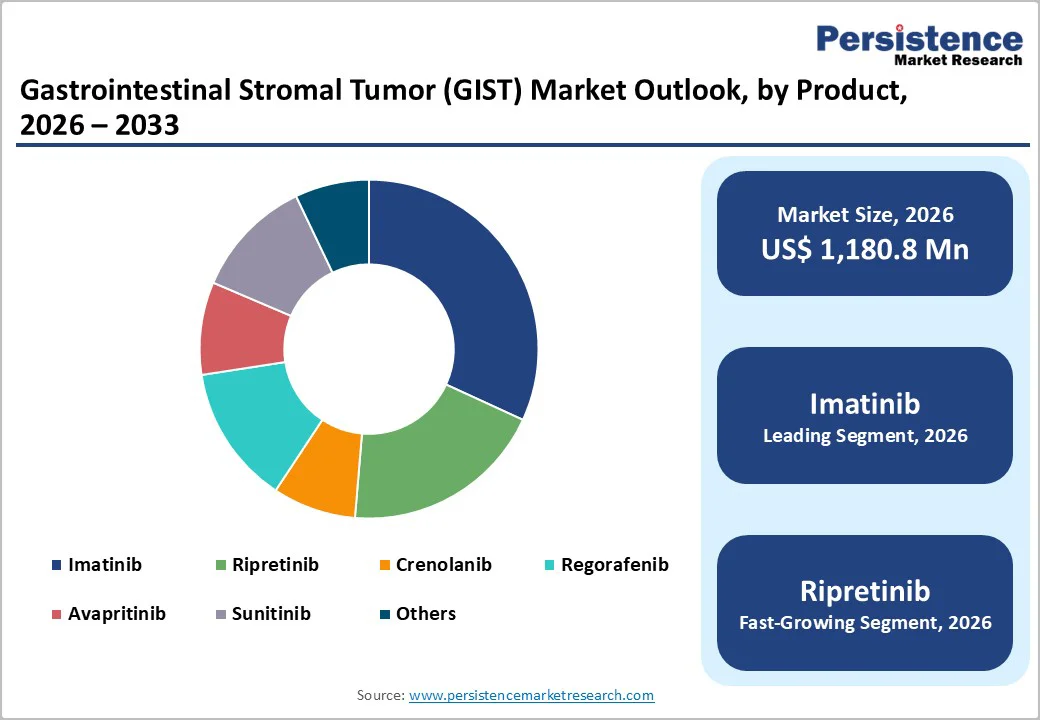

The global gastrointestinal stromal tumor (GIST) treatment market size is estimated to grow from US$1,180.8 million in 2026 to US$1,794.8 million by 2033. The market is projected to record a CAGR of 6.2% during the forecast period from 2026 to 2033.

Rise in incidence of rare cancers, increasing diagnosis rates, and strong adoption of targeted therapies such as imatinib, sunitinib, regorafenib, ripretinib, and avapritinib has encouraged the need for tumor treatment. Advancements in molecular testing for KIT and PDGFRA mutations further support personalized treatment decisions.

Growing awareness among oncologists, expanding access to oncology centers, and the introduction of fourth-line and mutation-specific therapies are boosting market growth. However, high treatment costs, drug resistance, and limited options for advanced or wild-type GIST remain major constraints. Emerging pipeline molecules and expanding approvals across regions present significant future opportunities.

Key Industry Highlights

- The GIST market is witnessing strong uptake of mutation-specific therapies such as avapritinib for PDGFRA D842V mutations, transforming outcomes for historically resistant cases.

- A number of hospitals and clinical institutions are adopting next-generation sequencing (NGS) for accurate detection of GIST mutations.

- Real-world data from hospital registries and long-term follow-up studies are increasingly influencing treatment guidelines.

- Imatinib is the primary and most widely prescribed treatment for newly diagnosed GIST.

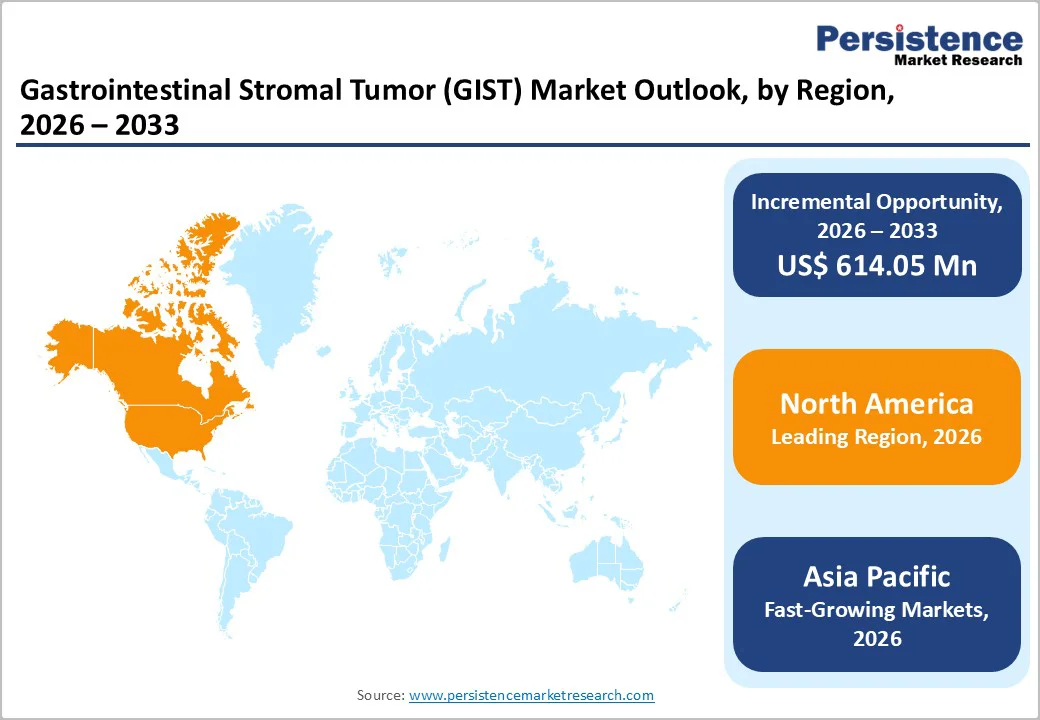

- North America is leading due to the highest adoption of targeted therapies such as imatinib, sunitinib, regorafenib, ripretinib, and avapritinib.

| Key Insights | Details |

|---|---|

| Gastrointestinal Stromal Tumor (GIST) Treatment Market Size (2026E) | US$1,180.8 Mn |

| Market Value Forecast (2033F) | US$1,794.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.2% |

| Historical Market Growth (CAGR 2020 to 2024) | 5.7% |

Market Dynamics

Driver - Higher Diagnosis Rates Due to Improved Imaging

The rising use of advanced imaging technologies is significantly improving the early diagnosis of Gastrointestinal Stromal Tumors (GIST). High-resolution CT scans, PET-CT imaging, and endoscopic ultrasound are increasingly available in tertiary hospitals, enabling precise visualization of small or asymptomatic tumors that were previously missed.

These modalities help detect lesions in complex anatomical locations, assess metastatic spread, and guide biopsy decisions more accurately. Earlier detection allows clinicians to initiate targeted therapies like imatinib at the right disease stage, improving long-term outcomes.

Enhanced imaging also supports treatment planning, monitoring response, and identifying resistance or recurrence earlier. As imaging access expands globally, diagnosis rates are rising, directly boosting demand for GIST testing and targeted treatment pathways.

Restraints - High Cost of Targeted TKIs Limits Access in Low

The high cost of targeted tyrosine kinase inhibitors (TKIs) remains a major barrier for GIST patients in low- and middle-income regions, even as generics enter the market. Many patients cannot afford long-term therapy, as treatment often continues for years and requires continuous monitoring.

Limited reimbursement frameworks, uneven insurance coverage, and high out-of-pocket expenses further restrict access. Hospitals in resource-constrained settings also struggle to stock multiple advanced TKIs, reducing treatment choices. As a result, many patients start therapy late, discontinue prematurely, or rely on less effective alternatives, widening survival gaps between high-income and developing regions.

Opportunity - Combination Therapy Development

Combination therapy in Gastrointestinal Stromal Tumor (GIST) is emerging as a promising strategy to overcome limitations of monotherapy. Traditional tyrosine kinase inhibitors (TKIs) like imatinib, sunitinib, and regorafenib often face resistance over time, especially in patients with secondary mutations.

To enhance efficacy, researchers are exploring combinations of TKIs with immunotherapies, such as immune checkpoint inhibitors, to stimulate anti-tumor immune responses. Additionally, metabolic inhibitors targeting SDH-deficient or wild-type GIST are being evaluated to exploit tumor-specific metabolic vulnerabilities.

These combination approaches aim to improve progression-free survival, reduce resistance, and address unmet needs in advanced or refractory GIST. Pharmaceutical companies are actively investing in clinical trials, positioning combination therapy as a key differentiator in the competitive GIST treatment landscape, while also creating opportunities for tailored, personalized treatment protocols.

Category-wise Analysis

By Drugs Insights

Imatinib is the leading drug in the GIST market due to its established efficacy, safety, and widespread adoption. It is the first-line standard of care for newly diagnosed GIST patients, particularly those with KIT or PDGFRA mutations, offering high response rates and long progression-free survival. Its early market entry in 2002 allowed it to gain global recognition and trust among oncologists.

Additionally, the availability of generic versions has improved affordability and accessibility worldwide. Imatinib’s proven long-term outcomes, strong clinical evidence, and broad patient base solidify its position as the most widely used and commercially dominant therapy in GIST treatment.

By Distribution Channel Insights

Hospital pharmacies are the leading distribution channel for GIST therapies due to their central role in specialized cancer care. Most GIST patients are treated in tertiary hospitals or oncology centers where prescription, monitoring, and follow-up can be closely managed. Targeted therapies such as imatinib, sunitinib, and regorafenib often require dosage adjustments, laboratory monitoring, and management of side effects, which hospitals are equipped to provide.

Additionally, hospital pharmacies facilitate insurance coverage, reimbursement, and patient assistance programs, making high-cost therapies more accessible. The combination of clinical oversight, patient volume, and financial support makes hospital pharmacies the primary channel for GIST drug distribution worldwide.

Regional Insights

North America Gastrointestinal Stromal Tumor (GIST) Trends

North America leads the Gastrointestinal Stromal Tumor (GIST) Treatment Market, driven by advanced healthcare infrastructure, high adoption of targeted therapies, and robust diagnostic capabilities. Widespread use of TKIs such as imatinib, sunitinib, and ripretinib is supported by extensive molecular testing for KIT and PDGFRA mutations, enabling personalized treatment.

In the U.S., early diagnosis and guideline-based therapy sequencing are facilitated by specialized oncology centers and strong insurance coverage, including patient assistance programs for expensive therapies. Additionally, ongoing clinical trials and real-world evidence studies help optimize treatment. Rising awareness among clinicians and patients, coupled with regulatory support, reinforces North America’s dominance in the GIST landscape.

Asia Pacific Gastrointestinal Stromal Tumor (GIST) Treatment Market Trends

Asia Pacific is emerging as a high-growth region in the Gastrointestinal Stromal Tumor (GIST) Treatment Market, driven by increasing awareness, improving healthcare infrastructure, and expanding access to advanced therapies. Rising adoption of targeted treatments such as imatinib, sunitinib, and regorafenib is supported by the growing availability of molecular diagnostic testing for KIT and PDGFRA mutations.

Countries like China, Japan, and India are witnessing higher diagnosis rates, increasing the patient pool for first- and later-line therapies. Additionally, expanding government support, rising private oncology investments, and patient assistance programs are improving affordability. These factors collectively position the Asia Pacific as a rapidly developing market for GIST treatments.

Competitive Landscape

The Gastrointestinal Stromal Tumor (GIST) Treatment Market features a competitive landscape driven by innovation in targeted therapies, later-line treatments, and mutation-specific drugs.

Companies compete by developing new TKIs, exploring combination therapies with immunotherapy or metabolic inhibitors, and expanding access in emerging regions. Market differentiation relies on pricing strategies, patient assistance programs, and the availability of molecular diagnostic support.

Key Industry Developments:

- In August 2024, the FDA cleared an investigational new drug (IND) application for ziftomenib as a therapy for patients with advanced gastrointestinal stromal tumors (GISTs), according to a press release from its developer, Kura Oncology, Inc.

Companies Covered in Gastrointestinal Stromal Tumor (GIST) Treatment Market

- Novartis

- Pfizer

- Bayer AG

- Deciphera Pharmaceuticals

- Blueprint Medicines

- Taiho Pharmaceutical

- Daiichi Sankyo

- Roche

- Bristol-Myers Squibb

- Sun Pharmaceutical

- Natco Pharma

- Others

Frequently Asked Questions

The global Gastrointestinal Stromal Tumor (GIST) Treatment Market is projected to be valued at US$1,180.8 million in 2026.

The increasing prevalence of gastrointestinal stromal tumors worldwide is expanding the patient pool for targeted therapies.

The global market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Combining TKIs with immunotherapy or metabolic inhibitors can overcome resistance and improve outcomes.

Novartis, Pfizer, Bayer AG, Deciphera Pharmaceuticals, Blueprint Medicines, and others.