- Plastics, Polymers & Resins

- Furniture Films and Foils Market

Furniture Films and Foils Market Size, Share, and Growth Forecast, 2025 - 2032

Furniture Films and Foils Market By Material Type (Polyvinyl Chloride (PVC), Polyester (BOPET), Others), Product Type (Self-Adhesive Films, Laminates and Over-Laminates, Others), Application, End-user, and Regional Analysis for 2025 - 2032

Furniture Films and Foils Market Size and Trends Analysis

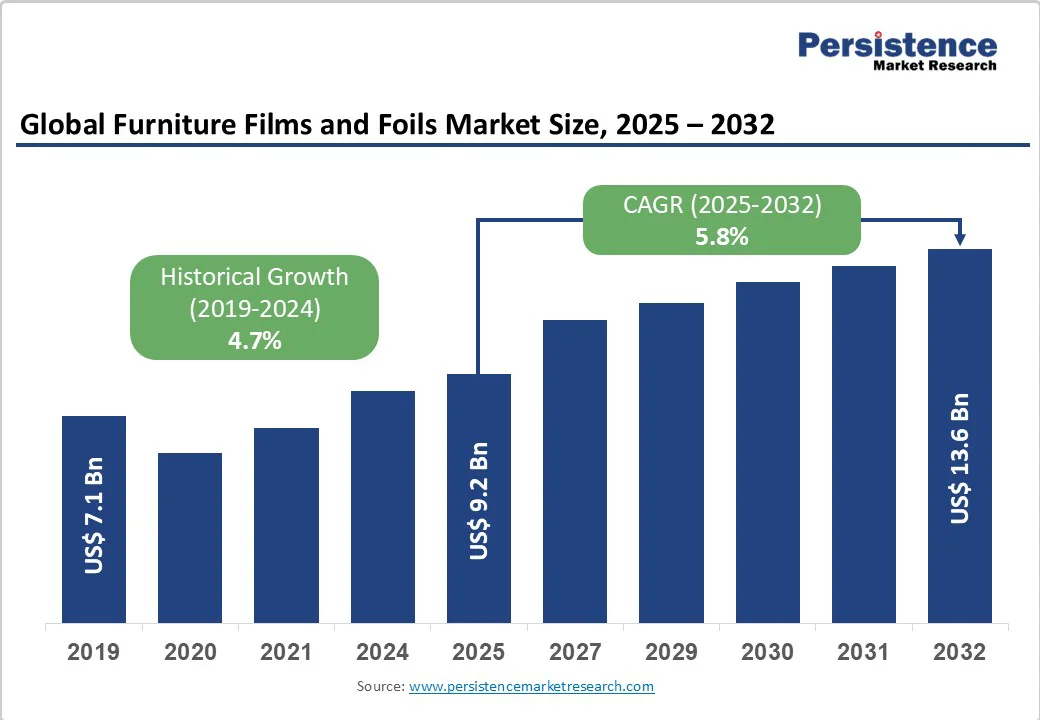

The global furniture films and foils market size is likely to be valued at US$9.2 Billion in 2025 and is expected to reach US$13.6 Billion by 2032, growing at a CAGR of 5.8% during the forecast period from 2025 to 2032, driven by rapid urbanization, demand for cost-efficient decorative materials, and increasing emphasis on sustainable, high-performance substrates.

Rising home renovations and a growing furniture sector in Asia Pacific are boosting demand. PVC-free, recyclable films are reshaping material trends, with furniture foils gaining traction as affordable, customizable alternatives to veneers. Eco-friendly coatings and advanced printing further enhance appeal for OEMs and designers.

Key Industry Highlights

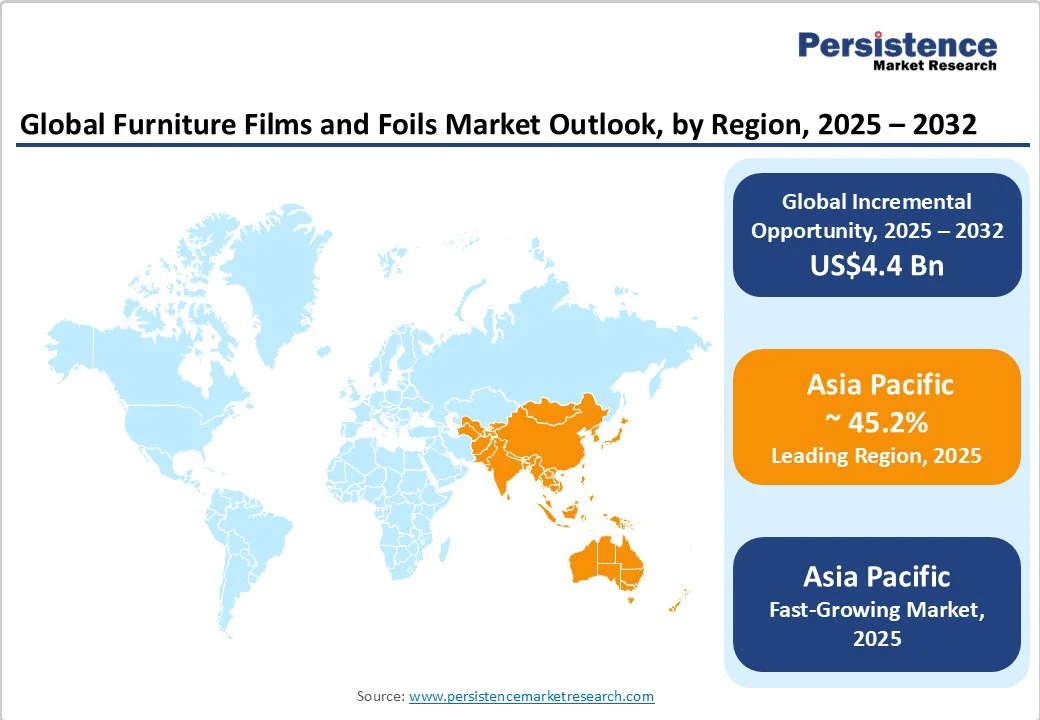

- Leading Region: Asia Pacific dominates the global market with approximately 45.2% share in 2025, driven by large-scale furniture manufacturing hubs in China, India, and Southeast Asia, and strong export capabilities.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, registering a CAGR of 6.3% between 2025 and 2032, supported by rising urbanization, modular furniture adoption, and increasing digital printing and customization of decorative films.

- Investment Plans: Major manufacturers are investing in capacity expansion and sustainable product development. Notable initiatives include LG Hausys’ production capacity expansion in South Korea (2025) and Cosmo Films’ PVC-free decorative film launch in India (2024), reflecting a strategic focus on eco-friendly and high-performance product lines.

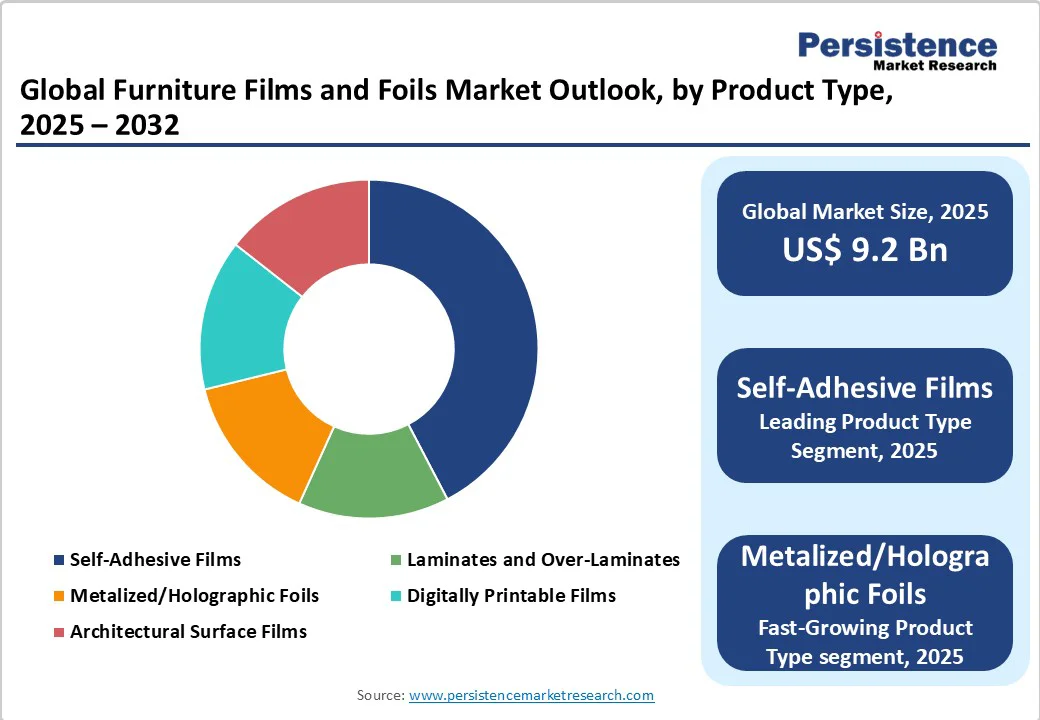

- Leading Product Type: Self-adhesive films account for 47% of market revenue in 2025, owing to ease of installation, versatility in DIY and professional projects, and growing demand for low-VOC and instant-application solutions in furniture refurbishment and interior decoration.

- Leading Application: Doors and windows remain the largest application segment, holding 55%, due to their extensive use in door skins, window frames, and architectural laminates that combine durability, UV resistance, and customizable finishes.

| Key Insights | Details |

|---|---|

| Furniture Films and Foils Market Size (2025E) | US$9.2 Bn |

| Market Value Forecast (2032F) | US$13.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Cost-Efficient Decorative Alternatives and Retrofit Demand

Furniture films and foils offer an economical substitute for natural veneers and laminates, meeting consumer preferences for attractive, durable finishes at lower costs. They provide quick installation, lightweight logistics, and high print adaptability, allowing manufacturers to offer multiple design options.

As construction and refurbishment activity increases, these products are increasingly adopted in the mid-market furniture segment, contract furnishings, and retail interiors. The rapid rise in DIY renovation trends in North America and Europe further amplifies recurring aftermarket sales.

Technological Innovation in Sustainable and Printable Films

Material innovation is transforming the market, with manufacturers introducing PVC-free, mono-polymer, and digitally printable films. These advancements respond to tightening environmental regulations and customer sustainability commitments. Recyclable substrates, solvent-free coatings, and digitally print-ready surfaces improve environmental compliance while enabling shorter production runs and bespoke designs. This convergence of sustainability and personalization is encouraging OEM partnerships and driving premium product margins across commercial and residential segments.

Expanding Furniture Manufacturing in Asia Pacific

Asia Pacific accounts for nearly half of global decorative film and foil demand, supported by large-scale manufacturing hubs in China, India, and Southeast Asia. Rapid industrialization and urban housing expansion have increased the consumption of low-cost decorative films in mass-market furniture production.

With labor and cost advantages, regional suppliers are capturing global export markets while meeting domestic demand for affordable home décor. The region’s ability to scale production efficiently positions it as the dominant contributor to global growth.

Barrier Analysis - Competition from High-Durability Laminates and Veneers

High-pressure laminates and engineered veneers continue to dominate premium and heavy-use applications due to superior scratch and chemical resistance. In commercial furniture and kitchen installations, durability often outweighs cost savings, restricting penetration of films and foils.

This limits average selling prices and caps volume expansion in certain high-end segments. The growing preference for hybrid laminates incorporating decorative foils partially mitigates this challenge but does not eliminate the material substitution threat.

Raw Material Volatility and Supply Chain Concentration

PVC, PET, and specialty coating materials are linked to petrochemical markets, making them vulnerable to global price fluctuations. Limited supplier bases for advanced coatings and adhesives add to procurement risks. Short-term feedstock shortages or logistics disruptions can compress converter margins and delay new projects. Maintaining multi-sourcing strategies and investing in regionalized supply networks have become essential risk-mitigation measures for manufacturers and distributors.

Opportunity Analysis - Emergence of Functional and Smart Decorative Films

Functional films integrating antimicrobial coatings, light diffusion, or printed electronics are expanding the product’s utility beyond aesthetics. These innovations address growing demand in healthcare, hospitality, and commercial interiors for surfaces with added hygiene or illumination benefits.

The market for functional decorative films is expected to represent several hundred million dollars in incremental revenue by 2030. Early adopters who integrate technical coatings into decorative products are well-positioned for above-average profitability.

Growing Retrofit and Aftermarket Opportunities

The retrofit and DIY furniture segments represent a rapidly growing revenue channel. Self-adhesive decorative films are increasingly used for quick, cost-effective upgrades in residential and commercial interiors. As refurbishment cycles shorten and consumers favor sustainable redecoration methods over full replacements, demand for peel-and-apply decorative films is rising sharply. Manufacturers offering ready-to-install kits and installer certification programs are expanding their market share in both developed and emerging economies.

Category-wise Analysis

Product Type Insights

Self-adhesive decorative films dominate the market, representing an estimated 47% of revenue in 2025. Their ease of installation, flexibility, and cost-effectiveness make them ideal for both professional applications and DIY home improvement projects. They are widely employed in furniture refurbishments, cabinetry wrapping, wall paneling, and temporary design solutions for rental properties, offices, and retail spaces.

For instance, self-adhesive PVC films are extensively used in the refurbishment of office furniture in large corporate campuses, where rapid installation with minimal downtime is required. Rental apartment refurbishments in Europe and North America use these films for quick, non-permanent upgrades. Low-VOC adhesives boost eco-compliance, while easy-apply formats speed up projects, reinforcing their dominance in the segment.

Metalized, holographic, and digitally printable films are emerging as the fastest-growing product sub-segment. Their capability to replicate intricate patterns, metallic textures, and custom designs positions them strongly in luxury and bespoke furniture applications. Examples include digitally printed foils for decorative wardrobes, high-end kitchen fronts, and hotel lobby paneling, where design complexity and premium finishes are critical.

These films are also expanding into cross-sector applications, such as lighting fixture overlays, consumer electronics casing, and automotive interior accents. By combining aesthetic sophistication with functional properties such as scratch resistance and UV stability, metalized and digitally printable foils enable furniture and interior designers to meet evolving consumer expectations. Their versatility and high customization potential are driving above-average growth rates across Europe, North America, and Asia Pacific.

Application Insights

Doors and windows represent the largest application segment by value, accounting for a market share of 55% in 2025. Decorative films and foils are extensively used for door skins, window frames, partitions, and laminated surfaces, offering both aesthetic enhancement and protective properties.

They allow for easy replication of premium finishes such as walnut, oak, or marble without incurring the cost of solid wood or natural stone. Major commercial and residential projects in the U.S. and Germany use PVC and polyester foils for durable, cost-effective surfaces. UV resistance, scratch protection, and fire retardancy are key, while transfer foils add texture and boost perceived quality in doors and windows.

Furniture applications represent the fastest-growing segment, driven by urbanization, modular furniture adoption, and frequent replacement cycles. Decorative foils are increasingly used in wardrobes, cabinets, tables, and shelving units to provide high-quality finishes at lower costs than traditional veneers.

DIY-friendly films have accelerated growth in this segment, with consumers and small-scale furniture manufacturers preferring peel-and-stick and heat-transfer applications for rapid design updates. European retailers such as IKEA and Conforama use decorative foils in flat-pack cabinets, while North American brands adopt digitally printed foils in modern furniture. Rising demand for customizable, lightweight, and low-maintenance pieces is set to drive strong growth in this segment.

Regional Insights

North America Furniture Films and Foils Market Trends - Sustainability and Customization Drive Renovation Demand

North America represents a mature but stable market for furniture films and foils, driven by high renovation expenditure and a well-established furniture manufacturing and interior design sector. The U.S. accounts for nearly 70% of the regional demand. Environmental regulations, including stringent VOC emission standards and sustainability mandates, have accelerated the adoption of low-VOC, recyclable, and carbon-neutral decorative films.

Leading suppliers, such as 3M and Avery Dennison, have introduced eco-friendly product lines, including self-adhesive films with post-consumer recycled content and low-emission adhesives, reinforcing their leadership in sustainable solutions.

Renovation activity in hospitality, commercial offices, and high-end residential projects continues to drive repeat sales, particularly for self-adhesive and digitally printable films. The competitive landscape is moderately consolidated, combining international producers and specialized domestic converters.

Recent developments include 3M’s launch of its DI-NOC Carbon Neutral Series in early 2025, targeting architectural surfaces with zero net carbon footprint, and Avery Dennison’s expansion of its self-adhesive decorative film portfolio for the office renovation market, reflecting increasing investment in digital printing technology, design libraries, and customization capabilities.

Europe Furniture Films and Foils Market Trends-Regulation-Led Shift to Eco-Friendly and Premium Finishes

Europe remains a design-centric and regulation-driven market, with Germany, the U.K., France, and Spain leading demand for decorative films and foils. Germany holds a strong position in specialty foils and engineered coatings for premium furniture, automotive interiors, and high-performance laminated surfaces.

European sustainability initiatives, such as the Circular Economy Action Plan and strict REACH compliance regulations, are reshaping product development. Manufacturers are increasingly focusing on halogen-free and fully recyclable laminates, aligning with environmental policies and consumer preference for sustainable furniture.

High disposable income levels and robust renovation incentives sustain steady demand in Western Europe. Collaborations between decorative film producers and furniture OEMs are expanding, focusing on recyclable transfer foils and digitally printed finishes for customized furniture.

Notable recent developments include Leonhard KURZ’s inauguration of its Sustainability Innovation Hub in Germany in 2025, aimed at advancing recyclable transfer foil technologies, and RENOLIT SE’s launch of eco-conscious PVC-free foils for kitchen and office furniture, highlighting the region’s dual emphasis on innovation and sustainability.

Asia Pacific Furniture Films and Foils Market Trends-Scalable Growth Backed by Manufacturing and E-Commerce

Asia Pacific is the largest and fastest-growing regional market, accounting for nearly 45.2% of global decorative film and foil consumption. China dominates production and exports, benefiting from a robust domestic furniture sector, cost-efficient manufacturing infrastructure, and strong government support for industrial modernization.

India is emerging as a key growth market, fueled by rising middle-class incomes, urban housing expansion, and increased investment in modular furniture. Japan and South Korea contribute high-value specialty films and advanced coating technologies, supporting premium and technical applications in commercial and residential furniture.

The region combines favorable raw material availability with a competitive labor cost advantage, enabling rapid scaling of production. Recent developments include Cosmo Films’ 2024 launch of PVC-free decorative films in India, targeting modular furniture applications, and LG Hausys’ 2025 expansion of its production capacity in South Korea to meet growing export demand.

The rising popularity of e-commerce furniture sales and the increasing adoption of digitally printed and customizable films are further propelling growth. Continued investment in sustainable, high-performance decorative lines positions Asia Pacific as a hub for innovation and market expansion through 2032.

Competitive Landscape

The global furniture films and foils market is moderately fragmented, characterized by a mix of multinational corporations and regional converters. Leading players such as 3M, Avery Dennison, LG Hausys, Leonhard KURZ, and Covestro collectively hold a significant market share through technological expertise, strong branding, and distribution networks. Smaller manufacturers compete on cost efficiency and local design customization. Upstream material supply, particularly for coatings and specialty polymers, remains more concentrated than the downstream converting segment.

Key strategic themes include product innovation through sustainable substrates, adoption of digital print technologies, and geographic expansion in high-growth emerging markets. Market leaders differentiate through brand partnerships, design customization, and R&D in functional coatings. Mid-tier converters focus on quick turnaround, local market responsiveness, and value-added surface design services.

Key Industry Developments

- In June 2025, Covestro signed an agreement to acquire Pontacol, a Swiss multilayer adhesive-film specialist, enhancing its specialty films product portfolio to support its “Sustainable Future” growth strategy.

- In April 2025, 3M unveiled the next-generation Crystalline and Color Stable series at FESPA 2025, along with a new Protection Wrap Film, positioning its film lineup toward high-performance and protective decorative surfaces.

Companies Covered in Furniture Films and Foils Market

- 3M Company

- Avery Dennison Corporation

- LG Hausys

- Leonhard KURZ

- Cosmo Films Ltd.

- RENOLIT SE

- Toray Industries, Inc.

- Mitsubishi Chemical Corporation

- Jindal Poly Films Ltd.

- Eastman Chemical Company

- Polyplex Corporation Ltd.

- OMNOVA Solutions

- Foleinwerk Wolfen GmbH

- Skai / Continental AG

- Berry Global, Inc.

- Huhtamaki PPL Ltd.

- Covestro AG

- Flex Films Ltd.

- Indorama Ventures Public Company Limited

- Sun Chemical Corporation

Frequently Asked Questions

The furniture films and foils market size was US$9.2 Billion in 2025.

The furniture films and foils market is projected to reach US$13.6 Billion by 2032, growing at a CAGR of 5.8% from 2025 to 2032.

Key trends include rising adoption of eco-friendly, PVC-free, and recyclable films and increasing use of digitally printable and metalized foils for luxury and custom furniture applications.

By product type, self-adhesive films hold approximately 47% of the market share in 2025. By application, doors and windows hold approximately 55% of the market share in 2025

The furniture films and foils market is expected to grow at a CAGR of 5.8% between 2025 and 2032.

Major players include 3M Company, Avery Dennison Corporation, LG Hausys, Leonhard KURZ, and Cosmo Films Ltd.