- Industrial Goods & Service

- Expansion Joints Market

Expansion Joints Market Size, Share, and Growth Forecast, 2026 - 2033

Expansion Joints Market by Material Type (Metallic (Single, Hinged, Gimbal, Universal, Pressure-Balanced, Toroida), Fabric (Standard, Multi-Layer), Rubber (Spool-Type, Arch-Type), Equipment Type (Axial, Lateral, Angular, Universal / Multi-Directional, Pressure Balanced), Application (Power & Energy, Oil & Gas, Chemical & Petrochemical, Water & Wastewater, HVAC & Building Services, Pulp & Paper / Steel & Metals), and Regional Analysis for 2026 - 2033

Expansion Joints Market Size and Trends Analysis

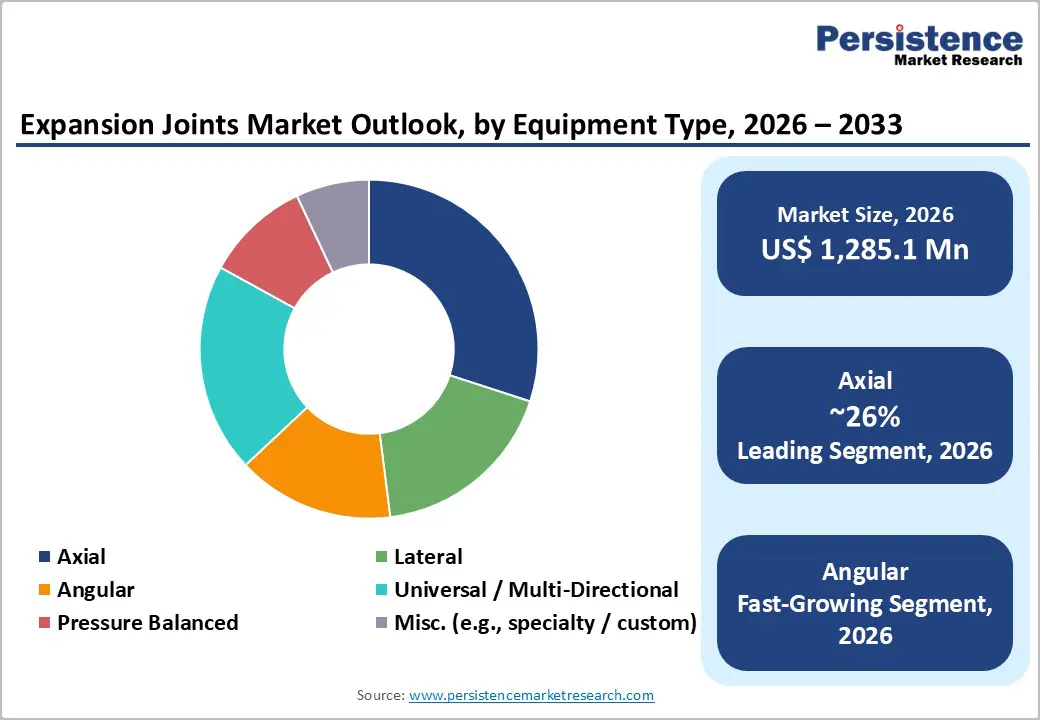

The global expansion joints market size is likely to be valued at US$ 1,285.1 Million in 2026 and is projected to reach US$ 1,695.1 Million by 2033, growing at a CAGR of 4.0% between 2026 and 2033.

The market's steady compounding is driven by sustained global energy infrastructure investment across oil, gas, and power generation sectors; mandatory regulatory requirements for pressure equipment and pipeline safety in advanced economies; and the accelerating shift toward low-carbon energy infrastructure, including district heating, nuclear, and liquefied natural gas facilities that demand high-performance thermal expansion management solutions. According to the International Energy Agency (IEA), global energy demand grew by 2.2% in 2024, with electricity demand surging 4.3%, outpacing global GDP growth of 3.2%, reinforcing capital investment across all energy infrastructure sub-sectors that are primary end-use markets for the Expansion Joints Market.

Key Industry Highlights:

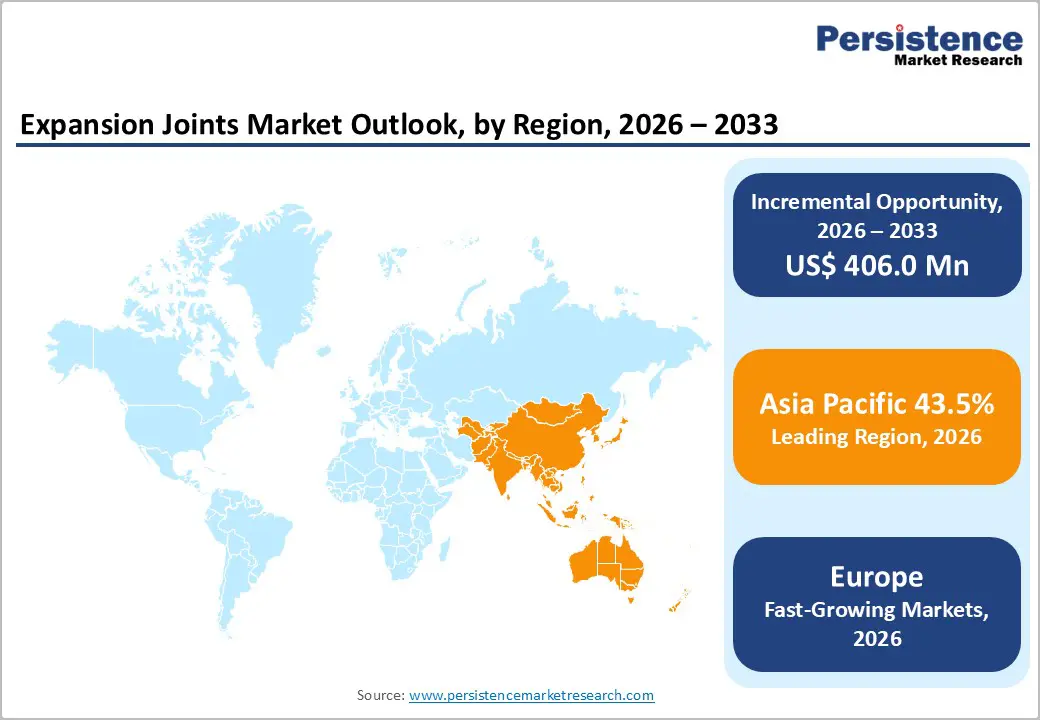

- Dominance of East Asia: East Asia leads the Expansion Joints Market with approximately 30% share, supported by rapid industrialization, large-scale energy infrastructure projects, and extensive pipeline, district heating, and renewable energy installations across China, Japan, and South Korea.

- Leading Equipment: Axial expansion joints account for nearly 30% of total market share, driven by their fundamental role in managing thermal expansion and vibration across power plants, oil refineries, chemical processing, and water transmission pipelines

- Leading Material: Metallic joints hold around 55% share, remaining the backbone of high-pressure, high-temperature industrial systems due to superior thermal, chemical, and mechanical endurance.

- Fastest-Growing Equipment: Angular expansion joints represent the fastest-growing segment, propelled by complex pipeline geometries, seismic zone infrastructure, LNG, nuclear, and hydrogen pipelines requiring rotational movement accommodation.

- Regional Leadership:North America captures roughly 22% market share, strengthened by infrastructure modernization, renewable energy storage buildouts, and strict pipeline, fire-safety, and industrial compliance regulations in the U.S. and Canada.

| Key Insights | Details |

|---|---|

| Expansion Joints Market Size (2026E) | US$ 1,285.1 Mn |

| Market Value Forecast (2033F) | US$ 1,691.1 Mn |

| Projected Growth (CAGR 2026 to 2033) | 4.0% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Dynamics

Growth Drivers

Global Energy Infrastructure Investment and Pipeline Network Expansion Driving Demand

Expansion joints are indispensable components across energy infrastructure managing thermal expansion, vibration, misalignment, and pressure in high-stakes piping systems across power plants, refineries, LNG terminals, and gas distribution networks.

The IEA's tracking of global clean energy progress confirms that energy infrastructure investment is accelerating across all major economies, with global oil production capacity set to expand substantially and non-OPEC producers including the United States, Brazil, Guyana, Canada, and Argentina contributing 4.6 million barrels per day of net new capacity by 2030. In the oil and gas downstream sector, structural growth in refining capacity is concentrated in Asia, particularly China and India, generating direct procurement demand for metallic and fabric expansion joints in high-temperature, high-pressure pipeline applications.

The Global Expansion Joints Market benefits structurally from this sustained capital expenditure cycle across energy infrastructure, with replacement and new installation demand compounding across the forecast period as operational networks age and new capacity is commissioned globally.

Mandatory Safety Regulations and Pressure Equipment Directives Compelling Product Compliance

Stringent global regulatory frameworks governing pipeline safety, pressure equipment performance, and fire-resistance in industrial and construction applications are a critical structural driver for the Expansion Joints Market. In Europe, the Pressure Equipment Directive (PED 2014/68/EU) and harmonized standard EN 14917 mandate rigorous design, testing, and certification requirements for metallic expansion joints used in pressure-bearing systems, compelling OEM specification of certified, high-performance products.

In the United States, federal pipeline safety regulations administered by the Pipeline and Hazardous Materials Safety Administration (PHMSA) require compliant expansion accommodations across regulated pipelines, while the International Building Code (IBC) governs fire-rated expansion joint performance in commercial and multi-family construction. A landmark example is Balco's achievement of the industry's first UL 2079 listing for its MetaBlock® fire-rated expansion joint barriers for wood-frame floor and wall assemblies, addressing previously unresolved fire-resistance gaps in multi-family construction while maintaining joint movement performance per IBC requirements. These compliance requirements create a sustained and growing non-discretionary replacement and new-installation procurement base across the Expansion Joints Market globally.

Electrification, District Heating, and Decarbonization Infrastructure Creating New Demand Vectors

The global energy transition is creating entirely new applications and procurement streams for expansion joints that go beyond traditional oil and gas markets. District heating networks which are integral to the European Union's decarbonisation strategy under the Renewable Energy Directive (EU/2023/2413) are critical consumers of specialized expansion joints for pre-insulated underground piping systems that manage ground movement and thermal cycling. The global district heating expansion joints segment is estimated to be growing at approximately 7% CAGR through 2033, driven by Northern Europe's well-established networks and rapid build-out across China, South Korea, and Central Europe.

The IEA reports that global renewable energy capacity additions reached a record 700 GW in 2024, 80% of which was solar PV, with nuclear power also adding over 7 GW of new capacity the highest in three decades all of which require expansion joint solutions within plant piping systems. The Expansion Joints Market is therefore capturing structural demand across the full spectrum of decarbonisation infrastructure, from district heating pipelines to nuclear steam systems and geothermal energy plants.

Restraint - Raw Material Price Volatility Compressing Manufacturer Margins

The global expansion joints market is exposed to meaningful margin compression risk from price volatility in primary inputs including stainless steel, carbon steel, specialty alloys, and high-performance elastomers. Metallic expansion joints which represent the dominant product segment are particularly sensitive to steel price cycles, which are influenced by global energy costs, trade tariffs, and geopolitical supply disruptions. Fabrication costs for customized, multi-ply metallic bellows can be substantial, and in commodity-competitive market segments, input cost spikes cannot always be passed through to end customers, squeezing margins for manufacturers without long-term supply agreements or vertical integration.

Long Sales Cycles and Project Dependency Limiting Revenue Predictability

A structural characteristic of the Expansion Joints Market that constrains growth predictability is the deep dependency on large, long-cycle industrial capital expenditure projects including power plants, refineries, chemical facilities, and pipeline infrastructure programs where procurement decisions can shift significantly based on regulatory delays, financing conditions, and macroeconomic cycles. Project cancellations or deferments in energy infrastructure spending, as experienced during the COVID-19 period, can rapidly reduce order intake for expansion joint manufacturers. This cyclicality creates revenue volatility, particularly for suppliers concentrated in single end-use sectors, and limits the ability to sustain consistent capacity utilization across manufacturing facilities during demand downturns.

Opportunity - Decarbonization Infrastructure and Nuclear Renaissance Creating Premium Demand

The accelerating deployment of low-carbon energy infrastructure including nuclear power plants, advanced district heating systems, hydrogen pipelines, and large-scale geothermal facilities represents a strategically high-value growth opportunity for Expansion Joints Market participants capable of supplying certified, application-specific solutions for extreme operating conditions.

The IEA confirmed that nuclear power added over 7 GW of new capacity globally in 2024, a 33% increase over 2023 and the fifth highest in three decades, with construction starts for new nuclear plants increasing by 50% using designs predominantly in China and Russia. Each new nuclear facility requires specialized metallic bellows and expansion joints rated for high radiation environments, extreme temperature cycling, and seismic performance a premium and technically differentiated sub-segment of the Expansion Joints Market.

Daikin's high-temperature VRF system capable of delivering hot water up to 90 degrees Celsius for industrial processes and district heating in Europe similarly illustrates the cascading demand for advanced thermal management components across decarbonization applications, creating well-defined and high-margin addressable market pockets for expansion joint specialists in the 2026 to 2033 forecast window.

Emerging Economy Industrialization and Infrastructure Modernization Opening New Markets

Rapid industrialization in India, Southeast Asia, and Latin America combined with government-led infrastructure modernization programs is creating a multi-decade demand runway for expansion joint products across construction, water and wastewater, power generation, and chemical processing sectors in these geographies.

India's expansion joints market is driven by the government's Make in India initiative, surging foreign direct investment in energy, and India's growing role as a refining hub requiring petrochemical pipeline and process equipment. The IEA reports that India recorded the second-largest absolute rise in global energy demand in 2024, surpassing the combined increase of all advanced economies a macro signal directly translating into long-cycle capital investment in energy infrastructure where expansion joints are an obligatory specification.

In Latin America, clean energy investment reached USD 70 billion in 2025, with Brazil implementing approximately 350 independent power transmission projects totaling 10,500 km of transmission lines in 2024 alone all representing infrastructure deployments that embed demand for industrial expansion joint components. EagleBurgmann's inauguration of a Shared Services Center in Chennai, India to support manufacturing of expansion joints and mechanical seals for Food and Beverage, Oil and Gas, and Chemicals sectors directly validates this emerging market opportunity trajectory for the Expansion Joints Market.

Category-wise Analysis

Equipment Type Insights

Axial expansion joints are the leading equipment type segment, holding approximately 30%% of the Global Expansion Joints Market in 2026. Axial joints accommodate compressive and elongation movements along the pipeline axis the most fundamental and prevalent type of thermal expansion movement in straight pipe runs across virtually all industrial and infrastructure applications, from steam distribution lines to process piping in oil refineries and chemical plants. Their relatively straightforward design, broad applicability across metal types and temperature ranges, and established engineering specification across international piping design codes including ASME, EN 14917, and ISO standards underpin their commanding market position. Axial expansion joints are additionally the primary configuration deployed in district heating networks, water transmission infrastructure, and HVAC piping systems all sectors experiencing sustained procurement demand driven by decarbonization and urban infrastructure investment.

Angular expansion joints are the fastest-growing equipment type segment within the Global Expansion Joints Market. Angular joints are designed to absorb rotational deflection between connected pipe sections a movement accommodation requirement that has become increasingly prevalent in complex pipeline geometries associated with seismic zone infrastructure, offshore platforms, LNG transfer systems, and nuclear plant piping. The IEA projection of nearly 35-fold expansion in grid-scale battery storage capacity between 2022 and 2030 signals large-scale energy infrastructure build-out that incorporates multi-directional and angularly complex piping configurations where angular joints are engineered for structural compliance. Innovative angular and multi-directional joint configurations are also being adopted in next-generation geothermal and hydrogen pipeline projects, positioning this segment for structurally differentiated growth across the forecast period.

Material Type Insights

Metallic expansion joints are the leading material type segment in the Global Expansion Joints Market, commanding an estimated 55% market share in 2026. This dominant positioning reflects metallic expansion joints' unique combination of high-pressure tolerance, superior thermal endurance across cryogenic to ultra-high-temperature operating ranges, chemical resistance, and long service life in demanding industrial applications including power generation steam systems, refinery piping, LNG facilities, and nuclear plant process lines. Metallic types encompassing Single, Hinged, Gimbal, Universal, Pressure-Balanced, and Toroidal configurations are the technically specified solution for the highest-pressure and highest-temperature industrial applications, where rubber and fabric alternatives cannot meet design code requirements. The top three companies in the metallic expansion joints sub-market collectively account for approximately 24% of market share, with Witzenmann, BOA Group, and Kadant Unaflex among the principal global suppliers.

Fabric expansion joints represent the fastest-growing material type segment within the Global Expansion Joints Market. Their momentum is driven by the global build-out of combined cycle gas turbines, biomass power plants, industrial furnaces, and waste-to-energy facilities all of which require flexible, high-temperature gas duct connectors where fabric bellows offer superior thermal insulation performance, vibration absorption, and acoustic damping compared to metallic alternatives. Fabric joints are increasingly specified in applications demanding low angular stiffness, large lateral movement accommodation, and chemical resistance in flue gas desulfurization systems. Their cost-competitive positioning relative to engineered metallic assemblies is additionally expanding their addressable market in process industries across Asia Pacific and Latin America as industrialization deepens.

Regional Insights and Trends

East Asia Expansion Joint Market Trends

East Asia commands approximately 30% of the global expansion joints market the largest regional share driven by China's position as the world's largest energy consumer and infrastructure investor, combined with Japan's and South Korea's advanced industrial manufacturing and LNG procurement bases. China alone contributed over half of global electricity demand growth in 2024, according to the IEA, with renewables reaching nearly 20% of total generation and new renewable capacity additions driving large-scale power plant and grid infrastructure procurement that embeds expansion joint demand across turbine, condenser, and piping systems.

China's government has announced plans to install over 30 GW of energy storage by 2025, and cumulative user-side energy storage installations for the first eleven months of 2025 reached 39.5 GW a 28% increase compared to the same period in 2024 with commercial and industrial applications dominating nearly 90% of installations, all of which require compliant piping systems with certified expansion joint assemblies.

In Japan and South Korea, multi-billion-dollar LNG fleet investments and infrastructure expansions are sustaining industrial demand for high-performance metallic expansion joints in gas receiving terminals, regasification plants, and distribution networks. South Korea's long-term energy plans envision LNG imports decreasing by 20% through the mid-2030s as renewables and nuclear scale up, but near-term infrastructure build-out continues to sustain procurement of industrial process components including expansion joints.

North America Expansion Joint Market Trends

North America accounts for approximately 22% of the global expansion joints market, with the United States as the dominant country market underpinned by the world's most extensive pipeline network, significant refinery infrastructure, and multi-trillion-dollar federal investment in infrastructure modernization. The U.S. Bipartisan Infrastructure Law has allocated substantial capital for bridge rehabilitation and transportation infrastructure directly driving demand for construction-grade expansion joints, with the U.S. bridge expansion joints market projected to grow at a CAGR of 6% from 2025 to 2035.

The North American Building Expansion Joints Market is, driven by urbanization, infrastructure maintenance, and stringent seismic and fire safety standards. U.S. energy storage capacity surpassed 40 GW operationally and is projected to reach 98 GW by 2030, with utility-scale projects in Texas, California, and Arizona each adding over 1 GW in Q2 2025 alone energy infrastructure deployments that require industrial-grade expansion joints across power plant and grid-connected facility piping systems. The North America Industrial Expansion Joint Market, reflecting the broad-based nature of U.S. industrial procurement across oil and gas operations, advanced manufacturing, and renewable energy installations.

Europe Expansion Joint Market Trends

Europe accounts for approximately 18.5% of the global expansion joints market, with the region's profile differentiated by its strong regulatory environment, deep district heating infrastructure, and accelerating industrial decarbonization. The EU's Renewable Energy Directive (EU/2023/2413) mandating renewable heating and cooling targets directly drives district heating network expansion across Germany, Denmark, the Netherlands, Poland, and the Nordic markets all of which require high-performance expansion joints for pre-insulated district heating pipelines operating at elevated temperatures and pressures. The district heating expansion joints segment globally is estimated at USD 500 million in 2025 and is projected to grow at a CAGR of 7% through 2033, with Northern Europe including Scandinavian countries and Germany leading demand alongside East Asia.

Competitive Landscape

The global Expansion Joints market is moderately consolidated, dominated by a few major players while also featuring numerous regional and specialized manufacturers. Leading companies such as EagleBurgmann, Witzenmann Group, Indutrade AB (Belman), CSW Industrials (Balco), and Belman A/S hold significant market share, leveraging their extensive product portfolios, technological expertise, and global distribution networks. These players focus on metallic and non-metallic expansion joints, pressure-balanced systems, and fire-resistive solutions, serving industries like power generation, oil & gas, HVAC, and petrochemicals.

Regional manufacturers contribute to the fragmented aspect of the market, catering to niche, customized, and low-volume projects. Strategic acquisitions and capacity expansions, such as Indutrade’s acquisition of Belman and Witzenmann’s plant growth, are driving further consolidation and strengthening regional footprints. Competition is largely based on product quality, certifications, engineering support, and compliance with industry standards.

Key Industry Developments:

- In February 2026: Indutrade AB (publ) completed the acquisition of Belman A/S, a Danish manufacturer of customized metallic and non-metallic expansion joints and bellows for industries including marine, process, and power generation, expanding Indutrade’s Process, Energy & Water business area and strengthening its global footprint with production sites in Denmark and India.

- In February 2026, Balco, a subsidiary of CSW Industrials, Inc., achieved an industry first by obtaining UL 2079 listing for its MetaBlock® fire-rated expansion joint barriers specifically for wood-frame floor and wall assemblies, addressing fire-resistance gaps in multi-family and mixed-use wood-frame construction while maintaining joint movement and meeting International Building Code (IBC) requirements.

Companies Covered in Expansion Joints Market

- Trelleborg AB

- EagleBurgmann

- Witzenmann

- Weldmac

- Unaflex

- BOA Group

- Flexider

- Senior Flexonics Pathway

- Macoga

- Tofle

- S. Bellows

- Technoflex

Frequently Asked Questions

The global Expansion Joints Market is projected to be valued at US$ 1,285.1 Mn in 2026.

The Metallic Expansion Joints segment is expected to account for approximately 55% of the Global Expansion Joints Market by Material Type in 2026.

The market is expected to witness a CAGR of 4.0% from 2026 to 2033.

Global Expansion Joints Market growth is driven by rising energy infrastructure investment, pipeline network expansion, stringent safety and compliance regulations, and new demand from electrification, district heating, and decarbonization projects.

Key market opportunities in the global Expansion Joints Market lie in decarbonization infrastructure, nuclear power expansion, hydrogen and geothermal pipelines, and industrialization-driven infrastructure growth in emerging economies like India, Southeast Asia, and Latin America.

Key players in the Expansion Joints Market include EagleBurgmann, Witzenmann Group, Indutrade AB (Belman), CSW Industrials (Balco), and Belman A/S.