- Smart Packaging

- EVOH for Packaging Market

EVOH for Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

EVOH for Packaging Market by End-use Industry (Food & Beverages, Pharmaceuticals, Others), Applications (Films & Wraps, Pouches & Bags, Others), Product Types (Cast Films, Blown Films, Others), Thickness Levels, and Regional Analysis for 2026 - 2033

EVOH for Packaging Market Size and Trends Analysis

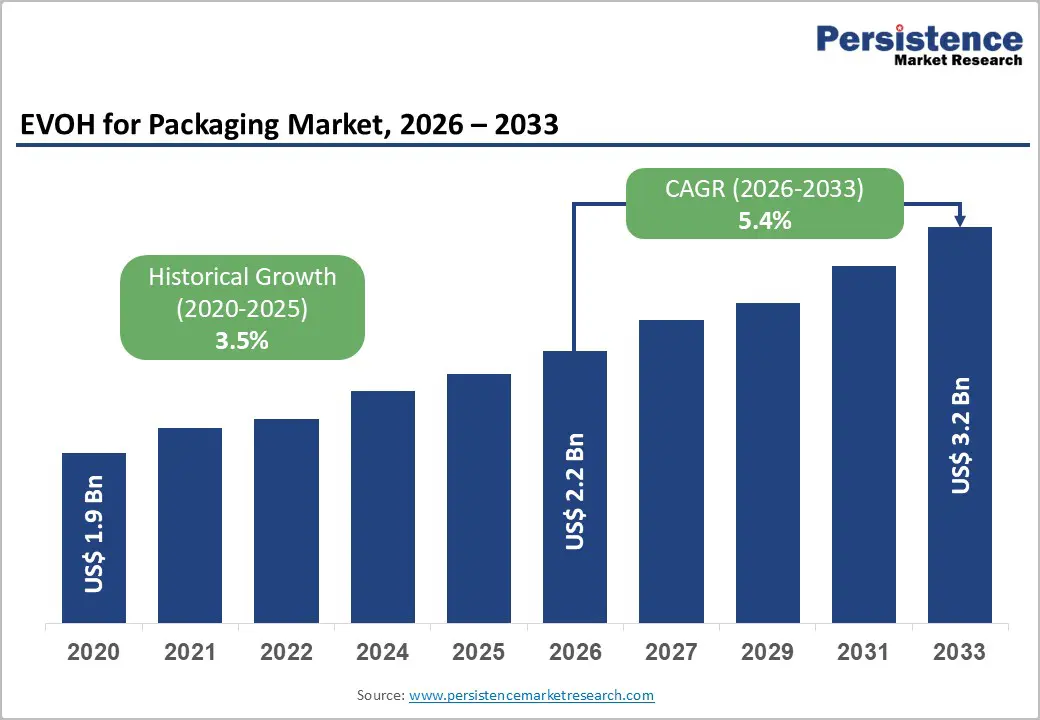

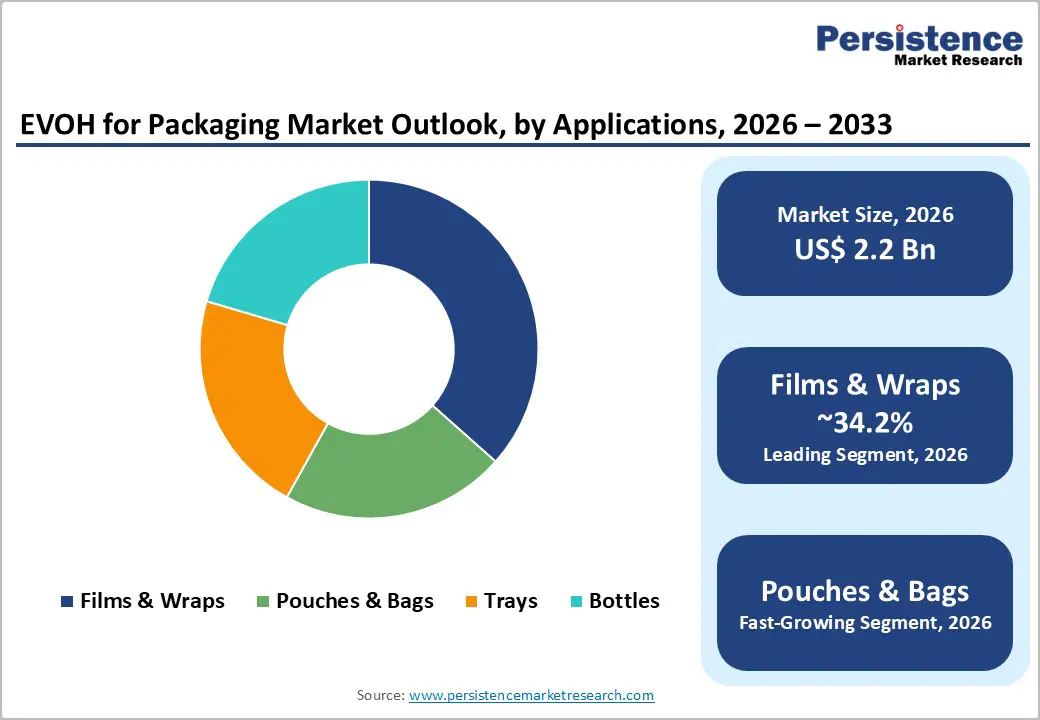

The global EVOH for packaging market size is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$3.2 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033, driven by increasing demand for extended food shelf life, regulatory pressure to replace chlorine-containing barrier materials such as PVDC, and the shift toward recyclable multilayer flexible packaging structures. EVOH enables strong oxygen-barrier performance at minimal thickness, supporting both sustainability and product-protection goals.

Key Industry Highlights:

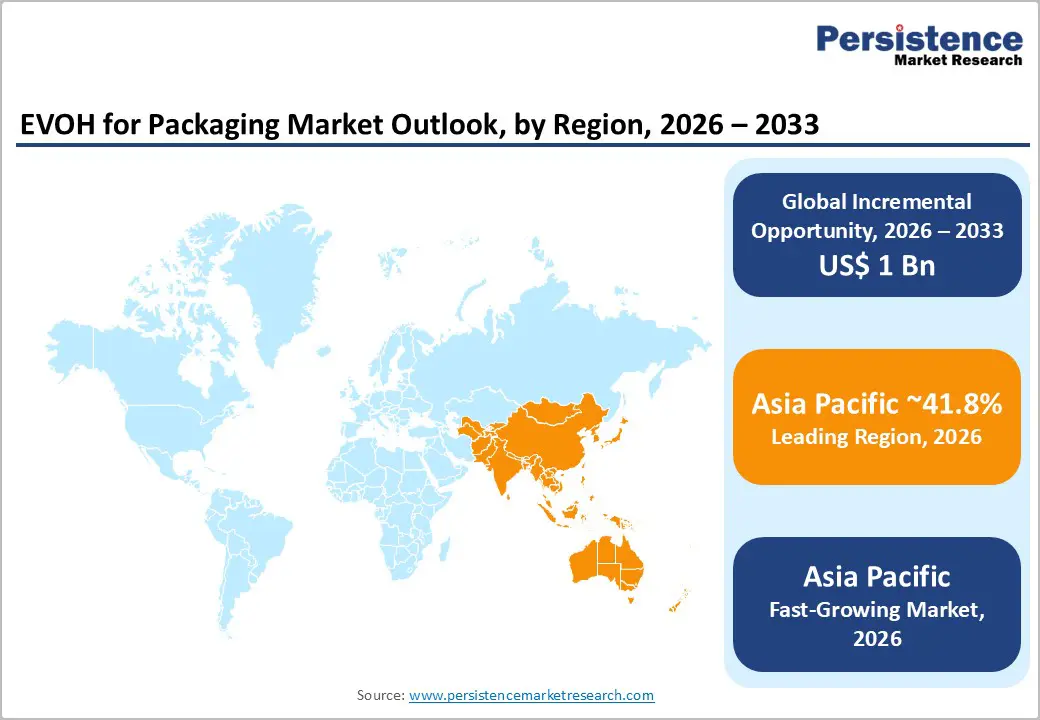

- Leading Region: Asia Pacific is projected to account for approximately 41.8% of market share, supported by strong food-processing capacity in China, advanced barrier technology adoption in Japan, and expanding packaged food demand across India and ASEAN.

- Fastest-growing Region: Asia Pacific projected to record the highest growth rate during the forecast period, driven by retail modernization, cold-chain expansion, and rising flexible packaging penetration.

- Investment Plans: Converters across North America, Europe, and Asia Pacific are expanding multilayer co-extrusion and recyclable PE-based film capacity, with capital allocation focused on downgauged EVOH barrier layers compatible with recyclability certification frameworks (e.g., APR, RecyClass).

- Dominant End-use Industries: Food & beverages is anticipated to account for 51.9% market share, led by meat overwrap, dairy packaging, retort pouches, and MAP applications that require high oxygen-barrier performance.

- Leading Applications: Films & wraps are expected to hold 34.2% of market share, maintaining leadership due to strong adoption in chilled food packaging, private-label retail growth, and extended distribution supply chains.

| Key Insights | Details |

|---|---|

| EVOH for Packaging Market Size (2026E) | US$2.2 Bn |

| Market Value Forecast (2033F) | US$3.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 3.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory and Sustainability Substitution Pressure

Global packaging regulations are tightening recyclability and material composition requirements. The European Union’s Packaging and Packaging Waste Regulation (PPWR) mandates higher recyclability thresholds and discourages chlorine-based barrier materials such as PVDC. EVOH serves as a functional substitute, enabling PE-dominant multilayer films that can meet design-for-recycling criteria when appropriately engineered. In the United States, food-contact compliance under 21 CFR provides a stable regulatory pathway for EVOH use in direct-contact applications. Regulatory clarity reduces compliance risk and accelerates adoption among brand owners seeking validated barrier materials. Regulatory-driven substitution is accelerating specification changes in Europe and influencing multinational food companies globally. This shift creates measurable volume growth in recyclable multilayer films incorporating EVOH.

Food Waste Reduction and Fresh-Food Retail Economics

Retail modernization, cold-chain expansion, and e-grocery growth are increasing demand for high-barrier packaging that extends shelf life and reduces spoilage. EVOH provides superior oxygen-barrier properties compared with standard polyolefins, enabling thinner multilayer structures while maintaining product freshness. In chilled meats, dairy, ready meals, and modified atmosphere packaging (MAP), EVOH layers significantly reduce oxygen transmission rates. Even as overall packaging weight declines due to lightweighting, EVOH loading per unit in high-value food segments continues to increase. Reduced shrinkage, fewer product returns, and extended distribution windows translate into quantifiable economic benefits for retailers and processors, supporting steady resin demand growth.

Capacity Expansion and Sustainable Grade Development

Major resin manufacturers have invested in expanding EVOH production capacity and launching sustainability-certified grades, including bio-based and mass-balance-certified variants. These initiatives improve supply reliability and align with FMCG sustainability targets. Expanded capacity reduces historical supply tightness, stabilizes pricing, and increases penetration in cost-sensitive markets. Sustainability certifications also support procurement requirements among global food brands seeking lower-carbon packaging inputs. Improved availability and sustainable product positioning underpin the projected 5.4% CAGR, particularly in Asia Pacific, where manufacturing integration strengthens regional supply chains.

Barrier Analysis - Cost Premium versus Commodity Polymers

EVOH carries a price premium compared with polyethylene (PE), polypropylene (PP), and some metallized or coated barrier alternatives. In applications where shelf-life extension does not generate sufficient economic return, converters may favor lower-cost materials. In certain flexible packaging formats, EVOH incorporation can increase total film cost by an estimated 5-12%, depending on thickness and structure complexity. In emerging markets with heightened price sensitivity, this premium can limit adoption unless regulatory or performance requirements mandate higher barrier performance.

Multilayer Recycling Infrastructure Limitations

While EVOH enables recyclable PE-dominant constructions, actual recyclability depends on local collection and processing infrastructure. Regions with limited store-drop or curbside multilayer film recycling face slower conversion rates. Certification frameworks such as How2Recycle (U.S.) and RecyClass (Europe) require compliance with defined EVOH content thresholds. Markets lacking mature recycling systems may delay adoption despite technical feasibility.

Opportunity Analysis - Thin-Gauge Flexible Packaging (Up to 18 Microns)

Advances in co-extrusion technology allow precise control of barrier-layer thickness, enabling EVOH usage in ultra-thin segments (up to 18 microns). These thinner structures reduce total material usage while maintaining performance. This creates opportunities in snack packaging, liquid pouches, and convenience foods where sustainability and cost optimization are critical purchasing criteria. Converters investing in multilayer extrusion lines with advanced dosing systems can capture premium growth.

Premium Pharmaceutical and Aseptic Applications

Biologics, nutraceuticals, and sensitive active pharmaceutical ingredients require packaging with superior oxygen and aroma barriers. EVOH-based multilayer laminates meet these requirements in blister packs, strip packaging, and sterile pouches. Pharmaceutical packaging commands higher margins, and regulatory validation strengthens supplier relationships. Converters developing validated regulatory documentation and traceable supply chains can access this high-growth niche.

Emerging Market Food Processing Expansion

Rapid urbanization in India, Southeast Asia, and parts of Latin America is expanding packaged food consumption. Cold-chain investments and retail modernization create demand for extended shelf-life packaging solutions. Localizing EVOH supply chains and providing technical support to regional converters represent actionable growth pathways.

Category-wise Analysis

End-use Industry Insights

The food & beverages segment is anticipated to account for over 51.9% of the market share over the forecast period. Applications span fresh and processed meat overwrap, ready-to-eat meals, dairy packaging, retort pouches, coffee packs, condiments, and modified atmosphere packaging (MAP). EVOH is typically incorporated as a thin internal barrier layer within multilayer PE, PP, or PET structures to significantly reduce oxygen transmission rates (OTR). For example, vacuum skin packaging for fresh meat and thermoformed trays for sliced cheese commonly use EVOH-based barrier layers to extend refrigerated shelf life while preserving color and flavor integrity. In retort applications such as ready meals and soups, EVOH enhances oxygen resistance in combination with high-temperature-resistant polymers. Its ability to enable downgauging while maintaining barrier performance supports brand owners’ lightweighting and sustainability goals. Retailers benefit from reduced spoilage, longer distribution cycles, and improved inventory turnover across organized retail and e-commerce grocery channels. Resin producers and converters should prioritize long-term supply agreements with major food processors and global packaged food brands, while investing in high-speed form-fill-seal (FFS), thermoforming, and retort-compatible multilayer extrusion capabilities to strengthen competitive positioning.

Pharmaceutical packaging is projected to be the fastest-growing end-use segment, driven by increasing demand for oxygen-sensitive drug formulations and biologics. Stricter regulatory requirements related to drug stability, coupled with global expansion of generics and specialty pharmaceuticals, are accelerating the adoption of high-barrier packaging materials. EVOH is widely used in multilayer laminates for blister lidding films, sachets, stick packs, and sterile packaging systems where oxygen and moisture protection are critical. For instance, oral solid dosage packaging often integrates EVOH layers within cold-form or thermoform blister structures to enhance barrier integrity without significantly increasing material thickness. In parenteral and diagnostic packaging formats, EVOH supports extended shelf stability for sensitive formulations. Although total packaging volumes remain lower than food applications, higher regulatory standards and premium-grade material requirements increase the per-unit resin value, strengthening revenue contribution. Suppliers should invest in pharmaceutical-grade production lines, regulatory compliance documentation (e.g., DMF support), traceability systems, and long-term validation partnerships with contract manufacturing organizations (CMOs) to capture high-margin growth opportunities.

Applications Insights

Films & wraps are anticipated to account for approximately 34.2% of market share in 2026. This segment includes cast and blown co-extruded films used in meat packaging, chilled and frozen food wraps, cheese films, and MAP systems. Multilayer film structures typically combine EVOH with polyethylene tie layers and sealant resins to balance barrier performance with flexibility and machinability. Retail-ready meat trays with stretch films incorporating EVOH barriers exemplify widespread adoption, particularly in organized retail chains and export-oriented supply chains. The growth of private-label food brands and cross-border food distribution has reinforced demand for packaging that preserves freshness across longer logistics cycles. EVOH-based films also support downgauging strategies, reducing total material consumption while maintaining shelf-life performance. Continuous investment in multilayer cast-film and blown-film extrusion technologies, along with barrier optimization expertise, remains essential for converters aiming to secure long-term supply contracts with large food processors.

Flexible pouches and bags represent the fastest-growing application segment, fueled by the shift toward lightweight, convenience-oriented packaging formats. Stand-up pouches (SUPs), spouted pouches for baby food and beverages, and retort pouches for ready-to-eat meals increasingly incorporate EVOH layers to provide superior oxygen and aroma barrier properties. For example, dairy beverages, sauces, and ready-to-drink nutritional products rely on EVOH to maintain flavor stability and prevent oxidative degradation. Re-closable zipper pouches and premium stand-up formats typically contain higher barrier-layer content per unit compared to traditional rigid containers, increasing resin consumption intensity. The transition from rigid containers (glass or metal) to flexible laminated structures further amplifies EVOH demand due to its ability to combine high barrier performance with material efficiency. Converters expanding pouch-making capacity, lamination capabilities, and high-barrier adhesive technologies will be positioned to capture disproportionate growth as brands continue migrating toward flexible, sustainability-aligned packaging formats.

Regional Insights

North America EVOH for Packaging Market Trends - Recycle-Ready PE Multilayers and Cold-Chain Protein Demand

North America represents a substantial share of global EVOH packaging demand, with the United States accounting for the majority of regional consumption. The region benefits from highly developed cold-chain infrastructure, widespread penetration of modified atmosphere packaging (MAP), and strong per-capita consumption of packaged meat, dairy, and ready-to-eat foods. Major packaged food producers such as Tyson Foods and Hormel Foods rely on high-barrier multilayer films incorporating EVOH to extend refrigerated shelf life and reduce retail shrinkage in protein categories.

A key structural shift in the region involves the transition toward recyclable, polyethylene (PE)-dominant multilayer films. Resin producers such as Kuraray Co., Ltd. and Nippon Gohsei (Soarnol™ EVOH) have expanded technical support for downgauged barrier films compatible with PE recycling streams. Meanwhile, packaging leaders such as Amcor plc and Sealed Air have introduced recycle-ready flexible packaging platforms in North America, incorporating EVOH in carefully controlled thin layers to meet recyclability guidelines established by organizations such as the Association of Plastic Recyclers (APR). These developments directly influence EVOH formulation strategies, as converters balance barrier performance with recyclability thresholds.

Pharmaceutical packaging is another growth pillar. Companies, including West Pharmaceutical Services and Berry Global, have expanded high-barrier healthcare packaging capabilities to serve biologics and specialty drug manufacturers. EVOH-based multilayer structures are increasingly used in sterile packaging, diagnostic kits, and oral solid-dose laminates. The regulatory environment remains stable, with the U.S. Food and Drug Administration (FDA) food-contact approvals providing long-term compliance certainty for resin producers and converters.

Europe EVOH for Packaging Market Trends - PPWR-Driven Recyclability Innovation and Retail-Led Material Optimization

Europe remains a technologically advanced and regulation-driven EVOH packaging market, characterized by strong environmental governance and rapid adoption of recyclable packaging frameworks. Germany leads regional consumption due to its large processed meat and dairy sectors, followed by the U.K., France, and Spain. Multilayer thermoforming and tray-sealing systems are widely deployed across European supermarket chains, reinforcing demand for high-performance oxygen barriers. The European Union’s Packaging and Packaging Waste Regulation (PPWR) is a transformative force reshaping material selection. The policy framework encourages recyclable multilayer structures and discourages materials that hinder mechanical recycling. This shift has accelerated innovation among packaging leaders such as Mondi Group and Coveris, both of which have introduced mono-material PE or PP-based flexible packaging incorporating optimized EVOH barrier layers. For instance, mono-PE high-barrier pouches developed for meat and cheese applications are designed to meet recyclability certification standards under initiatives such as RecyClass.

Retailers also play a decisive role. European supermarket groups such as Lidl and Tesco have publicly committed to improving packaging recyclability and reducing food waste. Their sustainability pledges encourage brand owners to adopt thinner EVOH layers within recyclable film matrices, driving resin innovation focused on compatibility and minimal contamination thresholds. Converters across Germany and the Netherlands are investing heavily in R&D to refine co-extrusion formulations that satisfy recyclability criteria without compromising oxygen transmission performance.

Asia Pacific EVOH for Packaging Market Trends - Food Processing Expansion and Thin-Gauge Co-Extrusion Leadership

Asia Pacific leads the market with approximately 41.8% share in 2026 and remains the fastest-growing regional market. Growth is anchored by expanding food-processing industries, rapid urbanization, and rising demand for packaged convenience foods. China represents the largest single-country market, supported by the modernization of supermarket chains and strong domestic ready-meal production. Retail expansion by companies such as Sun Art Retail Group has reinforced demand for extended-shelf-life packaging in fresh and chilled food categories. Japan maintains technological leadership, supported by domestic resin production from firms including Kuraray Co., Ltd., a key global EVOH supplier. Japanese converters pioneered thin-gauge multilayer co-extrusion technologies widely adopted across Asia, particularly in retort pouches and high-barrier films for seafood and prepared meals. The country’s mature convenience store culture, led by chains such as 7-Eleven Japan, sustains consistent demand for high-performance barrier packaging.

India and ASEAN countries are experiencing accelerated growth due to expanding cold-chain infrastructure and increasing packaged food penetration. Companies such as UFlex Ltd. have invested in advanced multilayer film production lines to cater to domestic and export markets. Rising e-commerce grocery adoption across urban India and Southeast Asia further increases the need for packaging that protects product integrity across longer logistics cycles. Multinational brands operating in the region are also aligning with global sustainability targets, prompting the adoption of recyclable PE-based barrier films incorporating EVOH in optimized concentrations.

Competitive Landscape

The global EVOH for packaging market is moderately concentrated at the resin manufacturing level, with a limited number of global producers controlling significant capacity. Downstream converting remains fragmented across regional players. Leading producers focus on technological innovation, sustainable-grade development, and supply reliability.

Key strategies include sustainable product development, co-extrusion technology innovation, capacity expansion, and partnerships with converters and retailers. Competitive advantage increasingly depends on recyclability validation and technical service capabilities.

Key Industry Developments

- In May 2025, Pregis announced an expansion of its EVOH barrier film production capacity at its Anderson, South Carolina, facility to support the growing demand for recyclable mono-material packaging structures, reinforcing its sustainable packaging portfolio and ability to supply high-barrier solutions in key North American and global markets.

Companies Covered in EVOH for Packaging Market

- Kuraray Co., Ltd.

- Mitsubishi Chemical Group

- Nippon Gohsei

- Chang Chun Group

- China Petrochemical Corporation (Sinopec)

- SK Geo Centric

- Formosa Plastics Corporation

- Amcor plc

- Sealed Air

- Berry Global

- Mondi Group

- Coveris

- Winpak Ltd.

- Toray Industries, Inc.

- Toppan Holdings Inc.

- UFlex Ltd.

- Cosmo Films Ltd.

- Constantia Flexibles

Frequently Asked Questions

The global EVOH for packaging market is valued at US$2.2 billion in 2026.

The EVOH for packaging market is projected to reach US$3.2 billion by 2033.

Key trends include the shift toward recyclable PE-dominant multilayer structures, downgauging of barrier layers, rising demand for modified atmosphere packaging (MAP), growth in stand-up and retort pouches, and increasing pharmaceutical-grade barrier applications driven by biologics and specialty drugs.

The food & beverages segment leads the market, anticipated to account for over 51.9% share, driven by meat overwrap, dairy packaging, retort pouches, and extended-shelf-life chilled food applications.

The EVOH for packaging market is expected to grow at a CAGR of 5.4% between 2026 and 2033.

Major companies include Kuraray Co., Ltd., Mitsubishi Chemical Group, Nippon Gohsei, Amcor plc, and Sealed Air.