- Automotive Components & Materials

- EV Battery Management System Market

EV Battery Management System Market Size, Share, and Growth Forecast 2026 - 2033

EV Battery Management System Market by Battery Type (Lithium-Ion (Li-Ion), Nickel-Metal Hydride, Others), by Propulsion Type (Battery Electric Vehicle, Hybrid Electric Vehicle), by Topology (Modular BMS, Decentralized BMS, Centralized BMS), by Vehicle Type (Passenger Car, Commercial Vehicles, Others), by Regional Analysis, 2026 - 2033

EV Battery Management System Market Size and Trend Analysis

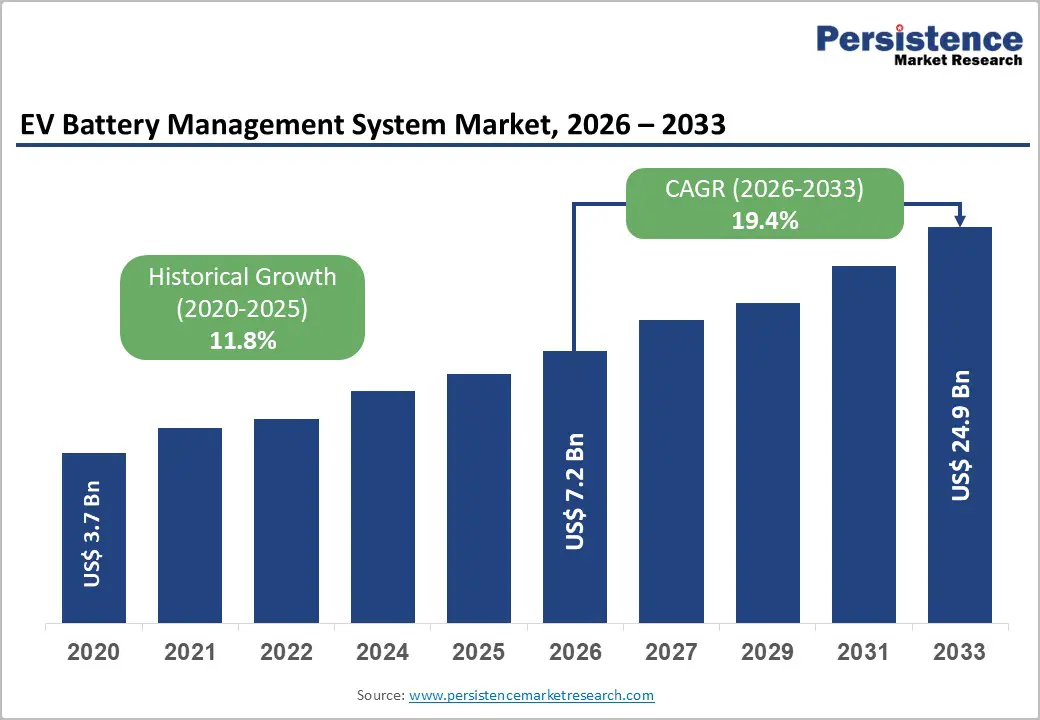

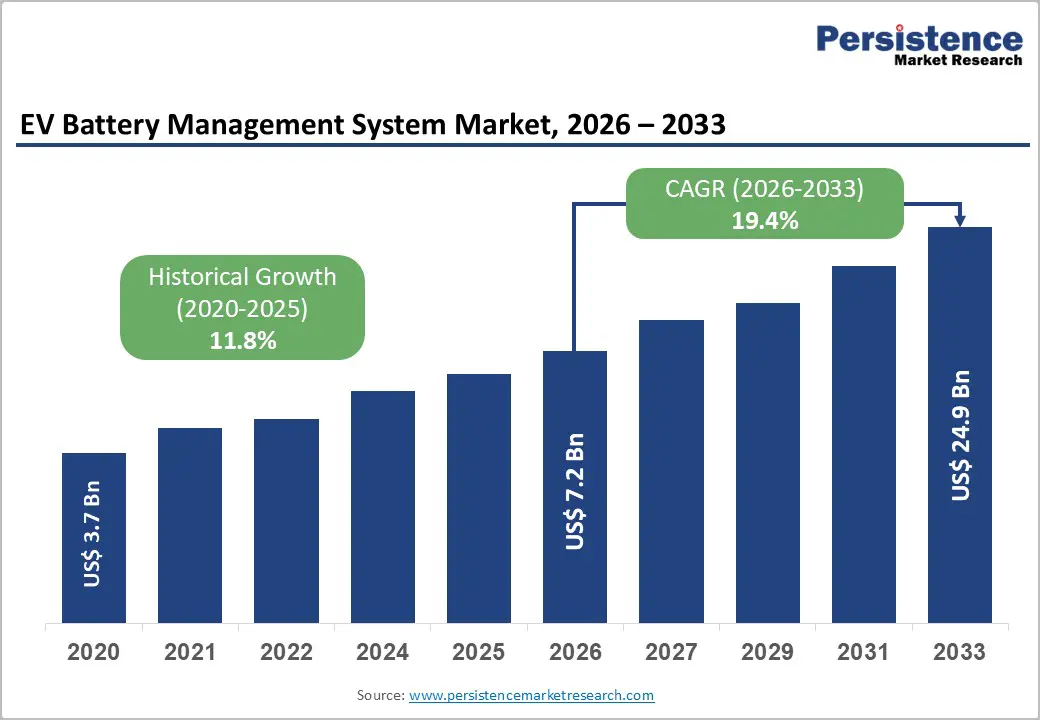

The global EV battery management system market is expected to reach US$7.2 billion in 2026 and US$24.9 billion by 2033, growing at a CAGR of 19.4% over the forecast period from 2026 to 2033. The market's exceptional growth trajectory is driven primarily by the rapid and sustained global expansion of electric vehicle adoption, tightening battery safety standards, and the increasing integration of artificial intelligence, IoT, and cloud computing into next-generation BMS architectures.

Key Market Highlights

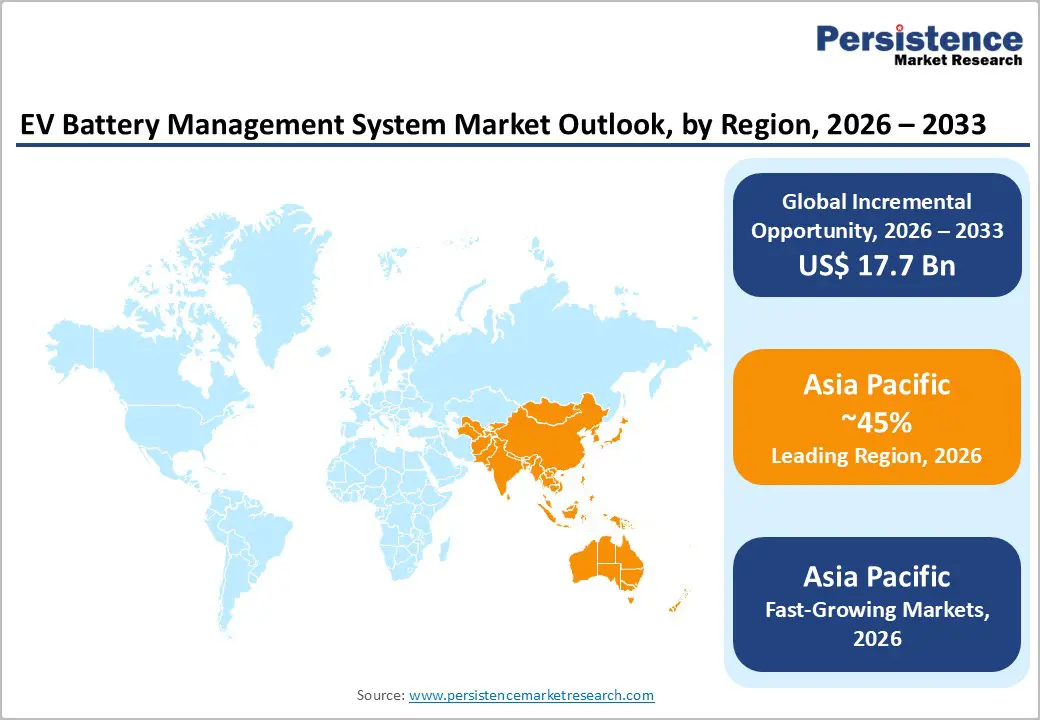

- Leading Region: Asia Pacific leads the global EV BMS Market with approximately 45% revenue share, driven by China's dominant EV production ecosystem, Japan's semiconductor leadership, and India's rapidly accelerating EV adoption supported by the PM E-Drive scheme allocating USD 1.3 billion to EV infrastructure

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region through 2033, propelled by India's booming EV policy momentum, China's NEV Plan targeting more than 40% EV share of new vehicle sales by 2035, and expanding BMS engineering ecosystems across ASEAN manufacturing hubs

- Leading Segment: Lithium-Ion (Li-Ion) chemistry dominates the By Battery Type category with approximately 72% revenue share, anchored by universal OEM adoption across BEV and HEV platforms and continuous investment by leading cell manufacturers in next-generation NMC and LFP chemistries, driving BMS demand

- Fastest-Growing Segment: Battery Electric Vehicles (BEVs) are the fastest-growing propulsion segment, with 14 million new EV registrations in 2023 and binding EU 2035 ICE phase-out regulation ensuring sustained structural demand growth for full-function, high-complexity BMS platforms through the forecast period

- Key Opportunity: AI- and machine learning-integrated predictive BMS platforms represent the highest-value opportunity, reducing battery failure risk by 20% and extending pack life by 15%, enabling BMS suppliers to offer premium OEM-validated platforms and BMS-as-a-Service subscription models generating recurring revenue streams

| Key Insights | Details |

|---|---|

|

EV Battery Management System Market Size (2026E) |

US$ 7.2 Billion |

|

Market Value Forecast (2033F) |

US$ 24.9 Billion |

|

Projected Growth CAGR (2026–2033) |

19.4% |

|

Historical Market Growth (2020–2025) |

11.8% |

Market Dynamics

Market Growth Drivers

Explosive Global EV Adoption Creating Structural, High-Volume Demand for Advanced BMS Solutions

The rapid global adoption of electric vehicles (EVs) is the strongest structural driver for the EV Battery Management System (BMS) market. Every battery electric and hybrid vehicle requires a BMS to monitor cell voltage, manage temperature, estimate state-of-charge (SOC) and state-of-health (SOH), and ensure safe battery operation, making it an essential component. Global EV battery consumption reached 285.4 GWh in the first five months of 2024, growing 23% year-on-year, highlighting the fast pace of EV production worldwide.

At the same time, automakers are shifting toward high-voltage battery systems such as 800V and 1,200V architectures, used by brands like Hyundai, Porsche, and Kia to enable ultra-fast charging. This transition is increasing the need for more precise monitoring, advanced thermal management, and better fault detection. As a result, BMS systems are becoming more complex and valuable, significantly increasing their cost and market potential per vehicle.

Increasingly Stringent Battery Safety Regulations Mandating Advanced BMS Compliance

Stricter global regulations around EV battery safety are driving the demand for more advanced and compliant BMS solutions. Automotive manufacturers must meet key international standards such as ISO 26262 for functional safety, IEC 62619 for battery safety, ISO 18243 for thermal risk management, and SAE J2929 for high-voltage battery systems. In addition, the European Union’s Battery Regulation (EU) 2023/1542 requires EV batteries to include a digital battery passport by 2026, capturing data such as battery health and carbon footprint.

This creates a direct need for BMS systems with real-time monitoring, data logging, and cloud connectivity. Meeting these requirements forces BMS suppliers to continuously upgrade their systems and maintain certifications. This ongoing need for updates and compliance creates recurring revenue opportunities through software upgrades, re-certification, and lifecycle management services, making regulatory pressure a strong and sustained market growth driver.

Market Restraints

High Development Cost and Integration Complexity in Multi-Chemistry Battery Architectures

Developing advanced BMS platforms requires significant investment, especially as EV manufacturers adopt multi-chemistry battery systems that combine lithium-iron-phosphate (LFP), nickel-manganese-cobalt (NMC), and emerging solid-state cells. Each chemistry has different performance and safety requirements, making integration more complex. Designing a BMS that meets the highest safety standard, ISO 26262 ASIL-D, can cost several million to tens of millions of dollars per platform.

This high development cost creates a major barrier for smaller suppliers and startups, limiting their ability to compete with established companies that already have certified systems in place. As a result, the market tends to favor large, experienced players. Additionally, in cost-sensitive markets, especially in developing regions, high system costs can slow the adoption of advanced BMS technologies, thereby restricting innovation and delaying the rollout of next-generation battery management solutions.

Cybersecurity Vulnerabilities in Connected BMS Architectures

As BMS systems become more connected through cloud platforms, IoT sensors, and over-the-air (OTA) updates, cybersecurity risks are emerging as a key challenge. A security breach in a BMS could allow unauthorized access to battery controls, potentially causing safety failures such as thermal runaway or system shutdowns. This creates serious safety and legal concerns for manufacturers. To address these risks, governments and regulatory bodies are introducing strict cybersecurity requirements.

UN Regulation No. 155 (UN R155), effective from July 2024, mandates that automakers implement cybersecurity management systems across the vehicle lifecycle. Compliance with such regulations increases the complexity and costs of BMS development for BMS providers. Companies must now invest heavily in secure hardware, encrypted communication, and continuous monitoring systems, making cybersecurity not only a technical challenge but also a significant financial and operational restraint in the market.

Market Opportunities

AI- and Machine Learning-Enabled Predictive BMS as a High-Value Differentiation Platform

The integration of artificial intelligence (AI) and machine learning (ML) into BMS platforms presents a major growth opportunity in the EV market. AI-powered BMS systems use real-time sensor data along with cloud-based algorithms to predict battery health, optimize charging patterns, and detect early signs of degradation. Research shows that AI-based SOC and SOH estimation can reduce battery failure risk by around 20% and extend battery life by up to 15% compared to traditional systems.

Leading companies such as Infineon, STMicroelectronics, and Monolithic Power Systems are actively developing AI-enabled BMS chips and software solutions. These advanced systems can be offered as upgrades to existing vehicle platforms, making them highly attractive to fleet operators aiming to reduce maintenance costs and improve battery performance. As a result, AI-driven BMS solutions are expected to command premium pricing and support long-term service-based revenue models.

Vehicle-to-Grid (V2G) Integration and Second-Life Battery Applications

The rise of vehicle-to-grid (V2G) technology and second-life battery applications is creating new opportunities for advanced BMS solutions beyond traditional automotive use. V2G allows EV batteries to supply energy back to the grid during peak demand, requiring BMS systems to manage two-way energy flow while maintaining battery safety and efficiency. This adds a new level of complexity compared to standard charging systems.

According to the International Renewable Energy Agency (IRENA), V2G-enabled EVs could provide around 780 GW of grid-support capacity by 2030, underscoring the scale of this opportunity. Additionally, retired EV batteries are increasingly being reused in stationary energy storage systems, creating demand for BMS reprogramming, health monitoring, and certification services. Companies like LOHUM in India are leading this space, developing scalable solutions that generate recurring revenue streams independent of new-vehicle sales.

Category-wise Insights

By Battery Type Analysis

Lithium-ion (Li-ion) batteries dominate the EV battery management system market by battery type, accounting for approximately 72% of total revenue. This dominance is driven by their high energy density, long lifecycle, and continuous cost reductions, making them the preferred choice for most EV manufacturers worldwide. Major battery producers such as Panasonic, CATL, and LG Energy Solution continue to invest in advanced lithium-ion technologies, including NMC and LFP chemistries.

These batteries require highly sophisticated BMS solutions to accurately manage voltage, temperature, and cell balancing, thereby increasing the overall system value. This complexity allows BMS suppliers to command higher prices than simpler battery types. Meanwhile, Nickel-Metal Hydride (NiMH) batteries still hold a smaller share in hybrid vehicles but are gradually declining as the market shifts toward fully electric vehicles powered by lithium-ion technology.

By Propulsion Type Analysis

Battery Electric Vehicles (BEVs) lead the EV BMS market by propulsion type, contributing around 68% of total revenue. This leadership is due to the global shift toward full electrification, where BEVs rely entirely on battery systems for operation. Unlike hybrid vehicles, BEVs require larger battery packs, typically ranging from 40 kWh to over 150 kWh, which increases the need for advanced and highly reliable BMS solutions.

The performance, driving range, and safety of a BEV depend heavily on the accuracy and efficiency of its BMS, making it a critical component. Governments across regions, including Europe, China, the U.S., and the U.K., are introducing strict regulations to phase out internal combustion engines, further accelerating BEV adoption. This trend ensures that demand for high-performance BMS systems in BEVs will continue to grow strongly over the coming years.

By Topology Analysis

The centralized BMS topology currently holds the largest market share, accounting for approximately 47%, due to its simple design, lower cost, and ease of integration. In this setup, all monitoring and control functions are handled by a single control unit, making it suitable for standard passenger EVs with moderate battery sizes. It also simplifies compliance with safety standards such as ISO 26262.

The modular BMS architecture is emerging as the fastest-growing segment, especially in commercial vehicles, electric buses, and large battery systems. Modular designs offer better scalability, improved fault tolerance, and easier maintenance, making them ideal for high-capacity battery applications. As global EV battery demand continues to grow rapidly, manufacturers are increasingly adopting modular BMS solutions that can be customized across multiple platforms without requiring complete redesign, improving efficiency and reducing long-term costs.

By Vehicle Type Analysis

Passenger cars dominate the EV BMS market by vehicle type, accounting for around 61% of total revenue. This is largely due to the high volume of global EV adoption in the passenger segment, with over 14 million new EV registrations recorded in 2023. BMS systems in passenger vehicles are designed to deliver reliability, support over-the-air updates, and integrate with advanced vehicle systems such as infotainment and telematics.

These features increase their overall value and importance. At the same time, the commercial vehicle segment is growing at the fastest pace, driven by the electrification of buses, delivery vans, and heavy trucks. Commercial vehicles require more robust BMS systems capable of handling longer operating hours, higher loads, and fleet-level monitoring. These advanced requirements result in higher system complexity and pricing, making this segment a key contributor to future market growth.

Regional Insights

North America EV Battery Management System Market Trends

North America represents a highly innovative and policy-driven market for EV Battery Management Systems, supported by strong government initiatives such as the U.S. Inflation Reduction Act of 2022. This act allocates over USD 370 billion toward clean energy and electric mobility, including incentives for domestic battery production, which directly supports BMS supply chain growth. Research institutions like Argonne National Laboratory, Oak Ridge National Laboratory, and the National Renewable Energy Laboratory are actively developing next-generation BMS technologies, including AI-based battery monitoring and grid-integrated charging systems.

The region also hosts leading companies such as Infineon Technologies and Monolithic Power Systems, which are developing advanced BMS semiconductors aligned with strict safety standards. In addition, Canada’s EV infrastructure programs and incentives are boosting EV adoption, increasing demand for advanced BMS solutions across both passenger and commercial vehicle segments.

Europe EV Battery Management System Market Trends

Europe offers one of the most supportive regulatory environments for the growth of EV BMS technologies, driven by policies such as the EU Battery Regulation and the Fit for 55 initiative. The requirement for a digital battery passport by 2026 is pushing automakers to adopt advanced BMS systems capable of real-time data tracking and lifecycle monitoring. Germany leads the region, with major automakers like BMW, Volkswagen, and Mercedes-Benz investing heavily in EV development.

Countries such as France and the U.K. are expanding battery manufacturing capacity through new gigafactories, increasing demand for BMS integration. Spain is also emerging as a key EV production hub. Additionally, strict cybersecurity regulations, including UN R155 compliance, are forcing manufacturers to adopt secure and encrypted BMS systems, raising both the technical standards and overall value of BMS solutions across the European market.

Asia Pacific EV Battery Management System Market Trends

Asia Pacific dominates the global EV BMS market, accounting for approximately 45% of total revenue, led by China’s strong position in EV production and battery manufacturing. Government policies such as China’s NEV Development Plan (2021–2035) are driving large-scale EV adoption, ensuring sustained demand for BMS solutions. Chinese companies like CATL and BYD have developed integrated battery and BMS systems, strengthening their competitive advantage.

Japan contributes through advanced semiconductor technologies from companies like Panasonic and Renesas. India is emerging as a fast-growing market, supported by government initiatives such as the PM E-Drive scheme, which promotes EV adoption and infrastructure development. Indian firms, including Tata Elxsi, eInfochips, Cyient, and SRM Technologies, are building strong capabilities in BMS software and engineering services, positioning the country as an important hub for global BMS development.

Competitive Landscape

The EV battery management system market is moderately fragmented, with competition among global semiconductor leaders, system integrators, and emerging software-focused companies. Established players such as Infineon, STMicroelectronics, and Texas Instruments lead the market with automotive-grade semiconductor solutions that meet strict safety standards like ISO 26262 ASIL-D. System integrators such as Aptiv provide complete BMS platforms, while newer companies like eInfochips and Tata Elxsi focus on software innovation.

Key competitive advantages include advanced SOC and SOH estimation algorithms, AI integration, and strong partnerships with automotive manufacturers. New business models, such as BMS-as-a-Service (BMSaaS), are gaining traction by offering cloud-based battery monitoring on a subscription basis. Additionally, ongoing research into solid-state battery compatibility and advanced power electronics is intensifying competition, as companies prepare for the next generation of EV technologies expected to emerge in the coming years.

Key Market Developments

- In February 2025: Infineon Technologies introduced the XENSIV TLF35584 automotive power management IC family, engineered for advanced 800V EV battery systems. The solution enhances functional safety, supports ISO 26262 ASIL-D compliance, and strengthens reliability for next-generation global OEM BMS architectures.

- In October 2024: Tata Elxsi deployed its AI-powered BMS software platform with a leading Indian electric bus OEM. The platform integrates machine learning-based SOH prediction and OTA updates, advancing localized BMS innovation and improving battery lifecycle management in South Asia’s EV ecosystem.

- In March 2024, STMicroelectronics launched the L9963E multi-cell battery monitoring IC, designed for high-voltage EV battery packs. Qualified under AEC-Q100 Grade 1, it ensures automotive-grade reliability, precise cell monitoring, and supports scalable BMS designs for global OEMs and Tier-1 integrators.

Companies Covered in EV Battery Management System Market

- Infineon Technologies

- Zebra Technologies

- Panasonic

- Cyient

- SRM Technologies Private Ltd.

- Monolithic Power Systems, Inc.

- Aptiv

- LOHUM

- eInfochips

- STMicroelectronics

- LocoNav

- Cavli Inc.

- Tata Elxsi

- Bacancy Company

- LEM International SA

- Texas Instruments

Frequently Asked Questions

The global EV Battery Management System Market is estimated at US$ 7.2 Billion in 2026 and is projected to reach US$ 24.9 Billion by 2033, growing at a CAGR of 19.4%, driven by accelerating EV adoption, with the IEA reporting 14 million new EV registrations globally in 2023, and increasingly stringent battery safety compliance requirements under ISO 26262 and EU Battery Regulation 2023/1542.

The key drivers are explosive global EV adoption, with battery consumption growing 23% year-on-year through mid-2024, combined with mandatory regulatory compliance requirements under IEC 62619, ISO 26262 ASIL-D, and the EU Battery Regulation mandating a digital battery passport from 2026, compelling OEMs to deploy advanced, cloud-connected BMS platforms with real-time diagnostics and lifecycle traceability.

Lithium-Ion (Li-Ion) batteries lead the By Battery Type segment with approximately 72% market share, owing to their universal adoption across BEV and HEV platforms by global OEMs, superior energy density, declining cell cost trajectory, and the technical complexity of Li-Ion management, requiring advanced cell balancing, thermal regulation, and SOC estimation, which commands premium BMS system pricing from suppliers including Infineon, STMicroelectronics, and Panasonic.

Asia Pacific is the leading region with approximately 45% of global revenues, anchored by China's position as the world's largest EV market under the NEV Industry Development Plan (2021–2035), Japan's semiconductor and BMS technology leadership, and India's rapidly accelerating EV adoption bolstered by the PM E-Drive scheme's USD 1.3 billion infrastructure investment commitment.

The integration of AI and machine learning into predictive BMS platforms represents the most commercially valuable opportunity, with published research demonstrating a 20% reduction in battery failure risk and 15% extension of pack service life versus conventional BMS. Suppliers offering OEM-validated AI-BMS platforms with cloud connectivity and BMS-as-a-Service subscription pricing can capture premium revenue and recurring contract streams through 2033.

The leading market participants include Infineon Technologies, STMicroelectronics, Panasonic, Aptiv, Monolithic Power Systems, Inc., LEM International SA, Tata Elxsi, eInfochips, Cyient, SRM Technologies Private Ltd., LOHUM, LocoNav, Cavli Inc., Bacancy Company, and Zebra, alongside additional key players NXP Semiconductors, Texas Instruments, Renesas Electronics, and Analog Devices who supply critical BMS semiconductor platforms globally.