- Automotive Components & Materials

- Automotive Carbon Brush Market

Automotive Carbon Brush Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Carbon Brush Market by Brush Grade (Electrographite, Silver Graphite, Others), Application (Safety and Chassis Electronic System, Body Electronic System, Others), Vehicle Type, Propulsion, and Regional Analysis for 2026 - 2033

Automotive Carbon Brush Market Size and Trends Analysis

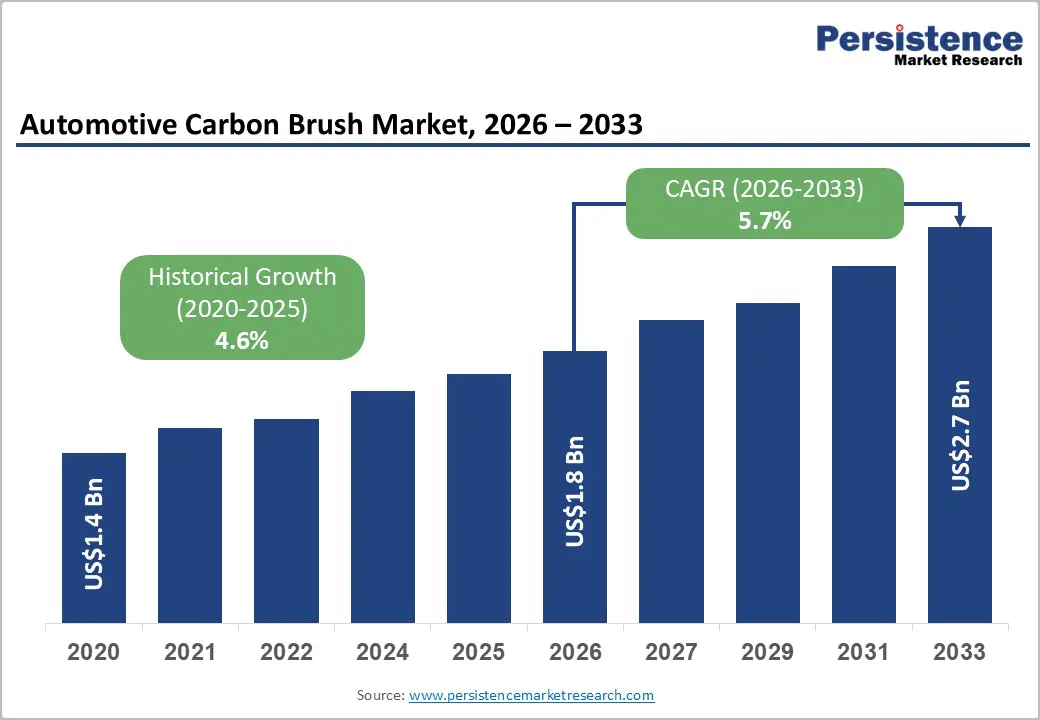

The global automotive carbon brush market size is likely to be valued at US$1.8 billion in 2026 and is expected to reach US$2.7 billion by 2033, growing at a CAGR of 5.7% during the forecast period from 2026 to 2033, driven by the continued use of carbon brushes in starters, alternators, fuel pumps, HVAC motors, windshield wipers, power windows, and electronic comfort systems across passenger and commercial vehicles.

Rising electrification in vehicles is increasing demand for high-performance brush materials capable of delivering superior conductivity, lower wear, and enhanced thermal stability. Growing adoption of brushless motor technologies is encouraging manufacturers to focus on engineered carbon grades, advanced lifecycle performance, and application-specific solutions rather than volume-driven production.

Key Industry Highlights:

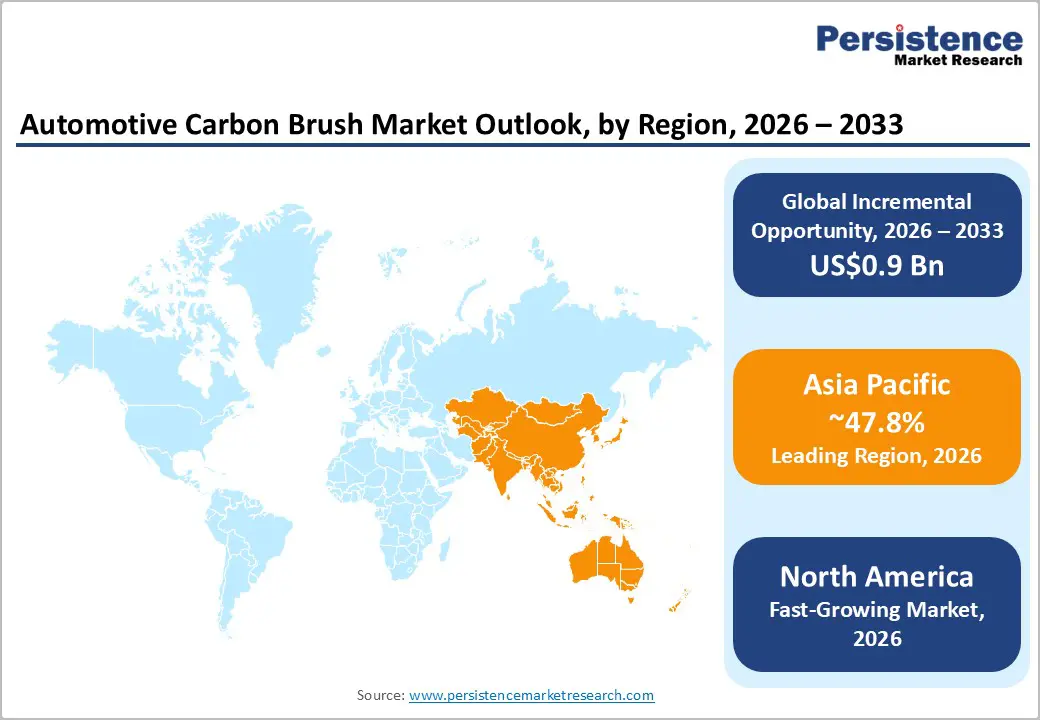

- Leading Region: Asia Pacific is projected to account for approximately 47.8% of the market share, supported by large-scale automotive production in China, Japan, India, and South Korea, along with strong EV manufacturing and aftermarket demand.

- Fastest-growing Region: North America is projected to register the fastest growth, driven by rising EV adoption, expanding SUV demand, and increasing replacement demand from commercial vehicle fleets.

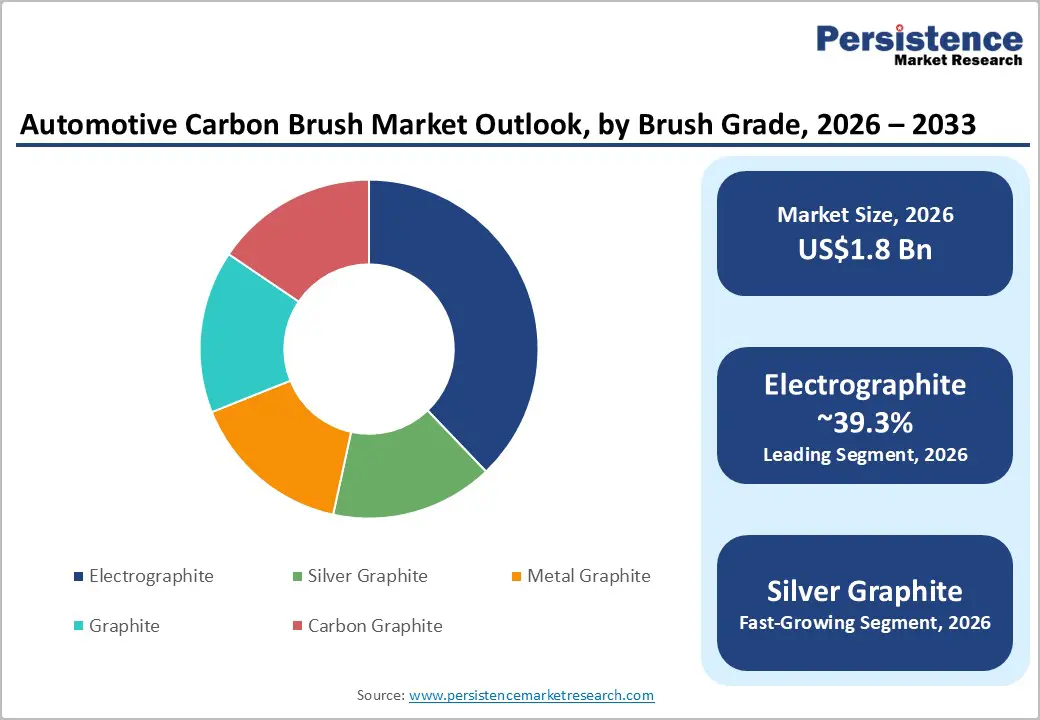

- Dominant Brush Grade: Electrographite is anticipated to lead, accounting for approximately 39.3% market share, owing to its balanced conductivity, wear resistance, thermal stability, and broad compatibility across ICE and hybrid vehicle systems.

- Leading Application: Safety and chassis electronic systems are estimated to account for approximately 48.4% market share, supported by growing integration of ABS systems, electric steering modules, braking systems, fuel pumps, and electronically controlled safety components across modern vehicles.

DRO Analysis

Driver - Vehicle Electrification Is Increasing Demand for Advanced Carbon Brush Solutions

The rapid growth of vehicle electrification is significantly increasing the use of electrical motors and electronically actuated systems across passenger and commercial vehicles. Global electric vehicle adoption continues to accelerate, with electric car sales surpassing 17 million units in 2024 and accounting for more than 20% of total global car sales. Electrified vehicles require a larger number of auxiliary motors for thermal management, HVAC systems, battery cooling, steering systems, fuel pumps, braking systems, and comfort features. These systems depend on reliable current transfer and long operating life, creating higher demand for advanced carbon brush materials.

Automotive manufacturers are increasingly prioritizing carbon brushes with improved conductivity, reduced sparking characteristics, and superior wear resistance. Suppliers are investing in electrographitic and silver graphite grades capable of operating under high-temperature and high-current environments. The transition toward hybrid and electric vehicle platforms is therefore not eliminating carbon brush demand entirely; instead, it is shifting the market toward premium-grade engineered products designed for enhanced durability and operational efficiency.

Strong Automotive Production in Asia Pacific Is Sustaining Long-Term Market Volume

Automotive manufacturing concentration in Asia Pacific remains a major growth driver for the Automotive Carbon Brush market. China produced more than 31 million vehicles in 2024, while Japan, India, and South Korea collectively accounted for a substantial share of global automotive output. Asia-Oceania contributed nearly 55 million vehicles to global production, making the region the largest manufacturing base for automotive electrical components and replacement parts.

India has emerged as a particularly important growth market due to rising domestic vehicle demand, expanding exports, and government-backed EV initiatives. Domestic automotive sales in India increased by more than 7% in FY2024-25, while exports recorded double-digit growth. Rising vehicle ownership directly increases demand for replacement carbon brushes used in starters, alternators, blower motors, and power systems. Manufacturers with localized production facilities, regional distribution capabilities, and broad product portfolios are gaining competitive advantages through reduced logistics costs and faster aftermarket response times.

Restraint - Increasing Adoption of Brushless Motor Technologies Is Limiting Market Expansion

The growing shift toward brushless motor systems represents the most significant structural challenge for the Automotive Carbon Brush market. Modern automotive platforms are increasingly adopting brushless DC motors in applications such as cooling systems, electric steering, HVAC assemblies, and advanced powertrain systems because these technologies offer lower maintenance requirements, improved efficiency, and reduced wear.

Electric vehicle manufacturers are accelerating this transition by redesigning electrical architectures to reduce mechanical friction and improve energy efficiency. Many newly introduced EV models now integrate brushless systems for auxiliary applications that historically relied on conventional carbon brush assemblies. Although carbon brushes remain essential across multiple systems, the gradual shift toward brushless technologies is reducing the addressable market volume in some applications.

Opportunity - Aftermarket Replacement Demand and Fleet Maintenance Are Creating Stable Revenue Streams

The automotive aftermarket remains a major opportunity for carbon brush suppliers, driven by the ongoing replacement needs of commercial fleets and the aging vehicle population. Carbon brushes experience natural wear during operation and require periodic replacement to maintain electrical performance in starters, alternators, fuel pumps, and comfort-system motors. Heavy-duty trucks, buses, construction equipment, and logistics fleets generate particularly strong replacement demand because equipment uptime directly affects operational profitability.

Fleet operators increasingly prefer high-durability replacement components that minimize maintenance intervals and reduce downtime. This trend creates opportunities for manufacturers offering engineered brush kits, brush-holder assemblies, and predictive maintenance support services. North America and Asia Pacific are especially attractive markets due to their large commercial vehicle populations and expanding logistics sectors.

High-Performance Brush Grades for Electrified Systems Are Expanding Premium Product Demand

The market is witnessing a clear transition from standard carbon materials toward specialized brush grades designed for demanding electrical environments. Electrified vehicle systems require improved current transfer stability, thermal resistance, and operational reliability under continuous load conditions. This is increasing demand for silver-graphite, electrographitic, and metal-graphite brush materials used in advanced auxiliary systems and high-current applications.

Manufacturers are actively introducing premium formulations that reduce friction, extend component life, and improve energy efficiency. Demand for advanced grades is expected to rise in EV thermal management systems, electrically assisted steering systems, battery cooling systems, and high-speed rotating electrical assemblies. The opportunity is particularly strong in regions investing heavily in electric mobility infrastructure and advanced automotive manufacturing.

Category-wise Analysis

Brush Grade Insights

Electrographite is anticipated to account for approximately 39.3% of the market share in 2026, making it the leading brush grade segment. The segment maintains leadership because electrographitic brushes provide an effective balance between conductivity, mechanical strength, commutator compatibility, and wear resistance. These brushes are widely used in alternators, starter motors, blower motors, windshield wiper systems, and fuel pumps across passenger and commercial vehicles.

Major automotive suppliers use electrographitic grades in starter assemblies and HVAC blower systems because of their stable performance under fluctuating voltage and thermal conditions. Automotive OEMs continue to prefer electrographitic grades because they offer reliable operational performance while maintaining manageable replacement costs.

Silver graphite is anticipated to witness the fastest growth. Growth is being driven by increasing demand for high-conductivity materials capable of supporting advanced electrical systems operating under high current density and elevated temperatures. Automotive manufacturers are increasingly deploying silver graphite brushes in premium auxiliary systems where low electrical resistance and operational stability are critical. Silver graphite brushes offer lower contact resistance, reduced energy losses, and improved wear performance compared to conventional grades.

For instance, electric cooling pumps, battery thermal-control systems, and electronically assisted steering assemblies increasingly require high-performance brush materials capable of operating continuously under demanding electrical loads.

Application Insights

Safety and chassis electronic systems are anticipated to account for approximately 48.4% share in 2026, making them the leading application segment. Carbon brushes are extensively used in ABS systems, braking modules, fuel pumps, windshield wiper systems, starter assemblies, and steering-related electronic systems where reliable current transmission is critical. The increasing integration of electronically controlled braking and steering technologies across passenger vehicles continues to strengthen demand for durable carbon brush assemblies.

The growing integration of electronically controlled safety systems across both premium and mass-market vehicles continues to strengthen demand. Automotive manufacturers are increasing the number of electrically actuated systems in vehicles to improve safety performance, driving comfort, and operational reliability. For example, electric power steering systems and anti-lock braking modules in SUVs and premium sedans rely on stable electrical contact systems capable of operating under continuous vibration and temperature variation.

Body electronic systems are the fastest-growing application segment. Demand is increasing due to the rising adoption of powered windows, power seats, mirrors, sunroofs, automated tailgates, and electronically controlled cabin comfort systems across all vehicle categories. Modern passenger vehicles now incorporate a significantly greater number of compact electric motors than previous generations, thereby increasing carbon brush consumption. Consumer preference for convenience and premium cabin experiences is accelerating the integration of electrical actuators and motor-driven systems even in mid-range vehicles.

For instance, premium SUVs increasingly feature powered tailgates, automatic seat-adjustment systems, and multi-zone climate-control assemblies that depend on compact motor systems using carbon brush technology.

Regional Insights

North America Automotive Carbon Brush Market Trends

North America is expected to be the fastest-growing regional market and is projected to expand at approximately 7.1% CAGR during the forecast period. The region benefits from strong automotive production, rising electrification, growing SUV penetration, and a well-established commercial vehicle aftermarket. Increasing adoption of electronically controlled comfort and safety systems is supporting demand for advanced automotive carbon brushes across OEM and replacement channels.

U.S. Automotive Carbon Brush Market Trends

The U.S. represents the largest market in North America due to its substantial automotive manufacturing base and high demand for SUVs, pickup trucks, and commercial vehicles. Vehicle production across the country exceeded 10 million units in 2024, supporting strong consumption of electrical components used in starters, alternators, HVAC systems, windshield wipers, and fuel pumps.

The country is also witnessing rapid electric vehicle adoption, with automakers increasing investments in advanced electrical architectures and high-performance auxiliary systems. Heavy-duty trucks and logistics fleets generate significant aftermarket replacement demand for carbon brushes used in charging systems, blower motors, and powertrain support systems. The growing popularity of premium SUVs equipped with powered seating systems, automated tailgates, and advanced climate-control systems is further increasing carbon brush integration per vehicle.

Rising automotive exports and increasing localization of component manufacturing are creating favorable conditions for carbon brush suppliers operating in the region. Manufacturers are increasingly using the country as a regional production base for automotive electrical assemblies and replacement components serving both North American markets.

Europe Automotive Carbon Brush Market Trends

Europe remains a technologically advanced and regulation-driven market for automotive carbon brushes. The region benefits from strong automotive engineering capabilities, high penetration of advanced electronic systems, and growing investment in vehicle electrification technologies. European automakers continue to prioritize efficiency optimization, lightweight vehicle design, and premium electrical architectures, creating demand for advanced carbon brush materials capable of operating under stringent performance requirements.

Germany Automotive Carbon Brush Market Trends

Germany remains the leading automotive manufacturing country in Europe and serves as the region’s primary innovation center for advanced vehicle technologies. German automakers continue to invest heavily in electrification, premium mobility systems, and next-generation electronic architectures, directly supporting demand for high-performance carbon brushes. The country’s strong production base for luxury vehicles and premium SUVs increases demand for advanced comfort systems, electronically controlled chassis modules, and precision motor assemblies. German suppliers are also focusing on engineered electrographitic and silver graphite grades capable of supporting higher electrical efficiency and longer service life.

U.K. Automotive Carbon Brush Market Trends

The U.K. remains an important market for automotive engineering, premium vehicle manufacturing, and electric mobility development. The country is increasing investments in EV infrastructure, battery manufacturing, and electrified transportation systems, supporting demand for advanced electrical components.

Luxury vehicle production and strong adoption of technologically advanced comfort systems continue to create demand for premium carbon brush materials. The aftermarket segment also remains important due to the country’s large vehicle parc and established automotive service network.

The country also benefits from strong aftermarket demand due to aging vehicle fleets and increasing maintenance requirements for commercial transportation systems. Suppliers are focusing on durable brush materials capable of operating under demanding mechanical and thermal conditions.

Asia Pacific Automotive Carbon Brush Market Trends

Asia Pacific is projected to lead the market with approximately 47.8% share and is projected to expand at a 5.4% CAGR during the forecast period. The region remains the global center for automotive manufacturing due to high production volumes, integrated supply chains, cost-efficient manufacturing capabilities, and rising domestic vehicle demand. Strong growth in EV adoption and increasing localization of automotive component production continue to support long-term market expansion.

China Automotive Carbon Brush Market Trends

China represents the largest automotive market globally and remains the dominant contributor to regional automotive carbon brush demand. The country produced more than 31 million vehicles in 2024 and continues to lead global EV sales and battery manufacturing capacity.

The rapid expansion of electric vehicles, smart mobility systems, and advanced electronic vehicle architectures is increasing demand for high-performance carbon brush materials used in auxiliary systems, thermal management modules, and electrically controlled components. China’s strong manufacturing ecosystem and large-scale automotive exports continue to strengthen its leadership position in the regional market.

Japan Automotive Carbon Brush Market Trends

Japan remains a major center for automotive engineering, precision manufacturing, and advanced electrical component development. Japanese automakers continue to prioritize hybrid vehicles, fuel-efficient technologies, and premium electrical systems that require reliable current-transfer materials.

The country’s strong presence in compact motors, thermal-control systems, and precision automotive electronics supports steady demand for electrographitic and specialty carbon brush grades. Japanese suppliers are also investing in advanced materials research focused on durability, conductivity, and reduced wear characteristics.

Increasing urbanization, rising disposable income, and expanding automotive assembly operations are supporting demand for electrical components and aftermarket replacement parts across the region. As EV investments increase across ASEAN economies, demand for advanced automotive carbon brush materials is expected to strengthen steadily over the forecast period.

Competitive Landscape

The global automotive carbon brush market is moderately fragmented, with a combination of global material specialists and regional manufacturers competing across OEM and aftermarket channels. Leading companies collectively account for a significant share of global revenue, although regional suppliers continue to maintain strong positions in local markets due to cost competitiveness and established distribution networks.

Leading companies are focusing on premium material innovation, localized manufacturing expansion, and lifecycle service capabilities. Strategic priorities include the development of high-performance brush grades, the strengthening of aftermarket distribution networks, and increased collaboration with automotive OEMs on customized electrical system solutions.

Key Industry Developments:

- In May 2025, Morgan Advanced Materials announced the launch of its new National™ S22 silver carbon brush grade, developed to deliver lower contact resistance, extended service life, and improved efficiency in high-current applications, strengthening the company’s advanced carbon materials portfolio for electrified mobility and industrial systems.

Companies Covered in Automotive Carbon Brush Market

- Mersen

- Schunk Group

- Morgan Advanced Materials

- Helwig Carbon Products

- Toyo Tanso Co., Ltd.

- Fuji Carbon Manufacturing Co., Ltd.

- AVOCarbon Group

- Assam Carbon Products Ltd.

- Omniscient International

- Graphite India Limited

- SGL Carbon SE

- Tris Incorporated

- Carbone Lorraine

- Aupac Co., Ltd.

- Elektrokarbon a.s.

- Phynyx Industrial Products Pvt. Ltd.

Frequently Asked Questions

The global automotive carbon brush market is likely to be valued at approximately US$1.8 billion in 2026.

The market is expected to reach approximately US$2.7 billion by 2033.

The automotive carbon brush market is projected to grow at a CAGR of 5.7% between 2026 and 2033.

Key trends include rising adoption of high-performance brush materials, increasing electrification of vehicle systems, expansion of EV thermal-management applications, growing demand for aftermarket replacement components, and higher integration of electronically controlled comfort and safety systems.

Electrographite is the leading brush grade segment, accounting for approximately 39.3% market share, owing to its balanced conductivity, wear resistance, and cost efficiency across automotive electrical applications.

Some of the major companies include Mersen, Schunk Group, Morgan Advanced Materials, Helwig Carbon Products, and Toyo Tanso Co., Ltd.