- Automotive Components & Materials

- Premium and Prestige Tire Market

Premium and Prestige Tire Market Size, Share, and Growth Forecast 2026 - 2033

Premium and Prestige Tire Market by Vehicle Type (Passenger Cars, SUVs & Crossovers, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers, Off-the-Road Vehicles), and Product Construction (Radial Tires, Bias Tires, Tubeless Tires, Tube-Type Tires), by Technology, by Sales Channel, End-user, and Regional Analysis, 2026 - 2033

Premium and Prestige Tire Market Size and Trend Analysis

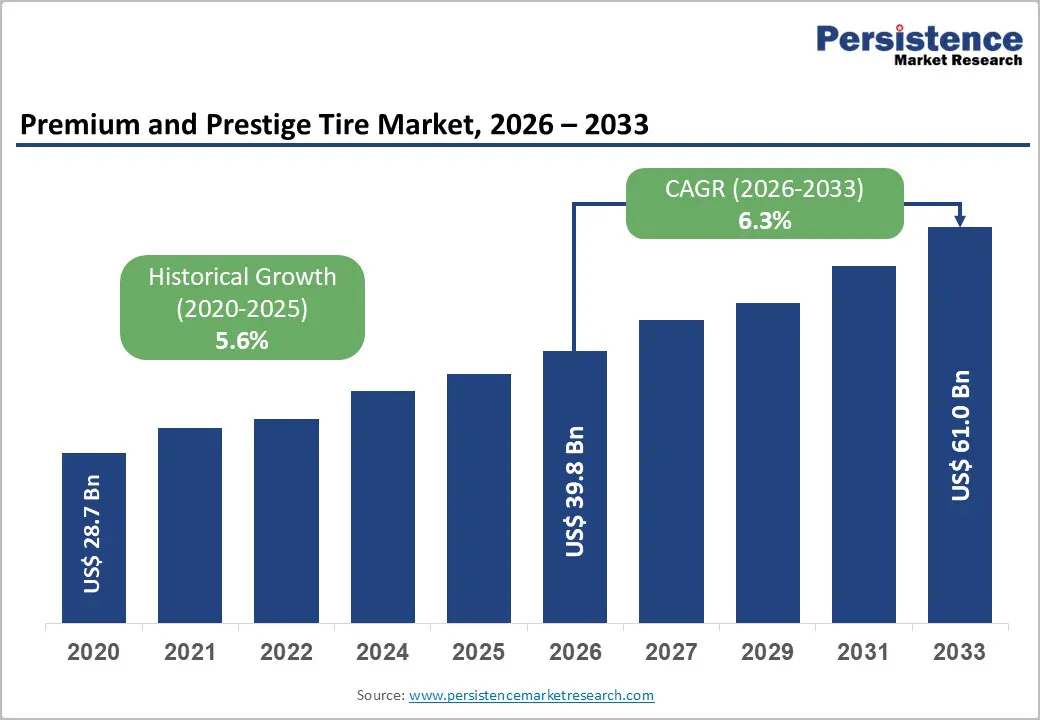

The global Premium and Prestige Tire market size is likely to be valued at US$ 39.8 billion in 2026 and is expected to reach US$ 61.0 billion by 2033, growing at a CAGR of 6.3% during the forecast period from 2026 to 2033. The premium and prestige tire market is experiencing robust and sustained growth, driven by the global proliferation of luxury and high-performance vehicles, the rapid electrification of passenger car fleets, and rising consumer expectations for ride quality, safety, and sustainability.

Key Industry Highlights:

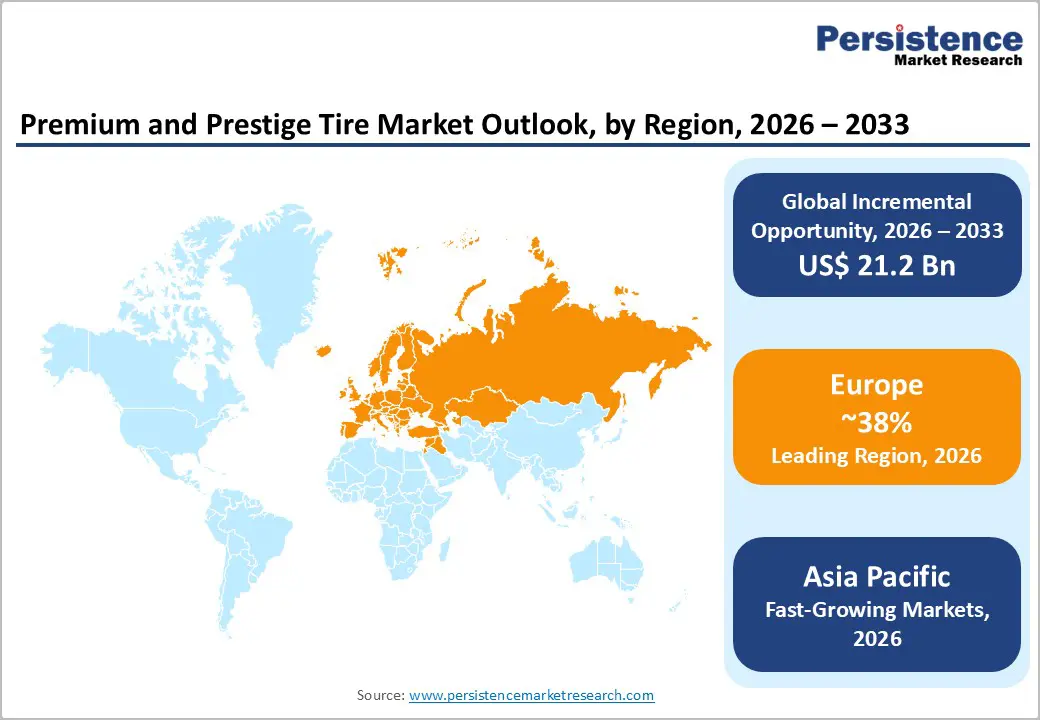

- Leading Region: Europe leads the global premium and prestige tire market likely to account for 38% share in 2026, driven by its world-class automotive OEM base, including BMW Group, Mercedes-Benz Group, and Volkswagen Group, and strong regulatory demand for high-rated, low rolling resistance premium tire fitments.

- Fastest Growing Market: Asia Pacific is the fastest-growing region with a CAGR of 7.8%, with China's luxury car market expanding at double-digit rates, India's premium vehicle sales surging, and ASEAN nations recording rising automotive ownership and aspirational premium tire adoption.

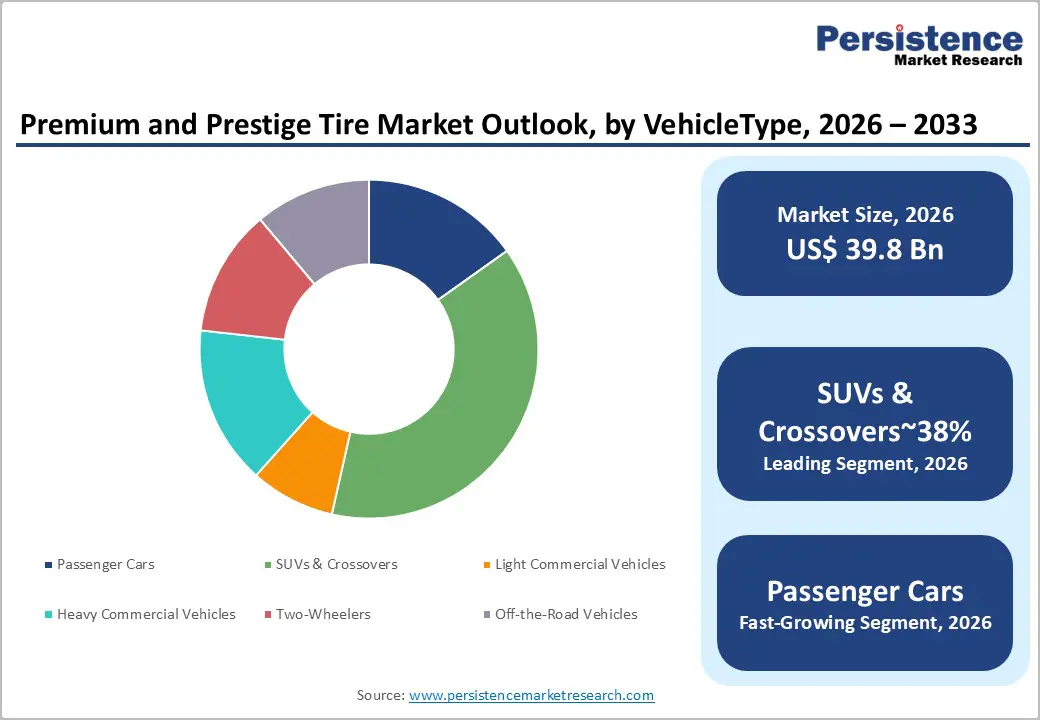

- Dominant Segment: SUVs & crossovers dominate with approximately 38% market share, driven by the explosive global growth of premium SUV models requiring large-diameter, high-specification tires from brands across Europe, North America, and Asia Pacific.

- Fastest Growing Segment: EV-specific tires are the fastest-growing technology segment, as global EV adoption surpasses 14 million annual units, demanding reinforced, low-rolling-resistance, acoustically optimized tires that command significant premiums over standard fitments.

- Key Opportunity: Smart tire technology, integrating embedded sensors and connected vehicle platforms, offers premium manufacturers a transformational opportunity to move beyond commodity replacement cycles into high-margin, data-enabled recurring revenue models.

Market Dynamics

Drivers - Global Luxury Vehicle Sales Growth and OEM Premiumization Trend

The sustained global expansion of luxury and premium vehicle sales is the primary structural driver of the premium tire market. According to the European Automobile Manufacturers' Association (ACEA), premium vehicle segments have consistently outgrown volume segments in registrations across Europe and major global markets.

Brands such as BMW, Mercedes-Benz, Audi, and Porsche continue to grow their global vehicle parc, with each unit requiring premium-specification tires both at OEM fitment and across multiple replacement cycles. The World Motor Vehicle Council notes that premium SUVs and crossovers now account for the fastest-growing vehicle sub-segment globally, further amplifying per-vehicle tire size and specification requirements. This structural premiumization of the global vehicle fleet ensures consistent, compounding demand for premium tire manufacturers.

Rapid EV Adoption and the Emergence of EV-Specific Tire Demand

The electrification of global passenger car fleets is fundamentally reshaping tire specification requirements and creating a significant new premium tire demand category. Electric vehicles exert unique stresses on tires: instantaneous torque delivery accelerates tread wear, higher curb weights increase load demands, and EV buyers prioritize rolling resistance efficiency for extended range.

The International Energy Agency (IEA) reports that global EV sales exceeded 14 million units in 2023, with China, Europe, and the U.S. leading adoption. EV-specific tires, featuring reinforced sidewalls, low rolling resistance compounds, and acoustic foam insulation, command significant price premiums over standard tires. Manufacturers, including Michelin and Continental AG have already introduced dedicated EV tire product lines, reflecting the opportunity's commercial significance.

Restraints - Intense Price Competition from Mid-Tier and Economy Tire Brands

The premium tire market faces persistent downward pricing pressure from the proliferation of capable mid-tier brands, particularly manufacturers from China, South Korea, and other Asian markets offering competitive performance at significantly lower price points.

According to the European Tyre & Rubber Manufacturers' Association (ETRMA), price sensitivity remains a dominant purchasing criterion for a significant proportion of replacement tire buyers, even among those owning premium vehicles. Budget-conscious consumers frequently opt for second-tier brands during replacement, limiting the addressable market for premium-price-point tires in cost-sensitive regions and economic downturns.

Raw Material Price Volatility Impacting Production Economics

Premium tire manufacturing relies heavily on natural rubber, synthetic rubber, carbon black, and specialty chemicals, all of which are subject to significant price volatility. Natural rubber prices are influenced by weather conditions in major producing countries including Thailand, Indonesia, and Vietnam.

The Association of Natural Rubber Producing Countries (ANRPC) documents frequent supply disruptions and price swings that compress manufacturer margins. Petroleum-derived synthetic rubber prices correlate with crude oil market volatility, creating compounding input cost uncertainty that challenges premium tire manufacturers' pricing strategies and profitability management.

Opportunities - Smart Tire Technology and Connected Vehicle Ecosystem Integration

The emergence of smart tire technology represents one of the most transformational opportunities for premium tire manufacturers. Smart tires embedded with RFID sensors, pressure monitoring systems, and real-time wear analytics can provide drivers and fleet operators with actionable safety and maintenance data. The integration of smart tires with connected vehicle platforms and autonomous driving systems positions them as essential safety-critical components rather than commodity products.

The U.S. National Highway Traffic Safety Administration (NHTSA) has mandated tire pressure monitoring systems (TPMS) on all new passenger vehicles since 2008, establishing a regulatory foundation for expanded tire sensor integration. Premium manufacturers such as Pirelli & C. S.p.A. have already commercialized Cyber Tyre® technology with embedded sensors, signaling the commercial viability and growing consumer appetite for intelligent tire products in high-performance and luxury segments.

SUV and High-Performance Tire Segment Expansion in Emerging Markets

Rising affluence and rapidly expanding premium vehicle ownership in emerging markets, particularly China, India, the Middle East, and Southeast Asia, are creating a high-growth opportunity for premium tire manufacturers. The China Passenger Car Association (CPCA) reports that premium and luxury vehicle sales in China have grown at double-digit rates, with the country now representing the world's largest single luxury car market by volume.

In India, the Society of Indian Automobile Manufacturers (SIAM) documents consistent above-market growth in SUV and premium vehicle sales. These consumers, often first-time luxury vehicle buyers, are highly receptive to premium tire brand positioning and are less price-sensitive than mature market consumers. Establishing distribution networks, dealer partnerships, and brand awareness in these high-growth markets offers significant revenue expansion potential for established premium tire brands.

Category-wise Analysis

By Vehicle Type Insights

SUVs & Crossovers represent the dominant vehicle type segment in the premium and prestige tire market, commanding approximately 38% of total revenue. The explosive global growth of SUV and crossover vehicles across both premium and mainstream segments has driven unprecedented demand for large-diameter, high-load-rated premium tires.

According to the ACEA, SUVs accounted for over 45% of all new passenger car registrations in Europe in 2023, a trend mirrored across North America, China, and emerging markets. Premium SUVs from brands such as Porsche, Range Rover, and Mercedes-Benz GLE are OEM-fitted with large-diameter (20–23") premium tires, driving substantial revenue per vehicle and positioning SUVs & Crossovers as the market's growth engine.

By Product Construction Insights

Radial Tires dominate the product construction segment with an estimated 72% market share. Radial tire construction, characterized by cord plies arranged perpendicular to the direction of travel, delivers superior ride comfort, fuel efficiency, handling precision, and longevity compared to bias-ply alternatives. These performance attributes are precisely aligned with the expectations of premium vehicle buyers.

The European Tyre & Rubber Manufacturers' Association (ETRMA) confirms that radial tires represent the overwhelming majority of passenger car tire fitments across European markets. All major premium tire manufacturers, including Michelin, Bridgestone Corporation, and Continental AG, have built their premium product portfolios exclusively around radial construction, reinforcing segment dominance.

By Technology Analysis

EV-Specific Tires represent the fastest-growing technology segment, but Low Rolling Resistance Tires currently command the largest technology segment share at approximately 30%, driven by regulatory pressure and consumer demand for improved fuel efficiency across both conventional and electric vehicles.

The European Union's tire labeling regulation (EU) 1222/2009 requires standardized grading of rolling resistance, wet grip, and noise, creating a compliance-driven demand floor for low rolling resistance premium tires. Automakers seeking to meet EU fleet CO2 emission targets and U.S. CAFE standards increasingly specify low rolling resistance premium tires as OEM fitment, ensuring sustained regulatory pull for this technology segment across major global markets.

By Sales Channel Insights

The Aftermarket sales channel represents the dominant revenue stream for premium and prestige tires, accounting for approximately 58% of total market revenue. While OEM fitment is critically important for brand positioning and specification, the replacement cycle, which occurs every 3–5 years depending on driving patterns, generates the majority of commercial volume.

Premium vehicle owners demonstrate significantly higher brand loyalty in tire replacement than standard vehicle owners, tending to repurchase the same brand as their OEM-fitted tire. The Tire Industry Association (TIA) notes that independent tire dealers and franchise retail networks remain the dominant aftermarket distribution channel globally, supplemented by growing online tire retail platforms that are expanding consumer access to premium tire brands.

By End-user Insights

Individual consumers represent the dominant end-user segment, accounting for approximately 62% of the premium and prestige tire market. Luxury and premium vehicle ownership is predominantly individual consumer-driven, and these buyers exhibit strong preferences for branded, performance-certified tires backed by OEM endorsement.

Brand loyalty is significantly higher among premium vehicle consumers than in the mass market: studies by automotive consumer intelligence firms and OEM dealer networks consistently show that owners of brands such as BMW, Audi, and Porsche are highly likely to request OEM-recommended tire brands at replacement. This brand loyalty dynamic creates a durable, recurring revenue base that reinforces individual consumer dominance in the premium tire market.

Regional Insights

North America Premium and Prestige Tire Market Trends & Analysis

North America represents a mature yet high-value premium tire market, driven by strong SUV and performance vehicle penetration. OEM partnerships and EV-specific tire innovation are accelerating growth. Regulatory mandates such as TPMS ensure consistent replacement demand, while high consumer purchasing power sustains premiumization trends across both OEM and aftermarket segments.

- U.S. Premium and Prestige Tire Market Size

The U.S. dominates the regional market, accounting for approximately USD 14.5 Billion in 2026, supported by over 300 million annual tire shipments. Strong luxury vehicle sales, expanding EV adoption, and large-diameter tire demand position the U.S. as a key revenue generator, with steady replacement cycles sustaining long-term growth.

Europe Premium and Prestige Tire Market Trends, Drivers & Insights

Europe remains the global hub for premium tire manufacturing, supported by a strong luxury automotive OEM base and strict regulatory frameworks. EU tire labeling and sustainability mandates are driving demand for high-performance, low rolling resistance tires. Strong brand loyalty and OEM-fitment alignment further reinforce premium segment dominance.

- Germany Premium and Prestige Tire Market Size

Germany leads Europe with an estimated USD 6.2 Billion in 2026, driven by its dense concentration of luxury OEMs and strong export-oriented automotive production. High demand for OEM-fit premium tires and technological leadership in performance mobility sustain market growth.

- U.K. Premium and Prestige Tire Market Size

The U.K. market is valued at approximately USD 3.4 Billion in 2026, supported by a strong luxury vehicle parc and replacement demand. Premium tire adoption is driven by consumer preference for branded, high-performance products and increasing EV penetration.

- France Premium and Prestige Tire Market Size

France accounts for around USD 3.2 Billion in 2026, with growth driven by regulatory compliance, sustainable mobility initiatives, and strong replacement market demand. Premium tire penetration is supported by OEM recommendations and consumer emphasis on safety and efficiency.

Asia Pacific Premium and Prestige Tire Market Drivers & Analysis

Asia Pacific is the fastest-growing region, driven by rising affluence, luxury vehicle sales, and expanding OEM manufacturing. China leads in volume, while Japan drives innovation and India emerges as a high-growth market. Increasing EV adoption and premium vehicle imports are reshaping demand across the region.

- China Premium and Prestige Tire Market Size

China dominates globally with an estimated USD 13.0 billion in 2026, fueled by rapid luxury vehicle sales and domestic OEM production. Strong demand for OEM-fit premium tires and expanding high-income consumer base are key growth drivers.

- India Premium and Prestige Tire Market Size

India’s market ecosystem is projected at USD 3.0 billion in 2026, supported by rising disposable income, luxury vehicle penetration, and urbanization. Growth is primarily driven by replacement demand and increasing presence of global OEMs.

- Japan Premium and Prestige Tire Market Size

Japan holds a market size of approximately USD 4.5 billion in 2026, characterized by advanced tire technology and strong domestic manufacturers. Innovation in EV-specific and smart tires continues to support premium segment expansion.

Competitive Landscape

The global Premium and Prestige Tire market is moderately consolidated, with a ‘Big Three’ of Michelin, Bridgestone Corporation, and Continental AG collectively accounting for a significant share of global premium tire revenue. Key differentiators include OEM qualification credentials, proprietary compound and construction technology, motorsport heritage (particularly for Pirelli & C. S.p.A. and Michelin), and sustainability credentials in low rolling resistance and green compound development.

Emerging business models include tire-as-a-service (TaaS) for fleet operators, digital tire monitoring subscriptions, and circular economy programs for used premium tires. Asian challengers, notably Hankook Tire & Technology and Nokian Tyres, are aggressively pursuing OEM qualifications to break into premium fitment specifications.

Key Developments:

- January, 2025: Michelin announced the commercial launch of its Uptis (Unique Puncture-proof Tire System) airless tire technology for passenger vehicles, targeting premium and fleet segments with zero puncture risk and extended service life.

- March, 2024: Pirelli & C. S.p.A. unveiled its new Cyber Tyre®-enabled P Zero range featuring embedded sensors compatible with BMW and Ferrari OEM connected vehicle systems, reinforcing its position in the ultra-premium performance tire segment.

- September, 2023: Continental AG launched its UltraContact NXT tire, the company's first premium tire incorporating 65% sustainable materials, targeting European OEMs committed to lifecycle sustainability targets under the EU Green Deal framework.

Global Premium and Prestige Tire Market- Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 28.7 Bn |

|

Current Market Value (2026) |

US$ 39.8 Bn |

|

Projected Market Value (2033) |

US$ 61.0 Bn |

|

CAGR (2026-2033) |

6.3% |

|

Leading Region |

Europe, 38% share |

|

Dominant Vehicle Type |

SUVs & Crossovers, 38% share |

|

Top-ranking End User |

Individual Consumers, 62% |

|

Incremental Opportunity |

US$ 5.1 Bn |

Companies Covered in Premium and Prestige Tire Market

- Michelin

- Bridgestone Corporation

- Continental AG

- Goodyear Tire & Rubber Company

- Pirelli & C. S.p.A.

- Hankook Tire & Technology

- Yokohama Rubber Company

- Sumitomo Rubber Industries

- Toyo Tire Corporation

- Kumho Tire

- Nokian Tyres

- Apollo Tyres

- Cooper Tire & Rubber Company

- Maxxis International

- Nexen Tire Corporation

- Giti Tire

- Falken Tire Corporation

- Vredestein

Frequently Asked Questions

The global Premium and Prestige Tire market is estimated at US$ 39.8 Billion in 2026 and is forecast to reach US$ 61.0 Billion by 2033, growing at a CAGR of 6.3% over the forecast period. The market delivered an exceptional historical CAGR of 20.6% from 2020 to 2025, driven by rapid luxury vehicle growth, EV adoption, and strong consumer premiumization trends globally.

The primary growth drivers are the global expansion of luxury and premium vehicle sales, with SUVs and crossovers growing fastest, and the rapid adoption of electric vehicles, which require specialized EV-specific tires featuring reinforced sidewalls, low rolling resistance compounds, and acoustic insulation. IEA data confirms over 14 million EV units sold globally in 2023, directly expanding the premium EV tire specification market.

SUVs & Crossovers represent the dominant vehicle type segment with approximately 38% market share. The explosive global growth of premium SUV models from brands such as Porsche, Range Rover, and Mercedes-Benz GLE, with OEM-specified large-diameter tires of 20 to 23 inches, drives substantial per-vehicle tire revenue and positions this segment as the market's primary growth engine.

Europe is the leading region in the Premium and Prestige Tire market, anchored by its world-class automotive OEM base including BMW Group, Mercedes-Benz Group, Volkswagen Group, and Stellantis. EU regulatory frameworks, including tire labeling regulations and forthcoming Euro 7 emission standards, further drive demand for high-rated premium tires, making Europe a structurally dominant and innovation-leading market.

The most significant opportunities are in smart tire technology, integrating embedded sensors and connected vehicle platforms for real-time monitoring, and in capturing the rapidly growing SUV and luxury vehicle premium tier in Asia Pacific markets, particularly China and India, where double-digit luxury vehicle sales growth is creating large new consumer bases for premium tire brands.

Leading companies in the global Premium and Prestige Tire market include Michelin, Bridgestone Corporation, Continental AG, Goodyear Tire & Rubber Company, Pirelli & C. S.p.A., Hankook Tire & Technology, Yokohama Rubber Company, Sumitomo Rubber Industries, Toyo Tire Corporation, Kumho Tire, Nokian Tyres, Apollo Tyres, Cooper Tire & Rubber Company, Maxxis International, and Nexen Tire Corporation, among others.