- Automotive Components & Materials

- Last Mile Delivery Tires Market

Last Mile Delivery Tires Market Size, Share, and Growth Forecast 2026 - 2033

Last Mile Delivery Tires Market by Vehicle Type (Delivery Vans, Pickup Trucks, Mini-Trucks & LCVs, Electric Delivery Vehicles, Two-Wheelers & Scooters), Tire Type (Tubeless Tires, Tube-Type Tires, Run-Flat Tires, All-Season Tires, Urban Specialized Tires), Application, Distribution Channel, End-user, and Regional Analysis, 2026 - 2033

Last Mile Delivery Tires Market Size and Trend Analysis

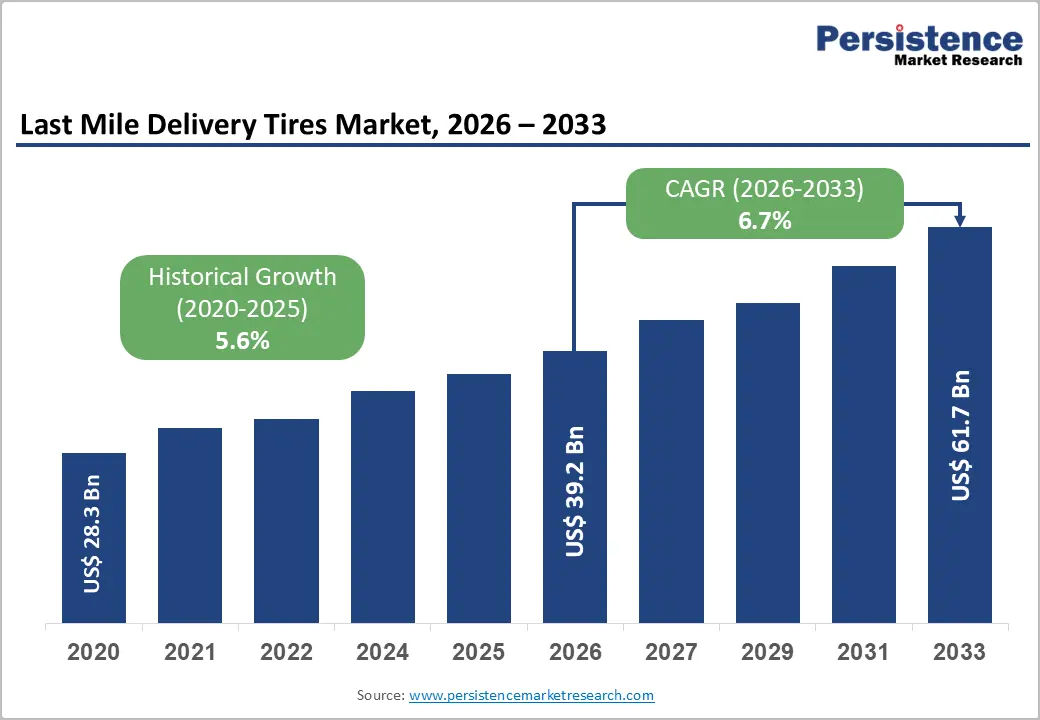

The global last-mile delivery tire market size is likely to be valued at US$ 39.2 billion in 2026 and is expected to reach US$ 61.7 billion by 2033, growing at a CAGR of 6.7% during the forecast period from 2026 to 2033. The last-mile delivery tires market is expanding at an accelerating pace, driven by the explosive global growth of e-commerce, the rapid electrification of urban delivery fleets, and intensifying consumer demand for same-day and next-day delivery services.

Key Industry Highlights:

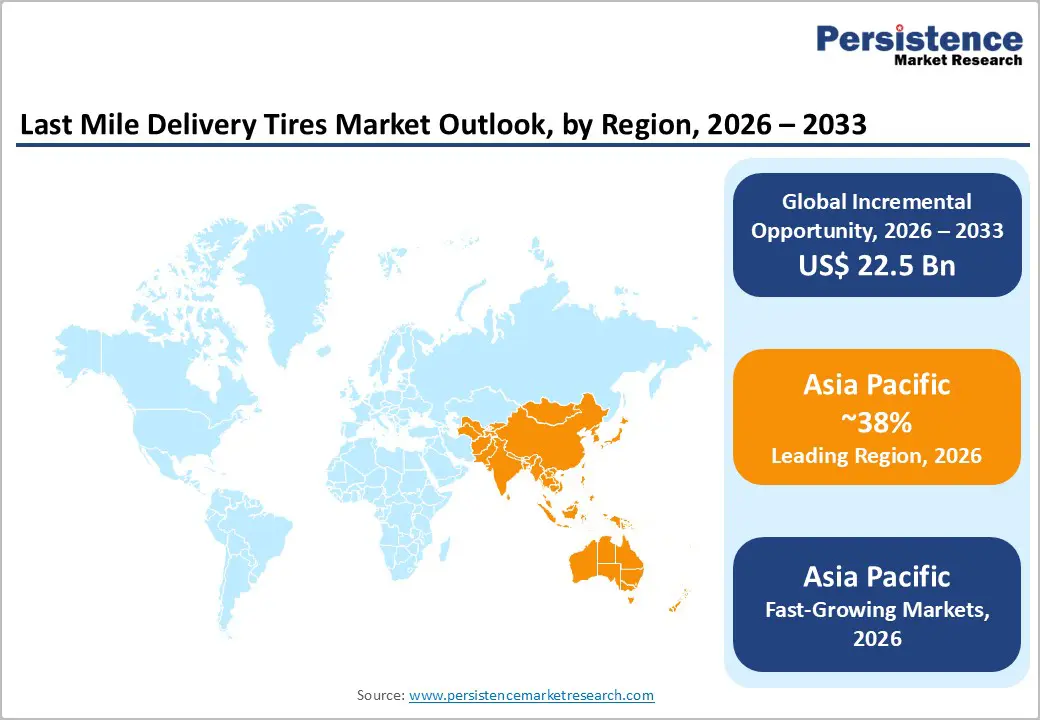

- Leading Region: Asia Pacific leads the global last-mile delivery tire market, holding 38% share, driven by China's 130+ billion annual parcel volumes, India's booming two-wheeler delivery ecosystem, and rapid e-commerce logistics expansion across ASEAN nations.

- Fastest-Growing Region: Asia Pacific is also the fastest-growing region, with India's delivery platforms, China's adoption of electric LCVs, and Southeast Asian logistics growth collectively driving the highest incremental tire demand globally through 2033.

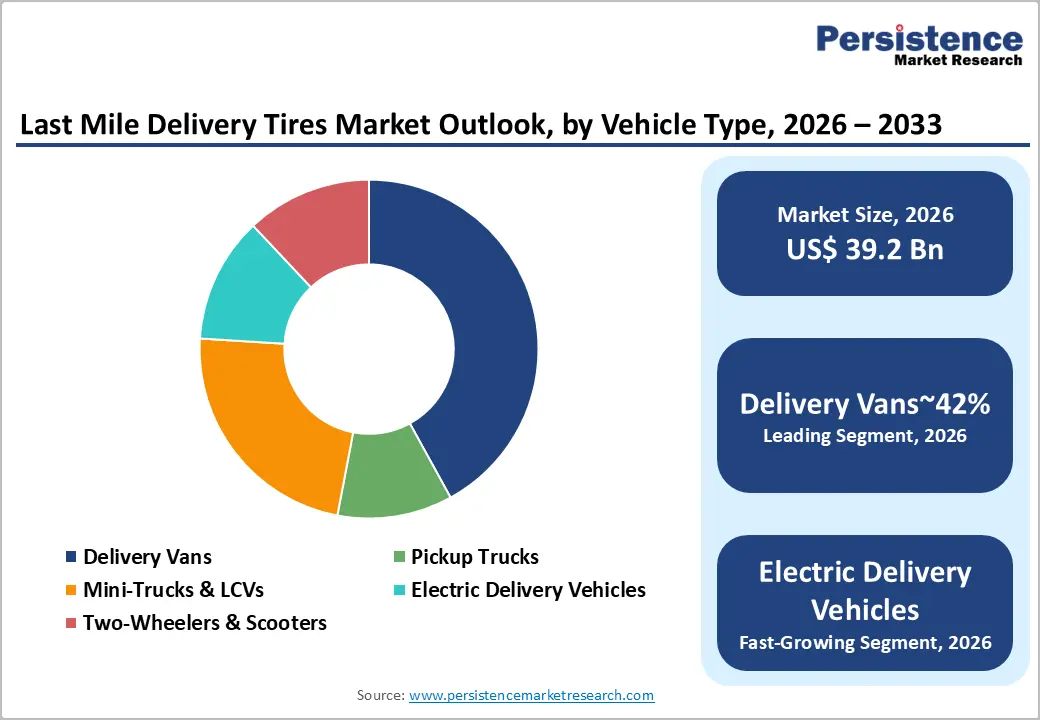

- Dominant Segment (By Vehicle Type): Delivery Vans lead with approximately 42% market share, as the primary workhorse vehicle for parcel, e-commerce, and grocery delivery fleets operated by Amazon, UPS, FedEx, and DHL across global markets.

- Fastest-Growing Segment (By Vehicle Type): Electric Delivery Vehicles are the fastest-growing

- segment, as major logistics operators commit to fleet electrification under regulatory and ESG pressure, driving demand for specialized EDV-optimized tire formulations.

- Key Opportunity: Smart tire technology integrated with fleet telematics, enabling real-time monitoring and tire-as-a-service business models, offers premium manufacturers a path to recurring revenue and deeper relationships with large-scale last-mile fleet operators.

Market Dynamics

Drivers - Global E-commerce Boom and Surge in Parcel Delivery Volume

The relentless expansion of global e-commerce is the most powerful structural driver of the last-mile delivery tire market. As online retail continues to capture share from physical stores, parcel volumes are growing at unprecedented rates, requiring larger, more intensively utilized delivery vehicle fleets. The International Post Corporation (IPC) reports that global parcel volumes have grown by over 40% since 2019, with same-day and next-day delivery services driving especially high vehicle utilization rates.

Delivery vans and light commercial vehicles in urban last-mile operations can cover 150–300 kilometers per day across multiple stops, creating tire wear patterns that sharply reduce service life compared to long-haul applications. This high replacement frequency, multiplied across millions of fleet vehicles, generates a structurally elevated and recurring demand base for specialized last-mile delivery tires.

Rapid Electrification of Urban Delivery Fleets and EDV-Specific Tire Demand

The accelerating transition to electric delivery vehicles (EDVs) in urban last mile logistics is creating a compelling new tier of tire demand with distinct performance requirements. Major logistics operators, including Amazon, UPS, FedEx, and DHL, have committed to electrifying significant proportions of their delivery fleets. The International Energy Agency (IEA) reports that electric LCVs and delivery vans are among the fastest-growing EV segments globally.

Electric delivery vehicles impose higher torque loads at takeoff, carry greater curb weights, and require tires optimized for low rolling resistance to maximize range. These unique operational demands necessitate EDV-specific tire formulations commanding premium price points, directly expanding revenue per vehicle in the last-mile delivery tire market.

Restraints - Intense Price Competition from Low-Cost Tire Manufacturers

Fleet operators managing large delivery vehicle pools are acutely cost-conscious, creating persistent downward pricing pressure in the last-mile delivery tire market. Procurement managers at logistics companies typically seek the lowest cost-per-kilometer metric, which frequently favors established mid-tier or economy Asian tire brands over premium-specification alternatives.

The European Tire & Rubber Manufacturers' Association (ETRMA) notes that price sensitivity is particularly pronounced among third-party logistics providers (3PLs) and gig-economy delivery operators, maintaining thin margins, limiting premium tire penetration in fleet replacement channels.

Urban Traffic Congestion and Stop-Start Driving Patterns Accelerating Tire Wear

Last-mile delivery tires face uniquely punishing operating conditions in dense urban environments: constant acceleration and braking, tight turns, curb mounting, and road surface variability dramatically shorten tire service life compared to highway applications.

Research by the Tire Industry Association (TIA) indicates that urban commercial vehicle tires can wear out 2–3 times faster than equivalent long-haul tires. While this accelerates replacement frequency, it also increases the total cost of ownership for fleet operators, prompting procurement decisions that may prioritize lower-cost alternatives over performance-optimized tires, constraining margin potential for premium manufacturers.

Opportunities - Electric Two-Wheeler and Cargo Bike Tire Segment for Urban Micro-Mobility Delivery

The explosive growth of electric two-wheelers, cargo bikes, and micro-mobility delivery platforms in urban last mile logistics is creating a high-growth specialty tire segment with limited existing competition from established fleet tire manufacturers. Cities across Europe and Asia are actively promoting cargo bike and e-scooter deliveries as low-emission alternatives in dense urban areas, with municipalities such as Amsterdam, Paris, and Tokyo providing regulatory support and infrastructure.

The European Cyclists' Federation estimates that cargo bikes could replace up to 51% of all motorized urban freight trips. Tire manufacturers that develop purpose-designed urban cargo tire solutions, balancing puncture resistance, grip, and durability on mixed urban surfaces, can capture first-mover advantage in this emerging, volume-growing segment before major competitors standardize offerings.

Smart Tire Technology for Fleet Telematics and Predictive Maintenance Integration

The integration of smart tire technology, featuring embedded sensors for real-time pressure, temperature, and wear monitoring, with fleet telematics platforms, represents a transformational opportunity for tire manufacturers serving last-mile delivery operators. Fleet managers operating hundreds or thousands of vehicles face significant challenges in monitoring tire health across distributed networks; smart tires providing continuous data feeds directly address this pain point.

The U.S. National Highway Traffic Safety Administration (NHTSA) mandated TPMS on all light vehicles since 2008, establishing a regulatory and technical foundation for expanded sensor integration. Companies, including Michelin and Bridgestone Corporation, are actively developing connected tire solutions for commercial fleet applications. Smart tire subscriptions and tire-as-a-service (TaaS) business models, where operators pay per kilometer rather than per unit, offer premium manufacturers a path to recurring revenue and deeper fleet relationships that transcend the transactional replacement tire market.

Category-wise Analysis

By Vehicle Type Insights

Delivery Vans represent the dominant vehicle type segment in the last mile delivery tires market, accounting for approximately 42% of total revenue. Delivery vans remain the workhorse of urban and suburban last mile logistics, deployed by every major parcel carrier, grocery delivery operator, and courier network globally.

Operators, including Amazon Logistics, UPS, and DHL, collectively operate millions of delivery vans, each requiring four tires with replacement cycles driven by intensive urban use. The transition of van fleets to electric platforms, particularly through vehicles like the Mercedes-Benz eSprinter and Ford E-Transit, is further evolving tire specifications, maintaining delivery vans' market-leading position while adding EV-specific performance dimensions.

By Tire Type Insights

Tubeless Tires dominate the tire type segment, accounting for approximately 55% of the last-mile delivery tire market. Tubeless technology has become the standard fitment for virtually all modern commercial delivery vehicles due to its superior safety profile, reduced risk of sudden deflation, lower unsprung weight, and easier maintenance compared to tube-type alternatives.

Fleet operators particularly value tubeless tires for their ability to be temporarily repaired roadside using sealant plugs, reducing costly vehicle downtime in urban delivery schedules. The European Tire & Rubber Manufacturers' Association (ETRMA) confirms that tubeless tires represent the overwhelming majority of new commercial vehicle tire fitments across European markets, a pattern mirrored globally as vehicle manufacturers standardize on tubeless construction across van and LCV platforms.

By Application Insights

E-commerce Logistics is the leading application segment, representing approximately 35% of the last-mile delivery tires market. The structural growth of online retail, now accounting for approximately 20% of total global retail sales according to UNCTAD, generates the highest volume and frequency of last mile deliveries of any application segment.

E-commerce deliveries are characterized by high stop frequency, diverse package weights, and intensive urban routing, which create accelerated tire wear patterns relative to conventional distribution. The continued growth of online marketplaces, particularly Amazon, Alibaba, and Flipkart, and their expanding proprietary delivery networks ensures that e-commerce logistics will maintain its market-leading application segment position throughout the forecast period.

By Distribution Channel Insights

The Aftermarket distribution channel dominates the last-mile delivery tires market, accounting for approximately 65% of total revenue. Fleet operators replacing worn tires across large vehicle pools drive the majority of last mile delivery tire procurement through aftermarket channels, including tire dealers, fleet service providers, online tire retailers, and direct manufacturer programs.

The high replacement frequency inherent in urban delivery operations, with van and LCV tires often requiring replacement every 40,000–60,000 kilometers under intensive urban duty cycles, creates a consistent, recurring aftermarket revenue stream. The Tire Industry Association (TIA) notes that fleet tire management programs, offering consolidated procurement, mobile fitting, and digital fleet tracking, are growing rapidly as large fleet operators seek to streamline tire lifecycle management.

By End-user Insights

Logistics companies represent the largest end-user segment, commanding approximately 38% of the last-mile delivery tires market. Integrated logistics operators, including DHL, FedEx, UPS, and DB Schenker, operate the world's largest proprietary delivery vehicle fleets, generating the highest absolute volumes of tire procurement.

These operators run centralized fleet maintenance programs that create concentrated, predictable, and high-volume tire purchasing cycles highly attractive to both premium and mid-tier tire manufacturers. The ongoing fleet electrification commitments of major logistics companies are also shifting tire specifications toward EDV-optimized products, increasing average selling prices and creating incremental revenue opportunities within this dominant end-user segment.

Regional Insights

North America Last Mile Delivery Tires Market Trends & Analysis

North America represents a high-value, replacement-driven market supported by advanced logistics infrastructure and strong e-commerce penetration. The region accounts for approximately 28% of global market share in 2026, ~US$ 11.5 billion, driven by high fleet utilization, suburban delivery density, and increasing electric delivery van adoption.

- U.S. Last Mile Delivery Tires Market Size

The U.S. dominates the regional market with an estimated ~US$ 9.5 billion in 2026, representing over 85% of North America. Strong parcel volumes exceeding 20 billion annually and rapid electrification of delivery fleets are sustaining high replacement tire demand and accelerating adoption of EV-optimized tires.

Europe Last Mile Delivery Tires Market Trends, Drivers & Insights

Europe is a mature and regulation-driven market, accounting for approximately 24% of the global share, ~US$ 9.5 billion in 2026. Growth is fueled by urban logistics density, sustainability mandates, and the rapid adoption of low-rolling-resistance tires aligned with the efficiency requirements of electric delivery vehicles.

- Germany Last Mile Delivery Tires Market Size

Germany leads Europe with an estimated ~US$ 2.4 billion in 2026, supported by its strong logistics backbone and dense urban delivery networks. High adoption of fleet electrification and premium tire technologies is shaping demand.

- U.K. Last Mile Delivery Tires Market Size

The U.K. market is valued at approximately ~US$ 1.8 billion in 2026, driven by rapid e-commerce growth and strict urban emission regulations, particularly in London’s low-emission zones, boosting demand for EV-compatible tires.

- France Last Mile Delivery Tires Market Size

France is estimated at ~US$ 1.8 billion in 2026, supported by strong parcel growth and regulatory push toward sustainable logistics. Urban delivery modernization and electrification are key contributors to tire replacement cycles.

Asia Pacific Last Mile Delivery Tires Market Drivers & Analysis

Asia Pacific is the largest and fastest-growing region, accounting for approximately 38% of global market ~US$ 16.5 billion in 2026. Growth is driven by massive parcel volumes, expanding delivery ecosystems, and a high reliance on two-wheelers and light commercial vehicles, leading to frequent tire replacements.

- China Last Mile Delivery Tires Market Size

China leads globally with an estimated ~US$ 9.8 billion in 2026, supported by over 130 billion annual parcel deliveries. High fleet turnover and dominance of domestic tire manufacturers drive strong volume demand.

- India Last Mile Delivery Tires Market Size

India is valued at approximately ~US$ 2.2 billion in 2026, driven by the rapid expansion of e-commerce and food delivery platforms. The dominance of two-wheelers creates a high-frequency replacement market, accelerating overall tire consumption.

- Japan Last Mile Delivery Tires Market Size

Japan’s market is estimated at ~US$ 1.5 billion in 2026, characterized by advanced urban logistics systems and growing adoption of electric delivery fleets. Demand is focused on premium, durable, and fuel-efficient tire solutions.

Competitive Landscape

The global last-mile delivery tire market is moderately consolidated at the premium tier, with Michelin, Bridgestone Corporation, and Continental AG commanding significant market share through fleet qualification programs, OEM relationships, and proprietary commercial tire technology.

Key differentiators include EDV-optimized tire compounds, integrated fleet telematics compatibility, and tire-as-a-service (TaaS) business models. Asian manufacturers, including Zhongce Rubber Group, Giti Tire, and Maxxis International, compete aggressively on price across mid-tier fleet segments. Emerging trends include smart tire subscriptions, mobile fleet fitting services, and digital tire lifecycle platforms targeting large-scale last mile operators.

Key Developments:

- March, 2025: Michelin launched its X MULTI ENERGY Z tire line specifically designed for electric light commercial vehicles and delivery vans, offering optimized load capacity, low rolling resistance, and reduced road noise for urban fleet operations.

- November, 2024: Bridgestone Corporation expanded its Tirematics connected tire solution to cover delivery van fleets across Europe, enabling real-time pressure and wear monitoring integrated with fleet management systems for major logistics operators.

- June, 2023: Continental AG introduced its Conti.eContact urban commercial tire range, purpose-engineered for electric delivery vehicles and micro-mobility platforms operating in dense European city environments with low-emission zone restrictions.

Companies Covered in Last Mile Delivery Tires Market

- Michelin

- Bridgestone Corporation

- The Goodyear Tire & Rubber Company

- Continental AG

- Pirelli & C. S.p.A.

- Sumitomo Rubber Industries

- Hankook Tire & Technology

- Yokohama Rubber Company

- Toyo Tire Corporation

- Kumho Tire

- Apollo Tyres Ltd.

- MRF Tyres

- Maxxis International

- Giti Tire

- Zhongce Rubber Group

- Nokian Tyres

- Sailun Group

- Triangle Tire Co., Ltd.

Frequently Asked Questions

The global last mile delivery tires market is valued at US$ 39.2 Billion in 2026 and is projected to reach US$ 61.7 Billion by 2033, at a CAGR of 6.7% during the forecast period. Historically, the market expanded at a CAGR of 5.6% from 2020 to 2025, driven by surging e-commerce parcel volumes and the rapid expansion of dedicated last mile delivery vehicle fleets globally.

The primary growth drivers are the global e-commerce boom, with UNCTAD reporting annual sales exceeding US$ 5.8 trillion, generating unprecedented parcel delivery volumes, and the rapid electrification of urban delivery fleets by major operators including Amazon, UPS, FedEx, and DHL. Electric delivery vehicles require specialized tire formulations for higher torque loads, greater curb weight, and range optimization, creating a premium-priced, fast-growing market sub-segment.

Delivery Vans represent the dominant vehicle type segment with approximately 42% market share. Vans are the primary last mile delivery vehicle for all major global logistics operators, generating the highest absolute tire volumes. The ongoing transition of van fleets to electric platforms, including Mercedes-Benz eSprinter and Ford E-Transit, is further evolving tire specifications while maintaining the van segment's leadership position.

Asia Pacific is the largest regional market, led by China's world-leading parcel volume of over 130 billion annual deliveries as reported by the State Post Bureau of China, and India's rapidly expanding two-wheeler and LCV delivery ecosystem. The region's manufacturing cost advantages, large domestic fleet base, and rapidly growing e-commerce penetration across ASEAN nations collectively ensure Asia Pacific's market leadership through 2033.

The most significant opportunities are in smart tire technology integrated with fleet telematics, enabling real-time monitoring and tire-as-a-service (TaaS) business models, and in purpose-designed tires for electric two-wheelers and cargo bikes serving urban micro-mobility delivery. The European Cyclists' Federation estimates cargo bikes could replace up to 51% of motorized urban freight trips, signaling a high-growth emerging segment for specialty urban delivery tire manufacturers.

Leading companies in the global Last Mile Delivery Tires market include Michelin, Bridgestone Corporation, The Goodyear Tire & Rubber Company, Continental AG, Pirelli & C. S.p.A., Sumitomo Rubber Industries, Hankook Tire & Technology, Yokohama Rubber Company, Toyo Tire Corporation, Kumho Tire, Apollo Tyres Ltd., MRF Tyres, Maxxis International, Giti Tire, and Zhongce Rubber Group, among others.