- Healthcare Services

- ePharmacy Market

ePharmacy Market Size, Share, and Growth Forecast 2026 - 2033

ePharmacy Market by Product Type (Prescription Medicines, Over-the-Counter (OTC) Medicines, Health & Wellness Products, Others), by Pharmacy Size (Large ePharmacies, Medium ePharmacies, Small ePharmacies), by Regional Analysis, 2026 - 2033

ePharmacy Market Size and Share Analysis

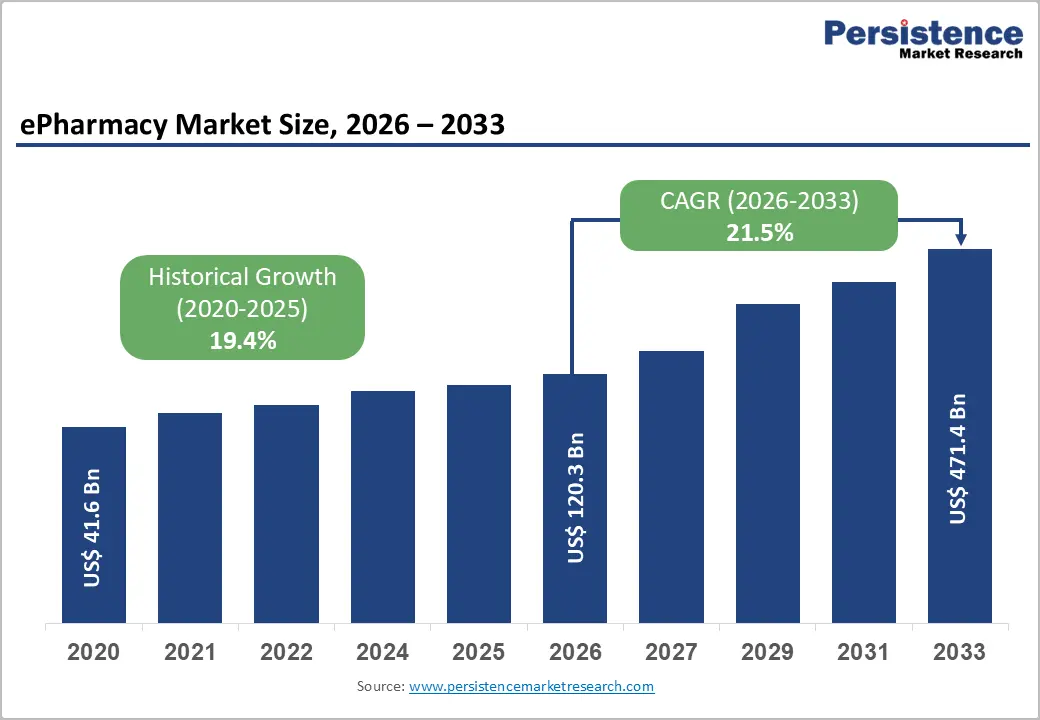

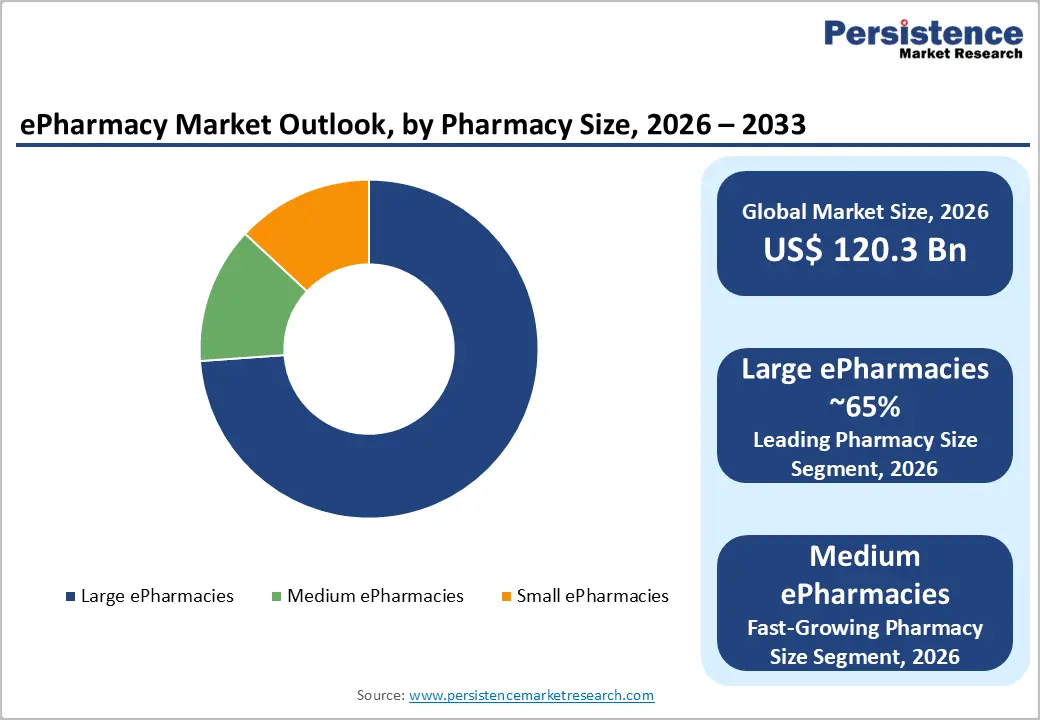

The global ePharmacy market size is expected to be valued at US$ 120.3 billion in 2026 and projected to reach US$ 471.4 billion by 2033, growing at a CAGR of 21.5% between 2026 and 2033.

The market is expanding due to rising digital health adoption and consumer preference for convenient medicine delivery. Supportive factors include smartphone penetration exceeding 5 billion users globally and the prevalence of chronic disease affecting 1.9 billion adults, driving online procurement. Post-pandemic e-commerce shifts and telemedicine integration further accelerate growth by enabling seamless e-prescriptions and home delivery.

Key Industry Highlights

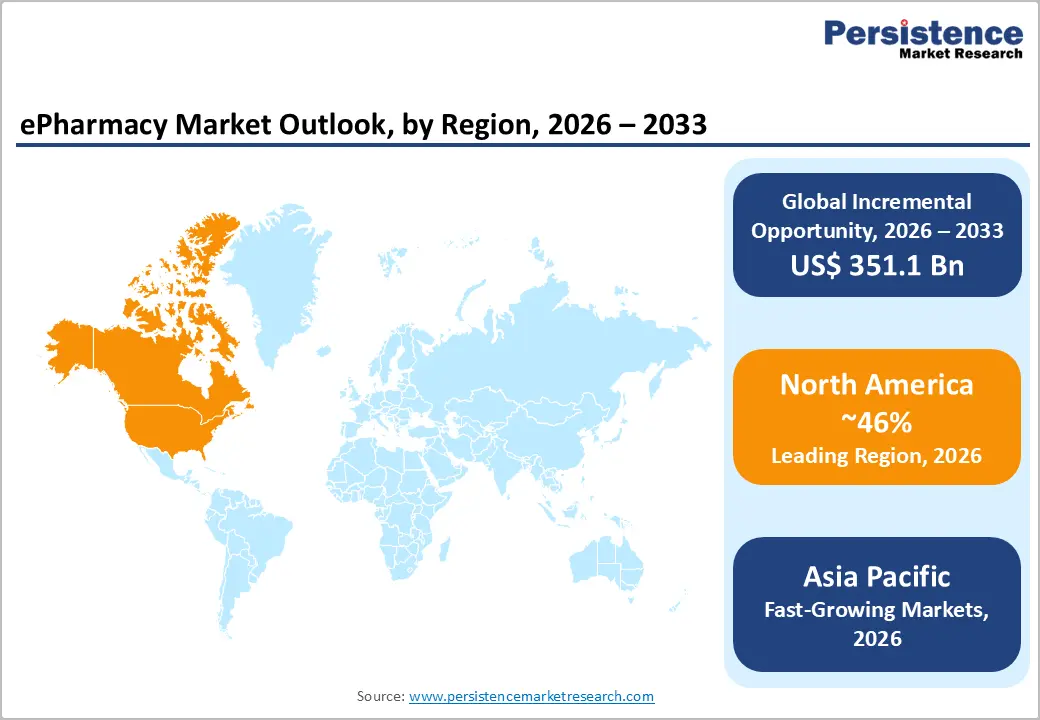

- Leading Region: North America leads the global ePharmacy market, supported by strong digital infrastructure, high e-prescription adoption, favorable reimbursement policies, and mature logistics networks.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising internet penetration, expanding telemedicine use, supportive government digital health initiatives, and large underserved populations in India and Southeast Asia.

- Dominant Segment: Prescription medicines remain the dominant segment, driven by the prevalence of chronic diseases, repeat-refill demand, teleconsultation-led e-prescriptions, and regulatory-backed authentication systems.

- Fastest-Growing Segment: OTC medicines and wellness products are the fastest-growing segment due to rising self-medication trends, growing preventive healthcare awareness, and convenient home delivery models.

| Key Insights | Details |

|---|---|

|

ePharmacy Size (2026E) |

US$ 120.3 billion |

|

Market Value Forecast (2033F) |

US$ 471.4 billion |

|

Projected Growth CAGR (2026-2033) |

21.5% |

|

Historical Market Growth (2020-2025) |

19.4% |

Market Dynamics

Driver - Rising Digital Connectivity, Supportive Government Initiatives, and Healthcare Spending Growth Driving ePharmacy Market Expansion

The key factor driving the growth of the ePharmacy market is increasing internet penetration. Around 62.5% of the global population has internet access, which is likely to swell significantly in the near future. For instance, the digital initiatives the government and the Ministry of Health & Family Welfare of India have undertaken to improve the efficiency and effectiveness of the public healthcare system, such as the National Health Portal, Online registration system, e-hospital@NIC, and the Central Drugs Standards Control Organization (SUGAM) have propagated the healthcare infrastructure in India.

The Union Cabinet of India approved amending the existing FDI law in the pharmaceutical sector to allow 100% FDI, making FDI up to this amount permissible for the production of medical devices under certain conditions. This helps India maintain a continuous pipeline of drugs and streamline the production of life-saving medicines.

Medical expenditures for people are projected to rise at a 3.6-6% CAGR between 2022 and 2025, reaching approximately US$ 1.6 trillion, driven by rising consumer spending, rapid urbanization, the rise of noncommunicable diseases, and progressively increasing medical insurance, among others.

Restraints - Stringent Regulatory Compliance Burdens

The ePharmacy market faces significant restraints due to stringent and fragmented regulatory compliance requirements across regions. Regulatory authorities have increased scrutiny of online pharmacy platforms to curb illegal drug sales and protect patient safety. For instance, regulatory actions, such as the FDA warnings issued in May 2024 against unauthorized platforms, highlight the need for strict licensing, valid e-prescription verification, and robust pharmacovigilance systems. These requirements often delay market entry and increase operational complexity, particularly for new and smaller players. Additionally, varying national and regional regulations create challenges for cross-border ePharmacy operations. In Europe, restrictions on online prescription drug advertising under the E-Commerce Directive further limit growth opportunities. Compliance with data protection frameworks such as HIPAA and GDPR has also increased operational costs by an estimated 15–20%, driven by investments in cybersecurity, encryption, and data governance. Collectively, these regulatory burdens reduce scalability, slow innovation, and discourage small and mid-sized companies from expanding, while ongoing concerns about counterfeit medicines continue to impact consumer trust and market adoption.

Opportunity - Data Security and Counterfeit Drug Concerns

Growing concerns around data security and counterfeit drugs present a critical opportunity for the ePharmacy market to strengthen credibility and long-term growth. Cyber threats and large-scale data breaches that expose nearly 700 million healthcare records annually have heightened awareness of patient data protection and secure digital transactions. At the same time, the presence of unauthorized online pharmacies selling unapproved or substandard medicines has prompted regulatory crackdowns, including FDA actions against more than 100 websites in 2024. An estimated 10% penetration of counterfeit drugs in online channels underscores the urgent need for standardized verification systems, secure supply chains, and transparent sourcing. EPharmacy platforms that invest in advanced cybersecurity solutions, blockchain-based drug traceability, AI-driven prescription validation, and regulatory-aligned compliance frameworks can differentiate themselves and rebuild consumer confidence. By proactively addressing safety, authenticity, and data protection concerns, ePharmacies can position themselves as trusted healthcare partners. This creates opportunities for premium services, stronger partnerships with regulators and manufacturers, and increased adoption among risk-averse consumers seeking convenience without compromising safety.

Category-wise Analysis

Product Type Analysis

Prescription medicines dominated the ePharmacy market, with an estimated 45% share in 2025, primarily driven by the rapid expansion of telemedicine and digital prescribing practices. The growing acceptance of e-prescriptions, supported by regulatory authorities and healthcare providers, has significantly increased online prescription volumes, particularly in developed markets. Chronic disease management plays a central role in this dominance, as patients with conditions such as diabetes, cardiovascular disorders, and respiratory diseases require regular and repeat medication refills.

EPharmacy platforms offer convenience, adherence support, and automated refill reminders, making them a preferred channel for long-term therapies. Integration with electronic health records and teleconsultation platforms enables seamless prescription validation and fulfillment, ensuring compliance and authenticity. Compared with OTC products, prescription medicines benefit from higher order values, repeat-purchase behavior, and stronger regulatory trust. A large proportion of chronic users consistently rely on online platforms, driving sustained demand and reinforcing the leadership of prescription medicines within the ePharmacy product mix.

Pharmacy Size Analysis

Large ePharmacies accounted for approximately 65% of the global ePharmacy market share in 2025, supported by their extensive operational scale and advanced infrastructure. These players benefit from nationwide logistics networks, centralized warehouses with temperature-controlled storage, and integrated supply chains that enable faster and more reliable order fulfillment. Their strong partnerships with insurers, healthcare providers, and diagnostic platforms allow seamless processing of online prescriptions and reimbursements, improving customer retention.

Advanced technologies such as AI-driven demand forecasting, inventory optimization, and automated dispensing further enhance efficiency and reduce delivery timelines, often enabling same-day or near-instant delivery in urban areas.

Additionally, large ePharmacies invest heavily in compliance systems, cybersecurity measures, and customer engagement tools to ensure regulatory adherence and trust. In contrast, small and medium platforms often face limitations related to capital, reach, and compliance costs. These structural advantages continue to reinforce the dominance of large ePharmacies across mature and high-volume markets.

Region-wise Insights

North America ePharmacy Market Trends

North America remains the most mature and revenue-generating ePharmacy market globally, with the United States accounting for the majority share. Market growth is supported by high healthcare spending, strong digital adoption, and an increasing number of hospital admissions requiring long-term medication therapy. Favorable Medicare and private insurance reimbursement policies have significantly improved patient access to online prescription fulfillment, particularly for chronic and specialty drugs.

The region has also benefited from the widespread use of electronic prescriptions and integrated healthcare systems, enabling seamless coordination between physicians, pharmacies, and payers. Large pharmacy networks with omnichannel capabilities have expanded rapidly, combining physical retail presence with digital platforms to enhance convenience and delivery speed. Specialty pharmacy services have gained traction due to the rising prevalence of complex conditions, including oncology and autoimmune diseases tretment. Overall, strong regulatory oversight, established logistics infrastructure, and payer integration continue to reinforce North America’s leadership in the ePharmacy landscape.

Asia and Pacific ePharmacy Market Trends

The Asia Pacific ePharmacy market is witnessing rapid expansion, driven by rising internet penetration, growing smartphone usage, and increasing demand for accessible healthcare services. Large populations, coupled with a rising burden of chronic diseases and expanding middle-class incomes, are accelerating the shift toward online purchasing of medicine. Governments across the region are investing in digital health initiatives to improve healthcare delivery, particularly in densely populated and semi-urban areas.

Growth is further supported by improvements in logistics networks and partnerships among ePharmacy platforms, hospitals, and teleconsultation providers. Consumers are increasingly adopting ePharmacy services due to competitive pricing, home delivery, and access to a wider range of medicines. While regulatory frameworks continue to evolve, greater clarity and oversight are gradually strengthening consumer trust. Emerging economies such as India, China, and Southeast Asian countries are expected to drive long-term growth, positioning the Asia Pacific as the fastest-growing regional ePharmacy market.

Market Competitive Landscape

The ePharmacy market is highly competitive and characterized by the presence of large integrated pharmacy networks, regional digital platforms, and emerging local players. Competition is driven by pricing strategies, delivery speed, prescription fulfillment efficiency, and integration with telemedicine and insurance systems. Market leaders benefit from strong logistics infrastructure, broad product portfolios, and advanced digital platforms, enabling high-volume prescription processing and customer retention. Mid-sized and smaller players compete through niche focus, localized services, and discount-led models. Ongoing investments in automation, data security, and regulatory compliance continue to shape competitive differentiation, while consolidation and strategic partnerships are increasingly influencing market dynamics.

Key Industry Developments:

- In September 2025, Manipal Hospital in Gurugram launched an e-pharmacy service that provides free home delivery of medicines.

- In November 2023, Tata 1mg surpassed PharmEasy to emerge as the leading player in India’s e-pharmacy market by gross merchandise value (GMV), as reported by The Economic Times.

- In January 2022, Hyphens Pharma officially launched first HSA-approved e-pharmacy in Singapore.

Companies Covered in ePharmacy Market

- The Kroger Co.

- Walgreen Co.

- Giant Eagle, Inc.

- Walmart, Inc.

- Express Scripts Holding Company

- CVS Health

- Optum Rx, Inc.

- Rowlands Pharmacy

- DocMorris (Zur Rose Group AG)

- Others

Frequently Asked Questions

The global ePharmacy market is expected to reach US$ 120.3 billion in 2026.

Rising internet penetration and chronic disease prevalence drive demand, with 5.4 billion users enabling convenient access.

The global market is expected to witness a CAGR of 21.5% between 2026 and 2033.

Key opportunities include expanding telemedicine integration, chronic disease management services, rural healthcare access, faster delivery models, and advanced data security solutions.

Leading firms include CVS Health, Walgreens, Walmart, and DocMorris, controlling 65%+ share.