- Retail

- Entertainment and Amusement Market

Entertainment and Amusement Market Size, Share, and Growth Forecast, 2026 - 2033

Entertainment and Amusement Market by Product Type (Theme Park, Festivals and Concerts, Entertainment Sports, Live Events, Arcades, Cinemas), Age Group (Children, Teenagers, Young Adults, Adults, Seniors), and Regional Analysis for 2026 - 2033

Entertainment and Amusement Market Size and Trends Analysis

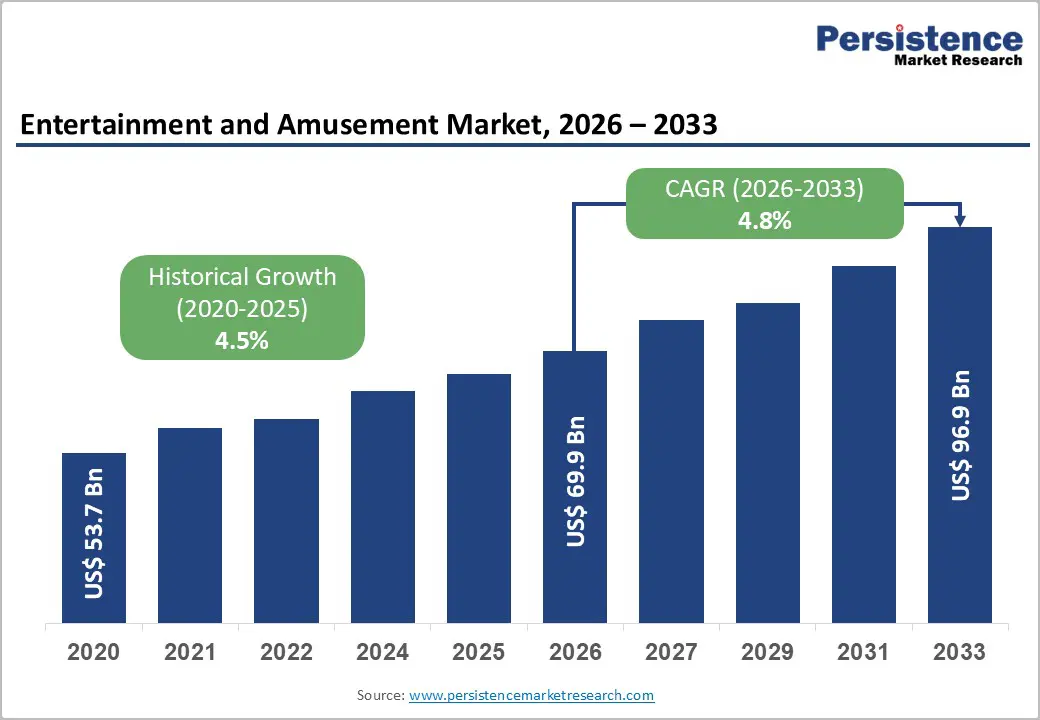

The global entertainment and amusement market size is likely to be valued at US$69.9 billion in 2026 and is expected to reach US$96.9 billion by 2033, growing at a CAGR of 4.8% during the forecast period from 2026 to 2033, driven by evolving consumer lifestyles and a structural shift toward experience-centric spending.

The sector includes theme parks, festivals, live sports and events, arcades, and cinemas, catering to all age groups. After pandemic disruptions, demand has rebounded strongly as consumers prioritize social, immersive, and out-of-home experiences. Urbanization, a growing middle class, and rising discretionary spending are supporting growth across regions. Technology adoption, including VR, AR, AI-driven personalization, contactless ticketing, and data analytics, is further enhancing engagement and operational efficiency.

Key Industry Highlights:

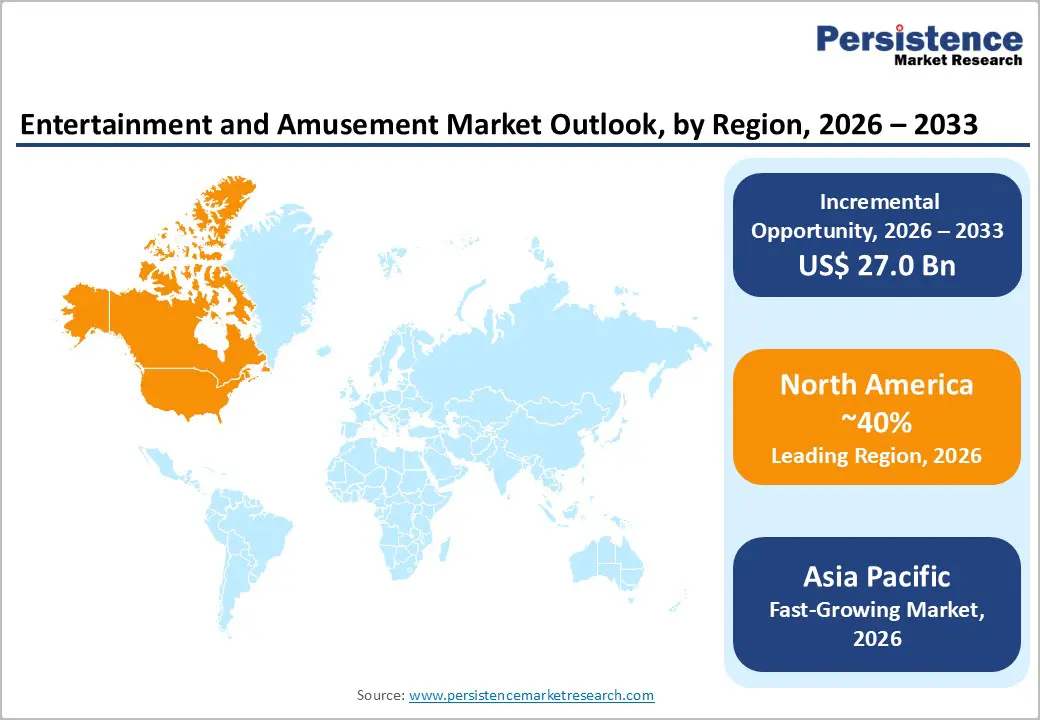

- Leading Region: North America, accounting for a market share of 40% in 2026, driven by strong leisure spending, advanced infrastructure, and high consumer demand for immersive experiences.

- Fastest-growing Region: Asia Pacific, supported by rapid urbanization, expanding middle-class populations, and strong investment in new attractions.

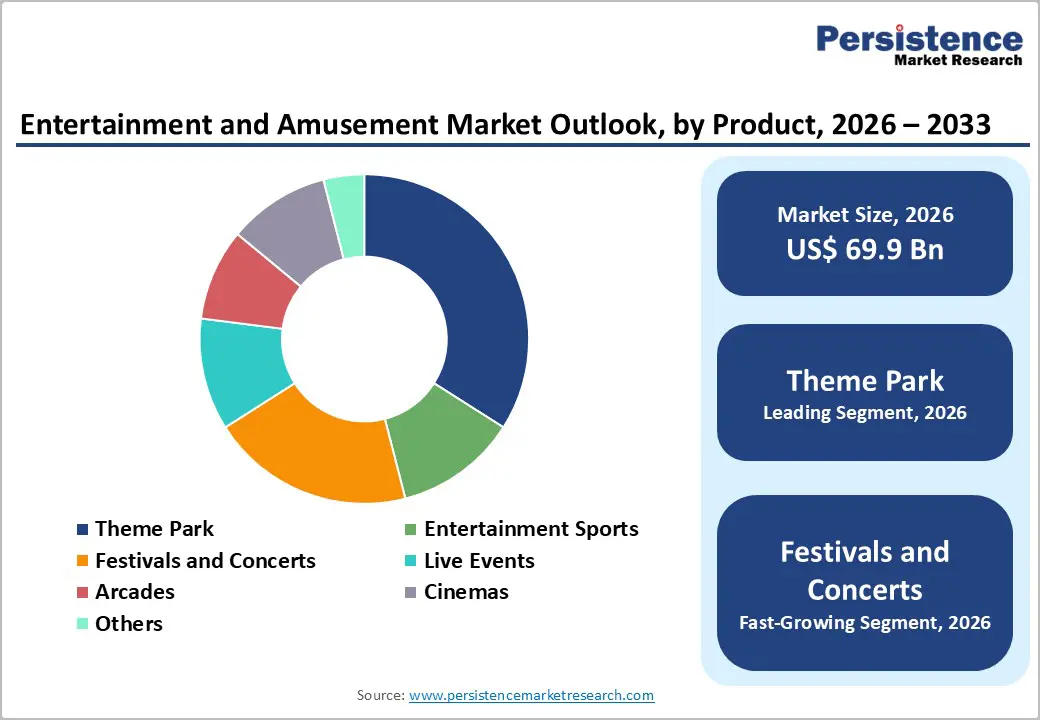

- Leading Product Type: Theme parks, accounting for 42% of the revenue share, driven by strong attendance, IP-based attractions, and rising demand for immersive destination experiences.

- Leading Age Group: Young adults, accounting for over 38% of the revenue share in 2026, supported by high discretionary spending, preference for experiential entertainment, and strong engagement with social and immersive attractions.

| Key Insights | Details |

|---|---|

|

Entertainment and Amusement Market Size (2026E) |

US$69.9 Bn |

|

Market Value Forecast (2033F) |

US$96.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Technological Advancements in Attractions and Digital Integration

Operators are integrating virtual reality, augmented reality, artificial intelligence, facial recognition, mobile applications, and contactless ticketing to enhance visitor convenience and engagement. Smart queue systems, personalized recommendations, and data-driven crowd management improve operational efficiency while elevating guest satisfaction. Digital twins and simulation technologies are also enabling safer ride design and predictive maintenance. These advancements not only modernize traditional amusement formats but also attract tech-savvy consumers seeking interactive and seamless experiences across theme parks, arcades, cinemas, and live entertainment venues.

Beyond operational efficiency, digital integration enhances revenue generation and customer retention. Mobile ecosystems allow dynamic pricing, targeted promotions, gamified loyalty programs, and real-time engagement before, during, and after visits. Immersive projection mapping, holographic performances, and AI-driven storytelling create differentiated attractions that increase dwell time and repeat visitation. Integration of social media sharing features amplifies brand visibility and organic marketing. As consumer expectations evolve, continuous technological upgrades are essential for competitiveness, scalability, and sustained growth in the entertainment and amusement market.

Rising Demand for Experiential and Immersive Entertainment

Consumers are increasingly prioritizing experiences over material purchases, significantly benefiting the entertainment and amusement sector. Families, young adults, and corporate groups seek memorable, shareable activities that foster social interaction and emotional connection. Immersive environments such as themed lands, live festivals, cinematic universes, and interactive sports events deliver multisensory engagement that traditional leisure formats cannot replicate. This shift toward experiential consumption is particularly strong among younger demographics who value unique and personalized moments.

The desire for immersive engagement is fueled by social media influence and lifestyle trends. Visitors gravitate toward attractions that provide visually striking, Instagrammable settings and exclusive events. Seasonal festivals, themed concerts, and large-scale entertainment sports tournaments amplify community participation and tourism. Operators are responding by investing in storytelling, intellectual property collaborations, and interactive installations that deepen emotional resonance. This structural shift toward experiential leisure ensures sustained footfall, diversified revenue streams, and long-term brand loyalty.

Barrier Analysis - Seasonality and Weather Dependencies

Seasonality remains a significant restraint, particularly for outdoor theme parks, festivals, and large-scale live events. Attendance often fluctuates based on holiday calendars, school vacations, and climatic conditions, leading to uneven revenue distribution throughout the year. Extreme weather events such as heavy rainfall, heatwaves, or storms can result in cancellations, reduced footfall, and increased operational risks. In certain regions, monsoons or prolonged winters shorten peak operating seasons, directly impacting profitability and resource utilization across entertainment venues.

Weather unpredictability complicates planning, staffing, and inventory management. Operators must invest in climate-resilient infrastructure, covered attractions, and diversified indoor offerings to mitigate risks. Insurance costs and maintenance expenses may rise due to environmental exposure. While dynamic pricing and seasonal promotions can partially offset fluctuations, dependence on favorable weather remains a structural challenge. Long term sustainability therefore, requires strategic geographic expansion, hybrid indoor-outdoor models, and diversified revenue channels to reduce vulnerability to seasonal volatility.

Shifting Consumer Preferences to Digital Alternatives

The rapid growth of digital streaming platforms, online gaming, esports, and virtual entertainment poses a competitive challenge to traditional amusement venues. Consumers increasingly access affordable, on-demand content from home, reducing the urgency to visit physical entertainment locations. Subscription-based digital ecosystems provide convenience, personalized recommendations, and lower-cost alternatives, particularly during economic slowdowns. This shift can decrease cinema attendance and limit spontaneous visits to arcades or live venues, especially among tech-oriented younger demographics.

Advancements in home entertainment technologies, including high definition displays and immersive audio systems, replicate elements of theatrical experiences. Social gaming platforms and virtual communities offer interactive engagement without geographic constraints. To remain competitive, amusement operators must continuously innovate, differentiate through real-world immersion, and emphasize social connectivity that digital platforms cannot fully replicate. Failure to adapt to evolving digital preferences gradually erode market share in certain sub-segments.

Opportunity Analysis - VR/AR and Hybrid Experiences

Virtual reality (VR) and augmented reality (AR) present transformative growth opportunities within the entertainment and amusement market. By blending physical environments with digital overlays, operators can create interactive storytelling experiences, gamified rides, and immersive simulations. These technologies enable cost-effective content updates without major structural changes, extending attraction lifecycles. VR-enabled arcades, AR-enhanced theme park zones, and immersive sports simulations are expanding audience reach while attracting technology-driven demographics seeking novel engagement formats.

Hybrid experiences that combine online and offline participation strengthen market potential. Live events streamed with interactive digital features expand monetization beyond physical capacity limits. App-based engagement before and after visits builds sustained relationships with customers. Integration of wearable devices and mixed-reality attractions enhances personalization and data collection. As technology becomes more accessible and affordable, virtual reality (VR) and augmented reality (AR) adoption is reshaping visitor expectations and unlocking scalable, high-margin revenue streams across multiple product categories.

Rise of Location-Based Entertainment (LBE) and Immersive Phygital Experiences

Location-based entertainment is gaining prominence as consumers seek social, shared experiences unavailable at home. Indoor entertainment centers, immersive escape rooms, experiential museums, themed dining venues, and interactive gaming arenas are expanding in urban malls and mixed-use developments. These venues require relatively lower capital investment compared to large theme parks while offering flexible scalability. LBE formats cater strongly to teenagers and young adults, supporting steady foot traffic in commercial hubs.

The emergence of phygital experiences, blending physical interaction with digital augmentation, amplifies growth prospects. Projection mapping, motion tracking, interactive walls, and gamified retail zones create dynamic, participatory environments. Retailtainment strategies integrate shopping with entertainment, increasing dwell time and cross-selling opportunities. As urbanization accelerates and mixed-use infrastructure expands, LBE and phygital concepts offer adaptable, high-engagement models that align with evolving consumer lifestyles and urban entertainment demand.

Category-wise Analysis

Product Type Insights

Theme parks are expected to lead the entertainment and amusement market, accounting for approximately 42% of revenue in 2026, driven by strong brand ecosystems, destination-based tourism, and immersive intellectual property integrations. These parks combine rides, themed environments, live performances, retail, and food experiences into a single, high-engagement format that attracts families, young adults, and international tourists alike. Large operators leverage recognized franchises to create multi-generational appeal and premium pricing strategies. For example, The Walt Disney Co. leverages its film and character portfolio to develop immersive lands that enhance guest engagement and extend on-site spending.

Festivals and concerts are likely to represent the fastest-growing segment, supported by rising demand for live, social, and culturally immersive experiences. Consumers increasingly prioritize music festivals, touring events, and hybrid live-streamed performances that combine physical attendance with digital participation. This segment benefits from strong youth engagement, social media amplification, and artist-driven branding that creates unique, time sensitive experiences. For example, Live Nation Entertainment has expanded festival formats, capitalizing on experiential demand and enhancing audience interaction.

Age Group Insights

Young adults are projected to lead the market, capturing around 38% of the revenue share in 2026, supported by high discretionary spending and a strong inclination toward social and experiential entertainment. This group actively seeks thrill-based attractions, music festivals, immersive gaming zones, and large-scale events that provide both engagement and shareable moments. Their digital connectivity amplifies marketing reach through social media exposure and peer influence. For example, Six Flags Entertainment Corp. attracts young adults with high-adrenaline rides and seasonal entertainment programming.

Teenagers are likely to represent the fastest-growing age group, driven by strong engagement with esports, arcades, and interactive entertainment formats. This demographic values competitive gaming, immersive digital attractions, and social gathering spaces within malls and urban centers. Location-based entertainment venues increasingly design youth-focused environments that blend technology with real-world interaction. Social media trends and influencer culture stimulate interest in experiential destinations. For example, Timezone Entertainment Pvt. Ltd. targets teenage audiences through gamified arcade environments and interactive group experiences.

Regional Insights

North America Entertainment and Amusement Market Trends

North America is anticipated to be the leading region, accounting for a market share of 40% in 2026, driven by strong consumer preferences and strategic diversification. The increasing integration of advanced technologies to enrich guest experiences and streamline operations. Operators are deploying contactless services, mobile engagement platforms, AI-driven personalization, and immersive attractions that bridge physical and digital environments. Consumers increasingly expect seamless, personalized interactions from the moment they plan a visit to post-experience engagement, prompting investment in data analytics and digital ecosystems.

The resurgence and reinvention of live and location-based entertainment following pandemic-era disruptions. Large festivals, concerts, and experiential sports events are drawing significant attendance as consumers prioritize shared social experiences and community-centered entertainment. Operators are experimenting with flexible venue formats and multi-city touring models that adapt to audience demand and maximize reach. For example, Universal Studios Recreation Group is investing in new immersive lands, franchise-driven attractions, and dynamic event schedules that appeal to diverse age groups.

Europe Entertainment and Amusement Market Trends

Europe is likely to be a significant market for entertainment and amusement in 2026, due to evolving consumer preferences and strategic diversification of experiences. The major trend is the growing demand for culturally immersive attractions and lifestyle-oriented entertainment options that blend leisure with social engagement. Traditional theme parks and amusement centers are enhancing guest experiences through localized content, seasonal programming, and special events that resonate with regional cultural identities. European markets are also expanding location-based entertainment offerings, such as indoor family entertainment centers and experiential retailtainment zones.

Europe is the integration of technology to elevate engagement and operational efficiency. Digital innovation, including mobile apps, augmented reality, and data analytics, is being used to personalize visitor experiences, optimize crowd management, and introduce interactive storytelling elements across attractions. Operators are crafting hybrid entertainment models that seamlessly connect physical and digital experiences, such as app-driven scavenger hunts, virtual queuing systems, and interactive exhibitions that cater to both local residents and international visitors. For example, Compagnie des Alpes is leveraging popular franchises and themed experiences in its European parks to increase attendance and deepen engagement.

Asia Pacific Entertainment and Amusement Market Trends

The Asia Pacific region is likely to be the fastest-growing region, driven by rapid urbanization, rising disposable incomes, and an expanding middle-class population with an appetite for experiential leisure. A defining trend is the expansion of large-scale theme parks and destination attractions that serve as regional tourism anchors. Governments across the region are increasingly supporting entertainment infrastructure as part of broader economic diversification and tourism strategies.

The rapid adoption of immersive and technology-enhanced attractions to meet evolving consumer preferences. Operators are incorporating digital experiences such as virtual reality (VR), augmented reality (AR), interactive gamification, and personalized mobile engagement platforms to create differentiated offerings. These technologies improve visitor experiences while helping manage crowds efficiently and support data-based decision making. Seasonal events, live performances, and hybrid entertainment formats are increasingly integrated into amusement spaces, enhancing repeat visitation and deepening audience interaction. For example, Chimelong Group Co. Ltd. has expanded its portfolio with tech-driven attractions and high-capacity ride systems to attract diverse demographic groups.

Competitive Landscape

The global entertainment and amusement market exhibits a moderately fragmented structure, driven by the presence of both multinational giants and numerous regional and niche operators competing for audience attention, brand loyalty, and technological edge. Market leadership is shaped by brand strength, intellectual property portfolios, operational scale, and experience in innovation, with the top five players capturing a majority of industry revenue while leaving space for agile and localized competitors.

With key leaders including The Walt Disney Co., Universal Studios Recreation Group, Merlin Entertainments, SeaWorld Parks & Entertainment, and Chimelong Group, competition is intense across and regional markets. These players compete through continuous innovation in attractions, integration of advanced technologies such as AR/VR, enhanced guest services, and strategic IP partnerships that deepen engagement and increase repeat visitation. Seasonal event programming and differentiated pricing models amplify competitive dynamics.

Key Industry Developments:

- In January 2026, Six Flags Entertainment Corporation officially opened Six Flags Qiddiya City in Saudi Arabia, marking the company’s first theme park developed outside North America. Located within Qiddiya City near Riyadh, the park features 28 rides and attractions across six themed lands, positioning it as a landmark entertainment destination in the region. The park introduces multiple record-breaking roller coasters, including Falcon's Flight, recognized as the world’s tallest, fastest, and longest roller coaster, along with other high-thrill attractions designed for audiences.

- In May 2025, Shott Amusement Limited launched its flagship indoor entertainment center at Nesco, Mumbai, marking a significant expansion in India’s premium location-based entertainment segment. Spanning over 25,000 sq. ft. across two levels, the new facility features VIP bowling lanes, next-generation laser tag arenas, immersive virtual reality experiences, more than 80 arcade games, curated dining spaces, and dedicated banquet areas for corporate and social events.

Companies Covered in Entertainment and Amusement Market

- Al Hokair Entertainment

- Aspro Parks SA

- CEDAR FAIR LP

- Chimelong Group Co., Ltd.

- Compagnie des Alpes

- Entertainment Plus Production

- Fakieh Hospitality & Leisure Group

- IMG Artists

- irque du Soleil Entertainment Group

- Motion JVco Ltd.

- PARQUES REUNIDOS SERVICIOS CENTRALES S.A.

- SeaWorld Parks and Entertainment Inc.

- Six Flags Entertainment Corp.

- The Mousetrap

- The Rocky Horror Show

- The Walt Disney Co.

- Timezone Entertainment Pvt. Ltd.

- Universal Studios Recreation Group.

- Untamed Entertainment

- Wonderla Amusement Park

Frequently Asked Questions

The global entertainment and amusement market is projected to reach US$69.9 billion in 2026.

Rising disposable incomes and growing demand for immersive, experience-based leisure activities drive the entertainment and amusement market.

The entertainment and amusement market is expected to grow at a CAGR of 4.8% from 2026 to 2033.

Key market opportunities lie in VR/AR integration, expansion of location-based entertainment, and growth in emerging urban markets.

Al Hokair Entertainment, Aspro Parks SA, Cedar Fair LP, Chimelong Group Co. Ltd., Compagnie des Alpes, and Entertainment Plus Production are the leading players.