- Sensors & Controls

- Distance Measurement Sensor Market

Distance Measurement Sensor Market Size, Share, and Growth Forecast, 2025 - 2032

Distance Measurement Sensor Market by Distance Measurement Range (Short-Range Sensors, Medium-Range Sensors, Long-Range Sensors), Technology (Laser Sensors, Ultrasonic Sensors, Infrared Sensors, Capacitive Sensors, Magnetic Sensors), Application, and Regional Analysis for 2025 - 2032

Distance Measurement Sensor Market Size and Trend Analysis

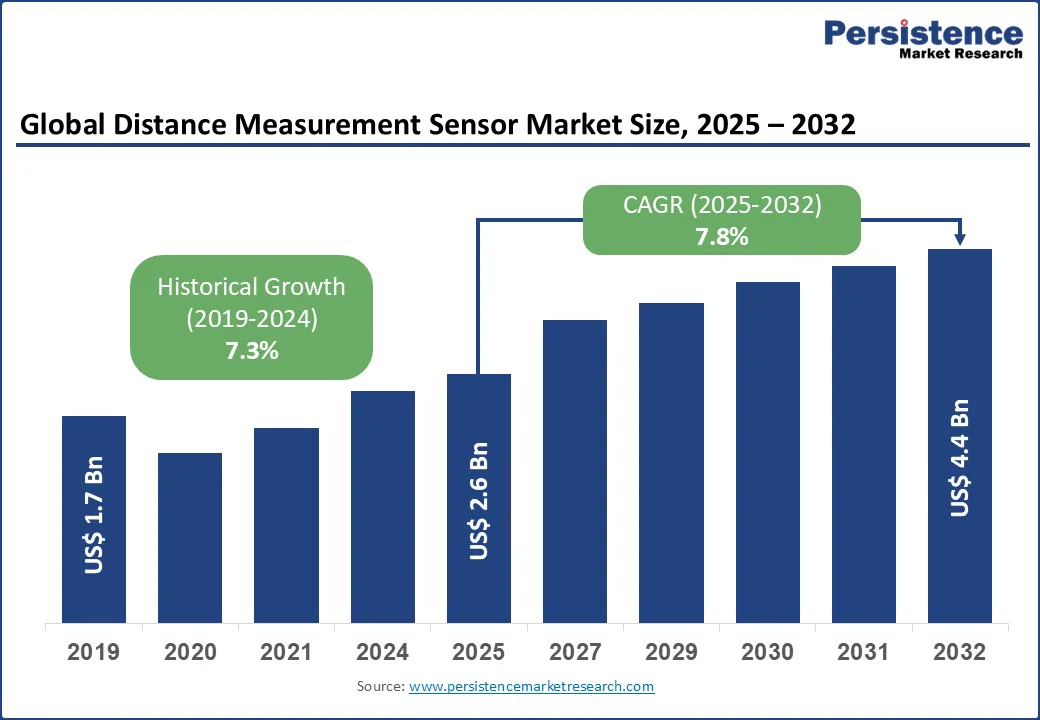

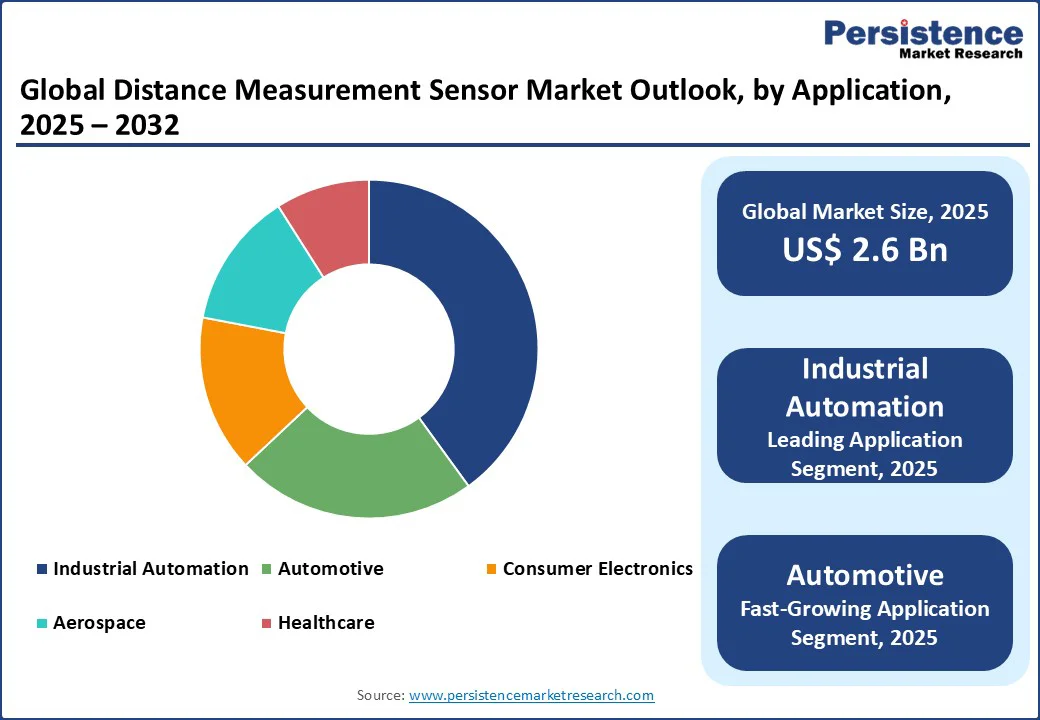

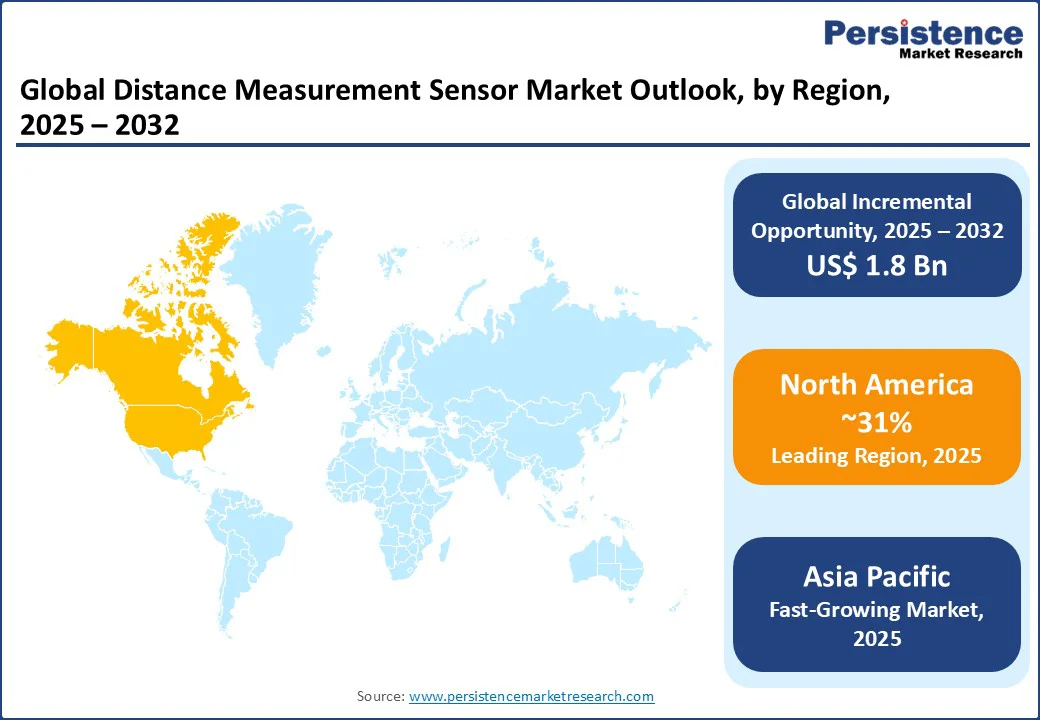

The global distance measurement sensor market size is likely to be valued at US$2.6 Bn by 2025 and expected to reach US$4.4 Bn by 2032, growing at a CAGR of 7.8% during the forecast period from 2025 to 2032, driven by the increasing adoption of automation across industries, advancements in sensor technologies, and the rising demand for precise and reliable distance measurement solutions.

Key Industry Highlights:

- Leading Region: North America is projected to account for a 31% share in 2025, driven by advanced industrial infrastructure and significant investments in sensor technologies in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, fueled by rising industrial automation and increasing demand for consumer electronics in China and Japan.

- Dominant Technology: Laser sensors account for a 33% share, favored for their high precision and versatility across various applications.

- Leading Application: Industrial automation contributes over 40% of market revenue, driven by the high adoption of sensors in manufacturing and robotics.

| Key Insights | Details |

|---|---|

|

Distance Measurement Sensor Market Size (2025E) |

US$2.6 Bn |

|

Market Value Forecast (2032F) |

US$4.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

7.3% |

Market Factors - Growth, Barrier, and Opportunity Analysis

Increasing Adoption of Industrial Automation

The rising adoption of industrial automation is a key driver of growth in the distance measurement sensor market. Industries across manufacturing, automotive, robotics, and electronics are increasingly integrating automation technologies to enhance operational efficiency, reduce human error, and improve product quality. Distance measurement sensors, including laser, ultrasonic, and optical types, play a crucial role in these automated systems by enabling precise position detection, object tracking, and level measurement in real-time.

For instance, Keyence laser sensors are widely used in electronics assembly lines to ensure accurate placement of delicate components. In contrast, SICK LiDAR sensors enable precise object detection for robotic arms in automotive production.

Automated production lines rely on sensors for accurate measurements during assembly, quality control, and material handling, allowing manufacturers to optimize processes and reduce downtime. In automotive manufacturing, sensors are extensively used for robotic arms, automated guided vehicles (AGVs), and safety systems, facilitating faster and more reliable operations. ABB and FANUC robotics utilize high-precision distance sensors for these purposes. Similarly, in electronics and consumer goods manufacturing, distance measurement sensors ensure precise alignment and assembly of delicate components.

The growing focus on smart factories, Industry 4.0 initiatives, and digital transformation strategies further accelerates demand for advanced sensors. By providing high accuracy, durability, and integration with industrial networks, distance measurement sensors are becoming indispensable for automated environments, making industrial automation a significant growth area.

High Costs of Advanced Sensor Technologies Act as a Barrier to Growth

The high costs associated with advanced sensor technologies, such as laser and ultrasonic sensors, pose a significant restraint to market growth. Laser sensors, LiDAR systems, and high-precision ultrasonic sensors often require sophisticated components, miniaturized optics, and cutting-edge electronics, which contribute to elevated manufacturing costs.

For instance, Velodyne LiDAR’s high-resolution LiDAR units used in autonomous vehicles can cost tens of thousands of dollars per unit, reflecting the complexity and precision involved. These expenses are further amplified by research and development investments, stringent quality control, and certification requirements for industrial and automotive applications, such as ISO 9001 certification for factory automation sensors or automotive-grade AEC-Q100 compliance.

High upfront costs can be a barrier for small and medium-sized enterprises, especially in regions with limited capital resources. While large industrial players, such as Siemens and Bosch, may absorb these costs due to long-term operational efficiency gains, smaller manufacturers often delay or limit integration of advanced sensors into production lines. This cost sensitivity can hinder market penetration, particularly in emerging economies where price competitiveness is a key factor.

Maintenance, calibration, and replacement costs for sophisticated sensors, such as those in ABB robotics or Keyence laser measurement systems, add to the total cost of ownership, influencing purchase decisions. Until production costs decrease and more cost-effective solutions become available, the high price of advanced sensor technologies will continue to be a notable restraint, affecting adoption across industrial, automotive, and consumer applications.

Growing Demand for Autonomous Vehicles Creates Numerous Opportunities

The growing demand for autonomous and semi-autonomous vehicles represents a significant opportunity for the distance measurement sensor market. These vehicles rely on advanced sensor technologies, including LiDAR, laser, ultrasonic, and radar sensors, to detect objects, measure distances, and navigate complex environments safely. Distance measurement sensors are critical for enabling real-time mapping, obstacle detection, collision avoidance, and adaptive cruise control, making them indispensable components in autonomous vehicle systems.

Automotive manufacturers and technology companies are investing heavily in sensor integration to achieve higher levels of vehicle autonomy. For instance, Waymo uses high-resolution LiDAR sensors combined with radar and camera systems to ensure safe navigation in urban and highway environments. Similarly, Tesla incorporates ultrasonic sensors for parking assistance and object detection, while NIO and BMW deploy LiDAR and laser sensors in their autonomous vehicle prototypes to enhance situational awareness and safety.

Regulatory initiatives, government funding, and consumer interest in smart mobility solutions further support the push toward fully autonomous vehicles. As the adoption of autonomous vehicles accelerates globally, the demand for high-precision distance measurement sensors is expected to grow substantially. This trend presents a major opportunity for sensor manufacturers to innovate, expand their product portfolios, and capture a share of the rapidly evolving automotive technology market.

Category-wise Analysis

Distance Measurement Range Insights

Medium-range sensors (1 meter to 10 meters) hold the largest market share due to their versatility in applications such as industrial automation, automotive safety systems, and consumer electronics. These sensors are widely used in robotics and vehicle parking systems for accurate distance measurement, ensuring compliance with safety and performance standards. Companies such as Micro-Epsilon and TR Electronics leverage advanced laser and ultrasonic technologies to cater to this segment, particularly in North America and Europe, where demand for precision measurement is high.

Long-range sensors (over 10 meters) are the fastest-growing segment, driven by their critical role in autonomous vehicles, aerospace, and large-scale industrial applications. The rise of LiDAR technology in self-driving cars and drone navigation is fueling demand for long-range sensors. Firms such as Sick AG and Leuze Electronic GmbH + CO. KG are expanding their long-range sensor offerings, particularly in research institutes and automotive companies, supported by increasing R&D investments in the Asia Pacific and North America.

Technology Insights

Laser sensors account for a 33% share in 2025, driven by their high precision, reliability, and ability to function in diverse environmental conditions. They are extensively used in industrial automation and automotive applications, such as LiDAR systems for autonomous vehicles. Companies such as Keyence Corporation and Baumer offer advanced laser sensor solutions, particularly in North America and Europe, where precise measurement is crucial for smart manufacturing.

Ultrasonic sensors are the fastest-growing segment, propelled by their cost-effectiveness and versatility in short- and medium-range applications. The increasing adoption of ultrasonic sensors in consumer electronics, such as smartphones and home automation systems, drives market growth. Companies such as Pepperl+Fuchs GmbH and Ifm Electronic GmbH are innovating with compact ultrasonic sensors, particularly in the Asia Pacific, where consumer electronics demand is surging.

Application Insights

Industrial automation accounts for over 40% of market revenue in 2025, driven by the high adoption of sensors in manufacturing, robotics, and logistics. Distance measurement sensors ensure precise positioning and quality control in automated systems, meeting the demands of smart factories. Major players, such as Sick AG and Eaton, supply sensor solutions for industrial settings, particularly in the urban markets of North America and the Asia Pacific.

Automotive is the fastest-growing segment due to the increasing integration of sensors in advanced driver-assistance systems (ADAS) and autonomous vehicles. The demand for precise distance measurement in collision avoidance and navigation systems drives the adoption of laser and ultrasonic sensors. Companies such as Omron Corporation and Honeywell are innovating with automotive-grade sensors, driven by rising demand in the Asia Pacific and Europe, where the automotive industries are expanding rapidly.

Regional Insights

North America Distance Measurement Sensor Market Trends

North America is likely to register 31% share in 2025, with the U.S. being the dominant contributor due to its advanced industrial infrastructure and significant investments in automation and automotive technologies. The region’s leadership is primarily driven by the United States, where rapid advancements in automation, robotics, and automotive technologies continue to create substantial demand for advanced sensing solutions. In particular, the growing integration of sensors in smart manufacturing, process optimization, and quality control systems has positioned distance measurement sensors as a critical enabler of industrial efficiency.

The U.S. automotive industry also plays a key role in fueling market growth, with increasing adoption of sensors in safety systems, driver assistance technologies, and autonomous vehicle development. This trend is further supported by the country’s strong research ecosystem and willingness to adopt emerging technologies across various sectors.

Regional companies such as Measurement Specialties Inc. and Banner Engineering Corp. are at the forefront of this transformation, delivering high-performance sensor solutions tailored for industrial and automotive applications. Their innovations, combined with ongoing investments in modernization and digital transformation, continue to reinforce North America’s position as a leader in the distance measurement sensor market.

Europe Distance Measurement Sensor Market Trends

Europe represents a key region in the distance measurement sensor market, with Germany, the U.K., and France leading adoption. The region’s growth is primarily driven by its strong automotive and industrial automation sectors. Germany, recognized as a hub for automotive manufacturing, demonstrates significant demand for laser sensors, particularly in advanced driver-assistance systems (ADAS) and autonomous vehicle applications. The integration of precision sensors into production lines and quality control processes has also reinforced the role of distance measurement technologies in European manufacturing.

The industrial automation sector across Europe continues to modernize, adopting innovative sensor solutions to enhance productivity, efficiency, and operational safety. France and the U.K. are increasingly investing in smart factories and connected manufacturing, further boosting the demand for versatile sensor technologies. Leading companies, such as Leuze Electronic GmbH + Co. KG and Baumer, are expanding their regional presence by focusing on high-precision sensors tailored for automotive, industrial, and manufacturing applications. Their continued innovation and focus on customization enable European manufacturers to meet stringent quality and safety standards, solidifying the region’s position as a significant contributor to the distance measurement sensor market.

Asia Pacific Distance Measurement Sensor Market Trends

The Asia Pacific is emerging as the fastest-growing region in the distance measurement sensor market, driven by rapid industrialization and increasing demand for consumer electronics in key countries, including China and Japan. China’s strong emphasis on smart manufacturing through initiatives has accelerated the adoption of laser and ultrasonic sensors in industrial automation, driving efficiency, precision, and operational safety in factories. The country’s growing automotive sector also contributes to the rising need for advanced sensor technologies in driver-assistance systems and autonomous vehicles.

Japan, renowned for its leadership in robotics and automotive manufacturing, continues to be a major adopter of distance measurement sensors. The country’s focus on high-tech automation and industrial precision further strengthens regional growth. Additionally, the region’s booming consumer electronics sector has increased the demand for short-range sensors in devices such as smartphones, smart home equipment, and wearable technology.

Leading companies such as Keyence Corporation and Omron Corporation are actively catering to the region’s growing automation and electronics markets, providing advanced sensor solutions that support industrial modernization, product innovation, and the evolving requirements of Asia Pacific’s dynamic technology landscape.

Competitive Landscape

The global distance measurement sensor market is highly competitive, with a mix of multinational leaders and specialized regional players. In North America and Europe, companies such as Micro-Epsilon, TR Electronics, Pepperl+Fuchs GmbH, Sick AG, Measurement Specialties Inc., and Leuze Electronic GmbH + CO. KG lead the sector through advanced R&D, strong product portfolios, and strategic collaborations. These firms focus on delivering high-precision laser, ultrasonic, and LiDAR sensors for industrial automation, automotive safety systems, and robotics applications.

Key Developments

- In November 2024, Micro-Epsilon introduced the optoNCDT 1220 laser triangulation sensors with an IO-Link interface, improving communication capabilities for integration into smart manufacturing systems.

- In October 2024, SICK AG company introduced the LMS4000 2D LiDAR sensor, combined with the Sensor Integration Machine SIM2x00 and SICK Nova, offering robust performance for various applications.

Companies Covered in Distance Measurement Sensor Market

- Micro-Epsilon

- TR Electronics

- Pepperl+Fuchs GmbH

- Impress Sensors and Systems Ltd

- Sick AG

- Measurement Specialties Inc

- Eaton

- Keyence Corporation

- Datalogic

- Balluf Inc

- Sensopart Industriessensorik GmbH

- Dimetrix AG

- Others

Frequently Asked Questions

The global distance measurement sensor market is projected to reach US$2.6 billion in 2025.

The rising adoption of industrial automation and advancements in sensor technologies, particularly laser and ultrasonic, are the key market drivers.

The distance measurement sensor market is poised to witness a CAGR of 7.8% from 2025 to 2032.

The growing demand for autonomous vehicles in decentralized mobility solutions is a key market opportunity.

Micro-Epsilon, Sick AG, Keyence Corporation, Pepperl+Fuchs GmbH, and Omron Corporation are key market players.