- Specialty & Fine Chemicals

- Dibromo Alkane Market

Dibromo Alkane Market Size, Share, and Growth Forecast 2026 – 2033

Dibromo Alkane Market by Product Type (Dibromo Methane, Dibromo Ethane, Dibromo Propane, Others), Application (Agriculture, Pharmaceuticals, Chemicals, Consumer Goods, Others), and Regional Analysis, 2026–2033

Dibromo Alkane Market Size and Trend Analysis

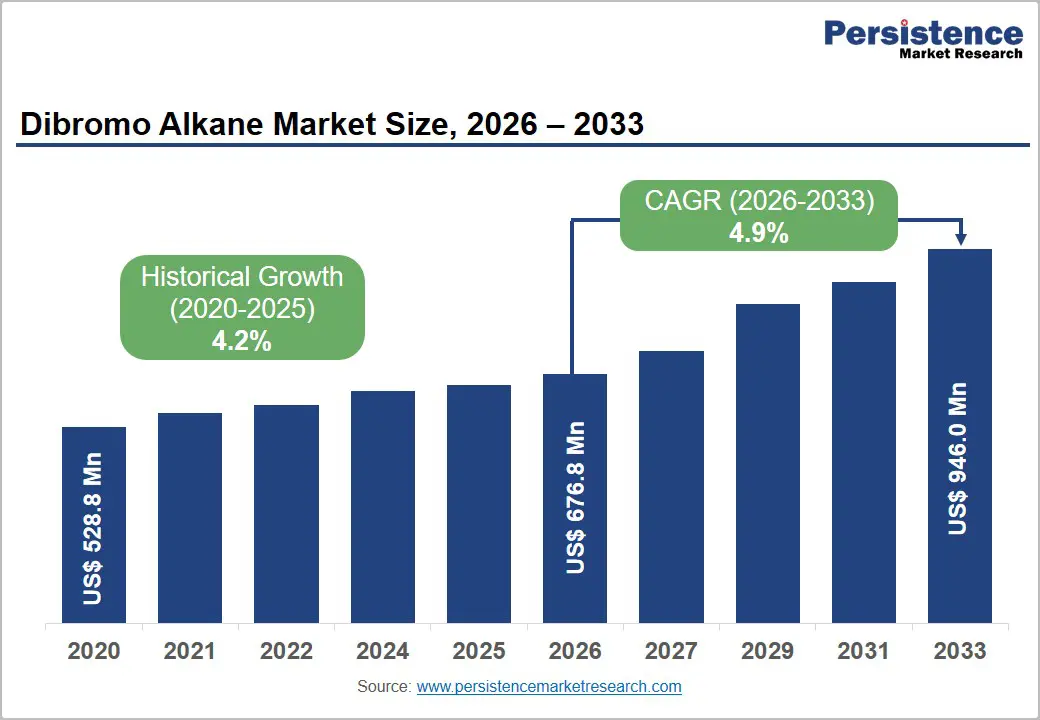

The global dibromo alkane market size is expected to be valued at US$ 676.8 million in 2026 and projected to reach US$ 946.0 million, growing at a CAGR of 4.9% between 2026 and 2033.

This steady expansion is principally driven by rising demand for bromine-based flame retardants across electronics and construction sectors, growing pharmaceutical API synthesis activity, and increasing agrochemical production across developing economies.

Reinforcing regulatory frameworks on fire safety standards and widening applications in specialty chemical manufacturing further solidify the long-term growth trajectory of the global dibromo alkane market.

Key Industry Highlights

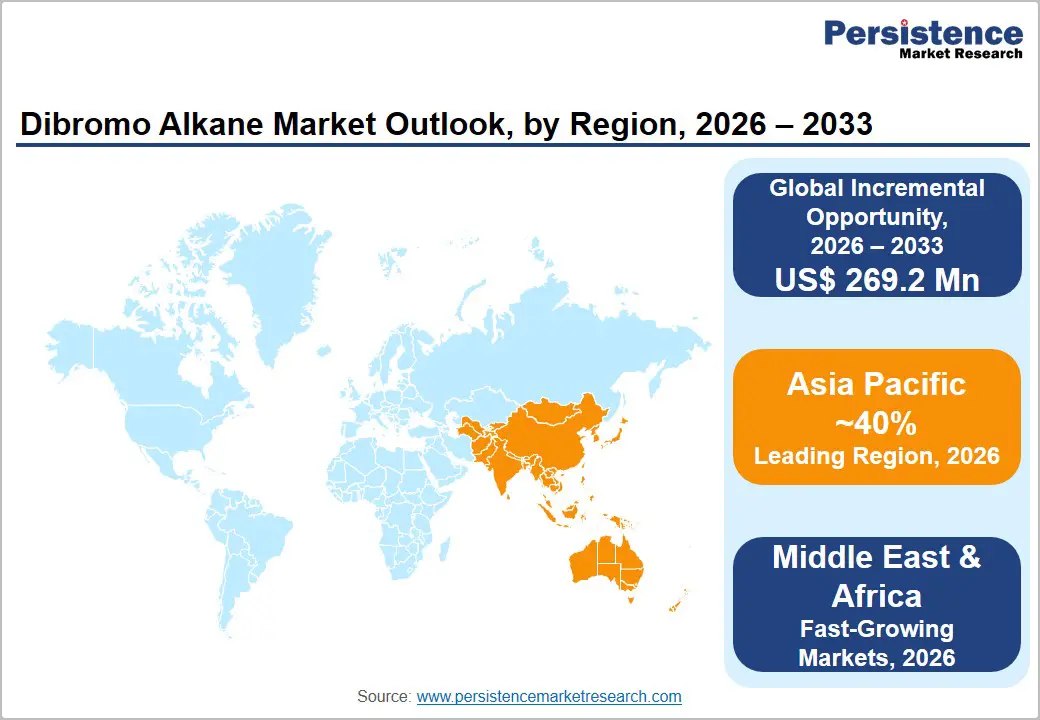

- Leading Region; Asia Pacific dominates the global dibromo alkane market with approximately 40% share in 2026, driven by large-scale chemical manufacturing in China, expanding pharmaceutical API production in India, and growing industrial activity across Southeast Asian markets contributing to the region's sustained leadership position.

- Fastest Growing Region: Middle East & Africa is the fastest growing regional market for dibromo alkanes supported by expanding chemical processing infrastructure, increasing agricultural input demand, and growing investment in specialty chemical manufacturing within Gulf Cooperation Council (GCC) nations and broader African markets.

- Dominant Product Type: Dibromo methane leads all product type segments with approximately 41% market share in 2026, underpinned by its multi-functional utility as a synthesis intermediate, high-density solvent, and laboratory reagent widely used in pharmaceutical API production, mineral processing, and specialty organic chemistry globally.

- Fastest Growing Segment: Dibromo ethane is the fastest growing product type segment, projected to expand at a CAGR of 6% between 2026 and 2033, driven by rising pharmaceutical synthesis demand and increasing adoption as a chemical intermediate across key manufacturing regions in Asia and Europe.

- Key Market Opportunity: A significant market opportunity is emerging in pharmaceutical API manufacturing expansion across India and Southeast Asia, underpinned by government-backed PLI incentives, capacity investments by key players including Neogen Chemicals Ltd and Mody Chemi Pharma Limited, and rising global export demand for generic pharmaceutical compounds.

DRO Analysis

Drivers - Rising Demand for Flame Retardants in Electronics and Construction

The accelerating global production of consumer electronics and the enforcement of building fire safety standards have created sustained, compounding demand for bromine-based flame retardants, with dibromo alkane compounds serving as critical chemical intermediates in their formulation. The International Electrotechnical Commission (IEC) reports that global electronics output has exceeded USD 3 trillion annually, necessitating the extensive use of halogenated flame-retardant chemicals.

Regulatory mandates such as the European Union's Construction Products Regulation (EU CPR) and the National Fire Protection Association (NFPA) codes in the United States require fire performance compliance in building materials, driving manufacturers to incorporate approved brominated intermediates. Dibromo methane and dibromo ethane are widely used in producing these formulations, positioning the dibromo alkane market to benefit from structural growth in electronics and infrastructure development globally.

Expanding Role in Pharmaceutical Synthesis and Agrochemicals

Dibromo alkanes function as indispensable alkylating agents and reaction intermediates in synthesizing active pharmaceutical ingredients (APIs) and crop protection chemicals, ensuring steady demand from two of the world's fastest-growing sectors. The World Health Organization (WHO) estimates global pharmaceutical production grows at approximately 5–6% annually, with significant contributions from generic API manufacturing concentrated in Asia and Europe.

The Food and Agriculture Organization (FAO) of the United Nations has documented a consistent rise in global agrochemical consumption, particularly across developing economies in Asia, Africa, and Latin America. Dibromo propane serves as a key precursor in nematicide synthesis and other agrochemical intermediates, while dibromo ethane finds application in pharmaceutical synthesis pathways, establishing a broad and resilient demand foundation across these essential end-use sectors.

Restraints - Stringent Environmental and Health Regulations

Regulatory restrictions on specific dibromo alkane compounds represent a material constraint on broader market adoption. 1,2-Dibromoethane (ethylene dibromide, EDB) has been classified as a probable human carcinogen by the U.S. Environmental Protection Agency (EPA) and faces severe restrictions under the European Chemicals Agency (ECHA) REACH regulation, which designates certain brominated compounds as substances of very high concern (SVHCs).

Compliance with these frameworks significantly raises production, handling, and formulation costs for manufacturers, while simultaneously limiting the addressable application scope in consumer product categories. These regulatory headwinds create barriers to market expansion in mature economies and constrain the commercialization of certain dibromo alkane variants across key industrial sectors.

Volatility in Bromine Raw Material Prices

Dibromo alkane manufacturing is fundamentally dependent on bromine as a primary feedstock, a commodity whose production is geographically concentrated in the United States, Israel, and China. According to the U.S. Geological Survey (USGS), global bromine output remains dominated by a limited number of producers, leaving the supply chain inherently vulnerable to geopolitical tensions, energy cost fluctuations, and logistical disruptions.

Periods of bromine price volatility directly compress manufacturing margins for dibromo alkane producers and translate into unpredictable pricing for downstream customers in the pharmaceutical, chemical, and agricultural industries, thereby complicating long-term procurement planning and constraining market growth potential.

Opportunities - Growing Pharmaceutical Manufacturing in Emerging Economies

The rapid scaling of pharmaceutical manufacturing infrastructure across India, China, and Southeast Asia represents a high-potential, long-term opportunity for dibromo alkane suppliers. India, widely recognized as the "Pharmacy of the World," exports pharmaceutical products to over 200 countries, and the Indian Pharmaceutical Alliance (IPA) projects continued double-digit growth in generic API production.

Dibromo ethane and dibromo propane are key intermediates in synthesizing several pharmaceutical compounds, and the establishment of new bulk drug parks under India's Production-Linked Incentive (PLI) scheme, with an approved outlay of INR 6,940 crore for bulk drug manufacturing, is expected to generate significant incremental demand. With global pharmaceutical companies diversifying supply chains beyond China, Indian and Southeast Asian manufacturers are actively expanding capacity, presenting direct and measurable volume growth opportunities for dibromo alkane producers strategically targeting this segment.

Increasing Adoption in Specialty Chemicals and Advanced Material Science

The proliferation of specialty chemical applications, advanced polymer synthesis, and emerging material science domains presents a compelling growth opportunity for dibromo alkane compounds over the forecast period. Dibromo methane, for example, is employed as a high-density solvent and synthesis intermediate for novel materials including high-performance coatings, semiconductor precursors, and photovoltaic cell manufacturing.

The American Chemical Society (ACS) has reported growing academic and industrial investment in advanced materials chemistry, supported by government funding programs in the U.S., Germany, and Japan. Furthermore, the European Flame Retardants Association (EFRA) has highlighted increasing adoption of technically advanced, compliant brominated flame retardants in defense textiles, transportation components, and data center infrastructure, broadening the end-use landscape and unlocking substantial incremental revenue streams for dibromo alkane market participants.

Category-wise Analysis

Product Type Insights

Dibromo methane commands the leading position within the product type segment, accounting for approximately 41% of the global dibromo alkane market in 2026. Its dominance is underpinned by its extensive and diversified utility as a chemical intermediate, laboratory reagent, and high-density solvent across pharmaceutical synthesis, mineral processing, and specialty chemical manufacturing. Dibromo methane (CH?Br?) is widely employed in Reformatsky reactions and Simmons-Smith cyclopropanation chemistries, making it a staple reagent in organic synthesis laboratories and industrial-scale API manufacturing.

Published data from the American Chemical Society (ACS) and peer-reviewed research journals consistently document its broad applicability across chemical disciplines. Importantly, its relatively more favorable regulatory acceptance profile compared to other dibromo alkane variants, particularly under current REACH assessments in Europe, facilitates continued procurement by pharmaceutical companies and specialty chemical manufacturers across North America and Europe, reinforcing its sustained market leadership.

Application Insights

The chemicals segment holds the dominant share in the application category, representing approximately 35% of the total dibromo alkane market revenue in 2026. This leadership position is anchored in the widespread use of dibromo alkane compounds as intermediates for flame-retardant synthesis, specialty chemical production, dye manufacturing, and polymer modification.

The global flame retardants industry, a major consumer of brominated chemical intermediates, has experienced consistent growth driven by fire safety mandates enforced by the National Fire Protection Association (NFPA) in the United States and the Building Research Establishment (BRE) in the United Kingdom, among other regulatory bodies.

Regional Analysis

North America Dibromo Alkane Market Trends and Insights

North America represents a mature yet strategically vital market for dibromo alkanes, shaped by robust demand from the U.S. pharmaceutical sector, specialty chemical manufacturers, and flame-retardant producers. Compliance obligations under EPA guidelines and continued R&D investment in advanced chemical intermediates are directing market activity toward technically superior, low-toxicity brominated formulations, maintaining a steady demand base across the region's well-established industrial chemical infrastructure.

U.S. Dibromo Alkane Market Size

The United States accounts for approximately 70–75% of total North American dibromo alkane revenues. Demand is underpinned by pharmaceutical API production, flame retardant manufacturing, and specialty laboratory chemical procurement. Albemarle Corporation, leveraging domestic bromine reserves in Arkansas, sustains a competitive supply advantage, supporting consistent product availability and pricing stability for downstream industrial consumers across the country.

Europe Dibromo Alkane Market Trends and Insights

Europe's dibromo alkane market is characterized by tightening compliance requirements under REACH and RoHS directives, which have simultaneously restricted legacy compound usage and stimulated innovation in compliant brominated formulations. Germany, the United Kingdom, and France remain principal consumption hubs, supported by pharmaceutical synthesis activity, specialty chemical manufacturing, and demand for technically advanced flame-retardant intermediates compliant with updated ECHA standards.

Germany Dibromo Alkane Market Size

Germany commands approximately 28% of the European dibromo alkane market, supported by its deep-rooted chemical manufacturing base and pharmaceutical sector. Lanxess AG, headquartered in Cologne, remains a strategic regional supplier of specialty bromine derivatives. Demand from Germany's automotive, electronics, and pharmaceutical industries reinforces consistent procurement of dibromo alkane intermediates across both industrial and laboratory-grade applications.

U.K. Dibromo Alkane Market Size

The United Kingdom accounts for approximately 18% of European dibromo alkane revenues. The country's pharmaceutical manufacturing and contract research organization (CRO) sector drives steady demand for laboratory-grade reagents, including dibromo methane. Post-Brexit, the adoption of UK REACH as an independent regulatory framework has maintained compliance-driven procurement standards, supporting a stable, quality-focused market for specialty dibromo alkane products.

France Dibromo Alkane Market Size

France represents approximately 14% of the European dibromo alkane market. Its established agrochemical and specialty chemical industries create consistent demand for dibromo alkane intermediates. Heightened focus on fire safety construction materials following high-profile building safety incidents across Europe has reinforced regulatory-driven demand for approved flame-retardant chemical intermediates within the French industrial and construction chemical supply chains.

Asia Pacific Dibromo Alkane Market Trends and Insights

Asia Pacific leads the global dibromo alkane market with approximately 40% of total share in 2026, driven by large-scale chemical production in China, expanding pharmaceutical API manufacturing in India, and rising industrial chemical demand across Southeast Asia. China serves as both a major producer and consumer, with companies including Zouping Mingxing Chemical Co. Ltd. and Alfa Aesar (China) Chemical Co. Ltd. forming integral nodes within regional and global supply chains.

India Dibromo Alkane Market Size

India holds approximately 20% of the Asia Pacific dibromo alkane market, propelled by rapid pharmaceutical and agrochemical sector expansion. The country's PLI scheme for bulk drugs and growing export-oriented API manufacturing creates direct incremental demand. Domestic producers including Neogen Chemicals Ltd and Mody Chemi Pharma Limited, are well-positioned to capitalize on rising domestic and export demand for bromine-derived chemical intermediates.

Japan Dibromo Alkane Market Size

Japan contributes approximately 12–14% of Asia Pacific revenues, characterized by high-value demand from precision pharmaceutical and specialty chemical manufacturing. Tosoh Corporation and Tokyo Chemical Industry Co., Ltd. are key domestic producers supplying laboratory-grade and industrial-grade dibromo alkane compounds. Japan's advanced electronics sector further supports demand for brominated flame-retardant precursor chemicals through the forecast period.

Southeast Asia Dibromo Alkane Market Size

Southeast Asia accounts for approximately 12% of the Asia Pacific dibromo alkane market revenues, with Indonesia, Vietnam, and Thailand emerging as key demand growth contributors. Government-led initiatives to attract pharmaceutical and specialty chemical manufacturing investments, combined with growing domestic agrochemical usage, are expected to accelerate incremental dibromo alkane consumption across the subregion.

Competitive Landscape

The global dibromo alkane market exhibits a moderately consolidated competitive structure, with established multinational players competing alongside cost-competitive regional manufacturers. Leaders such as Albemarle Corporation, Israel Chemicals Limited (ICL), and Lanxess AG maintain significant positions through vertically integrated bromine-to-specialty-chemical supply chains, proprietary production technologies, and extensive global distribution networks.

Emerging producers in India and China are intensifying competitive pressure through cost-efficient manufacturing and expanding export capabilities. Differentiation strategies increasingly focus on regulatory compliance, development of low-toxicity formulations, capacity investments in Asia, and strategic partnerships with pharmaceutical API manufacturers to secure long-term supply agreements.

Key Developments:

- In March 2024, Albemarle Corporation announced targeted investments to optimize its bromine derivatives production facilities in the United States, aimed at enhancing output of specialty chemical intermediates including halogenated compounds to serve growing pharmaceutical and flame-retardant market demand.

- In January 2024, Neogen Chemicals Ltd commissioned an expanded bromine chemistry manufacturing unit at its Dahej, Gujarat facility in India, significantly increasing production capacity for dibromo and multi-bromo derivatives to serve pharmaceutical and agrochemical export markets.

- In September 2023, Israel Chemicals Limited (ICL) announced a research collaboration with European specialty chemical partners to develop next-generation, REACH-compliant brominated flame-retardant intermediates, targeting replacement of compounds restricted under updated EU SVHC regulations.

Global Dibromo Alkane Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 528.8 Million |

|

Current Market Value (2026) |

US$ 676.8 Million |

|

Projected Market Value (2033) |

US$ 946.0 Million |

|

CAGR (2026-2033) |

4.9% |

|

Leading Region |

Asia Pacific, 40% market share (2026) |

|

Dominant Product Type |

Dibromo Methane, 41% market share (2026) |

|

Top-ranking Application |

Chemicals, ~35% market share (2026) |

|

Incremental Opportunity |

US$ 269.2 Million |

Companies Covered in Dibromo Alkane Market

- Mody Chemi Pharma Limited

- Dhruv Chem Industries

- Israel Chemicals Limited

- Albemarle Corporation

- Lanxess AG

- Tosoh Corporation

- Sontara Organo Industries

- Nova International

- Neogen Chemicals Ltd

- Tokyo Chemical Industry Co., Ltd.

- Zouping Mingxing Chemical Co. Ltd.

- Alfa Aesar (China) Chemical Co. Ltd.

- Aarnee International Pvt. Ltd.

- Central Drug House Private Limited

Frequently Asked Questions

The global Dibromo Alkane market is projected to be valued at US$ 676.8 million in 2026. The market is expected to grow at a CAGR of 4.9% between 2026 and 2033, reaching US$ 946.0 million by 2033.

Primary demand drivers include the expanding use of dibromo alkane compounds as intermediates in pharmaceutical API synthesis and brominated flame-retardant manufacturing, rising fire safety regulatory mandates from agencies such as the NFPA and EU CPR, and growing agrochemical consumption driven by the FAO-documented increase in global food production needs across developing economies in Asia and Africa.

Asia Pacific leads the global dibromo alkane market, accounting for approximately 40% of total market share in 2026. The region's leadership is sustained by large-scale chemical and pharmaceutical manufacturing in China and India, growing specialty chemical investments in Southeast Asia, and the presence of key producers including Neogen Chemicals Ltd, Zouping Mingxing Chemical Co. Ltd., and Tosoh Corporation.

A high-value opportunity exists in the rapidly scaling pharmaceutical API manufacturing infrastructure across India and Southeast Asia, supported by government-backed production incentive schemes including India's PLI scheme for bulk drugs and capacity expansion investments by regional producers.

Key companies operating in the global dibromo alkane market include Albemarle Corporation, Israel Chemicals Limited (ICL), Lanxess AG, Neogen Chemicals Ltd, Tosoh Corporation, Tokyo Chemical Industry Co., Ltd., Mody Chemi Pharma Limited, and Zouping Mingxing Chemical Co. Ltd., among others.