- Food Ingredients & Additives

- Dessert Flavor Market

Dessert Flavor Market Size, Share, and Growth Forecast 2026 - 2033

Dessert Flavor Market by Flavor Profile (Vanilla, Chocolate, Fruit & Nut), Flavor Nature (Natural, Synthetic), Flavor Form (Liquid & Gel, Dry & Powder), Application (Confectionery, Dairy & Frozen, Bakery), Consumer Trends, and Regional Analysis 2026 - 2033

Dessert Flavor Market Share and Trends Analysis

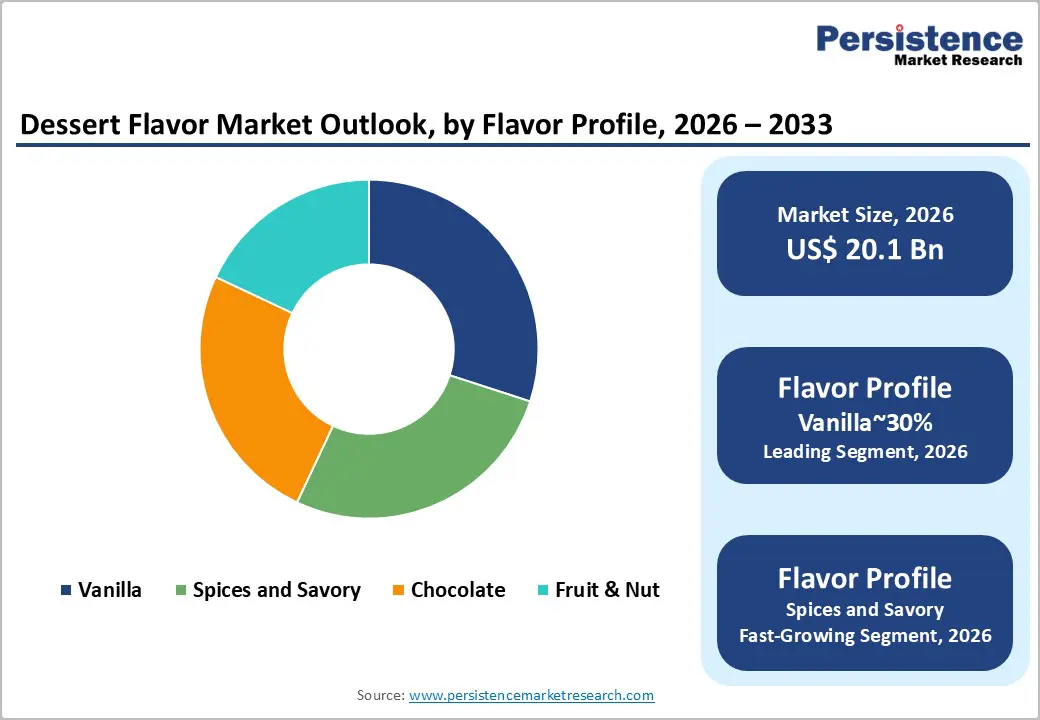

The global dessert flavor market size is likely to be valued at US$20.1 billion in 2026 and is projected to reach US$28.3 billion by 2033, growing at a CAGR of 5.0% during the forecast period between 2026 and 2033, driven by the growing desire for nostalgic, comfort-driven flavors (such as brown butter and traditional vanilla) alongside a rising interest in bold, exotic, and swicy (sweet and spicy) flavor combinations.

Shifting consumer preferences are also favoring botanicals and frozen desserts, while liquid and gel forms continue to dominate, despite the rise of powder-based options. Innovation in spices and savory profiles is further driving growth within specific market segments.

Key Industry Highlights:

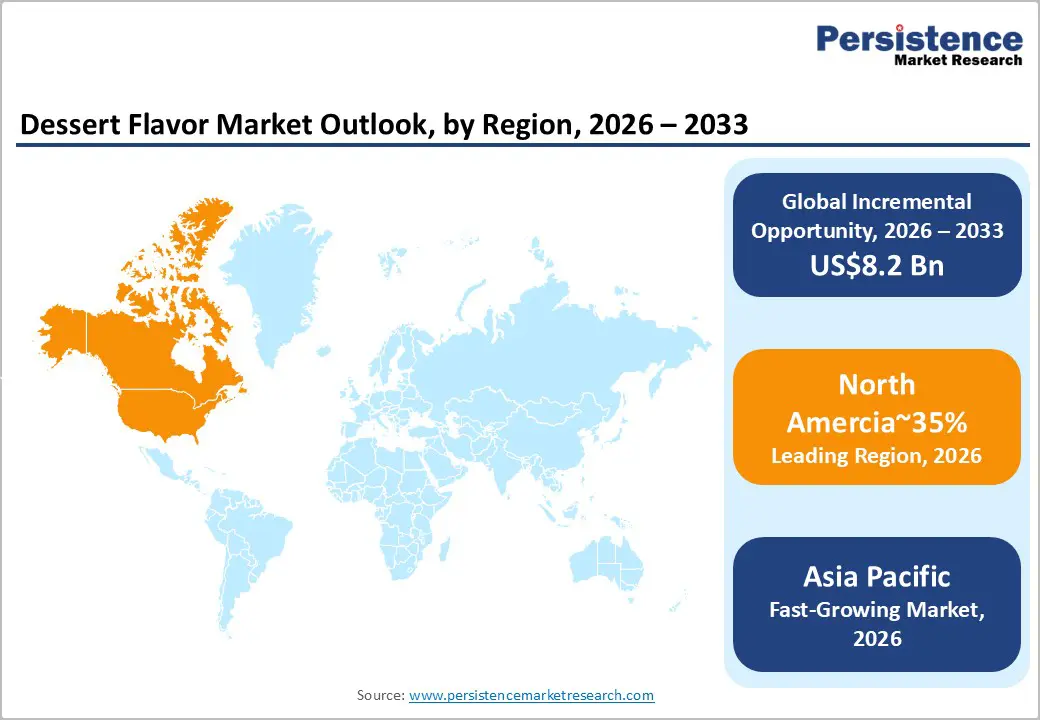

- Leading Region: North America is anticipated to lead the dessert flavor market with approximately 35% share, supported by mature consumption patterns, regulatory rigor, high adoption of natural and clean-label ingredients, and advanced manufacturing infrastructure that ensures consistent quality and reliable supply chains.

- Fastest-growing Region: Asia Pacific is expected to be the fastest-growing region, driven by rapid urbanization, expanding middle-class consumption, adoption of Western-style bakery and chocolate, and rising preference for regional flavors such as matcha, mango, and red bean.

- Leading Flavor Profile: Vanilla is expected to remain the leading flavor profile with around 30% share, functioning as a structural indulgence anchor across beverages, baked goods, and confectionery.

- Leading Application: Confectionery is expected to lead with approximately 42% market share, reflecting high-volume consumption, repeat purchases, and structural reliance on high-intensity flavor systems across mass-market and premium tiers.

- Key Industry Developments: In November 2024, Kerry Group sold its Dairy Ireland business for €500 million (US$530 million), finalizing its shift to a pure-play Taste & Nutrition leader. This move enabled Kerry to invest in high-growth "clean-label" and functional dessert segments, including its LactoSens acquisition, which offers manufacturers solutions for low-sugar, lactose-free desserts with a traditional mouthfeel.

| Key Insights | Details |

|---|---|

|

Dessert Flavor Market Size (2026E) |

US$20.1 Bn |

|

Market Value Forecast (2033F) |

US$28.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.6% |

Market Dynamics - Driver, Barrier, and Opportunity Analysis

Flavor-Enabled Indulgence as a Structural Demand

Consumer behavior in indulgent categories is being reshaped by a permissible indulgence framework, where emotional comfort is pursued without overt nutritional trade-offs. This shift is reinforcing demand for flavor systems that signal sweetness and warmth while enabling formulation restraint. Vanilla, caramel, and cinnamon profiles function as cognitive cues, anchoring perceptions of indulgence even as sugar and fat inputs are compressed.

Regulatory pressure on sugar disclosure, combined with retailer clean-label requirements, is intensifying adoption of these profiles across desserts. As a result, flavors are no longer merely decorative additives but structural levers that influence calorie perception, portion tolerance, and repeat-purchase behavior within value-sensitive indulgence segments.

From a functional perspective, flavor development is converging with sensory science to replicate the hedonic impact of sugar and fat. Sweet brown flavor architectures manipulate aroma release and temporal taste perception, allowing manufacturers to reduce sugar content by meaningful margins without eroding consumer satisfaction. This capability is reshaping margin structures by lowering dependence on volatile sweetener inputs while preserving premium positioning.

However, execution risk remains uneven, as overuse can trigger artificiality cues and regulatory scrutiny. Competitive advantage, therefore, accrues to suppliers with sensory models, compliant ingredient sourcing, and the scale to standardize the delivery of indulgence across formats.

Raw Material Supply Chain Volatility

The flavor industry remains structurally exposed to volatility in crop-based raw materials, particularly vanilla, cocoa, spices, and nuts, which are concentrated in a limited number of climate-sensitive and geopolitically exposed sourcing regions. Increasing weather unpredictability, combined with localized political and logistical disruptions, continues to destabilize the availability and consistency of procurement.

This dependency introduces planning uncertainty across the value chain, complicating long-term contracting, inventory management, and formulation standardization for manufacturers operating at scale.

Cost instability in natural extracts further constrains market expansion, as sharp input price movements compress margins and reduce pricing flexibility. While synthetic alternatives offer partial insulation, their adoption is limited by clean-label mandates and shifting consumer expectations, narrowing substitution options.

Smaller and mid-sized players are disproportionately impacted, as limited sourcing diversification and lower bargaining power restrict their ability to absorb cost shocks. As a result, supply chain volatility acts as a structural restraint, slowing the participation of new entrants and reinforcing scale-driven competitive advantages within the market.

AI-Enabled Predictive Flavor Development

The integration of artificial intelligence into flavor formulation is emerging as a structurally significant opportunity, reshaping how innovation is identified, validated, and commercialized.

Advanced models can synthesize large-scale consumer feedback, social discourse, and sensory databases to identify emerging taste preferences before they mature into mainstream demand. This capability shifts flavor development from reactive trend-following to anticipatory design, thereby improving alignment between consumer expectations and product launch timing.

As indulgent categories become increasingly crowded, the ability to algorithmically detect subtle preference inflections strengthens portfolio relevance and reduces innovation failure rates at the market level.

AI-driven formulation accelerates development by streamlining compound selection, sensory optimization, and iteration cycles. This fusion of data science and flavor chemistry is reshaping competitive dynamics, favoring suppliers with digital infrastructure, proprietary data, and scalable platforms.

As adoption grows, predictive flavor development will shift from a differentiator to a baseline capability. In April 2025, Symrise launched "Symvision AI" at World Vanilla Day to predict future trends in vanilla confectionery, marking a shift from reactive to predictive development and reducing R&D lead times for seasonal dessert launches.

Content–wise Analysis

Flavor Profile Insights

Vanilla flavor is expected to remain the leading segment with a share of around 30%, reflecting its structural role as the default indulgence anchor across dessert and beverage formulations. Its dominance is reinforced by unmatched versatility, enabling seamless use across ice creams, flavored milk, baked goods, and confectionery without formulation complexity.

Vanilla functions both as a standalone profile and as a flavor enhancer, rounding chocolate, caramel, and fruit notes while masking off-notes in reduced-sugar and plant-based recipes. This makes it especially valuable in clean-label reformulation strategies.

Brands such as Symrise, with its SymVan Supreme range, and Nielsen-Massey, with its premium bourbon vanilla extract, illustrate how origin-specific sourcing and high-purity extraction support premiumization and traceability.

McCormick Pure Vanilla further demonstrates vanilla’s scalability across retail and foodservice, reinforcing its position as a low-risk, high-dependability flavor foundation.

Spices and savory flavors are likely to be the fastest-growing segment, driven by the rise of experiential eating and global fusion trends in desserts, snacks, and beverages. Sweet-and-spicy combinations such as chili-chocolate, mango-habanero, and cardamom-caramel are gaining traction as brands target adventurous palates.

This segment also benefits from functional formulation needs, including sodium reduction, where umami-rich profiles, such as mushroom or miso, enhance depth without added salt.

Givaudan’s savory flavor systems for plant-based applications and Kerry Group’s customized spice blends for snacks and foodservice highlight industrial-scale adoption.

Premium spice brands such as Orika underscore growing consumer interest in authentic regional flavors such as saffron, tamarind, and ginger, positioning spices and savory notes as a key growth engine for differentiated, high-impact flavor innovation.

Application Insights

The confectionery segment is expected to lead with a 42% share, driven by high-volume categories such as candy, chocolates, and gums that rely on high-intensity flavor systems.

Its dominance is reinforced by the structural scale of global confectionery consumption, which provides stable demand and predictable formulation requirements. The segment benefits from established manufacturing processes, repeat purchase behavior, and portfolio integration across both mass-market and premium tiers, ensuring revenue reliability.

Texture-forward innovations, such as Ferrara’s Nerds Juicy Gummy Clusters, combine crunchy shells with soft centers, reinforcing multi-sensory appeal. Premium offerings like Lindt’s Dubai-Style Chocolate Bar further show how pistachio, nut pastes, and pastry inclusions elevate traditional chocolate matrices while maintaining formulation reliability and global scalability.

High adoption of core flavors such as chocolate and vanilla further solidifies its leadership, while ongoing innovation in mix-ins and textures sustains its relevance in competitive markets.

Frozen desserts are projected to be the fastest-growing subsegment, fueled by non-dairy innovations, novel textures, and inclusion-based experimentation that necessitate specialized, heat- and cold-stable flavor systems.

Driven by non-dairy formulations that closely replicate the creaminess and flavor release of conventional ice cream. Brands such as Ben & Jerry’s oat-based Chocolate Chip Cookie Dough highlight how neutral cereal notes from oats support classic chocolate and vanilla inclusions.

Häagen-Dazs vegan ice cream sandwiches leverage rich cocoa and coconut fat systems to preserve indulgent mouthfeel, while Talenti Roman Raspberry Sorbetto emphasizes fruit-forward acidity and freshness using high fruit content. Oatly’s collaborations with Shake Shack and KFC China demonstrate that oat-based frozen custards deliver clean, dairy-like sweetness across foodservice channels.

Precision fermentation players like Perfect Day further enhance realism by enabling authentic dairy flavor notes in animal-free bases. Together, these products underscore how taste fidelity, smooth texture, and indulgent inclusions position non-dairy frozen desserts as a key innovation engine.

Regional Insights

North America Dessert Flavor Market

North America is expected to lead the flavor market with an estimated 35% share in 2026, reflecting its maturity, regulatory rigor, and established consumption patterns. The region benefits from advanced manufacturing infrastructure, high adoption of clean-label and naturally derived ingredients, and structured distribution networks that enable consistent product quality.

Consumer demand is anchored by nostalgic flavors, including s’mores, birthday cake, and cookie dough, which dominate confectionery and frozen dessert categories. The Free-From movement, encompassing gluten-free and dairy-free products, further reinforces flavor modulation requirements, creating structural opportunities for compliant flavor systems.

Regulatory oversight, particularly FDA monitoring of synthetic dyes and artificial additives, continues to accelerate adoption of natural alternatives and ensures alignment with evolving health standards, reinforcing market stability and strategic predictability.

Investment activity in North America is concentrated on mid-sized flavor manufacturers specializing in organic and non-GMO-certified supply chains, strengthening supply security and portfolio differentiation. This focus complements infrastructure maturity and premium market adoption while mitigating raw material risks.

Collectively, these dynamics position the region as both a stable revenue base and a platform for innovation-led expansion, with regulatory and consumer frameworks shaping both competitive entry and growth potential.

Europe Dessert Flavor Market

Europe is expected to rank as the second-largest region with a strong focus on premiumization and provenance-driven consumption. Key markets, including Germany, France, and the UK, exhibit a preference for sophisticated and subtle flavor profiles, underpinned by high-quality ingredients such as Sicilian lemon and Belgian chocolate.

Market leadership is reinforced by advanced infrastructure, widespread adoption of certified sourcing by retailers, and consumer willingness to pay a premium for ethically sourced flavors. Sustainability considerations, particularly Fair Trade and Rainforest Alliance certifications, structurally shape purchasing behavior, embedding environmental and social compliance into product strategies and value chains.

Regulatory rigor is a defining factor, with the European Food Safety Authority enforcing strict additive guidelines that effectively restrict certain synthetic compounds permitted elsewhere. This regulatory landscape drives structural reliance on natural and nature-identical extracts while limiting the availability of low-cost alternatives.

Consequently, Europe combines high-margin, premium-oriented demand with a compliance-driven supply chain, creating a measured yet growth-oriented regional outlook. Innovation is concentrated in ethical sourcing and product differentiation, sustaining competitive positioning within the mature European market.

Asia Pacific Dessert Flavor Market

Asia Pacific is likely to be the fastest-growing region, driven by rapid urbanization, expanding middle-class consumption, and increasing adoption of processed desserts. Key markets, including China, India, and Japan, exhibit a dual dynamic: a rising preference among younger consumers for Western-style bakery and chocolate products, alongside sustained demand for regionally adapted flavors such as matcha, taro, red bean, and mango.

Structural growth is reinforced by policy support favoring natural ingredients, import duty reductions, and evolving regulatory frameworks that encourage compliance-aligned innovation. Manufacturing infrastructure in China and India provides cost-efficient production of synthetic and nature-identical flavors, enhancing accessibility for both domestic and export markets.

Regional expansion is further supported by foreign direct investment, with global flavor houses establishing R&D centers and production facilities to capitalize on scale advantages.

Fragmented local markets are progressively consolidating, creating structurally favorable conditions for supply-chain integration and innovation-led differentiation. Additional opportunities emerge in dry and powdered formats, which align with convenience-oriented applications and rapid growth in the bakery and frozen dessert sectors, strengthening the Asia Pacific’s competitive and revenue-generating profile.

Competitive Analysis

The global dessert flavor market is moderately consolidated, with top players, such as Givaudan, Symrise, and IFF, controlling approximately 55–60% of the total market value. Market concentration is the strongest in high-tech natural extraction, where R&D intensity and integrated supply chains create a durable competitive advantage.

Leading firms compete through total-solution offerings, combining flavor, texture, and nutritional modulation, while regional boutique houses focus on agile, bespoke, and small-batch creations to serve niche organic or ethnic profiles.

Strategic activity reinforces consolidation at the top. Givaudan launched a vanilla-botanical hybrid to boost clean-label frozen dessert sales, Symrise acquired a spice company to expand its savory portfolio in Asia, and IFF expanded its India facility for dry powders, capturing incremental APAC share.

Future market dynamics are expected to emphasize innovation-led differentiation, regional expansion, and integrated sensory solutions, sustaining barriers for smaller entrants while enabling premium positioning for established global players.

Key Industry Developments:

- In February 2025, International Flavors & Fragrances (IFF) unveiled its 2025 trend forecast, identifying "Banana Pudding" and "Brown Butter" as key growth drivers. The inclusion of specific dessert profiles like Brown Butter signaled a market shift toward "savory-sweet" hybrids, enabling brands to command premium pricing through "culinary-inspired" sophistication.

- In January 2025, Givaudan launched the "Guardians of Memories" Digital Initiative to co-create flavors based on emotional and nostalgic consumer data. By utilizing the "Myromi" handheld aroma technology, Givaudan enabled "hyper-personalization" in desserts, allowing manufacturers to customize flavor intensity according to specific regional taste memories.

Companies Covered in Dessert Flavor Market

- Givaudan

- Symrise AG

- International Flavors & Fragrances

- DSM Firmenich

- ADM Archer Daniels Midland

- Sensient Technologies

- Takasago International

- T. Hasegawa

- Robertet Group

- Synergy Flavors

- Blue Pacific Flavors

- Flavorchem

- Huabao International

- Bell Flavors

- Flavoursum

Frequently Asked Questions

The global dessert flavor market is projected to be valued at US$20.1 billion in 2026 and is expected to reach US$28.3 billion by 2033, supported by rising demand for premium, nostalgic, and botanical dessert profiles across food applications.

Consumer demand is evolving due to a strong preference for clean-label and natural ingredients, rising interest in nostalgic comfort flavors, and increasing experimentation with exotic, botanical, and sweet-spicy combinations in desserts.

The dessert flavor market is expected to grow at a CAGR of 5.0% between 2026 and 2033, driven by innovation in flavor formulation, AI-led trend forecasting, and the expansion of frozen and plant-based dessert categories.

The fastest growth opportunities are emerging in Asia Pacific, supported by expanding packaged food consumption, urbanization, evolving taste preferences, and increasing adoption of modern bakery, dairy, and frozen dessert products.

Key players include Givaudan, Symrise AG, International Flavors & Fragrances, DSM-Firmenich, Archer Daniels Midland, Sensient Technologies, Takasago International, Robertet Group, T. Hasegawa, Synergy Flavors, Huabao International, Bell Flavors, and Flavorchem.