- Beverages

- Dairy-Free Oat Bedtime Drink Market

Dairy-Free Oat Bedtime Drink Market Size, Share, and Growth Forecast 2026 – 2033

Dairy-Free Oat Bedtime Drink Market by Product Type (Unsweetened, Plain/Original, Sweetened), Source Type (Conventional, Organic), Packaging Type (Cartons, Bottles, Cans), Flavor Profile (Natural, Others), Distribution Channel, and Regional Analysis 2026 – 2033

Dairy-Free Oat Bedtime Drink Market Size and Trends Analysis

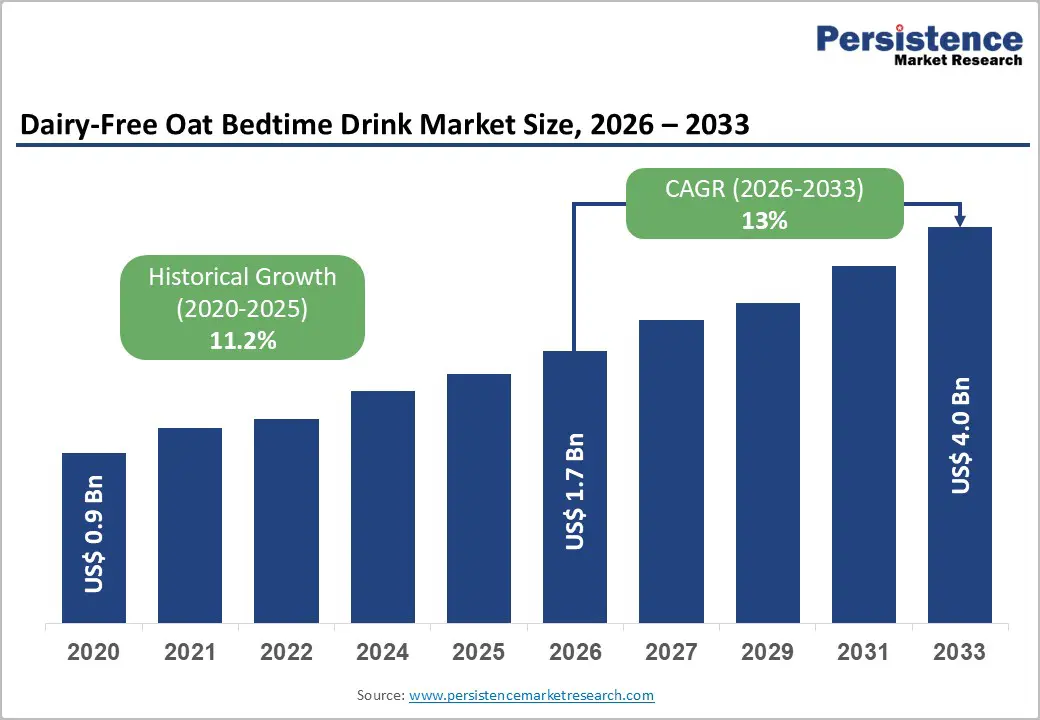

The global dairy-free oat bedtime drink market size is likely to be valued at US$1.7 billion in 2026 and is expected to reach US$4.0 billion by 2033, growing at a CAGR of 13% during the forecast period from 2026 to 2033, driven by increasing demand for plant-based functional drinks that promote sleep, thanks to the tryptophan in oats, which helps elevate serotonin and melatonin levels. This growth is also driven by the widespread occurrence of lactose intolerance worldwide and the perceived environmental advantages of oat farming compared with almond or dairy production.

Key Industry Highlights

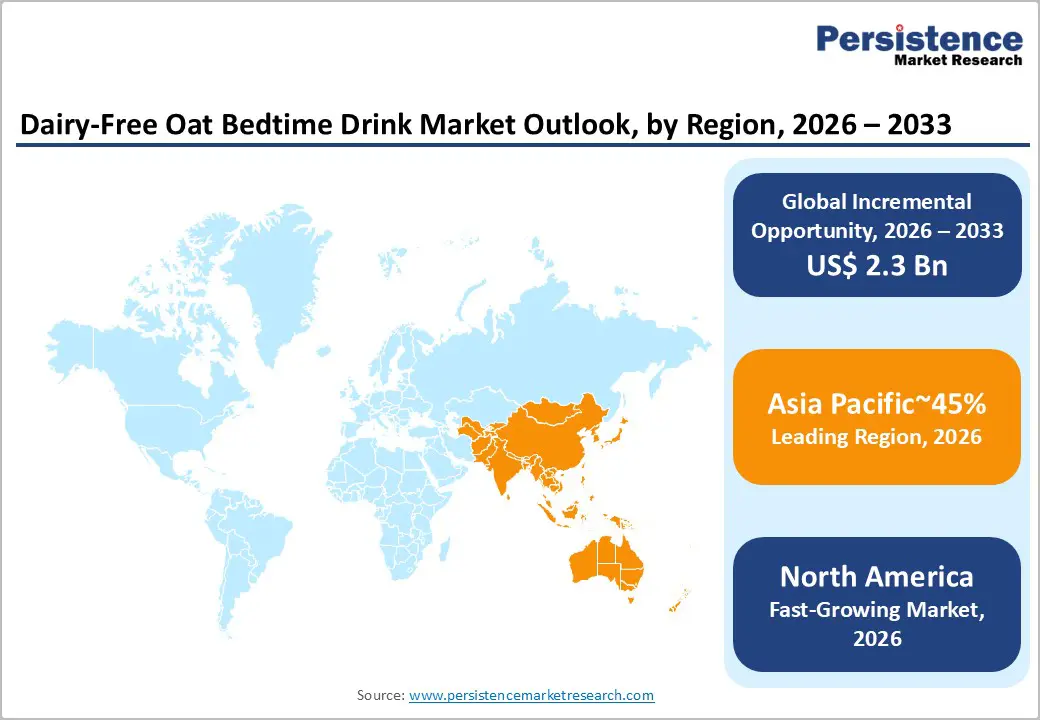

- Leading Region: Asia Pacific is expected to lead with approximately 45% of revenue in 2026, anchored by cultural integration, functional beverage ecosystems, and strong e-commerce adoption in China, India, and East Asia.

- Fastest-growing Region: North America, driven by high per-capita consumption, functional product innovation, and oat bedtime normalization in the U.S. and Canada.

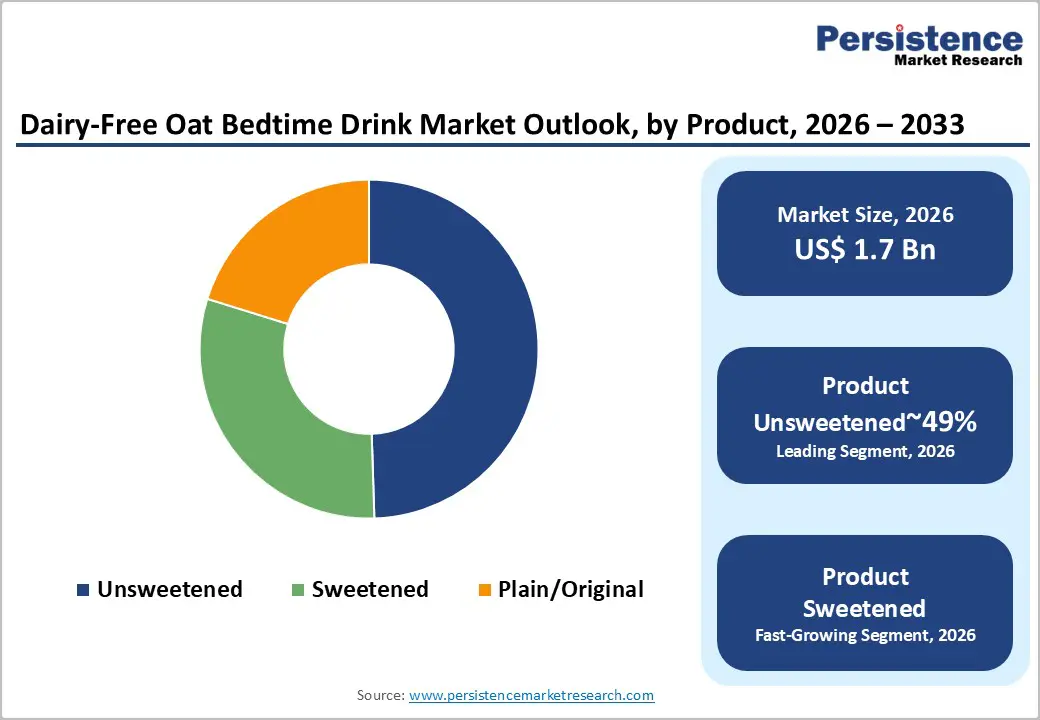

- Leading Product Type: Unsweetened oat milk is expected to be the leading segment, accounting for approximately 49% of the global demand, driven by health-first positioning, clean-label preference, and suitability for bedtime routines.

- Leading Distribution Channel: Off-trade channels are expected to dominate distribution at roughly a 92% share, underscoring the largely home-based nature of bedtime oat drink consumption.

- Key Industry Development: In September 2025, Organic Valley launched two new organic oat beverages free from gums and seed oils, catering to health-conscious consumers seeking clean-label, natural options for everyday or evening consumption.

| Global Market Attributes | Key Insights |

|---|---|

| Dairy-Free Oat Bedtime Drink Market Size (2026E) | US$1.7 Bn |

| Market Value Forecast (2033F) | US$4.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13% |

| Historical Market Growth (CAGR 2020 to 2025) | 11.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Plant-based Nutrition Demand and the Wellness-Sleep Nexus

The surge in consumer demand for plant-based nutrition is a primary driver shaping the dairy-free oat bedtime drink market. Modern consumers increasingly seek functional beverages that deliver tangible health benefits alongside ethical and environmental alignment. Oats, naturally rich in beta-glucans and tryptophan, support cardiovascular wellness, digestive health, and the regulation of serotonin and melatonin, making them ideal for improving sleep quality. Heightened awareness of lifestyle-related health conditions, including obesity and sleep disorders, has shifted bedtime routines toward natural, food-based interventions. This evolution positions oat drinks not just as a hydration option but as an integrated wellness tool, reflecting a broader behavioral trend toward preventive health and holistic nutrition.

Beyond nutrition, bedtime oat drinks align with rising demand for ethical and sustainable products, as oats require far fewer land and water resources than dairy. The segment also benefits from a shift away from pharmaceutical sleep aids toward natural solutions that offer both comfort and functional support. By blending efficacy with ritual, oat-based bedtime drinks are moving from niche wellness products into everyday routines. This trend is reflected in Oatside’s May 2025 launch of a matcha oat latte with high-dose L-theanine, positioned to support calmness, stress reduction, and sleep health.

Cost Barriers and Sensory Limitations

The dairy-free oat bedtime drink market is constrained by premium pricing and high production costs. Specialized processes such as enzymatic hydrolysis for natural sweetness and the use of premium adaptogens elevate prices well above conventional dairy and standard oat milk, creating a “vegan tax” that limits mass adoption, especially in price-sensitive regions. In developing markets, consumers may continue to prefer cheaper traditional sleep aids or regular milk. Volatile oat prices and complex milling and enzyming processes further raise costs, restricting scalability, discouraging smaller entrants, and reinforcing market concentration among premium producers.

Beyond pricing, product stability and sensory limitations pose notable adoption challenges. Clean-label formulations often have shorter refrigerated shelf lives, complicating distribution and retail logistics, while perceptions of graininess or uneven texture deter a segment of consumers. Competing plant-based alternatives, such as almond or soy milk, which offer a smoother mouthfeel, further intensify competitive pressures. Without ongoing innovation in taste, texture, and shelf-life optimization, consumer hesitancy may persist, slowing mainstream adoption and preventing the market from fully capitalizing on the rising demand for functional, plant-based bedtime beverages.

Ready-to-Heat and Ready-to-Drink Formats Capturing the Sleep Economy

The convergence of convenience culture and the expanding sleep economy is reshaping the dairy-free oat bedtime drink market, creating a high-impact opportunity in Ready-to-Heat (RTH) and Ready-to-Drink (RTD) formats. As urban lifestyles become increasingly time-constrained, consumers are deprioritizing labor-intensive nighttime rituals in favor of solutions that deliver relaxation with minimal effort. The shift away from powders toward RTH and RTD products directly addresses this friction point, transforming bedtime nutrition into a seamless, low-effort wellness habit. This evolution aligns with broader consumption trends where functionality, speed, and consistency outweigh customization, particularly among professionals, frequent travelers, and digitally native consumers.

Technological and packaging innovations are driving the shift towards bedtime oat drinks. Microwave-safe, high-barrier cartons allow for direct heating, while self-heating containers expand consumption to travel hubs and hotels. Shelf-stable RTD formats move these drinks from niche health aisles to high-traffic areas such as cafés and convenience stores. Subscription models targeting busy professionals help reinforce daily habits, integrating the drinks into “desk-to-bed” routines. These convenient formats offer a premium margin and position RTH and RTD oat drinks as a high-value segment in functional beverages. This trend is already emerging, as seen with Oatly’s limited-edition hot cocoa oat drink for the festive season.

Category–wise Analysis

Product Type Insights

Unsweetened oat milk is expected to remain the leading product type, accounting for approximately 49% of total demand in 2026. Its dominance is rooted in the health-first framing of bedtime consumption, where minimizing added sugars is a critical decision driver. Consumers increasingly link late-evening sugar intake with blood glucose volatility and compromised sleep quality, reinforcing unsweetened formulations as the default choice for nighttime use. This preference is further amplified by the clean-label movement, as buyers prioritize short ingredient lists, transparency, and the absence of hidden sugars. Beyond direct consumption, unsweetened oat milk offers functional versatility, serving as a neutral base for nighttime routines such as warm oatmeal, golden milk, or savory preparations. For manufacturers, unsweetened SKUs function as portfolio anchors, delivering stable baseline volumes, reducing reformulation risk amid tightening sugar disclosure requirements, and acting as the reference point for subsequent flavored and functional line extensions.

Sweetened oat milk is projected to be the fastest-growing segment, driven by its repositioning from an everyday staple to a controlled indulgence within evening self-care rituals. Growth is fueled by flavor-led innovation in variants such as chocolate and vanilla, paired with natural or low-impact sweeteners such as monk fruit or stevia to maintain a “guilt-managed” profile. Rather than competing on nutritional minimalism, sweetened formulations increasingly emphasize emotional comfort, sensory satisfaction, and relaxation cues aligned with bedtime wind-down moments. This evolution allows brands to capture incremental consumption occasions and preimmunize the category, positioning sweetened oat milk as an intentional nighttime treat rather than a default beverage.

Distribution Channel Insights

Off-trade is estimated to dominate the distribution landscape with an estimated 92% share in 2026, reflecting the fundamentally domestic nature of bedtime oat drink consumption. The category is structurally aligned with supermarkets, hypermarkets, and grocery-led e-commerce because sleep-oriented beverages are embedded into private, end-of-day routines rather than out-of-home occasions. Consumers treat bedtime oat drinks as a repeat, nightly necessity, driving bulk purchases of multi-serve cartons during routine grocery trips. Cost efficiency further reinforces off-trade leadership, as pantry-format purchases deliver multiple servings at a fraction of the per-unit cost of on-trade consumption. Shelf-stable aseptic packaging strengthens this channel by enabling stockpiling without refrigeration constraints, particularly relevant for urban households with limited cold storage. Together, habitual purchasing behavior, price sensitivity, and storage convenience consolidate off-trade as the structural backbone of category volumes.

On-trade is expected represent the fastest growing distribution channel, supported by selective, experience-driven use cases rather than volume-led consumption. Growth is concentrated within cafés, hotels, and premium hospitality settings that are repositioning evening offerings around relaxation and wellness rituals. While cafés face structural barriers such as declining post-afternoon footfall and inventory complexity, hospitality-led environments are emerging as effective sampling engines. High-end hotels and wellness-focused properties are integrating decaffeinated oat-based nightcap beverages into minibars, room service menus, and lounge concepts, introducing consumers to bedtime formulations in controlled, premium contexts. These touchpoints influence subsequent off-trade purchasing behavior, creating a halo effect where on-trade acts as a trial and brand-building channel rather than a primary sales driver.

Regional Insights

Asia Pacific Dairy-Free Oat Bedtime Drink Market Trends

Asia Pacific is projected to remain the leading region in the global dairy-free oat bedtime drink, accounting for approximately 45% of the total revenue in 2026. The region’s leadership will be underpinned by structural dietary factors, rapid product localization, and the scaling of functional beverage ecosystems across East Asia, South Asia, and Southeast Asia. APAC will continue transitioning from a historically soy-centric non-dairy base toward oat-led formulations, driven by superior mouthfeel, beta-glucan health positioning, and compatibility with traditional evening consumption rituals. Demand growth will concentrate in urban consumption clusters, where stress management, sleep optimization, and preventative nutrition converge within daily routines.

China will anchor regional volume growth, supported by strong e-commerce penetration and aggressive product innovation from brands such as Vitasoy and Oatly. Oat-based sleep-positioned beverages will increasingly integrate low-sugar formulations and calming botanicals to align with post-90s consumer preferences. India will act as the primary growth engine, where brands such as Alt Co. and Urban Platter will scale culturally adapted oat bedtime drinks linked to Ayurvedic night rituals. Japan and South Korea will lead value growth through certified functional claims and premium packaging innovation, while Southeast Asia will expand trial and adoption via café-led barista-grade oat formats, reinforcing APAC’s structural dominance.

North America Dairy-Free Oat Bedtime Drink Market Trends

North America is projected to remain the fastest-growing region, driven by high per-capita consumption, rapid functional product innovation, and the normalization of oat-based beverages as part of daily nutrition routines. The market will continue shifting from daytime barista-led usage toward structured evening consumption, where oat drinks are positioned as sleep-supportive, low-sugar, and nutritionally functional alternatives to traditional dairy milk. Strong retail infrastructure, high consumer willingness to pay for value-added formulations, and advanced product differentiation will reinforce North America’s growth trajectory.

The U.S. will dominate regional performance, contributing the majority of revenue through mass-market scaling and functional fortification. Brands will increasingly position oat bedtime drinks with magnesium, adaptogens, and low-glycemic formulations to address rising sleep hygiene awareness. Planet Oat will benefit from its price-accessible strategy and dairy-aisle placement, driving household penetration at scale, while Califia Farms and Chobani will capture premium and crossover consumers seeking indulgent yet functional variants. Canada will support steady growth through sustainability-led consumption, where Earth’s Own will expand its share by leveraging domestic oat sourcing and clean-label positioning. Across the region, unsweetened and extra-creamy formats, carton-based packaging, and off-trade dominance will persist, while small-format ready-to-drink bedtime variants will expand through convenience and subscription channels, reinforcing North America’s role as the market’s innovation and growth engine.

Europe Dairy-Free Oat Bedtime Drink Market Trends

Europe is expected to remain a mature and value-dense market, with growth driven more by premiumization, sustainability compliance, and functional specialization than by volume expansion. The region will continue to act as the strategic benchmark for oat-based dairy alternatives, particularly in bedtime and wellness-oriented consumption. Regulatory alignment under EU food labeling, sustainability mandates, and sugar-reduction policies will push manufacturers toward unsweetened, fortified, and low-additive formulations. As a result, Europe’s market evolution will favour margin stability and product sophistication rather than rapid unit growth. Organic oat drinks will expand faster than conventional formats, supported by the EU Farm to Fork strategy and strong consumer association between organic sourcing and environmental stewardship.

Western Europe will anchor regional performance, with Germany, the U.K., and the Nordics shaping demand patterns. Germany will sustain leadership through scale, driven by hard-discount retail penetration and private-label oat products that normalize daily and evening consumption. Sustainability-led formats such as oat milk powders and low-packaging solutions will gain traction, benefiting brands such as Blue Farm. The U.K. will continue to lead functional innovation, particularly in sleep-oriented oat beverages fortified with adaptogens and fibre, where brands such as Alpro and Minor Figures will expand usage beyond coffee into structured evening rituals. The Nordics, led by Sweden and Finland, will reinforce premium trust-driven demand, with Oatly maintaining dominance through clean-label, no-sugar, and decaf-compatible oat formulations aligned with bedtime use. In October 2025, Minor Figures launched Regenerative Barista Oat Milk in the U.K., and sustainability-focused sourcing strengthens eco-trends in oat drinks, appealing to conscious consumers for daily and bedtime use.

Competitive Landscape

The global dairy-free oat bedtime drink market is moderately consolidated, with the top regional and global brands capturing a combined estimated share of 45–50%, while a long tail of local and niche players accounts for the remainder. Market leadership is concentrated in Asia Pacific, where brands such as Oatly, Planet Oat, Califia Farms, and Vitasoy dominate through distribution scale, product innovation, and functional positioning. Competitive advantage is primarily driven by formulation efficacy (tryptophan, beta-glucans, adaptogens), clean-label credentials, and sensory quality. Fragmentation persists in emerging regions, particularly in South and Southeast Asia, where smaller brands compete on localized flavours, price accessibility, and culturally adapted bedtime formulations, creating space for both premium and mass-market growth strategies.

Fragmentation is most pronounced in the specialty and functional niche, where new entrants capitalize on Direct-to-Consumer channels and subscription models to deliver high-value bedtime-focused formulations. Smaller players differentiate through flavor innovation, ready-to-drink convenience, and fortified ingredients such as adaptogens, magnesium, and L-Theanine. Across the market, competitive dynamics are increasingly defined by the integration of product efficacy, sensory experience, and lifestyle alignment, with incumbents maintaining advantage through brand trust, portfolio depth, and sustainability initiatives.

Key Industry Highlights

- In April 2025, Minor Figures launched the Hyper Oat range (Berry, Matcha, Turmeric, Mango flavors) with functional ingredients. This redefines plant-based milk expectations, driving growth in functional oat drinks that support health and potential evening routines.

- In March 2025, Minor Figures announced Hyper Oat functional oat drink innovations at Natural Products Expo West. The announcement highlights adaptogens and nootropics in oat-based beverages, creating opportunities for wellness positioning, including relaxation benefits.

- In January 2025, Minus Coffee launched a beanless instant oat milk latte with L-Theanine and pea protein. This functional product offers calm energy without a caffeine crash, presenting an opportunity for evening consumption in the dairy-free oat category.

Companies Covered in Dairy-Free Oat Bedtime Drink Market

- Oatly Group AB

- Danone S.A.

- Califia Farms

- Minor Figures

- Oatside

- Vitasoy International

- SunOpta Inc.

- PepsiCo Inc. (Quaker)

- Chobani

- Moma Foods

- Epigamia (Drum Foods)

- Freedom Foods Group

- Earth's Own

- The Hain Celestial

- Rude Health

Frequently Asked Questions

The global dairy-free oat bedtime drink market is projected to be valued at US$1.7 billion in 2026 and is expected to reach US$4.0 billion by 2033, driven by rising demand for plant-based functional beverages that support sleep.

Demand is fueled by the growing consumer focus on plant-based nutrition, the natural sleep-promoting properties of oats (rich in tryptophan), widespread lactose intolerance, and the perceived environmental benefits of oat farming compared to dairy or almond production.

The dairy-free oat bedtime drink market is forecast to grow at a CAGR of 13.0% from 2026 to 2033, reflecting strong adoption within the wellness and sleep economy.

Asia Pacific is the leading regional market, accounting for approximately 45% of revenue, due to structural dietary shifts, rapid product localization, and the scaling of functional beverage ecosystems across China, India, and Southeast Asia.

Key players include Oatly Group AB, Danone S.A. (Alpro/Silk), Califia Farms, Minor Figures, Oatside, and Vitasoy International. Competition is driven by formulation efficacy, clean-label credentials, and distribution scale.