- Pharmaceuticals

- Cognitive Decline Market

Cognitive Decline Market Size, Share, and Growth Forecast 2026 - 2033

Cognitive Decline Market by Treatment (Drug therapy, Non-pharmacological therapy, Combination therapy), by Disease Type (Alzheimer's disease, Mild cognitive impairment (MCI), Vascular dementia, Parkinson's disease dementia, Lewy body dementia, Frontotemporal dementia, Others), by End User (Hospitals, Specialty clinics, Diagnostic centers, Research institutes), by Regional Analysis, 2026-2033

Cognitive Decline Market Size and Trend Analysis

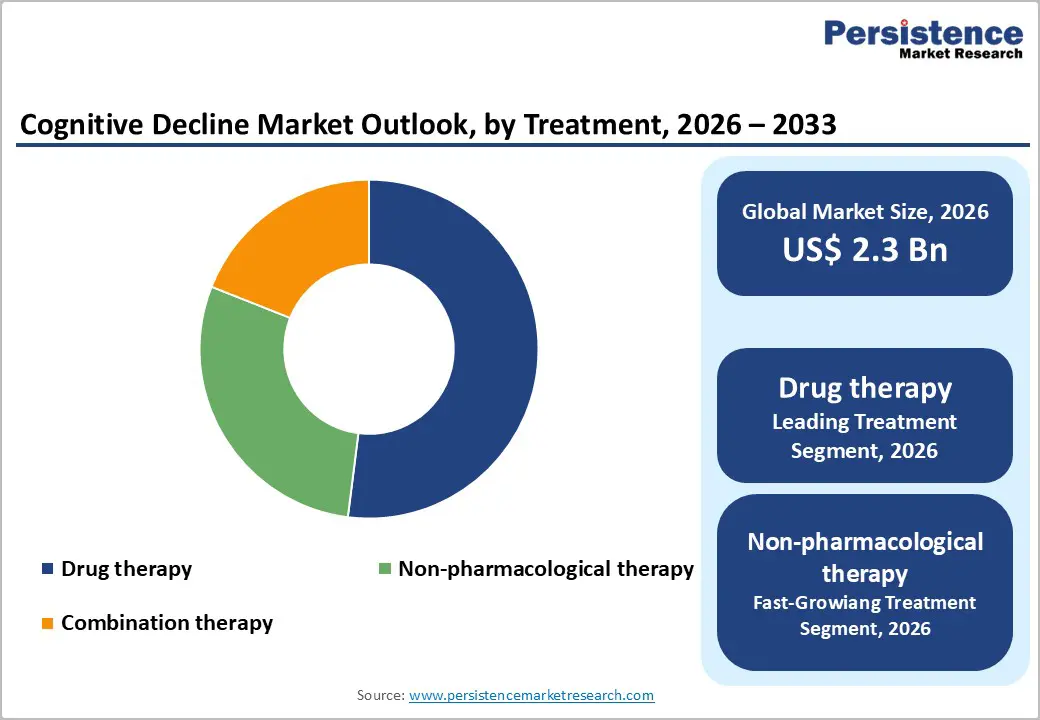

The global cognitive decline market size is expected to be valued at US$ 2.3 billion in 2026 and projected to reach US$ 3.4 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033.

The market expansion is primarily driven by the rapidly aging global population and increasing prevalence of neurodegenerative diseases, particularly Alzheimer's disease and other dementias. According to the World Health Organization (WHO), approximately 57 million people globally were living with dementia in 2021, with this number projected to reach 152.8 million by 2050, representing a staggering 160.84% increase. This demographic shift, coupled with improved diagnostic capabilities and heightened awareness about cognitive disorders, is propelling unprecedented demand for both pharmacological and non-pharmacological therapeutic interventions across developed and emerging healthcare markets worldwide.

Key Market Highlights

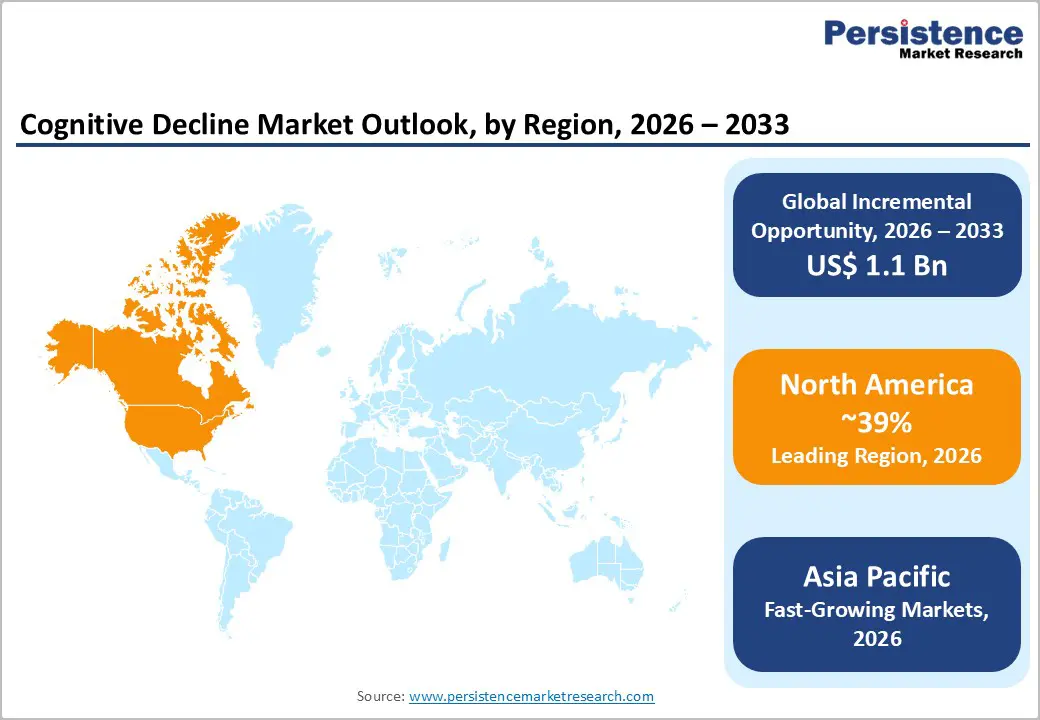

- Leading region: North America dominates the global cognitive decline market with 39% market share in 2025, driven by advanced healthcare infrastructure, substantial R&D investments, pioneering FDA regulatory approvals of disease-modifying therapies, and the presence of leading pharmaceutical companies, including Biogen Inc., Eli Lilly and Company, and Pfizer Inc. operating within a sophisticated innovation ecosystem.

- Fastest Growing Region: Asia Pacific represents the fastest-growing regional market, propelled by dramatic demographic aging with more than 17 million current dementia patients, massive government healthcare investments in China's "Healthy China 2030" plan, Japan's 14 trillion yen dementia care budget projections, and rapidly expanding diagnostic and treatment infrastructure across urban centers.

- Dominant Segment from Treatment Category: Drug therapy commands 52% market share in 2025, anchored by established standard-of-care cholinesterase inhibitors and NMDA receptor antagonists, recently approved disease-modifying anti-amyloid therapies (Leqembi and Kisunla), and 102 disease-targeted therapies (74%) comprising the global clinical trial pipeline with substantial biopharmaceutical R&D investments.

- Key Market Opportunity: The Asia Pacific region's transformation into a global growth engine presents exceptional market opportunities, with Japan's technology-focused dementia strategy, China's public-private partnership expansion enabling foreign investment, India's 18% annual home healthcare growth, and the region's demographic imperative creating sustained double-digit expansion through 2033 for strategic market participants.

| Global Market Attributes | Key Insights |

|---|---|

| Cognitive Decline Market Size (2026E) | US$ 2.3 billion |

| Market Value Forecast (2033F) | US$ 3.4 billion |

| Projected Growth CAGR (2026-2033) | 5.6% |

| Historical Market Growth (2020-2025) | 5.1% |

Market Dynamics

Market Growth Drivers

Accelerating Global Population Aging and Rising Dementia Prevalence

The unprecedented acceleration of global population aging stands as the most significant driver propelling the cognitive decline market forward. According to recent epidemiological studies, the global number of people living with Alzheimer's disease and other dementias has increased from approximately 19.8 million in 1990 to 52.6 million in 2021, representing a dramatic rise of 155.27% over three decades. The National Center for Biotechnology Information (NCBI) reports that mortality from Alzheimer's disease and other dementias nearly tripled during this period, rising from about 650,000 deaths in 1990 to nearly 1.92 million in 2021. China, Japan, and Germany exhibit the highest age-standardized incidence and prevalence rates globally, with Japan's Ministry of Health, Labor, and Welfare estimating that approximately 5.8 million seniors (one in seven Japanese seniors) will have dementia by 2040. This demographic tsunami is creating unprecedented pressures on healthcare systems and driving substantial investments in treatments for cognitive decline, diagnostics, and care management solutions across both developed and emerging markets.

Breakthrough Regulatory Approvals of Disease-Modifying Therapies

The recent wave of regulatory approvals for disease-modifying anti-amyloid therapies represents a paradigm shift in cognitive decline treatment approaches and market dynamics. In January 2023, the U.S. Food and Drug Administration (FDA) approved Leqembi (lecanemab), developed by Eisai Co., Ltd. and Biogen Inc., and in July 2024 approved Kisunla (donanemab) from Eli Lilly and Company for the treatment of early symptomatic Alzheimer's disease. The Clarity AD clinical trial demonstrated that lecanemab reduced clinical decline by 27% at 18 months compared with placebo and showed a 37% improvement in activities of daily living scores. These approvals mark the first disease-modifying treatments that can slow the progression of cognitive decline rather than merely managing symptoms. According to the Alzheimer's Association, there are now more than 180 trials underway testing nearly 140 experimental treatments for Alzheimer's disease across the globe, with over 30 in Phase 3 trials. This robust clinical development pipeline, combined with expanding global regulatory approvals, including markets like China, South Korea, Hong Kong, Israel, UAE, Great Britain, and Mexico, is fundamentally transforming treatment paradigms and driving substantial market growth momentum.

Market Restraints

High Treatment Costs and Limited Healthcare Reimbursement Coverage

The substantial financial burden associated with newly approved disease-modifying therapies presents a significant barrier to market accessibility and adoption. The annual treatment costs for anti-amyloid therapies such as Leqembi and Kisunla can exceed $26,000 per patient, excluding companion diagnostic testing, routine brain imaging for amyloid-related imaging abnormalities (ARIA), and infusion administration costs. Despite receiving positive opinions from the European Medicines Agency's Committee for Medicinal Products for Human Use (CHMP), neither lecanemab nor donanemab is currently offered through the National Health Service (NHS) in the UK, reflecting widespread reimbursement challenges. According to the European Dementia Monitor 2023, only Greece, Ireland, Slovakia, Sweden, and the United Kingdom (England) have established working groups or strategies to prepare for the introduction of these new treatments. This limited reimbursement coverage, particularly in universal healthcare systems and lower-middle-income countries, significantly restricts patient access and market penetration despite clinical efficacy demonstrated in trials.

Market Opportunities

Rapid Expansion of Non-Pharmacological Therapy Adoption

The accelerating adoption of evidence-based non-pharmacological interventions represents a substantial market opportunity, particularly as healthcare systems seek cost-effective alternatives and complementary approaches to expensive drug therapies. Research published in the Journal of Alzheimer's Disease demonstrates that Cognitive Stimulation Therapy (CST) can enhance cognitive function and provide benefits comparable to certain medications. Studies have shown that photobiomodulation (PBM) is most effective for treating cognitive dysfunction, followed by enriched-environment interventions, exercise therapy, and CST. The American Geriatrics Society (AGS) now endorses the delivery of non-pharmacologic interventions as a primary practice to address behavioral and psychological symptoms of dementia (BPSD). Digital therapeutics are gaining particular traction, with the digital therapeutics market valued at US$ 4.68 billion in 2024 and projected to grow at a CAGR of 16.61%, with dementia as a key focus area. Virtual reality therapy, robot-assisted therapy, music therapy, art therapy, and AI-driven cognitive assessment tools are proliferating rapidly across Asia Pacific markets, particularly in Japan, where the government's latest dementia strategy emphasizes technology utilization to alleviate care burden. This paradigm shift toward holistic, integrated care models combining pharmacological and non-pharmacological approaches creates substantial revenue opportunities for market participants developing innovative therapy platforms.

Category-Wise Insights

Treatment Analysis

Drug therapy dominates the cognitive decline treatment landscape with an estimated 52% market share in 2025, driven by the clinical necessity of pharmacological interventions for managing progressive cognitive decline and behavioral symptoms associated with neurodegenerative dementias. The segment's prominence stems from established standard-of-care protocols utilizing cholinesterase inhibitors (donepezil, rivastigmine, galantamine) and NMDA receptor antagonists (memantine) for Alzheimer's care pathways, which have demonstrated efficacy in slowing symptom progression. According to recent analyses of the pharmaceutical pipeline, there are 102 disease-targeted therapies (DTTs) representing 74% of drugs in clinical trials globally, with 60.20% of the dementia management market focused on drug therapy. The recent FDA approvals of Leqembi (lecanemab) and Kisunla (donanemab) as first-in-class disease-modifying anti-amyloid therapies have significantly strengthened this segment's market position, with both drugs demonstrating significant reductions in clinical decline in pivotal Phase 3 trials. Increased investments by biopharmaceutical companies, including Biogen Inc., Eisai Co., Ltd., Eli Lilly and Company, F. Hoffmann-La Roche Ltd., Novartis AG, and Pfizer Inc. in pipeline drugs targeting disease mechanisms beyond amyloid plaques, alongside continuous government-supported access programs and established regulatory approval pathways, have solidified drug therapy as the indispensable foundation of cognitive decline treatment regimens worldwide.

End User Analysis

Hospitals represent the leading end-user segment with an estimated 45% market share in 2025, driven by their comprehensive infrastructure for complex diagnostic procedures, specialized neurological care, and administration of advanced therapeutic interventions. Hospitals serve as primary hubs for cognitive decline management due to their capability to perform sophisticated diagnostic assessments, including amyloid positron emission tomography (PET) scans, cerebrospinal fluid (CSF) biomarker testing, advanced neuroimaging protocols (MRI, CT), and comprehensive neuropsychological evaluations required for accurate dementia subtype classification. The segment's dominance is reinforced by hospitals' capacity to administer newly approved intravenous anti-amyloid therapies, such as Leqembi and Kisunla, which require regular infusion procedures, continuous monitoring for amyloid-related imaging abnormalities (ARIA), and immediate access to emergency medical interventions in the event of adverse events. According to healthcare utilization studies, hospitals also serve as critical access points for managing behavioral and psychological symptoms of dementia (BPSD), acute medical complications, and coordinating multidisciplinary care teams involving neurologists, geriatricians, psychiatrists, nurses, and social workers. The establishment of specialized memory clinics and cognitive neurology departments within major hospital systems, particularly in developed markets across North America and Europe, alongside growing investments in neurology infrastructure in emerging Asia Pacific markets, including China, Japan, and India, ensures hospitals maintain their pivotal role as the primary destination for comprehensive cognitive decline assessment, treatment initiation, and ongoing disease management.

Regional Insights

North America Cognitive Decline Market Trends and Insights

North America holds the largest regional market share, at 39% in 2025, driven by the United States' advanced healthcare infrastructure, substantial research and development investments, and early adoption of innovative therapeutic interventions. The region's leadership is exemplified by the FDA's pioneering regulatory approvals of disease-modifying therapies, including Leqembi (lecanemab) in January 2023 and Kisunla (donanemab) in July 2024, establishing the U.S. as the global epicenter for cutting-edge Alzheimer's treatment access. The Alzheimer's Association reports that approximately 6.9 million Americans aged 65 and older are living with Alzheimer's disease in 2024, with projections indicating this figure could double by 2060 as the population ages, creating massive healthcare system pressures and economic burden.

The region benefits from a sophisticated innovation ecosystem encompassing world-leading pharmaceutical companies, including Biogen Inc., Eli Lilly and Company, Johnson & Johnson, Pfizer Inc., Merck & Co., Inc., and AbbVie Inc., alongside premier research institutions and clinical trial networks. The National Institutes of Health (NIH) provides substantial federal funding for dementia research, with the National Institute on Aging (NIA) leading major longitudinal studies and clinical trials. The Federal Trade Commission (FTC) reported that fraud targeting older Americans has surged, with the number losing over $100,000 to fraud increasing more than fivefold from 2020 to 2024, highlighting the vulnerability of the cognitively impaired population and driving demand for comprehensive care solutions. Robust Medicare and Medicaid coverage frameworks, albeit with ongoing reimbursement challenges for newer therapies, alongside widespread adoption of private insurance and well-established specialty memory clinics and diagnostic centers, position North America to maintain regional market leadership throughout the forecast period despite emerging competition from rapidly growing Asia-Pacific markets.

Asia Pacific Cognitive Decline Market Trends and Insights

Asia-Pacific emerges as the fastest-growing regional market, driven by dramatic demographic shifts, substantial government healthcare investments, and rapidly expanding diagnostic and treatment infrastructure in the region's most populous nations. The region currently houses more than 17 million persons with dementia according to Alzheimer's Disease International, with projections indicating that more than half of global dementia patients will reside in the region by mid-century, creating unprecedented market expansion opportunities. Japan, with the world's oldest demographic profile where nearly 30% of the population is aged 65 or older, leads regional market sophistication with the Ministry of Health, Labor, and Welfare predicting dementia-related health and social care costs will soar to 14 trillion yen (approximately $90 billion) by 2030 from 9 trillion yen in 2025.

Competitive Landscape

The cognitive decline market is highly competitive, driven by continuous innovation in therapeutics, diagnostics, and digital solutions. Key players focus on developing disease-modifying drugs, improving symptomatic treatments, and expanding non-pharmacological interventions such as cognitive training and lifestyle programs. Strategic initiatives include mergers, acquisitions, partnerships, and collaborations to strengthen research pipelines and market presence. Companies are also investing in advanced diagnostic tools and biomarker-based technologies for early detection and personalized treatment.

Key Market Developments

- In July 2025, i-Function®, a company focused on cognitive health and independent living, partnered with Lunavi, a leading digital solutions provider, to bring the LASSI-D™ (Loewenstein-Acevedo Scales of Semantic Interference and Learning – Digital) to market. This innovative digital tool enabled earlier and more accessible detection of Mild Cognitive Impairment (MCI), a precursor to Alzheimer's disease.

Companies Covered in Cognitive Decline Market

Biogen Inc., Eisai Co., Ltd., Eli Lilly and Company, F. Hoffmann-La Roche Ltd., Novartis AG, Johnson & Johnson, Pfizer Inc., Merck & Co., Inc., AbbVie Inc., H. Lundbeck A/S, Takeda Pharmaceutical Company, AstraZeneca plc, Cognition Therapeutics Inc., AC Immune SA, Axsome Therapeutics, Anavex Life Sciences Corp., Alector Inc., Probiodrug AG, Cortexyme Inc.

Frequently Asked Questions

The global cognitive decline market is expected to be valued at US$ 2.3 billion in 2026.

The primary demand drivers include the unprecedented global population aging with dementia cases projected to reach 152.8 million by 2050 (a 160.84% increase), breakthrough FDA approvals of disease-modifying anti-amyloid therapies demonstrating 27-37% clinical decline reduction, over 180 trials testing 140 experimental treatments globally, and expanding non-pharmacological therapy adoption including digital therapeutics growing at 16.61% CAGR as healthcare systems seek evidence-based, cost-effective complementary interventions addressing comprehensive patient care needs.

North America leads the cognitive decline market with 39% market share in 2025, driven by the United States' advanced healthcare infrastructure, substantial National Institutes of Health (NIH) research funding, pioneering FDA regulatory approvals establishing first-in-class disease-modifying therapy access, presence of leading pharmaceutical companies including Biogen Inc., Eli Lilly and Company, and Pfizer Inc., sophisticated innovation ecosystems, comprehensive diagnostic capabilities, and established specialty memory clinics and treatment centers nationwide.

The Asia Pacific region's emergence as the fastest-growing market represents the most significant opportunity, with more than 17 million current dementia patients projected to exceed half of global cases by mid-century, Japan's government allocating 14 trillion yen ($90 billion) for dementia care by 2030, China's "Healthy China 2030" plan promoting public-private partnerships, India's home healthcare growing at 18% annually, and regional demographic imperatives creating sustained double-digit expansion opportunities for strategic market participants.

Key market players include Biogen Inc., Eisai Co., Ltd., and Eli Lilly and Company leading disease-modifying therapy commercialization following FDA approvals of Leqembi and Kisunla, alongside major pharmaceutical corporations F. Hoffmann-La Roche Ltd., Novartis AG, Johnson & Johnson, Pfizer Inc., Merck & Co., Inc., AbbVie Inc., H. Lundbeck A/S, Takeda Pharmaceutical Company, and AstraZeneca plc pursuing robust clinical development pipelines, with emerging innovators Cognition Therapeutics Inc., AC Immune SA, and Alector Inc. developing next-generation therapies.