- Hardware & Software IT Services

- Cognitive Computing Market

Cognitive Computing Market Size, Share, and Growth Forecast, 2026 - 2033

Cognitive Computing Market By Solution (Cognitive Computing Platforms, Cognitive Computing APIs, AI & Cognitive Services, Professional Services), Application (Speech Recognition, Computer Vision, Text Analytics, Automated Pattern Discovery, BI Narratives & Visualizations, Others), Industry (BFSI, Retail & eCommerce, Manufacturing, Healthcare & Life Sciences, Government, IT & Telecom, Travel & Hospitality, Media & Entertainment, Others), and Region Analysis 2026 to 2033

Market Overview

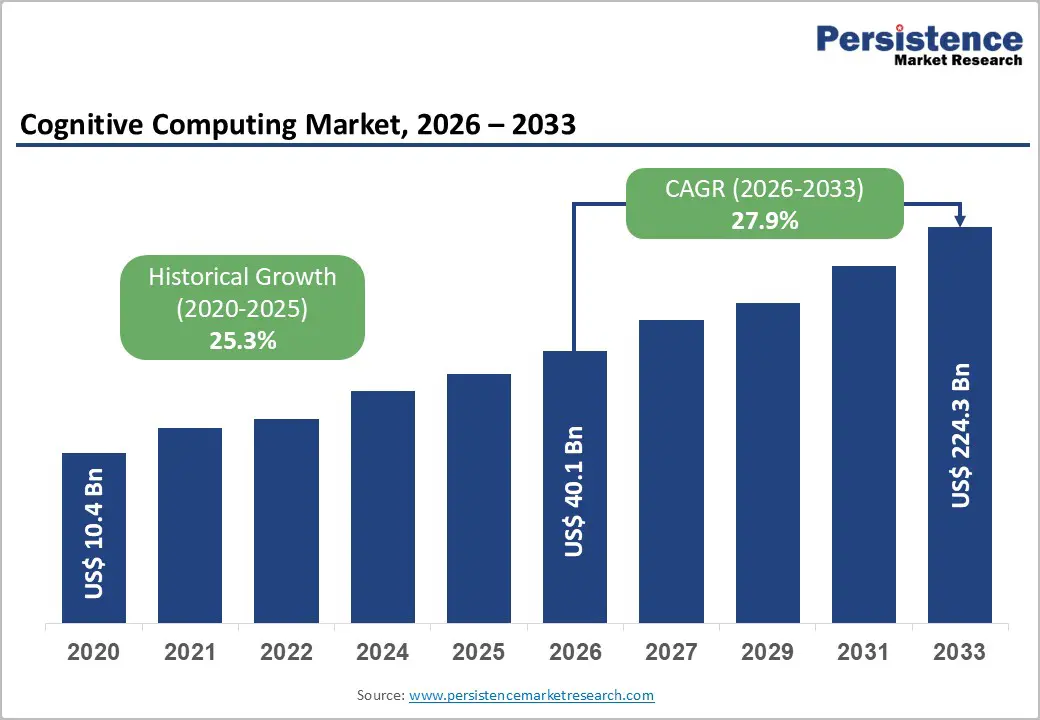

The global Cognitive Computing Market size is projected to be valued at US$40.1 Billion in 2026 and is anticipated to reach US$224.3 Billion by 2033, growing at a CAGR of 27.9% between 2026 and 2033. This remarkable expansion is driven by exponential growth in enterprise data generation exceeding 2.5 quintillion bytes daily, artificial intelligence investments surpassing US$154 billion globally, and digital transformation initiatives across 89% of enterprises worldwide. Advanced natural language processing capabilities achieving around 96% accuracy, cloud computing adoption reaching approximate 94% among Fortune 500 companies, and automation requirements reducing operational costs by 40% further accelerate market penetration.

Key Market Highlights

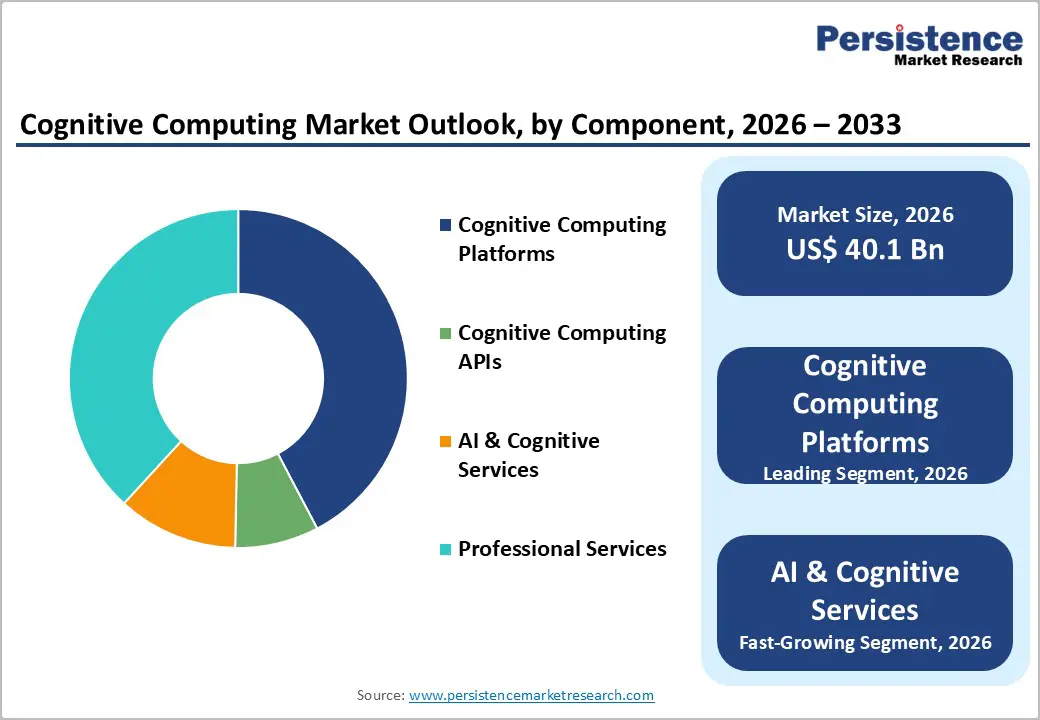

- Cognitive Computing Platforms dominate solutions with a 42% share (US$16.86 billion), while AI & Cognitive Services grow fastest at a 31.2% CAGR through API-led adoption.

- Text Analytics leads applications with a 22% share (US$8.83 billion), while Speech Recognition expands rapidly at a 29.0% CAGR driven by 8.4 billion virtual assistant users and 96% accuracy.

- BFSI holds industry leadership with a 23% share (US$9.23 billion), while Healthcare & Life Sciences grows fastest at a 30.4% CAGR due to advanced diagnostics and faster drug discovery.

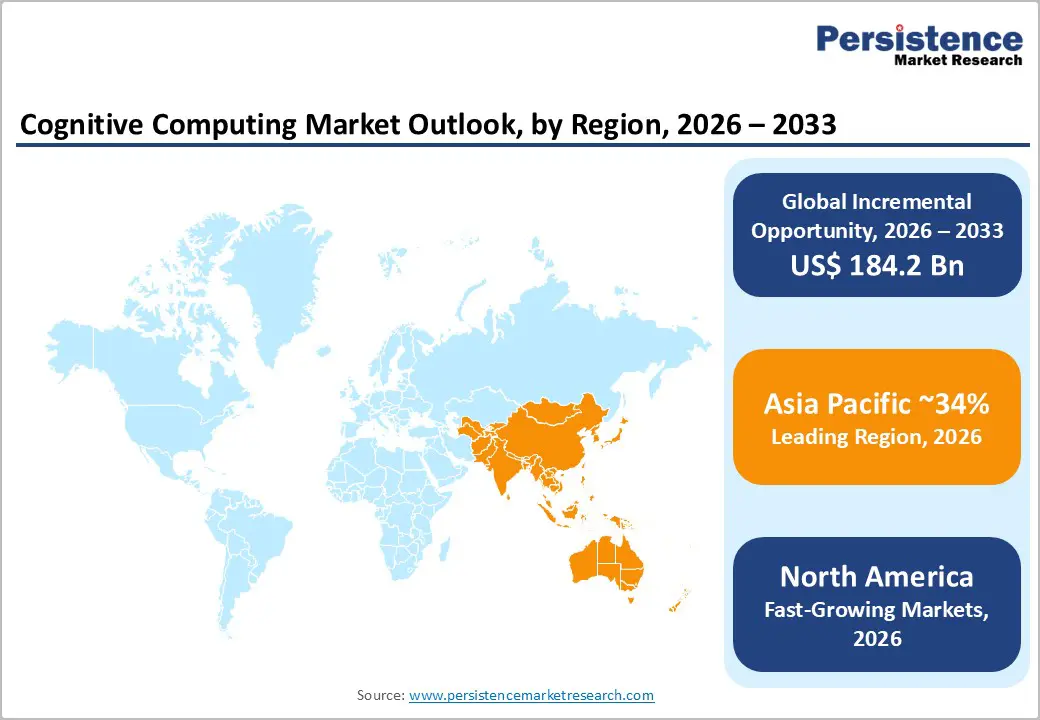

- Asia Pacific accounts for 34% market share, supported by China’s US$150 billion AI target and US$38 billion annual cognitive investments.

- North America records strong growth at a 27.9% CAGR, underpinned by US$89 billion in annual R&D spending.

- Europe grows steadily at a 26.7% CAGR, driven by €95 billion Horizon Europe funding and the AI Act’s ethical framework.

- Strategic initiatives focus on platform integration, healthcare expansion, and vertical solutions to accelerate revenue growth.

| Key Insights | Details |

|---|---|

| Cognitive Computing Market Size (2026E) | US$ 40.1 billion |

| Market Value Forecast (2033F) | US$ 224.3 billion |

| Projected Growth CAGR (2026-2033) | 27.9% |

| Historical Market Growth (2020-2025) | 25.3% |

Market Dynamics Analysis

Market Drivers

Exponential Growth in Enterprise Data and Analytics Requirements

Global data creation has reached unprecedented scale, with the International Data Corporation estimating 120 zettabytes generated in 2023 and projecting volumes to reach 181 zettabytes by 2025, reflecting rapid annual growth. Meanwhile, the U.S. Census Bureau notes that nearly 90% of enterprise data remains unstructured, limiting the effectiveness of conventional analytics tools. Cognitive computing platforms address this challenge by simultaneously processing natural language, images, audio, and structured datasets to extract unified, contextual insights. According to the World Economic Forum, organizations adopting cognitive analytics report faster decision making and improved operational efficiency. Enterprise analytics spending surpassed US$274 billion in 2023, with cognitive computing accounting for a meaningful share of advanced analytics investments. In sectors such as financial services and healthcare, cognitive systems enable real time fraud detection and improved diagnostic accuracy.

Artificial Intelligence and Machine Learning Technology Advancement

Corporate digital transformation programs are accelerating cognitive computing adoption, with Accenture indicating that 89% of enterprises pursuing comprehensive digitalization will invest nearly US$2.3 trillion through 2025. Customer experience optimization drives conversational AI adoption, as chatbots and virtual assistants manage up to 85% of customer service interactions in leading organizations, cutting response times by 73%. Public-sector momentum remains strong, with the European Commission’s Digital Europe Programme allocating €7.5 billion to advance AI and data capabilities across industries. Workforce augmentation use cases empower employees with real-time insights, automate routine processes, and shift focus toward high-value work, delivering productivity gains averaging 37%. In retail, cognitive personalization engines analyze browsing behavior, purchase histories, and preferences to lift conversion rates by 28% and customer lifetime value by 42%. Governments deploying cognitive platforms deliver efficiency gains.

Market Restraints

Data Privacy Concerns and Regulatory Compliance Complexity

Cognitive computing systems face significant challenges regarding data privacy, algorithmic bias, and regulatory compliance across jurisdictions. The General Data Protection Regulation imposes strict requirements on automated decision-making and data processing, with non-compliance penalties reaching 4% of global annual revenue or €20 million. Organizations implementing cognitive systems report average compliance costs of US$5.8 million annually for data governance, audit trails, and transparency mechanisms. Algorithmic bias concerns documented in 47% of AI deployments create legal liability risks and reputational damage, particularly in hiring, lending, and law enforcement applications. The California Consumer Privacy Act, Brazil's LGPD, and China's Personal Information Protection Law create fragmented compliance landscapes increasing implementation complexity by 68%. Consumer trust deficits regarding AI decision-making limit adoption in sensitive domains.

High Implementation Costs and Technical Complexity Barriers

Enterprise cognitive computing deployments require substantial investments averaging US$8.4 million to US$24.6 million for comprehensive implementations including infrastructure, software licensing, integration, and change management. Organizations report 58% of cognitive projects experience budget overruns averaging 47% due to underestimated complexity and extended timelines. Technical expertise shortages create implementation bottlenecks, with the World Economic Forum documenting 67% deficit in AI and data science specialists globally. Legacy system integration challenges increase deployment costs by 55-75%, while data quality issues requiring cleansing and standardization delay implementations by 6-12 months. Small and medium enterprises face particular barriers, with 72% citing upfront costs as primary adoption obstacle despite long-term value propositions.

Market Opportunities

Edge Computing Integration and IoT Data Processing

The convergence of cognitive computing with edge computing and Internet of Things represents a US$94.6 billion opportunity by 2032, enabling real-time decision-making in manufacturing, autonomous vehicles, and smart cities. IoT device deployments reached 16.7 billion connections in 2023, projected to exceed 29 billion by 2030, generating data volumes requiring localized cognitive processing. Edge computing enables cognitive analytics at data source reducing latency by 78% and bandwidth requirements by 65% compared to centralized cloud processing. Manufacturing applications utilize cognitive edge systems for predictive maintenance, quality control, and production optimization achieving 42% reduction in unplanned downtime. Autonomous vehicle systems process sensor data from cameras, lidar, and radar requiring cognitive capabilities making decisions within milliseconds ensuring safety and navigation accuracy.

Emerging Markets and Digital Leapfrogging Opportunities

Emerging economies present substantial growth potential as digital infrastructure improves and organizations adopt cloud-based cognitive services bypassing legacy technology investments. The Asian Development Bank projects digital economy growth in developing Asia reaching US$5.8 trillion by 2030, with cognitive computing representing 14% of enterprise technology spending. India's Digital India initiative allocates US$18.4 billion toward AI and analytics capabilities, while China's New Generation AI Development Plan targets US$150 billion domestic AI industry by 2030. Southeast Asian nations implement smart city programs across 450 cities requiring cognitive computing for traffic management, public safety, and municipal services. Mobile-first markets leverage cognitive capabilities in banking, agriculture, and healthcare addressing infrastructure limitations through accessible cloud services. Cost-competitive implementation models and government support programs create favorable conditions for rapid adoption.

Segmentation Analysis

Solution Analysis

Cognitive Computing Platforms, including cloud-based and on-premises solutions, hold a leading 42% market share, valued at approximately US$16.86 billion in 2026, acting as foundational infrastructure for natural language processing, machine learning, computer vision, and predictive analytics. These platforms deliver integrated development environments, pre-trained models, data orchestration tools, and deployment frameworks supporting diverse cognitive use cases. Cloud-based platforms dominate growth through scalability, lower infrastructure costs, and faster deployment cycles averaging six to eight weeks versus four to six months on-premises deployments.

AI and Cognitive Services represent the fastest-growing solution segment, expanding at a 31.2% CAGR through 2033, driven by API-based consumption models and pre-built capabilities. Services such as speech recognition, translation, sentiment analysis, and image recognition enable rapid integration, consumption-based pricing, and accelerated enterprise adoption without upfront infrastructure investments globally today.

Application Analysis

Text Analytics maintains application segment leadership with 22% market share, valued at approximately US$8.83 billion in 2026, supporting customer feedback analysis, document processing, social media monitoring, and compliance use cases. It processes unstructured text from emails, documents, reviews, and social platforms, extracting sentiment, topics, entities, and relationships to deliver actionable insights. Financial institutions analyze regulatory filings and market commentary for risk assessment, while customer service teams process tickets to achieve faster issue resolution and higher satisfaction.

Speech Recognition is the fastest-growing application at 29.0% CAGR, driven by virtual assistants, customer service automation, and accessibility mandates. Accuracy rates reaching 96% enable reliable use across call centers, healthcare documentation, and smart homes. Global virtual assistant users surpassed 8.4 billion in 2024, with enterprise deployments managing 85% of routine inquiries globally.

Industry Analysis

BFSI maintains industry leadership with 23% market share, valued at about US$9.23 billion in 2026, covering fraud detection, credit risk assessment, algorithmic trading, customer service automation, and regulatory compliance. Financial institutions process billions of daily transactions, requiring real-time cognitive analysis that detects fraud with 97% accuracy while cutting false positives by 68%. Credit decision systems analyze traditional and alternative data, including transaction patterns and behavioral indicators, improving approval rates by 34% while preserving risk controls. Banking chatbots manage 78% of routine inquiries across digital channels, lowering operating costs by US$7.3 billion annually for major banks.

Healthcare and Life Sciences is the fastest-growing segment at 30.4% CAGR, driven by imaging analysis, drug discovery, and clinical decision support. Cognitive systems achieve 94% diagnostic accuracy and cut drug development timelines by 60% globally.

Regional Market Insights

North America

North America demonstrates strong growth at a 27.9% CAGR, driven by a dense concentration of technology leaders, sustained R&D investments exceeding US$89 billion annually, and early enterprise adoption across multiple industries. The United States leads global cognitive computing deployment, with nearly 67% of Fortune 500 companies implementing AI-powered cognitive systems for customer service, operational optimization, and decision support. Silicon Valley’s innovation ecosystem, combined with mature digital infrastructure and sophisticated customer expectations, reinforces the region’s market leadership. Federal AI initiatives, including the National AI Research Resource, allocate approximately US$2.4 billion to advance cognitive computing capabilities. Healthcare providers deploy cognitive diagnostics and clinical decision tools, while financial institutions leverage fraud detection and algorithmic trading systems processing millions of transactions daily. Competitive dynamics remain intense, as hyperscale cloud providers and cognitive platforms.

Europe

Europe demonstrates steady growth at a 26.7% CAGR, influenced by stringent AI ethics regulations, sustained public-sector investments, and rising industrial automation requirements. Germany leads regional adoption through manufacturing-focused cognitive applications, including predictive maintenance, quality inspection, and supply chain optimization across automotive and industrial equipment sectors. The United Kingdom maintains a strong presence in financial services cognitive computing, while France advances healthcare and public-sector deployments. The European Commission’s AI Act establishes a comprehensive regulatory framework governing cognitive system development and deployment, mandating transparency, accountability, and human oversight. Complementing regulation, the Horizon Europe program allocates nearly €95 billion through 2027 to support AI and digital technology innovation. Europe’s emphasis on trustworthy, explainable AI shapes cognitive implementations prioritizing governance, risk management, and compliance. Additionally, GDPR requirements significantly influence data architectures and algorithm design.

Asia Pacific

Asia Pacific commands a significant 34% market share, driven by large-scale digital transformation initiatives, manufacturing automation, and proactive government AI development programs. China leads regional expansion through a comprehensive national AI strategy targeting a US$150 billion domestic industry by 2030, with cognitive deployments across smart cities, manufacturing, and financial services. Regional technology leaders invest nearly US$38 billion annually in cognitive capabilities, including natural language processing tailored for Mandarin and other local languages. Japan strengthens adoption through robotics integration and healthcare-focused cognitive applications, while India emerges as the fastest-growing market supported by IT services adoption and Digital India initiatives. ASEAN countries increasingly deploy cognitive systems for e-government, smart transportation, and customer engagement platforms. Manufacturing dominance accelerates use cases in quality control, predictive maintenance, and supply chain optimization. Supporting widespread regional adoption.

Competitive Landscape

Strategic Developments

- In May 2024, IBM Corporation and SAP expanded their collaboration to advance generative AI and industry-specific cloud solutions, integrating AI into SAP business processes while leveraging IBM’s hybrid cloud and AI expertise to accelerate enterprise digital transformation.

Business Strategies

Market leaders pursue platform ecosystem strategies integrating cognitive capabilities across cloud infrastructure, development tools, and industry solutions creating comprehensive AI environments. Innovation focus emphasizes large language models, multimodal processing, and edge deployment capabilities. Strategic partnerships with system integrators, independent software vendors, and industry specialists expand market reach and vertical expertise. Vertical market specialization addresses industry-specific requirements in healthcare, financial services, and manufacturing with pre-built models and compliance frameworks. Consumption-based pricing models lower adoption barriers while generating predictable recurring revenue streams.

Companies Covered in Cognitive Computing Market

- Microsoft Corporation

- Google LLC (Alphabet Inc.)

- IBM Corporation

- Amazon Web Services, Inc.

- Oracle Corporation

- Salesforce, Inc.

- SAP SE

- Baidu, Inc.

- Alibaba Cloud (Alibaba Group)

- Tencent Holdings Limited

- Intel Corporation

- NVIDIA Corporation

- SAS Institute Inc.

- Palantir Technologies Inc.

- Hewlett Packard Enterprise

Frequently Asked Questions

The Cognitive Computing Market is projected at US$40.14 Billion in 2026, expanding to US$224.32 Billion by 2033.

Key drivers include surging unstructured data volumes, rising AI investments improving language intelligence, widespread enterprise digital transformation, and faster, more accurate decision-making enabled by cognitive analytics.

The market is projected to grow at a CAGR of 27.9% between 2026 and 2033.

Major opportunities include expanding healthcare adoption of cognitive technologies, growing edge computing integration for real-time intelligence, and rapid digital economy growth in emerging markets enabled by cloud-based cognitive services.

Leading players include Microsoft Corporation, Google LLC, IBM Corporation, Amazon Web Services, Oracle Corporation, Salesforce Inc., SAP SE, Baidu Inc., Alibaba Cloud, Tencent Holdings, Intel Corporation, NVIDIA Corporation, SAS Institute, Palantir Technologies, and Hewlett Packard Enterprise.