- Pharmaceuticals

- CGRP Inhibitors Market

CGRP Inhibitors Market Size, Share, and Growth Forecast 2026 - 2033

CGRP Inhibitors Market by Drug Type (Monoclonal Antibodies, CGRP Antagonists), by Treatment Type (Acute (Abortive), Preventative), by Route of Administration (Oral, Injectable, Nasal), by Distribution Channel, by Patient Demographics, Regional Analysis, 2026-2033

CGRP Inhibitors Market Share and Trends Analysis

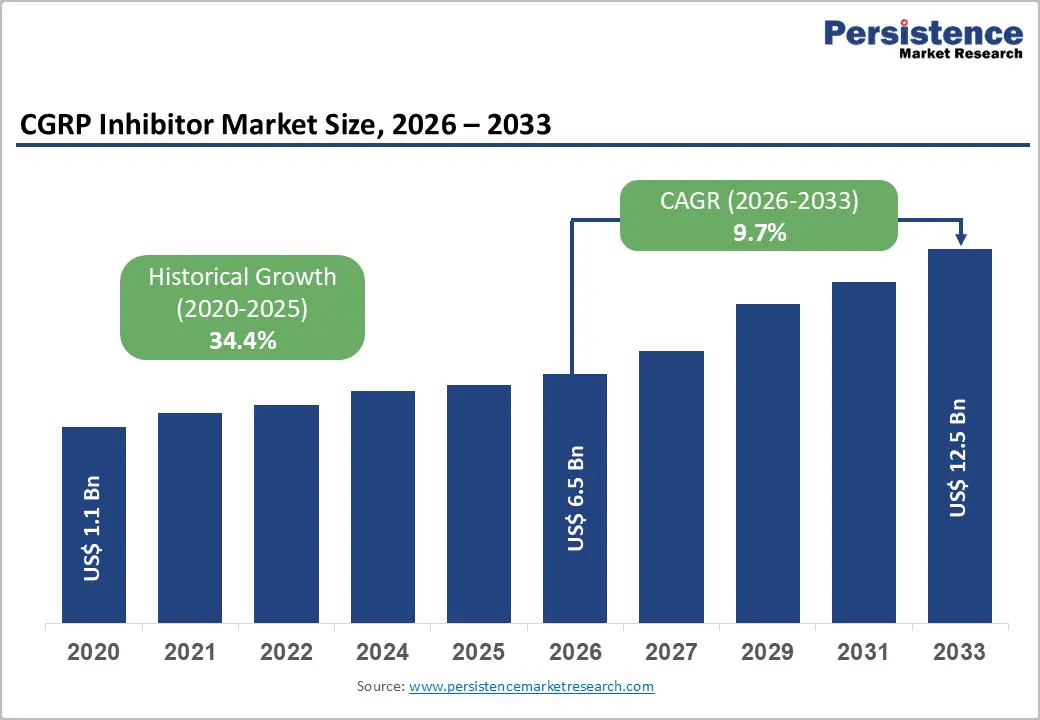

The global CGRP inhibitors market size is expected to be valued at US$ 6.5 billion in 2026 and projected to reach US$ 12.5 billion by 2033, growing at a CAGR of 9.7% between 2026 and 2033.

The CGRP inhibitors market has rapidly expanded following the introduction of monoclonal antibody therapies designed to prevent migraines by targeting calcitonin gene–related peptide pathways. These treatments have reshaped migraine management by providing more precise mechanisms of action and improved tolerability compared with older options such as triptans or antiepileptic drugs. Initially approved for adults with episodic and chronic migraine, leading products including erenumab, fremanezumab, and galcanezumab have shown strong clinical outcomes, reduced attack frequency and enhancing patient quality of life.

Key trends influencing the market include rising migraine prevalence, growing neurologist adoption of targeted biologics, and expanding clinical research into broader patient populations and combination therapies. Manufacturers are also exploring new delivery formats and next-generation CGRP agents. However, high therapy costs and reimbursement restrictions remain major challenges, prompting efforts toward pricing strategies, biosimilar development, and wider insurance coverage to improve long-term accessibility.

Key Industry Highlights

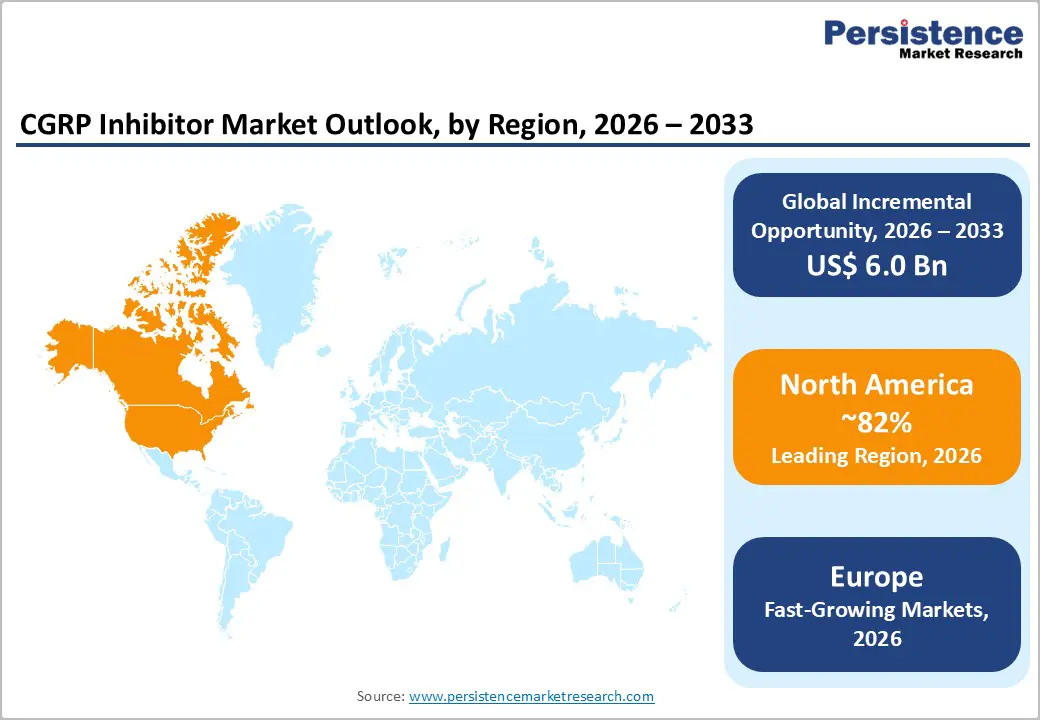

- Leading Region: North America leads the CGRP Inhibitors Market, supported by high migraine diagnosis rates, strong specialist access, rapid uptake of biologic therapies, favorable reimbursement in select populations, and active clinical research ecosystems.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by improving healthcare infrastructure, rising awareness of migraine as a neurological disorder, expanding neurology services, increasing disposable incomes, and broader availability of advanced preventive therapies.

- Dominant Segment: CGRP antagonists dominate the market due to their strong clinical efficacy in reducing migraine frequency, favorable safety profiles compared with older preventive therapies, convenient dosing options, and growing physician and patient preference for targeted migraine treatments.

- Fastest Growing Segment: Acute (abortive) treatments represent the fastest-growing segment, fueled by rising demand for rapid migraine relief, increasing diagnosis rates, expanding availability of oral CGRP therapies, patient preference for non-injectable options, and broader insurance coverage in key markets.

| Report Attribute | Details |

|---|---|

|

CGRP Inhibitors Market Size (2026E) |

US$ 6.5 billion |

|

Market Value Forecast (2033F) |

US$ 12.5 billion |

|

Projected Growth CAGR (2026-2033) |

9.7% |

|

Historical Market Growth (2020-2025) |

34.4% |

Market Dynamics

Driver – Innovative drug delivery technologies to play a crucial role

Innovative drug delivery technologies have improved patient adherence, convenience, and treatment outcomes. Traditional migraine treatments often required injections or multiple daily doses, which posed barriers for many patients. However, newer CGRP receptor antagonists, such as rimegepant and ubrogepant, have been formulated as orally disintegrating tablets (ODTs), allowing for easier administration without water.

This is particularly beneficial for migraine sufferers, who often experience nausea and vomiting during attacks, symptoms that can make swallowing pills difficult. The effectiveness and convenience of these ODT formulations are evident in their growing adoption.

For example, rimegepant, marketed as Nurtec® ODT, generated over US$435 million in U.S. sales, reflecting strong market acceptance. Additionally, Biohaven reported that more than one million prescriptions of Nurtec® ODT were filled within the first 18 months of launch, indicating high demand driven by its fast onset and ease of use. These technologies widely enhance patient experience and also expand access to treatment for those hesitant to use injectables, thus fueling the overall CGRP inhibitor market growth.

Restraints – Cost and accessibility-related constraints

Cost and accessibility remain major restraints in the CGRP inhibitor market, limiting widespread adoption despite clinical effectiveness. Injectable monoclonal antibodies such as erenumab and fremanezumab often cost over US$500–US$600 monthly without insurance, making them unaffordable for many especially in low- and middle-income countries. Even in developed nations, insurance gaps, high co-pays, and prior authorization requirements create access barriers. A 2022 Migraine.com article highlighted patient struggles with insurance denials and affordability. In emerging markets, CGRP inhibitors are often excluded from public health formularies, forcing reliance on out-of-pocket spending or less effective alternatives. The absence of biosimilars worsens the issue. Until affordable options or broader coverage emerges, these challenges will hinder market growth and equity.

Opportunity – Increasing inclination towards exploration of combination therapies

The CGRP inhibitor market is seeing rising interest in combination therapies to enhance efficacy, especially in patients with partial or no response to monotherapy. Chronic migraine sufferers often need multi-modal approaches, leading to combinations of CGRP inhibitors with botulinum toxin (Botox), anti-epileptics, triptans, or behavioral therapies.

A 2022 Cephalalgia study found that adding onabotulinumtoxinA to a CGRP monoclonal antibody reduced migraine days by 2–3 more per month than CGRP monotherapy alone. These additive effects open opportunities for more personalized treatments targeting multiple migraine pathways. Combination approaches also support expanded labeling and lifecycle strategies, encouraging clinical trials and increasing the addressable market. As focus shifts toward real-world effectiveness and patient-centered outcomes, combination therapies represent a key next step in unlocking the full clinical potential of CGRP inhibitors.

Category-wise Analysis

By Drug Type Analysis

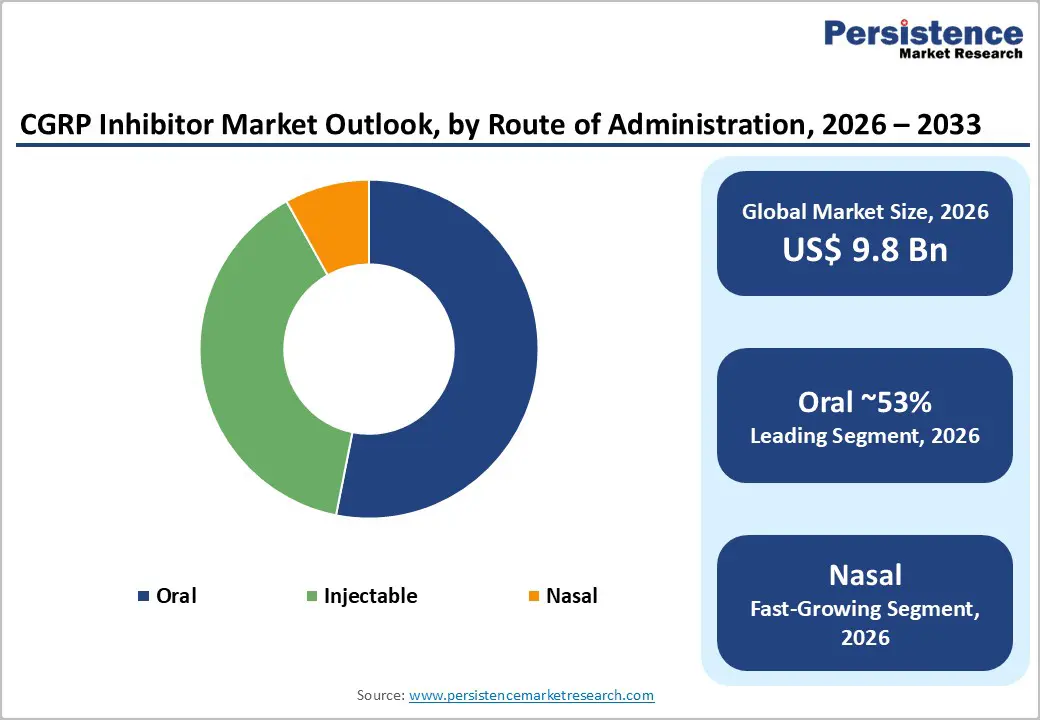

The CGRP inhibitor market is largely propelled by the growing demand for CGRP antagonists, particularly oral options like rimegepant and ubrogepant. These medications are favored for their ease of use and rapid pain relief, making them a preferred choice over traditional treatments that often come with more side effects. This increasing patient preference has allowed oral CGRP inhibitors to capture a significant portion of the market.

At the same time, monoclonal antibodies such as erenumab, fremanezumab, and galcanezumab contribute significantly to the landscape, primarily used for migraine prevention. Administered via injection, they effectively reduce monthly migraine days and are generally well-tolerated. While they may be costlier and less convenient than oral drugs, they offer a strong preventive solution for those with frequent or severe migraines. Together, oral antagonists and injectable monoclonal antibodies are redefining the future of migraine care.

By Treatment Type Analysis

The preventive treatment segment leads the CGRP inhibitor market due to strong clinical outcomes and patient adherence. Monoclonal antibodies such as erenumab and fremanezumab have shown significant reductions in monthly migraine days. A meta-analysis of 11 trials (4,402 patients) found a mean reduction of 1.44 days and a 50% responder rate higher than placebo (RR 1.51). Real-world studies also confirm long-term effectiveness. The American Headache Society recommends CGRP inhibitors as first-line preventive therapies. Moreover, data show reduced use of traditional preventives like topiramate since CGRP mAbs became available. These factors make preventive CGRP therapies the preferred choice in migraine management.

Region-wise Insights

North America CGRP Inhibitors Market Trends

North America accounts for the largest share of the CGRP inhibitor market, driven by a high prevalence of migraine diagnoses, heightened awareness of advanced treatment options, and a robust healthcare system. In the U.S., access to specialists and innovative therapies has supported widespread use of CGRP inhibitors such as erenumab, fremanezumab, and rimegepant. While insurance hurdles exist, coverage is generally more comprehensive than in other regions, enhancing treatment accessibility.

Additionally, pharmaceutical companies prefer North America for clinical trials and product launches, in the pursuit of fast regulatory approvals. Ongoing efforts to expand insurance access and include younger patient groups, such as adolescents, are likely to drive demand. With a strong presence of major industry players and supportive infrastructure, North America is positioned to maintain its lead in the CGRP inhibitor market for the foreseeable future.

Europe CGRP Inhibitors Market Trends

Europe is among the fastest-growing regions in the CGRP inhibitor market, primarily due to a high prevalence of migraines and the significant economic burden they impose. Approximately 41 million adults in Europe suffer from migraines, with 30.5 million having physician-diagnosed migraines in major countries such as Germany, France, the UK, Italy, and Spain, reflecting a prevalence of about 11.5%. Migraines cost Europe over €50 billion annually through healthcare expenses and lost productivity.

The European Medicines Agency (EMA) has approved several CGRP inhibitors, improving patient access to advanced therapies. Enhanced healthcare infrastructure, better insurance coverage, and growing awareness of innovative treatments contribute to increasing adoption. These factors collectively fuel rapid growth in the CGRP inhibitor market across Europe, with ongoing clinical developments and regulatory support expected to sustain momentum in the coming years.

Asia Pacific CGRP Inhibitors Market Trends

Asia Pacific is expected to witness the fast compound annual growth rate (CAGR) in the CGRP inhibitors market during the forecast period. This surge is primarily attributed to the rising incidence of migraines, influenced by cultural, lifestyle, and environmental stressors such as poor sleep, emotional strain, and dietary habits. As awareness grows and the need for effective migraine therapies increases, CGRP inhibitors are emerging as a crucial solution.

A January 2024 study found that in India, migraine triggers included emotional stress (97.5%), weather changes (69%), physical exertion (64.5%), missed meals (63.5%), travel (55.5%), and sleep deprivation (55%). These widespread triggers are fueling demand for advanced treatment options, making APAC a significant growth region for CGRP inhibitor adoption.

Market Competitive Landscape

The global CGRP inhibitors market is highly competitive, dominated by key players such as Amgen, Eli Lilly, and Teva Pharmaceuticals. These companies focus on innovation, strategic partnerships, and expanding product pipelines. Continuous clinical trials and regulatory approvals drive market positioning, while efforts to improve drug accessibility and affordability enhance competitive advantage.

Key Industry Developments:

- In November 2025, Pfizer’s India arm announced the launch of rimegepant, a calcitonin gene–related peptide (CGRP) receptor antagonist, for the acute treatment of migraine in adults who previously had an inadequate response to triptans.

- In August 2024, Organon healthcare company with a focus on women’s health, announced it has expanded its agreement with Eli Lilly and Company to become the sole distributor and promoter for the migraine medicine Emgality ® (galcanezumab) in the following additional markets: Canada, Colombia, Israel, South Korea, Kuwait, Mexico, Qatar, Saudi Arabia, Taiwan, Turkey and the United Arab Emirates.

- In April 2024, AbbVie announced an interim analysis of an ongoing Phase 3, open-label 156-week extension study evaluating the long-term safety and tolerability of oral atogepant for the prevention of migraine in participants with chronic or episodic migraine.

- In March 2023, the FDA approved Pfizer’s ZAVZPRET™ (zavegepant), a nasal spray treatment for migraines.

Companies Covered in CGRP Inhibitors Market

- AbbVie Inc.

- Amgen Inc.

- Eli Lilly and Company

- Teva Pharmaceutical Industries Ltd.

- Pfizer Inc.

- Lundbeck A/S

- Novartis AG

Frequently Asked Questions

The market is estimated to be valued at US$ 6.5 Bn in 2026.

Rising migraine prevalence, effective oral and injectable therapies, growing awareness, improved healthcare access, and expanding clinical approvals drive the CGRP inhibitors market.

The global market is expected to witness a CAGR of 9.7% between 2026 and 2033.

Major players include Amgen Inc., Teva Pharmaceutical Industries Ltd., Eli Lilly and Company, Lundbeck A/S, AbbVie Inc., Pfizer Inc. and Others.

North America is the leading region in the global CGRP inhibitors market.