- Smart Packaging

- CBD Pouches Market

CBD Pouches Market Size, Share, and Growth Forecast, 2026 - 2033

CBD Pouches Market by CBD Content (10-20 mg, Up to 10 mg, Others), Flavor (Flavored, Unflavored, Others), Distribution Channel, and Regional Analysis for 2026 - 2033

CBD Pouches Market Size and Trends Analysis

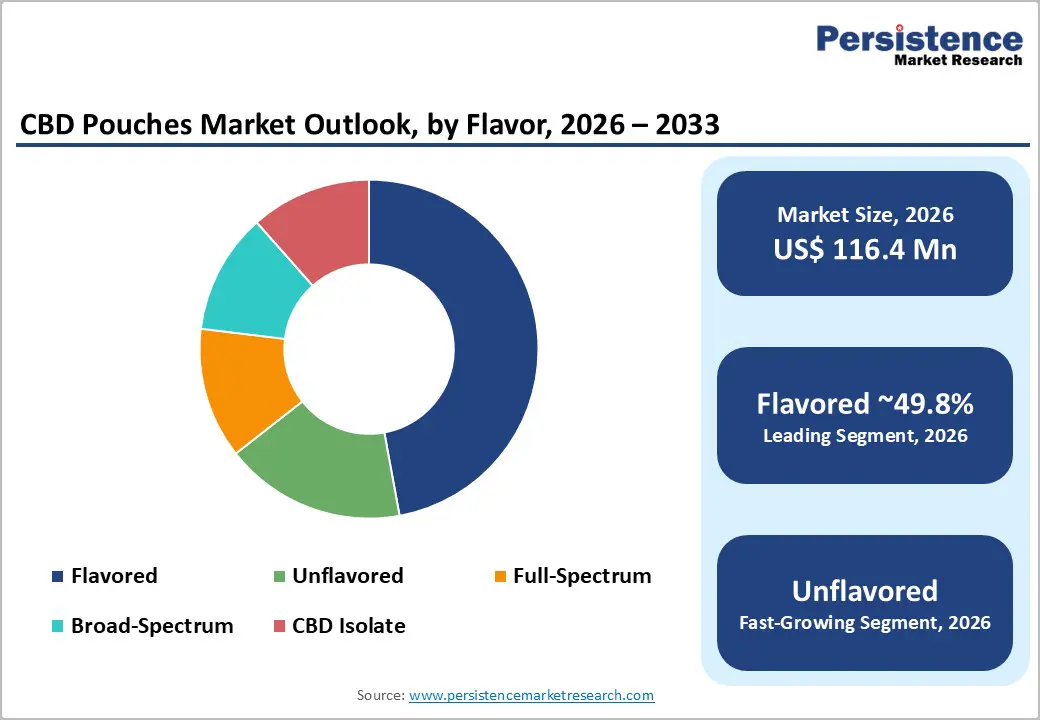

The global CBD pouches market size is likely to be valued at US$116.4 million in 2026 and is expected to reach US$407.2 million by 2033, growing at a CAGR of 19.6% between 2026 and 2033, driven by increasing consumer demand for discreet, smokeless cannabinoid consumption formats, continuous product-format innovation, and expanding retail availability across offline and digital channels.

Improvements in third-party testing transparency and product labeling are strengthening consumer confidence, while rapid product launches and packaging innovation are accelerating trial and repeat purchase. Broader wellness trends and the growing preference for alternatives to smoking further reinforce long-term adoption.

Key Industry Highlights

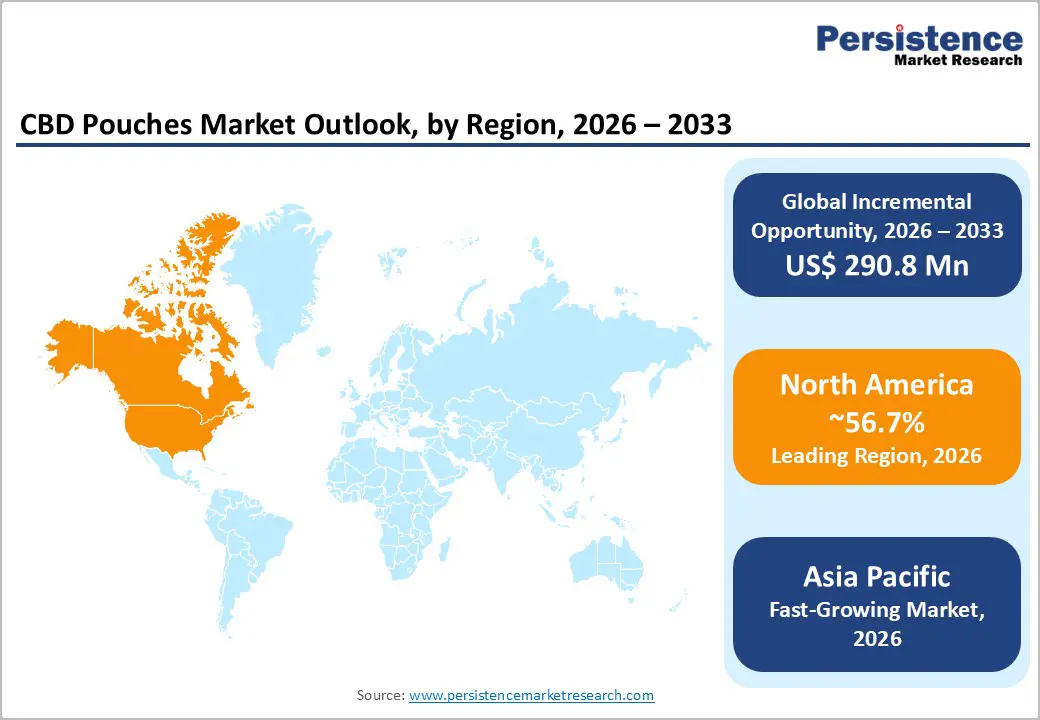

- Leading Region: North America is projected to account for over 56.7% of global market share, driven by strong consumer awareness, established hemp supply chains, mature convenience and specialty retail infrastructure, and early adoption of smokeless cannabinoid formats in the U.S.

- Fastest-growing Region: Asia Pacific, supported by expanding wellness consumption, rapid e-commerce penetration, manufacturing cost advantages, and growing acceptance of THC-non-detectable CBD products in markets such as Japan and parts of ASEAN.

- Dominant CBD Content: The 10-20 mg CBD pouch segment is anticipated to lead the market with a 49.8% share in 2026, reflecting its balance of noticeable effects and conservative dosing suitable for daily, workplace, and social use, making it the preferred strength range for both retailers and mainstream consumers.

- Leading Flavor: Flavored CBD pouches are estimated to dominate with an 85.6% market share, driven by strong consumer preference for mint, fruit, and botanical profiles that enhance trial, reduce sensory barriers, and support higher repeat purchase rates across offline and online retail channels.

| Key Insights | Details |

|---|---|

| CBD Pouches Market Size (2026E) | US$116.4 Mn |

| Market Value Forecast (2033F) | US$407.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 19.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 17.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Demand for Discreet, Smokeless Cannabinoid Delivery

Consumers are increasingly shifting away from inhalation-based cannabinoid formats toward oral and smokeless alternatives that offer greater discretion and convenience. CBD pouches provide a controlled per-dose experience without smoke, vapor, or odor, making them suitable for workplace, travel, and social settings. This functional advantage supports higher frequency usage and broadens the addressable consumer base. From a commercial perspective, pouch formats enable efficient SKU expansion across strengths and flavors, improving shelf productivity for retailers. For manufacturers, consistent dosing accuracy, validated certificates of analysis (COAs), and compliance-oriented packaging are critical to converting first-time users into repeat purchasers.

Offline and Omnichannel Retail Expansion

Brick-and-mortar retail continues to account for the majority of CBD pouch sales, supported by strong impulse purchasing and product discoverability. Convenience stores, specialty retail outlets, and independent wellness stores remain key revenue contributors, while online channels are expanding at a faster pace. Offline retail provides immediate scale and consumer exposure, whereas digital platforms enable rapid product iteration, subscription models, and direct customer engagement. Manufacturers that secure multi-chain retail partnerships while simultaneously building compliant digital commerce capabilities benefit from accelerated national rollouts, stronger margins, and diversified channel risk.

Product Innovation and Functional Positioning

Ongoing innovation in formulation, flavor engineering, and dosage precision is materially enhancing consumer adoption. Manufacturers are introducing a wide range of CBD strengths, terpene-driven flavor systems, and functional blends targeting sleep, relaxation, focus, and energy use cases. Controlled-release matrices and botanical adjuncts improve palatability and perceived efficacy. Strategic investment in formulation science and chemistry, manufacturing, and controls (CMC) capabilities improves product stability and shelf life, enabling premium pricing and increasing customer lifetime value.

Barrier Analysis - Regulatory Uncertainty for Ingestible CBD Products

Global regulatory frameworks for ingestible CBD remain fragmented and restrictive. In the U.S., CBD is not currently permitted for use in food or dietary supplements at the federal level, limiting permissible claims and complicating interstate commerce. In Europe, CBD is classified as a novel food, with ongoing data requirements delaying market authorizations. These uncertainties increase time-to-market and raise compliance costs by an estimated 8-15% for companies entering multiple jurisdictions. Regulatory non-compliance may result in product delistings, warning letters, or forced reformulation.

Quality, Consistency, and Safety Concerns

Long-term safety data for sustained or high-dose CBD use remain limited, and CBD is known to interact with certain prescription medications. Inconsistent labeling, inaccurate dosage claims, or inadequate third-party testing undermine consumer trust and retailer confidence. A failed laboratory analysis or safety issue can reduce reorder rates by more than 40% in affected channels and expose brands to regulatory scrutiny. Effective mitigation requires conservative dosing strategies, rigorous pharmacovigilance programs, and transparent, standardized third-party testing protocols.

Opportunity Analysis - International Expansion into Regulated Markets

As regulatory clarity improves, international markets in Europe and the Asia Pacific present significant growth potential. Even under conservative regulatory regimes, companies that invest in robust safety dossiers, localized packaging, and jurisdiction-specific compliance strategies can secure early mover advantages. Successful entry into selected European and Asia Pacific markets could generate 10-20% incremental global market share, equivalent to US$40-80 million in additional annual revenue for early entrants.

Premiumization and Functional Product Extensions

Consumers increasingly demonstrate a willingness to pay a premium for products that offer verified purity, precise dosing, and functional benefits such as sleep support or daytime focus. A premium sub-segment commanding a 15-25% price premium could represent 15-25% of total market revenue by 2030. Companies can unlock this opportunity by supporting product claims with human pharmacokinetic data, forming clinical research partnerships, and obtaining recognized quality certifications that enable entry into pharmacy and premium retail channels.

Direct-To-Consumer and Subscription Models

Digital direct-to-consumer models allow manufacturers to capture higher margins, gather first-party consumer data, and build recurring revenue streams. Subscription programs improve replenishment frequency and reduce customer acquisition costs. Converting just 5-10% of offline purchasers into subscription customers can improve gross margins by 6-10 percentage points and generate 15-30% of a mature brand’s revenue base. Successful execution requires investment in customer relationship management systems, compliant digital marketing, and discreet subscription-friendly packaging.

Category-wise Analysis

CBD Content Insights

The 10-20 mg dosage range is anticipated to account for approximately 49.8% of market share, positioning it as the dominant CBD content segment. This dosage level strikes an effective balance between perceptible functional benefits and conservative daily intake, making it suitable for routine use in professional, social, and travel settings. Retailers favor mid-strength SKUs as they appeal to both existing CBD users and confident repeat buyers while limiting adverse-effect concerns. From a merchandising perspective, this segment performs strongly in mixed-flavor tins and starter variety packs, commonly used by brands to encourage trial, upselling, and brand switching.

CBD pouches containing up to 10 mg are projected to expand at an anticipated CAGR of 19.8%, making them the fastest-growing dosage segment. Growth is fueled by increasing consumer adoption of micro-dosing practices, regulatory environments favoring lower daily intake thresholds, and rising health-conscious purchasing behavior. These products are particularly attractive to first-time users, older demographics, and wellness-oriented consumers seeking subtle relaxation without functional impairment. The adoption is strongest in pharmacy-led, wellness, and clinical retail environments, where conservative dosing, clear labeling, and perceived safety play a decisive role in purchase decisions.

Flavor Insights

Flavored CBD pouches are anticipated to account for approximately 85.6% of the market share, reflecting strong consumer preference for enhanced sensory experiences. Popular profiles such as mint, citrus, berry, and botanical blends help reduce the natural bitterness of cannabinoid formulations and lower the entry barrier for adult users transitioning from nicotine pouches or other oral alternatives. Retail performance is strengthened by broad flavor portfolios, seasonal and limited-edition launches, and multi-flavor packs that increase basket size and encourage repeat purchasing. Brands leveraging flavor innovation often achieve higher shelf visibility and faster SKU turnover.

Unflavored CBD pouches are expected to grow at a CAGR of 17.8%, driven by rising demand for minimalist formulations with fewer additives. This segment appeals to consumers with dietary sensitivities, flavor fatigue, or those using CBD alongside prescription medications where neutrality is preferred. Unflavored products are gaining traction in pharmacy, medical-adjacent, and clinical wellness retail settings, where transparent labeling, ingredient simplicity, and dosage clarity are prioritized. Manufacturers increasingly position these SKUs as “clean-label” or purity-focused offerings to strengthen credibility and trust.

Regional Insights

North America CBD Pouches Market Trends - Retail Expansion and Omnichannel Brand Consolidation

North America is projected to remain the dominant market, capturing more than 56.7% of the total share and functioning as a key center for product innovation, consumer adoption, and retail expansion. The U.S. represents the largest contribution, supported by strong consumer awareness of CBD benefits, a well-established wellness ecosystem, and an extensive network of more than 45,000 licensed CBD retailers and specialty outlets nationwide. Across convenience and specialty retail channels, brands such as Cannadips, FlowBlend, and On! have expanded their physical presence, with On! notably forming partnerships with major Midwest retail chains in 2025 to enhance visibility and accessibility across core U.S. markets.

Ongoing acquisition activity, such as Swedish Match’s 2025 acquisition of a flavored CBD pouch competitor to broaden its product portfolio and accelerate flavor innovation, highlights continued consolidation and portfolio diversification in the region. Domestic brands are also increasingly adopting omnichannel strategies that combine in-store distribution with strong direct-to-consumer platforms to drive repeat purchases and foster brand loyalty.

Canada operates within a more tightly regulated adult-use cannabis framework, enabling structured distribution through licensed dispensaries alongside hemp-derived product channels. Canadian multinational companies, including Tilray Brands, leverage integrated CBD and cannabis portfolios to support compliance, exports, and expansion across U.S. and international markets. This cross-border activity strengthens regional supply chains and allows companies to capitalize on regulatory differences as they expand into neighboring markets.

Overall regional growth is underpinned by diversified product offerings, broad retail penetration, and targeted marketing to adult consumers seeking smokeless nicotine alternatives. Regulatory uncertainty in the U.S., particularly evolving federal guidance around hemp-derived CBD products, has encouraged companies to pursue dual go-to-market approaches that encompass both hemp-based pathways and regulated cannabis channels where permitted. Brands that prioritize compliant supply chains, third-party testing, and diversified distribution models are better positioned to sustain long-term growth in the North American market.

Europe CBD Pouches Market Trends - Novel-Food Regulation Shaping Market Access and Scale

Europe represents a well-established consumer market characterized by high wellness spending and growing interest in CBD products, including CBD pouches, particularly across Germany, the U.K., France, and Spain, which together account for a substantial share of regional consumption. Germany remains the leading market, supported by strong demand for natural health solutions and an expanding range of CBD products available through both retail and pharmacy channels.

In the U.K., regulatory progress, most notably the advancement of the novel-foods approval process for a large number of CBD isolate products, signals increasing clarity that is expected to support wider retail distribution and strengthen consumer confidence in compliant, standardized CBD formats. Ongoing consultations and steps toward formal authorizations by the Food Standards Agency represent meaningful progress following years of regulatory uncertainty, opening clearer pathways for established brands to scale.

Despite favorable demand trends, Europe’s regulatory landscape remains challenging. The EU novel-food framework requires extensive safety data and detailed dossiers, often extending approval timelines and increasing upfront compliance costs. In markets such as France and Spain, strong uptake through specialty retail is tempered by country-specific regulatory requirements related to labeling and permissible formulations, requiring careful planning for companies seeking multi-country expansion. In response, European CBD and pouch manufacturers are increasingly pursuing partnerships, product innovation, and localized market-entry strategies.

For instance, collaborations between established European pouch manufacturers and regional distributors have broadened the availability of flavored and terpene-enhanced products in markets such as Sweden and Switzerland, improving consumer reach and market penetration. While continued progress in novel-food approvals is expected to accelerate growth over time, near-term success in Europe will depend on precise regulatory compliance, solid scientific validation of product safety, and strategic alliances with experienced distributors and wellness retailers across the region.

Asia Pacific CBD Pouches Market Trends - Regulatory Liberalization and Cross-Border Market Entry

Asia Pacific is emerging as the fastest-growing region for CBD pouches, driven by rising wellness awareness, expanding e-commerce adoption, and gradually evolving regulatory frameworks. Although the region currently accounts for a smaller share of global demand compared with North America and Europe, markets such as Japan, Australia, South Korea, and select ASEAN countries are showing rapid growth and strong long-term potential.

Japan, in particular, is easing certain CBD-related regulations and permitting wider availability of THC-free CBD products, creating early opportunities for flavored and functional CBD pouch formats as health-conscious consumers seek smokeless alternatives to tobacco and nicotine. Western brands, including Cannadips and FlowBlend, have begun entering Japan and Australia with streamlined, wellness-oriented CBD pouch offerings tailored to local consumer preferences. Australia’s regulatory landscape, supported by over-the-counter CBD approvals and broader access through pharmacy and wellness retail channels, further enhances consumer availability.

South Korea is also demonstrating growing institutional support, with government funding directed toward CBD product innovation, including improvements in bioavailability, indicating interest in advancing functional CBD formulations beyond traditional applications. China continues to play a critical role as a manufacturing and export hub for CBD raw materials and finished products, despite strict domestic regulations that limit consumer-facing applications. Meanwhile, India and ASEAN markets represent early-stage but expanding opportunities, where successful market entry depends on effective regulatory navigation and partnerships with local distributors.

Regional strategies are increasingly shaped by manufacturing cost advantages and cross-border e-commerce pilots that allow brands to gauge consumer demand without committing to full-scale retail launches. Companies that prioritize regulatory compliance, culturally adapted product design, and consumer education to address regulatory and safety concerns are best positioned to translate early market interest into sustainable revenue growth across the Asia Pacific region.

Competitive Landscape

The global CBD pouch market remains moderately fragmented, characterized by specialist pouch brands and diversified CBD product manufacturers. While several players command a strong regional presence, overall market concentration remains limited. Competitive differentiation is driven by brand credibility, product quality, regulatory compliance, and distribution reach.

Recent developments include international market expansion, new product launches emphasizing functional benefits, and regulatory-driven reformulation efforts. These initiatives reflect a broader industry shift toward compliance-led growth and portfolio diversification.

Leading companies focus on innovation, omnichannel distribution, and quality leadership. Subscription models, vertical supply control, and white-label manufacturing partnerships are emerging as scalable growth strategies.

Key Industry Developments

- In March 2025, Health Canada updated the Cannabis Regulations to simplify packaging and labeling requirements, thereby easing compliance burdens for CBD pouch producers and distributors in the Canadian market.

- In January 2025, Green Meadows partnered with Palisade Apothecary to introduce JuanaDips THC pouches in Massachusetts, expanding market access for cannabis-derived pouch products in the Northeast U.S.

Companies Covered in CBD Pouches Market

- Cannadips

- FlowBlend

- Voon Innovations

- Lyfted Made

- Black Buffalo (CBD product line)

- Outdare

- SpectrumLeaf

- Hemp & Barrel

- Cannapresso

- ACE pouches (brand)

- Snusline

- Social CBD

- Simply CBD

- CBDfx

- Green Roads

- Lazarus Naturals

- Charlotte’s Web

- Pure Ratios

Frequently Asked Questions

The global CBD pouches market size is estimated at US$116.4 million in 2026.

By 2033, the CBD pouches market is projected to reach US$407.2 million, reflecting strong expansion across consumer wellness and smokeless product categories.

Key trends include rising demand for discreet and smokeless CBD formats, increasing adoption of micro-dosing pouches, expansion of flavored and functional variants, and rapid growth of direct-to-consumer and subscription sales models.

By CBD content, the 10-20 mg dosage segment leads the market, accounting for the largest share due to its balance between noticeable effects and conservative dosing suitable for daily use.

The CBD pouches market is expected to grow at a CAGR of 19.6% between 2026 and 2033.

Major players include Cannadips, FlowBlend, Voon Innovations, Lyfted Made, and Black Buffalo.