- Medical Devices

- Capillary Electrophoresis Market

Capillary Electrophoresis Market Size, Share, and Growth Forecast 2026 - 2033

Capillary Electrophoresis Market by Product (Instruments, Consumables, Software), Mode (Capillary Zone Electrophoresis, Capillary Gel Electrophoresis, Capillary Electrochromatography), End-user (Research Organizations, Pharmaceutical and Biotechnology Companies, Clinical Laboratories), and Regional Analysis, 20262033

Capillary Electrophoresis Market Share and Trends Analysis

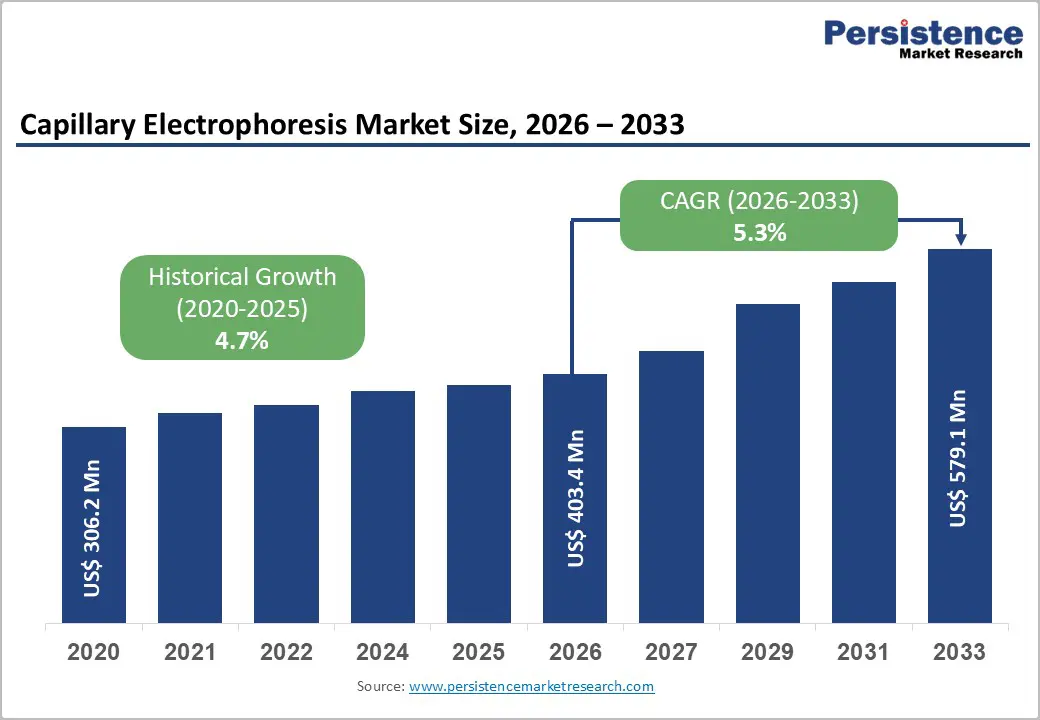

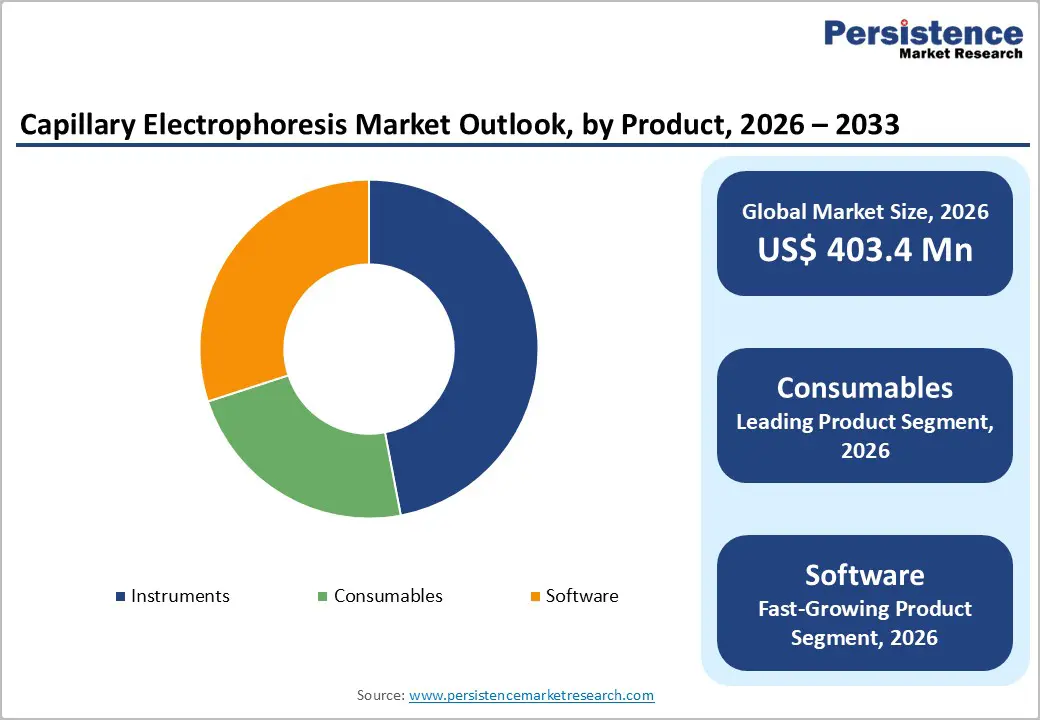

The global capillary electrophoresis market size is expected to be valued at US$ 403.4 million in 2026 and projected to reach US$ 579.1 million by 2033, growing at a CAGR of 5.3% between 2026 and 2033. Expanding biopharmaceutical quality control applications, rising adoption of nucleic acid and protein analysis within genomics and proteomics research, and the growing deployment of CE as a regulatory-mandated analytical technique for biologics characterization have fueled growth.

According to the International Council for Harmonisation (ICH), CE-based analytical methods are formally recognized in ICH Q2(R2) Analytical Method Validation guidance, cementing its role in pharmaceutical quality assurance workflows globally. The accelerating biologics pipeline, with the Pharmaceutical Research and Manufacturers of America (PhRMA) reporting over 900 biologics in late-stage clinical development, is sustaining above-average CE consumables and software demand.

Key Industry Highlights:

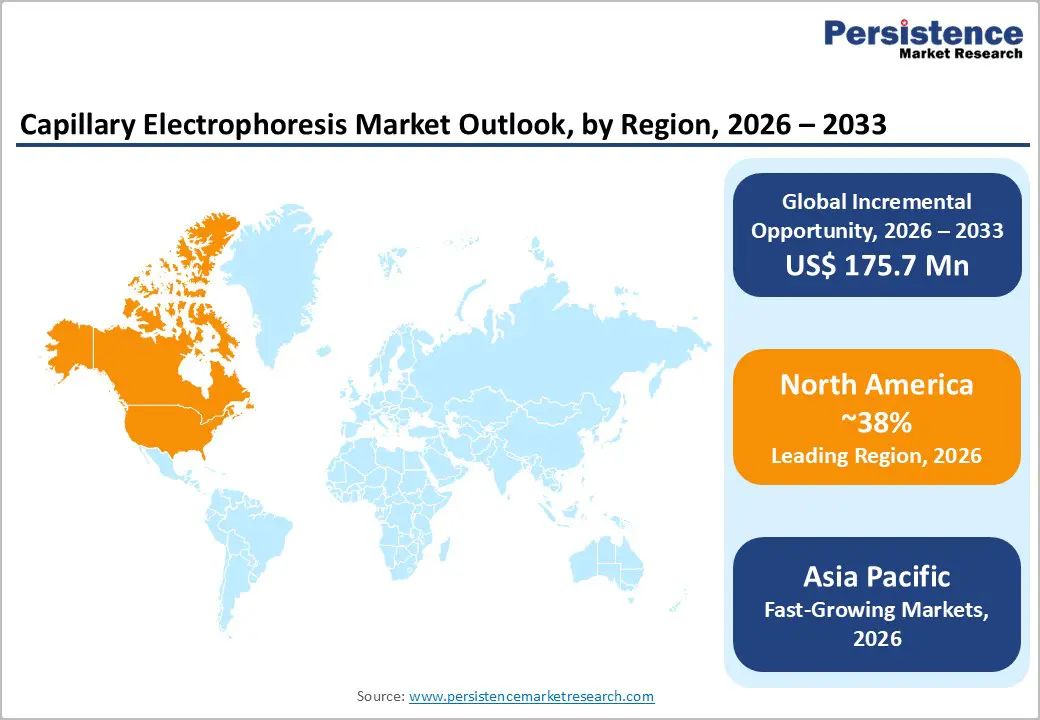

- Leading Region - North America commands 38% of the global CE market in 2026, anchored by the U.S.'s 900+ late-stage biologics pipeline requiring CE-based lot release testing, NIH-funded genomics research programs, and FDA 21 CFR Part 11-driven CE software investment in pharmaceutical QC laboratories.

- Fast-Growing Region - Asia-Pacific is the fastest-growing CE market, driven by China's 35% regional share under NMPA-ICH harmonization, India's biosimilar manufacturing CE compliance investment, and Southeast Asia's expanding CE-based newborn hemoglobin screening programs in Thailand, Vietnam, and Malaysia.

- Dominant Product Segment - Consumables are likely to lead with 47% share in 2026, generating predictable recurring revenues through mandatory capillary replacement every 50-200 runs and reagent kit consumption in FDA-regulated pharma QC workflows for 500+ approved biologics requiring ongoing CE lot release testing.

- Fast-Growing Product Segment - Software: Software is the fastest-growing product type, driven by FDA 21 CFR Part 11 and EMA Annex 11 compliance requirements, creating recurring software licensing demand, AI-powered CE data analytics integration by Agilent and Thermo Fisher, and emerging SaaS subscription models for pharmaceutical laboratory CE platforms.

- Key Opportunity - Clinical Laboratory CE Expansion: CE-based hemoglobin variant analysis for thalassemia and sickle cell screening targeting the WHO-estimated 300,000 annual severe hemoglobin disorder births represents a high-volume clinical laboratory growth opportunity as India, China, and Southeast Asia scale national newborn screening programs through 2033.

Market Dynamics

Drivers - Expanding Biopharmaceutical Quality Control Applications Mandating Capillary Electrophoresis Use

Capillary electrophoresis has become an indispensable analytical tool in biopharmaceutical quality control, mandated by global regulatory agencies for characterization of biologics, including monoclonal antibodies (mAbs), antibody-drug conjugates (ADCs), and gene therapy vectors. The U.S. FDA's guidance documents for biologics license applications (BLAs) require CE-based methods, including capillary isoelectric focusing (cIEF) and capillary sodium dodecyl sulfate electrophoresis (CE-SDS) for charge heterogeneity and molecular weight characterization of therapeutic proteins.

The European Medicines Agency (EMA) similarly mandates CE analytical methods under European Pharmacopoeia Chapter 2.2.47. With the Biotechnology Innovation Organization (BIO) reporting over 500 FDA-approved biologics on the U.S. market requiring ongoing lot release testing, CE consumable demand generates a predictable, high-frequency, non-discretionary revenue stream that directly underpins the Consumables segment's market leadership.

Genomics and Proteomics Research Expansion Driving CE Adoption in Academic and CRO Laboratories

The global expansion of genomics and proteomics research programs is driving substantial growth in capillary electrophoresis adoption across academic research institutes, genome centers, and contract research organizations. CE's unique capability for high-resolution, automated separation of DNA fragments, RNA species, and protein charge variants makes it the analytical technique of choice for next-generation sequencing (NGS) library quality control, gene therapy vector characterization, and protein glycoform analysis.

The National Human Genome Research Institute (NHGRI) has invested over US$ 3 billion cumulatively in genomics research infrastructure, with CE-based fragment analysis used in functional genomics and gene editing quality assessment. The Agilent Technologies Inc. Bioanalyzer and PerkinElmer Inc. LabChip platforms, both CE-based microfluidic systems, have achieved near-universal adoption in NGS library QC workflows globally, sustaining strong consumable pull-through demand.

Restraints - High Capital Cost and Technical Complexity Limiting Adoption in Resource-Constrained Settings

High-performance capillary electrophoresis systems from Agilent Technologies Inc. and Thermo Fisher Scientific Inc. carry purchase prices ranging from US$ 30,000 to US$ 150,000+ per instrument, representing a significant capital barrier for academic research laboratories and diagnostic centers in emerging economies.

Beyond instrument acquisition costs, CE systems require specialized fused-silica capillaries, buffer solutions, and trained operators, creating ongoing operational costs that further restrict adoption in budget-limited research environments. The National Institutes of Health (NIH) grant funding cycles introduce acquisition timing uncertainty for U.S. academic labs, creating lumpy capital purchase patterns that challenge revenue predictability for CE manufacturers.

Opportunities - Software and Data Analytics: Fastest-Growing Segment Driven by Regulatory Data Integrity Requirements

The Software segment represents the fastest-growing product category in the capillary electrophoresis market, projected to deliver the highest CAGR through 2033, driven by intensifying regulatory data integrity requirements in pharmaceutical laboratories and the growing complexity of CE data analysis for biologics characterization. The FDA's 21 CFR Part 11 and EMA's Annex 11 electronic records and signatures regulations require CE software to maintain complete audit trails, electronic batch records, and 21 CFR Part 11-compliant data management, creating recurring software licensing and maintenance revenue opportunities for instrument manufacturers.

Agilent Technologies Inc.'s OpenLAB CDS and Thermo Fisher Scientific's Chromeleon CDS platforms command significant per-laboratory subscription revenues. As AI-driven peak integration and automated reporting features are integrated into CE software platforms, subscription-based SaaS models are emerging as a high-margin revenue opportunity for leading instrument companies through 2033.

Category-wise Analysis

Product Insights

The consumables segment leads the global capillary electrophoresis market by product, commanding approximately 47% share in 2026. Consumables, including fused-silica capillaries, buffer solutions, gel matrices, polymer solutions, CE-SDS reagent kits, and microfluidic chips, generate recurring, high-frequency revenues that provide the most predictable commercial revenue stream in the CE market.

Every CE analysis requires fresh consumable inputs: capillaries require replacement every 50-200 runs, depending on the application, and biopharmaceutical QC laboratories performing hundreds of daily analyses consume substantial reagent volumes. The mandatory nature of consumable replenishment in FDA and EMA-regulated pharmaceutical QC workflows creates non-discretionary procurement demand. Software is the fastest-growing product segment, driven by 21 CFR Part 11 compliance requirements and AI-powered data analytics integration across pharmaceutical laboratory networks.

Mode Insights

The capillary zone electrophoresis (CZE) mode leads the capillary electrophoresis market, accounting for approximately 42% share in 2026. CZE's market leadership reflects its status as the simplest, most widely applicable CE mode enabling separation of charged analytes, including amino acids, peptides, proteins, organic acids, and inorganic ions based purely on electrophoretic mobility differences without a sieving matrix. CZE's versatility across pharmaceutical QC, environmental monitoring, and food safety testing applications drives broad adoption across diverse end-user segments. The European Pharmacopoeia references CZE methods for multiple pharmaceutical monographs, ensuring its continued use in regulated pharmaceutical quality control. Capillary Gel Electrophoresis (CGE) including CE-SDS for protein molecular weight analysis, is the second-largest mode, representing the biopharmaceutical industry's most critical CE application for mAb characterization.

End-user Insights

Pharmaceutical and Biotechnology Companies represent the leading end-user segment in the Capillary Electrophoresis market, commanding approximately 44% of the total revenue share in 2025. The pharmaceutical and biotech sector drives this leadership through mandatory, non-discretionary CE-based quality control testing embedded across biologics development and commercial manufacturing workflows.

Every FDA-licensed biologic product requires ongoing lot release testing using CE methods for charge heterogeneity (cIEF) and molecular weight assessment (CE-SDS), generating predictable, recurring reagent and consumable demand. Large biopharma companies, including Roche, AbbVie, Amgen, and Johnson & Johnson, operate extensive CE platforms across their global QC laboratory networks. Research Organizations are the second-largest segment, while Clinical Laboratories are the fastest-growing end-user, driven by hemoglobinopathy screening expansion and CE-based serum protein electrophoresis for myeloma diagnosis.

Regional Insights

North America Capillary Electrophoresis Market Trends and Insights

North America leads the global Capillary Electrophoresis market with 38% of market share in 2025, anchored by the U.S.'s dominant biopharmaceutical manufacturing sector, FDA 21 CFR Part 11-driven software investment, and the highest concentration of academic genomics and proteomics research programs funded by NIH and NHGRI. Strong biologics pipeline volumes and clinical laboratory hemoglobin screening programs sustain above-average CE consumable demand.

U.S. Capillary Electrophoresis Market Size

The U.S. accounts for approximately 87% of North America's CE market revenue, driven by its 900+ biologics in late-stage development per PhRMA, the world's largest concentration of biopharma QC laboratories requiring mandatory CE-based lot release testing, and extensive NIH-funded genomics research programs deploying CE for fragment analysis and NGS library QC.

Europe Capillary Electrophoresis Market Trends and Insights

Europe is the second-largest CE market, driven by European Pharmacopoeia Chapter 2.2.47 mandating CE analytical methods in pharmaceutical quality control, a dense biopharmaceutical manufacturing sector in Germany, the UK, Switzerland, and France, and active academic proteomics research across EU-funded programs. EU MDR and IVDR regulatory frameworks are also expanding CE adoption in clinical laboratory applications.

Germany Capillary Electrophoresis Market Size

Germany holds approximately 23% of the European CE market revenue, home to major pharma companies including Merck KGaA, Bayer, and Boehringer Ingelheim, operating extensive CE-based QC laboratories. Germany's dense network of Max Planck Institute and Helmholtz Association research centers drives strong academic CE consumables and instrument demand.

UK Capillary Electrophoresis Market Size

The UK contributes approximately 18% of European CE revenues, supported by its thriving biotech cluster in London and Cambridge, strong MHRA-regulated pharmaceutical QC infrastructure, and Medical Research Council (MRC)-funded proteomics and genomics programs at institutions including Wellcome Sanger Institute, deploying CE for high-throughput DNA fragment analysis.

France Capillary Electrophoresis Market Size

France accounts for approximately 14% of the European CE market revenues, driven by its significant pharmaceutical manufacturing sector anchored by Sanofi and Servier, active INSERM-funded biomedical research programs, and national hemoglobinopathy screening programs deploying CE-based platforms for newborn screening across French public health laboratories.

Asia Pacific Capillary Electrophoresis Market Trends and Insights

Asia-Pacific is the fastest-growing CE market, driven by rapid biopharmaceutical manufacturing expansion in China, Japan, South Korea, and India, growing adoption of international regulatory standards requiring CE-based analytical methods, and national genomics initiatives deploying CE for population health research. China represents approximately 35% of Asia-Pacific CE revenues, with the NMPA harmonizing CE quality standards with ICH guidelines driving biopharma QC investment.

India Capillary Electrophoresis Market Size

India contributes approximately 11% of Asia-Pacific CE revenues, driven by its rapidly growing biosimilar manufacturing sector requiring CE-based characterization for FDA and EMA export market compliance, expansion of academic genomics research under Department of Biotechnology (DBT)-funded programs, and growing deployment of CE hemoglobin platforms for India's large thalassemia screening population.

Competitive Landscape

The Capillary Electrophoresis market is moderately competitive, driven by continuous innovation in analytical instruments, consumables, and software solutions. Market participants focus on improving automation, sensitivity, and throughput to meet rising demand from pharmaceutical, biotechnology, clinical diagnostics, and academic research applications. Strategic priorities include product upgrades, regulatory compliance, expansion into emerging markets, and integration with advanced detection technologies such as mass spectrometry. Recurring demand for consumables strengthens long-term revenue generation, while service-based offerings and technical support enhance customer retention.

Key Developments

- In March 2025, Thermo Fisher Scientific introduced the Applied Biosystems SeqStudio Flex Dx Genetic Analyzer. It is an IVDR-compliant capillary electrophoresis system that supports both clinical and research applications for Sanger sequencing and fragment analysis in targeted genomic testing.

- In January 2024, Agilent Technologies Inc. launched a new automated parallel capillary electrophoresis system called the Agilent ProteoAnalyzer system for protein analysis at the 23rd Annual PepTalk Conference. The new platform enhances and simplifies the efficiency of analyzing complex protein mixtures.

Global Capillary Electrophoresis Market - Key Insights

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 306.2 Million |

|

Current Market Value (2026) |

US$ 403.4 Million |

|

Projected Market Value (2033) |

US$ 579.1 Million |

|

CAGR (2026-2033) |

5.3% |

|

Leading Region |

North America, 38% market share (2025) |

|

Dominant Category-1 (Product) |

Consumables, ~47% market share (2025) |

|

Top-ranking Category-2 (Mode) |

Capillary Zone Electrophoresis, ~42% market share (2025) |

|

Incremental Opportunity |

US$ 175.7 Million (2026-2033) |

Companies Covered in Capillary Electrophoresis Market

- CBS Scientific

- Agilent Technologies Inc.

- Helena Laboratories

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- QIAGEN

- PerkinElmer Inc.

- Bio-Rad Laboratories Inc.

- Shimadzu Corporation

- Bio-Techne Corporation

- Merck KGaA

Frequently Asked Questions

The market is projected to reach US$ 393.0 Mn in 2025.

Increasing use in forensic casework and rising demand for paternity tests in specific countries are the key market drivers.

The market is poised to witness a CAGR of 5.2% from 2025 to 2032.

Investments in precision medicine and surging genomics research activities are the key market opportunities.

CBS Scientific, Agilent Technologies Inc., and Helena Laboratories are a few key market players.