- Animal Health

- Canine Leptospirosis Market

Canine Leptospirosis Market Size, Share, and Growth Forecast, 2026 - 2033

Canine Leptospirosis Market by Treatment Type (Vaccines, Antibiotics, Adjunctive Therapies, Advanced Therapies), Route of Administration (Oral, Intravenous, Intranasal), Distribution Channel (Veterinary Hospitals, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026-2033

Canine Leptospirosis Market Share and Trends Analysis

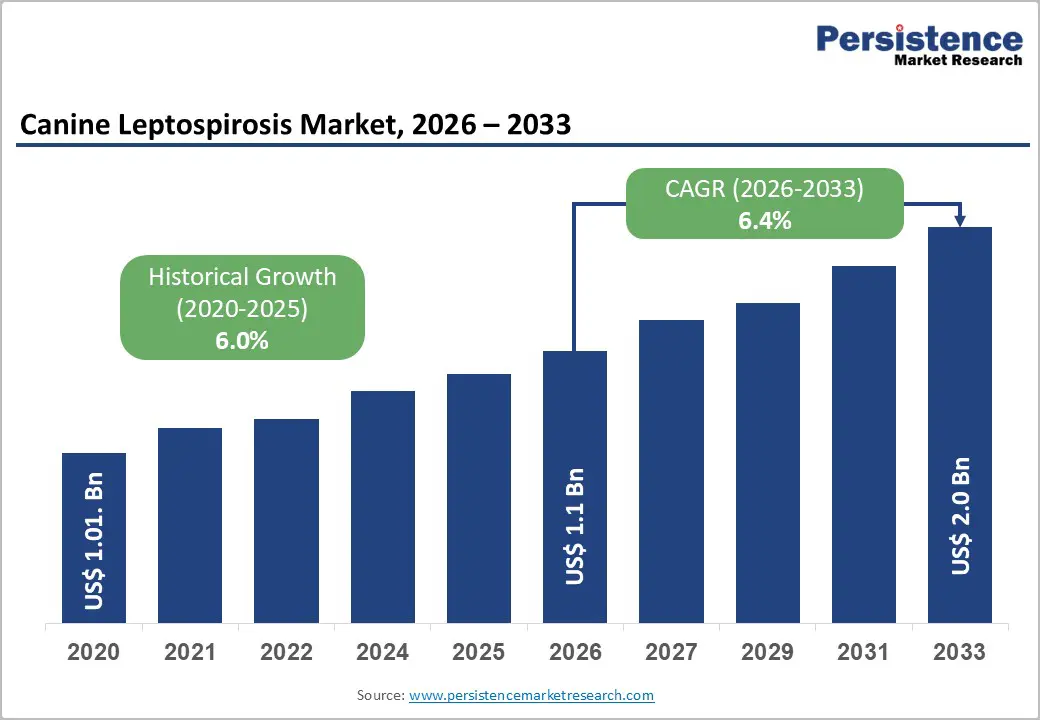

The global canine leptospirosis market size is likely to be valued at US$ 1.1 billion in 2026, and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 6.4% during the forecast period 2026−2033. This growth is powered by the increasing incidence of canine leptospirosis across geographies. Veterinarians and pet owners are recognizing the public health implications of zoonotic transmission, resulting in veterinary clinics recommending structured vaccination schedules and diagnostic screening programs.

Pharmaceutical companies are also introducing advanced multivalent vaccines and improved testing solutions, which are enhancing clinical outcomes and supporting long-term disease control initiatives. Regulatory alignment is further strengthening the commercial landscape. In 2024, the American Animal Hospital Association (AAHA) reclassified leptospirosis vaccination from a non-core category to a core protocol. This shift is standardizing annual immunization practices irrespective of lifestyle exposure risks. As clinics are adopting these updated guidelines, vaccine demand is becoming more consistent and predictable. Market participants are therefore focusing on supply chain stability, veterinarian education, and preventive health campaigns to ensure compliance and sustain uptake.

Key Industry Highlights

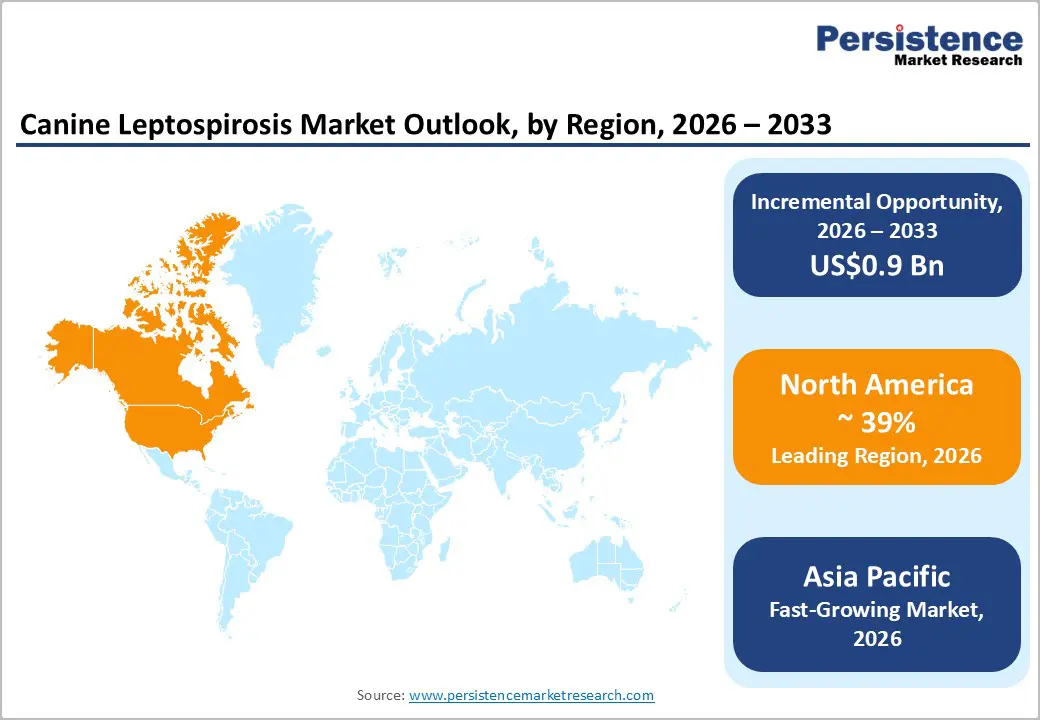

- Dominant Region: North America is expected to hold around 39% market share in 2026, supported by advanced veterinary infrastructure and widespread pet ownership culture.

- Fastest-growing Market: The Asia Pacific market is slated to be the fastest-growing through 2033, fueled by rapid urbanization and rising disposable incomes that transform pet ownership patterns.

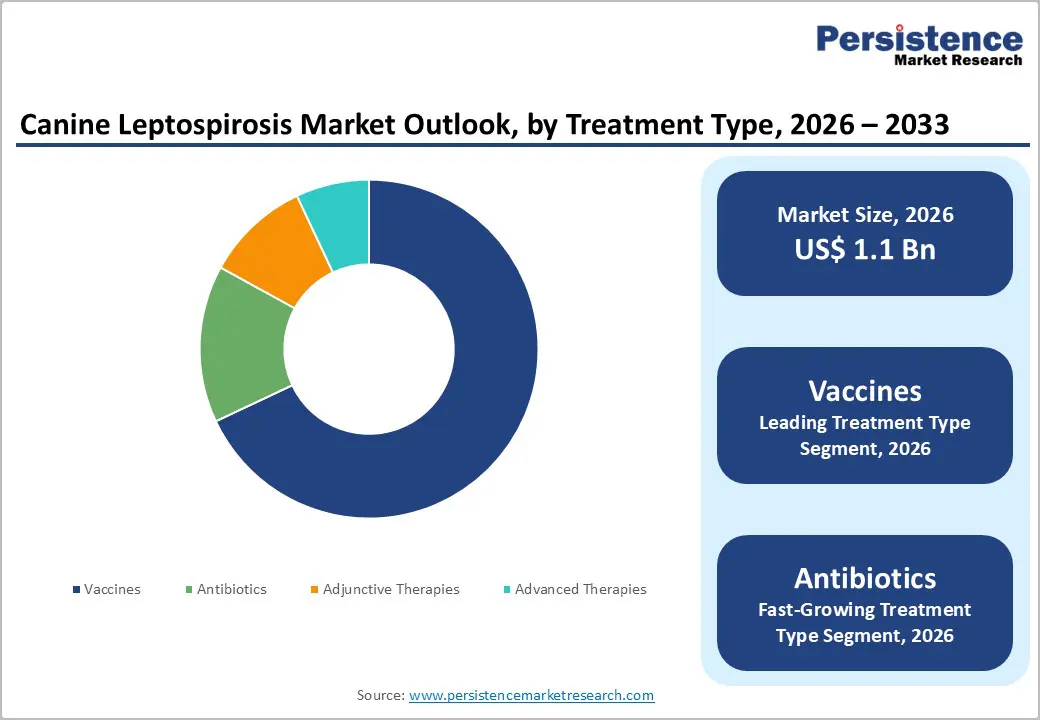

- Leading & Fastest-growing Treatment Type: Vaccines are poised to command approximately 68% of market revenues in 2026, while antibiotic therapeutics are likely to be the fastest-growing segment during the 2026-2033 forecast period.

- Leading & Fastest-growing Distribution Channel: Veterinary hospitals are set to lead with an estimated 55.4% revenue share in 2026, with online pharmacies growing the fastest between 2026 and 2033.

| Key Insights | Details |

|---|---|

| Canine Leptospirosis Market Size (2026E) | US$ 1.1 Bn |

| Market Value Forecast (2033F) | US$ 2.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Regulatory Mandate Evolution and Vaccination Protocol Standardization

The fundamental catalyst for the canine leptospirosis market stems from the 2024 guideline revision by the AAHA, which reclassified leptospirosis as a core vaccine for all dogs. This shift positions leptospirosis vaccination alongside other essential immunizations and embeds it within standard preventive care protocols. The guideline now recommends annual administration for every dog, irrespective of breed, region, or perceived exposure risk, which materially broadens the addressable vaccination base. For veterinary practices, this translates into a formalized obligation to discuss leptospirosis during routine wellness visits, update vaccination plans, and align reminder systems, such as digital recall tools and annual health plan templates, with the new standard.

By reframing leptospirosis as a ubiquitous threat rather than a localized or lifestyle disease, the consensus and subsequent guideline revisions reduce clinical ambiguity and support more assertive recommendations at the point of care. For manufacturers such as Zoetis, Merck Animal Health, and Boehringer Ingelheim, the regulatory alignment and unified clinical guidance provide stronger demand visibility and a clearer basis for long-term capacity planning. In practical terms, this supports decisions on scaling fill-finish operations, optimizing supply to veterinary distributors, and designing educational initiatives that help clinics integrate leptospirosis vaccination into comprehensive preventive health programs, rather than treating it as an optional add-on.

Stringent Regulatory Approval Processes and Development Cost Escalation

Regulatory authorities impose increasingly stringent requirements on pharmaceutical development for veterinary biologics. These frameworks demand thorough validation of safety and efficacy profiles. The United States Department of Agriculture (USDA) and the European Medicines Agency (EMA) in Europe lead with comprehensive standards, while Asian bodies maintain parallel oversight. Developers must conduct multi-year clinical trials to test products across diverse canine demographics and health conditions. Such rigorous processes ensure reliable performance data but significantly extend timelines for new vaccine candidates.

Veterinary manufacturers face particular hurdles in Asian markets, where approval cycles require additional harmonization efforts. These delays challenge strategic planning for global launches and resource allocation. Smaller biotechnology firms encounter high entry barriers due to substantial capital demands, which favor established players with proven compliance infrastructure. This dynamic limits the pace of innovation, especially for advanced recombinant vaccines and multivalent options targeting evolving Leptospira serovars such as Australis and Grippotyphosa. Companies can benefit by prioritizing modular development platforms and leveraging regulatory science expertise to navigate this complexity while maintaining competitive differentiation.

Growth in Veterinary Clinics and Animal Hospitals

The expansion of specialized veterinary clinics and animal hospitals drives significant market accessibility for canine leptospirosis treatments. These facilities adopt advanced diagnostic capabilities, such as point-of-care polymerase chain reaction (PCR) testing and rapid serology panels, which enable early detection and prompt intervention. Unlike general practices, specialty centers maintain dedicated infectious disease protocols and maintain an inventory of broad-spectrum antibiotics and supportive therapies tailored to leptospirosis cases. This infrastructure growth follows rising pet ownership rates and increased willingness among dog owners to seek premium care. Urbanization concentrates demand in metropolitan areas, where new clinic developments cluster near affluent residential zones. Corporate consolidations accelerate this trend as veterinary service chains standardize leptospirosis management across multiple locations, ensuring consistent treatment protocols and bulk procurement that lowers per-unit costs.

Emergency and referral hospitals contribute disproportionately to market volume through their capacity to handle severe cases requiring hospitalization, intravenous fluid therapy, and intensive monitoring. These facilities generate higher revenue per case due to comprehensive care packages that combine diagnostics, treatment, and follow-up consultations. For manufacturers, this clinic proliferation creates predictable distribution channels with higher order volumes and faster inventory turnover. Strategic partnerships with veterinary chains secure preferred supplier status, while clinic networks provide real-world evidence for product performance that supports regulatory submissions and marketing claims. The trend favors companies that offer bundled solutions combining therapeutics with diagnostic support services.

Category-wise Analysis

Treatment Type Insights

Vaccines are anticipated to be the dominant treatment type in 2026, commanding approximately 68% of the canine leptospirosis market revenue share, backed by expanding vaccination protocols and increased booster compliance. Veterinary medicine increasingly embraces preventive healthcare paradigms, positioning leptospirosis vaccination as a cornerstone of routine wellness protocols. This regulatory shift standardizes vaccination schedules across practices and drives consistent demand.

Zoetis' Vanguard L4 protects against four key Leptospira serovars with proven immunogenicity. Merck's NOBIVAC formulations deliver multivalent coverage through flexible administration options. Boehringer Ingelheim's EURICAN L4 offers robust serovar protection with favorable safety profiles across diverse canine populations.

Antibiotic therapeutics are likely to be the fastest-growing segment during the 2026-2033 forecast period, driven by rising infection incidence rates and improved diagnostic capabilities enabling timely treatment initiation. Doxycycline maintains preference as first-line therapy for early-stage leptospirosis due to its favorable pharmacokinetics and broad-spectrum activity against multiple serovars. Penicillin-based formulations, including ampicillin, retain clinical relevance for severe acute cases requiring hospitalization and intensive supportive care.

The antibiotic segment benefits from generic drug availability, reducing treatment costs while maintaining therapeutic efficacy. Market dynamics within this segment reflect growing emphasis on combination therapy protocols integrating multiple antibiotic agents with supportive interventions, including fluid therapy, renal support, and hepatic protection strategies for complicated leptospirosis cases requiring specialized veterinary critical care.

Route of Administration Insights

Intravenous is likely to lead by capturing approximately 52% of the canine leptospirosis market share in 2026. This route delivers antibiotics such as doxycycline and penicillin G directly into the bloodstream, achieving rapid therapeutic concentrations critical for combating systemic bacterial dissemination. Veterinary protocols prioritize IV therapy in hospitalized dogs exhibiting renal compromise or severe symptoms, ensuring optimal bioavailability and precise dosing adjustments based on clinical response. Hospital-based administration reinforces its dominance, as emergency clinics maintain dedicated IV fluid stations and monitoring equipment.

Oral is expected to be the fastest-growing administration route over the 2026-2033 forecast period, driven by demand for outpatient treatment protocols that enable home recovery. Tablets and suspensions offer convenient follow-on therapy after initial IV stabilization, improving owner compliance through simplified dosing schedules. Advances in palatable formulations and extended-release technologies reduce gastrointestinal side effects while maintaining steady-state drug levels. This shift aligns with preventive care trends and telemedicine integration, positioning oral delivery as preferred for mild-to-moderate cases and post-discharge management.

Distribution Channel Insights

Veterinary hospitals are expected to be the top distribution channel in 2026, holding an approximate 55.4% market revenue share. These facilities possess critical advantages including established veterinarian-client-patient relationships, diagnostic capabilities for leptospirosis confirmation, and clinical expertise for complex case management. Full-service veterinary hospitals offer comprehensive leptospirosis care including vaccination, acute treatment protocols, and chronic complication management, generating higher average transaction values compared to wellness-focused practices.

The segment benefits from pet insurance expansion, which reduces owner price sensitivity while supporting adherence to recommended vaccination schedules and treatment protocols.

Online pharmacies is projected to be the fastest-growing segment during the 2026-2033 forecast period, driven by digital transformation of veterinary healthcare delivery and consumer preference for convenience-oriented service models. Platforms including Chewy Pharmacy, PetMeds, and integrated telemedicine services expand market access by linking prescription issuance to home delivery of therapeutic agents, particularly oral antibiotics for uncomplicated leptospirosis treatment.

However, vaccine distribution through online channels remains constrained by cold-chain requirements and regulatory frameworks mandating veterinary administration for injectable biologics. The multi-channel distribution evolution enhances market efficiency while expanding geographic reach, particularly benefiting pet owners in rural or underserved areas with limited access to full-service veterinary facilities.

Regional Insights

North America Canine Leptospirosis Market Trends

North America is set to command a significant portion of the canine leptospirosis market share at approximately 39% in 2026 due to its advanced veterinary infrastructure and widespread pet ownership culture. The United States anchors regional dominance with extensive clinic networks and high preventive care adoption rates. Canada complements this leadership by enforcing strict animal health standards that promote consistent vaccination protocols. Mature reimbursement systems, including pet insurance coverage, reduce financial barriers for owners and encourage comprehensive wellness programs. This environment creates stable demand channels that favor manufacturers with established distribution partnerships.

Primary growth drivers stem from recent guideline revisions by the AAHA, which have elevated leptospirosis vaccination to core status within routine canine care. Veterinary practices now integrate these vaccines into standard examination protocols across diverse patient populations. The regional innovation ecosystem thrives with major players such as Zoetis, Merck Animal Health, and Elanco maintaining significant research and development investments in advanced vaccine formulations.

Competitive dynamics feature moderate concentration, where leading manufacturers control substantial market positions through differentiated product portfolios and strong clinician relationships. Investment flows toward digital health tools, telemedicine platforms, and data-driven practice management systems, positioning North America for sustained leadership as preventive care paradigms mature.

Europe Canine Leptospirosis Market Trends

Europe is foreseen to sustain strong positioning in the global market for canine leptospirosis through 2033, owing to unified regulatory oversight from the EMA and mature companion animal healthcare networks. Germany anchors regional leadership with rigorous animal health mandates that require broad vaccination coverage against core canine pathogens. The United Kingdom supports this foundation through extensive dog ownership and established veterinary infrastructure.

France and Spain contribute meaningfully as urban pet populations drive demand for accessible clinic services and preventive care solutions. The regulatory landscape shapes market evolution via the European Pharmacopoeia standards for leptospirosis vaccine development, testing, and performance validation.

This harmonization has streamlined approvals across member states while upholding stringent safety requirements. Geographic differences in vaccination compliance have created targeted opportunities for education campaigns aimed at veterinarians and pet owners. Key catalysts include heightened awareness of zoonotic transmission risks, reinforced by One Health initiatives post-COVID-19, stricter pet travel documentation rules, and boarding facility vaccination policies. Leading companies such as Boehringer Ingelheim, Virbac, and Ceva Santé Animale maintain competitive advantages through localized operations and expanded multivalent portfolios addressing regional serovar variations.

Investment focuses on next-generation formulations and clinician engagement programs, positioning Europe for steady expansion as preventive paradigms strengthen across diverse markets.

Asia Pacific Canine Leptospirosis Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for canine leptospirosis between 2026 and 2033, fueled by rapid urbanization and rising disposable incomes that transform pet ownership patterns. China leads with massive urban pet populations and expanding veterinary services, while India offers substantial untapped potential through concentrated canine ownership in cities. Government programs integrate animal and human health surveillance to address zoonotic threats systematically. Japan provides regional maturity through advanced pet healthcare systems and high per-animal spending on preventive treatments.

Prime ASEAN economies, mainly Thailand, Vietnam, the Philippines, and Indonesia, are experiencing an accelerated adoption of companion animals by middle-class households. Mass vaccination initiatives target rabies and related diseases, creating broad infrastructure for leptospirosis protocols. Manufacturing hubs attract global pharmaceutical firms that establish local production for domestic consumption and exports. Regulatory processes demand extended approvals, which balance innovation pace with quality assurance.

Multinational companies partner with regional distributors to penetrate markets effectively. Investments are targeting clinic networks, cold-chain systems, and veterinarian training programs that build diagnostic and treatment capabilities, positioning Asia Pacific as a pivotal engine for sustained global market development.

Competitive Landscape

The global canine leptospirosis market structure is moderately concentrated, with established animal health corporations shaping competitive dynamics through extensive vaccine and therapeutic portfolios. Key participants include Zoetis Inc., Merck & Co., Inc., Boehringer Ingelheim International GmbH, Elanco Animal Health Incorporated, and Pfizer Inc. These companies are competing through product differentiation, lifecycle management strategies, and strong distribution networks. They are investing in research and development to strengthen strain coverage and improve immunogenicity profiles. As a result, rivalry remains high because leading firms are protecting market share while expanding their preventive care offerings across veterinary channels.

Supplier bargaining power remains moderate because veterinary clinics are relying on branded vaccines that demonstrate validated safety and efficacy data. However, generic antibiotic therapies are providing limited pricing flexibility in treatment settings. The threat of new entrants continues to remain low due to regulatory barriers and capital intensity. Approvals from the USDA and the EMA are requiring rigorous compliance processes, including multi-year clinical trials and validated manufacturing standards. Companies that are planning market entry will therefore need to prioritize regulatory strategy, quality assurance systems, and scalable production capabilities to achieve sustainable participation in this structured competitive environment.

Key Industry Developments

- In January 2026, Virbac launched Canixin L, a new L2 leptospirosis vaccine for dogs designed to stimulate immunity against two key Leptospira interrogans serogroups and help reduce infection, clinical signs, kidney colonization, and urinary shedding. The vaccine, intended for puppies from eight weeks of age with a follow-up dose three to four weeks later, is positioned to play an important role in lowering disease transmission risks.

- In June 2025, MSD Animal Health received a positive opinion from the EMA’s Committee for Veterinary Medicinal Products (CVMP) for its NOBIVAC® L6 and NOBIVAC® LoVo L6 canine leptospirosis vaccines, which are now recommended for active immunization against six Leptospira serovars if the European Commission adopts the endorsement. These vaccines are positioned to be the first in the region with broad serovar coverage to prevent or reduce mortality, clinical signs, infection, renal lesions, and urinary shedding in dogs.

- In March 2025, Santa Barbara Humane began promoting updated canine vaccination guidance in which leptospirosis has been classified as a core vaccine by veterinary authorities, encouraging all dogs to receive protection against this potentially fatal bacterial disease. This shift reflects broader AAHA guideline changes that now consider leptospirosis vaccination essential due to infection risks for dogs and its potential to spread to humans.

Companies Covered in Canine Leptospirosis Market

- Zoetis Inc.

- Merck & Co., Inc.

- Boehringer Ingelheim International GmbH

- Elanco Animal Health Incorporated

- Virbac S.A.

- Ceva Santé Animale

- Pfizer Inc.

- Baxter International Inc.

- Sun Pharmaceutical Industries Ltd.

- Aurobindo Pharma Limited

- Zoetic Pharmaceuticals Private Limited

- Bioveta a.s.

- IDEXX Laboratories, Inc.

- Heska Corporation

Frequently Asked Questions

The global canine leptospirosis market is projected to reach US$1.1 Bn in 2026.

AAHA core vaccine designation and rising pet humanization are driving vaccine adoption across veterinary protocols.

The market is poised to witness a CAGR of 6.4% from 2026 to 2033.

Major opportunities lie in Asia Pacific urbanization and government zoonotic programs create massive untapped demand in high-growth emerging markets.

Zoetis Inc., Merck & Co., Inc., Boehringer Ingelheim International GmbH, Elanco Animal Health Incorporated and Pfizer Inc. are some of the key players in the market.