- Food Ingredients & Additives

- Cane Molasses Market

Cane Molasses Market Size, Share, and Growth Forecast 2026 - 2033

Cane Molasses Market by Nature (Organic, Conventional), by Application (Food & beverages, Animal feed, Ethanol/biofuel, Industrial uses), by Distribution Channel (Direct/wholesale, Retail stores, Supermarkets/hypermarkets, Online), by Regional Analysis, 2026 - 2033

Cane Molasses Market Share and Trends Analysis

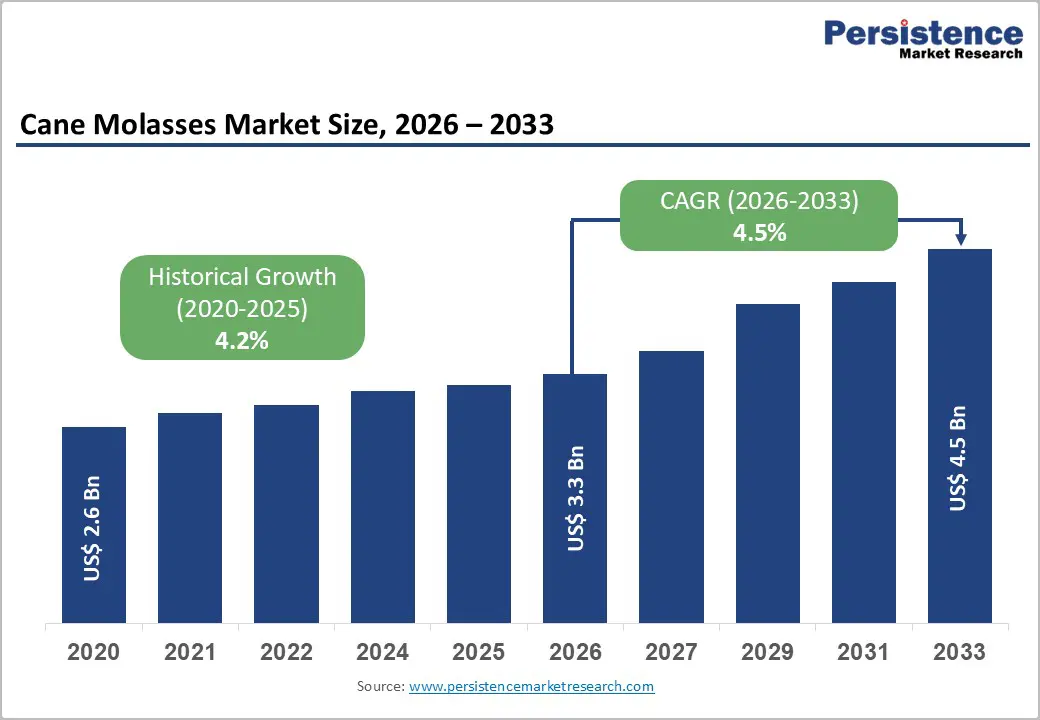

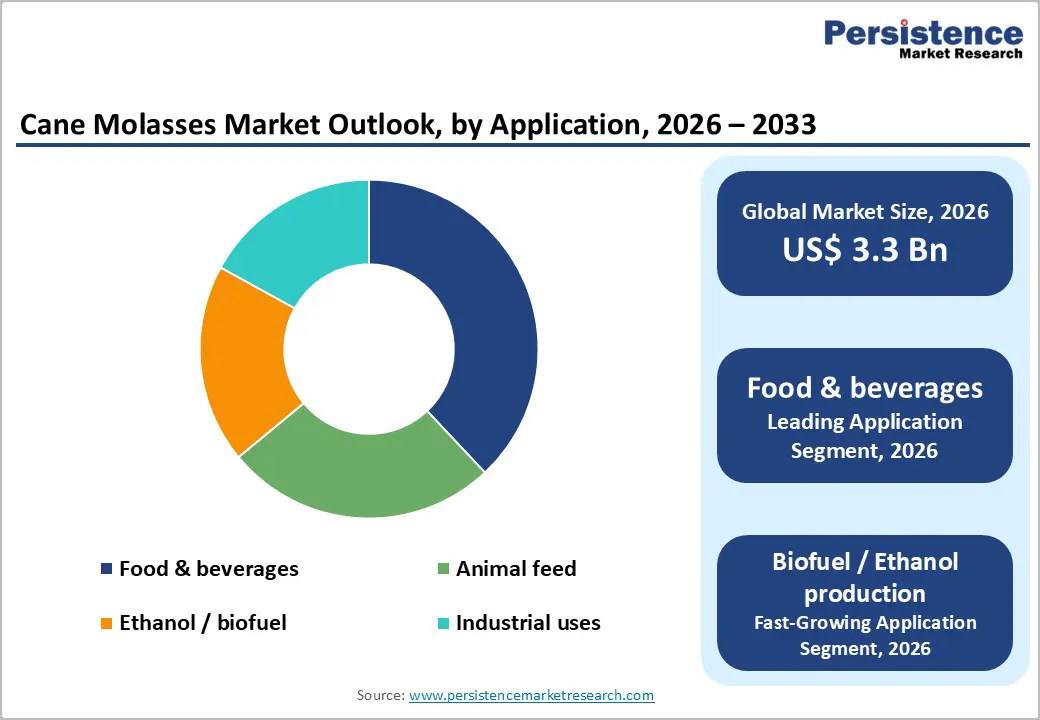

The global cane molasses market size is expected to be valued at US$ 3.3 billion in 2026 and projected to reach US$ 4.5 billion by 2033, growing at a CAGR of 4.5% between 2026 and 2033.

Market expansion is primarily driven by growing demand from the biofuel sector, particularly for ethanol production, as governments implement renewable energy mandates to reduce carbon emissions, supported by international climate commitments and renewable blending targets. In parallel, structural growth in the global livestock and animal feed industry is reinforcing molasses’ role as a cost-effective, energy-dense ingredient that enhances feed palatability and supports rumen function. Together with increasing use in food and beverage formulations as a clean-label sweetener and flavoring agent, these demand drivers create a resilient, multi-sector growth platform for the cane molasses market over the forecast horizon.

Key Industry Highlights:

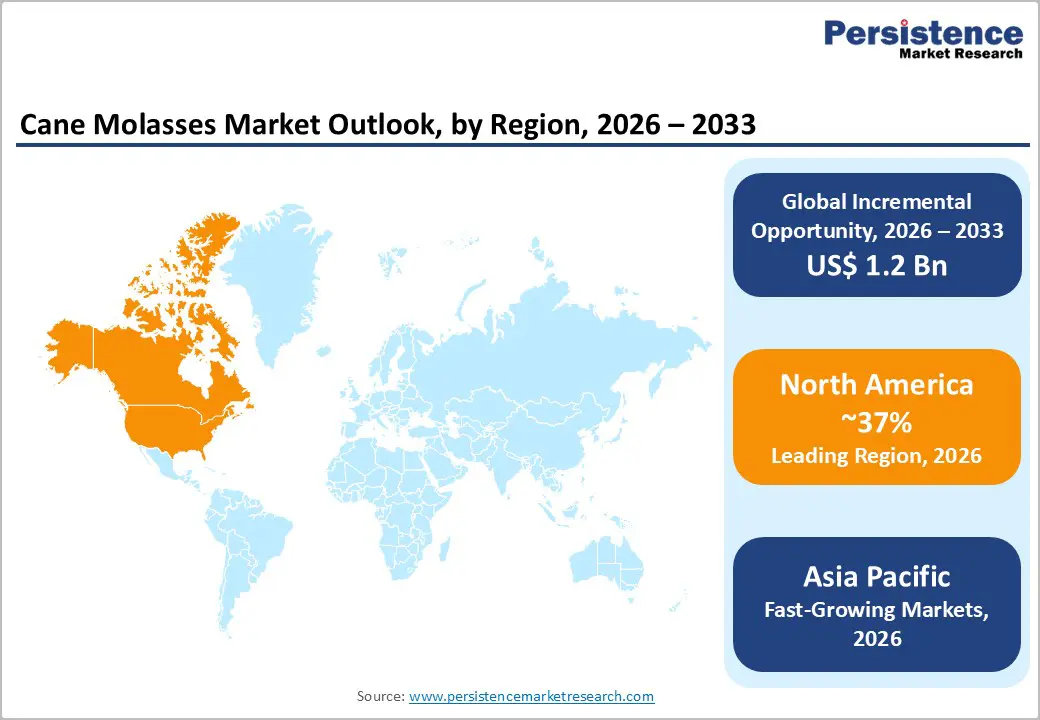

- North America is expected to remain the leading regional market, holding around 37% share in 2025, supported by a mature animal feed sector, strong food manufacturing industry, and stable molasses imports complemented by cane production in Florida and Louisiana.

- The Asia-Pacific region is the fastest-growing market through 2033, driven by India’s ethanol-blending expansion, rising livestock feed demand, and strong sugarcane industries in Thailand, Australia, and other ASEAN countries, collectively underpinning robust increases in molasses production and utilization.

- The food & beverages domain dominates with approximately 38% share, underpinned by molasses’ functional role as a natural sweetener, colorant, and flavoring agent in bakery, confectionery, sauce, and beverage formulations aligned with clean-label and natural ingredient trends.

- Ethanol / biofuel is the fastest-growing application segment, as national blending mandates, decarbonization targets, and investments in distillery capacity boost consumption of molasses as a key feedstock for fuel ethanol and other bioenergy products in sugarcane-producing regions.

- The rise of organic and certified sustainable molasses offers a key market opportunity, with organic and specialty certified grades growing at higher rates than conventional products and commanding premium pricing, supported by retailer commitments, consumer preferences, and stricter sustainability requirements in developed markets.

| Key Insights | Details |

|---|---|

|

Cane Molasses Market Size (2026E) |

US$ 3.3 Bn |

|

Market Value Forecast (2033F) |

US$ 4.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Dynamics

Drivers - Accelerating Biofuel Production and Renewable Energy Mandates

Rising investments in ethanol and biofuel capacity expansions have made cane molasses a strategically important feedstock, especially in sugarcane-producing economies. National blending schemes in large emerging markets are pushing higher ethanol-gasoline blends, which in turn are increasing the offtake of B-heavy and C-heavy molasses as feedstock for fuel ethanol. In India, official energy and agriculture statistics indicate a rapid rise in ethanol output and blending levels in recent years, with molasses-based routes forming a material share of total ethanol supply to oil marketing companies. Similarly, Brazil’s longstanding sugarcane ethanol program sustains sizeable structural demand for molasses in integrated sugar–ethanol complexes. In the European Union, renewable energy policies continue to recognize sugar industry by-products, including molasses, as eligible inputs for advanced and conventional biofuels under sustainability criteria. As more countries adopt net-zero roadmaps and raise their renewable fuel mandates, molasses’ position as a low-cost, biomass-derived feedstock underpins robust and durable demand growth from the biofuel segment.

Expanding Animal Feed Industry and Livestock Nutrition Enhancement

The global animal feed industry’s steady expansion is another critical driver of cane molasses demand, particularly in ruminant and compound feed formulations. Recent global feed outlooks indicate total compound feed production exceeding 1.3 billion metric tons, with year-on-year growth despite disease outbreaks and macroeconomic headwinds. Molasses is widely used as a liquid energy source, pellet binder, dust suppressant, and palatability enhancer in cattle, dairy, and other livestock diets. Nutrition research and feed industry practice highlight that the inclusion of molasses supports rumen function by providing readily fermentable carbohydrates while improving the intake of fibrous feeds. In large livestock-producing regions across North America, Europe, and Asia Pacific, feed manufacturers increasingly blend molasses into mineral blocks, lick tubs, and total mixed rations to optimize feed utilization and reduce wastage. As investments in commercial dairy, beef, and small ruminant operations grow, especially in Asia and Latin America, the role of molasses as a flexible, economical feed component is expected to strengthen further, thereby anchoring a sizeable base load of demand that is independent of sugar price cycles.

Restraints - Sugarcane Production Volatility and Feedstock Supply Constraints

The cane molasses market is inherently exposed to the cyclicality and climate sensitivity of sugarcane cultivation. Droughts, excess rainfall, pest pressure, and changing agronomic conditions in major producers such as Brazil, India, and Thailand have periodically reduced cane yields and sugar recovery rates, thereby compressing molasses output. In some years, governments have resorted to export taxes, quantitative restrictions, or prioritization of domestic use of molasses and sugar for regulated ethanol programs, which tightens availability for other downstream sectors. Trade and agricultural outlooks have also documented years of below-trend output in key producing countries, resulting in a tighter molasses supply and greater price volatility for importing regions. This combination of agronomic risk, policy-driven allocation changes, and freight constraints creates uncertainty for long-term planning among feed, fuel, and food processors that depend on molasses as a key input.

Competition from Alternative Sweeteners and Synthetic Feed Additives

Cane molasses faces increasing competition from a range of substitutes across its main end-use segments. In food and beverages, it competes with refined sugar, high-fructose corn syrup, glucose syrups, and newer natural sweeteners such as stevia and monk fruit extracts, which are often favored in sugar-reduction and low-calorie product reformulations. In animal nutrition, molasses can be partially replaced by cereal grains, glycerol, and formulated liquid supplements that provide more standardized nutrient compositions. Industrial and fermentation users may consider dextrose or other carbohydrate sources where consistent specifications and handling characteristics are prioritized. In some developed markets, health-driven reductions in sugar intake and reformulation targets in packaged foods could also modestly affect demand for molasses-based sweetening systems. Overall, this competitive pressure limits pricing power in certain applications and forces molasses suppliers to differentiate via sustainability credentials, quality assurance, and tailored technical support.

Opportunity - Organic and Non-GMO Certified Molasses Market Expansion

The shift toward organic, non-GMO, and clean-label ingredients in both food and feed presents a compelling opportunity for organic cane molasses. Organic sugarcane cultivation is expanding in select regions of Latin America, Asia, and Africa, enabling a growing pipeline of certified organic molasses suited for bakery, breakfast cereals, snack bars, and specialty beverages. Industry estimates indicate that the organic molasses segment already accounts for several hundred million dollars in annual sales and is growing faster than conventional categories, with reported growth profiles around high single-digit CAGR in premium markets such as North America and Western Europe.

Organic molasses is also increasingly used in organic livestock systems where standards require certified organic feed inputs, particularly in organic dairy and meat value chains sold through specialized retail channels. Brands leveraging certified organic molasses can command price premiums in the order of double-digit percentages compared with conventional grades. As traceability platforms, sustainability certifications, and consumer awareness continue to rise, producers capable of offering certified organic and non-GMO molasses with transparent supply chains are positioned to capture outsized value over the next decade.

Advanced Biofuel Technologies and Bio-Based Chemical Production

Cane molasses is emerging as a versatile feedstock for next-generation bio-based industries, extending beyond traditional fuel ethanol into higher-value biochemical and bioenergy applications. Biorefinery concepts in Europe and Asia are increasingly exploring molasses as a fermentation substrate for the production of organic acids, amino acids, yeast extracts, vitamins, and specialty chemicals, owing to its high fermentable sugar content and relatively low cost. Pilot and commercial plants in countries such as and Brazil have demonstrated the technical feasibility of producing biogas, bio-based polymers, and other advanced biofuels from molasses streams integrated into existing sugar complexes. Corporate announcements in recent years from major agribusiness and sugar groups indicate strategic investments, acquisitions, and joint ventures targeting molasses-processing assets, integrated feed plants, and fermentation-based product lines.

As policy frameworks in the EU and other regions further embed circular economy and resource-efficiency principles, valorizing molasses as a feedstock for high-value, low-carbon products offers an attractive route to margin expansion. For cane millers and integrated players, moving up the value chain into bio-based chemicals and advanced fuels represents a key structural opportunity that can partially decouple molasses economics from cyclical sugar markets.

Category-wise Analysis

Nature Insights

The conventional segment currently dominates the cane molasses market, with an estimated share of around 65% in 2025, owing to its deep integration with mainstream sugar processing and extensive use in bulk applications such as animal feed and fuel ethanol. Conventional molasses benefits from mature infrastructure, long-standing trade routes linking major producing regions to deficit markets, and the ability to serve large-volume industrial buyers that prioritize cost efficiency over certification attributes. Nonetheless, the organic molasses segment is expanding faster from a smaller base, with growth rates often in the mid- to high single digits annually in developed markets.

Organic processors in regions such as Europe and North America are increasingly specifying organic molasses in bakery mixes, cereal products, and natural sweetener blends in response to consumer preference for minimally processed ingredients. Organic molasses is also gaining traction in organic livestock programs in Europe and selected Asian markets. As certification schemes such as EU Organic, USDA Organic, and sustainability labels gain wider traction at the retail level, the relative share of organic molasses is projected to rise gradually, although conventional grades will continue to account for the majority of total volumes over the forecast period.

Application Insights

The food and beverages segment holds a leading position, accounting for approximately 38% of the cane molasses market in 2025, driven by its long-established use as a functional sweetener and flavoring agent. In bakery applications, molasses contributes to the characteristic color, flavor complexity, and moisture retention of bread, cookies, and cakes. It is integral to traditional products such as gingerbread, dark breads, and regional confectionery, and is also used in sauces, marinades, and syrups for both retail and foodservice channels. In beverages, molasses is a crucial substrate in rum production and contributes flavor notes in certain craft beverages and health-oriented drinks.

Food ingredient companies emphasize their role as a natural color and flavor system aligned with clean-label trends. At the same time, ethanol and biofuel production represent the fastest-growing application segment, supported by national blending mandates and decarbonization policies. In countries with strong sugarcane industries, refinery configurations increasingly allow flexible diversion of cane juice and molasses between sugar and ethanol, depending on relative economics and policy incentives. This structural flexibility means that as energy and climate policies favor renewable fuels, the share of molasses going into fuel and industrial alcohols is likely to rise faster than traditional uses, even as food and feed demand remains resilient.

Distribution Channel Insights

Direct and wholesale channels account for the largest share of cane molasses distribution, estimated at around 58% share in 2025, reflecting the predominance of large industrial buyers that require bulk, contract-based supply. Ethanol plants, integrated sugar-ethanol complexes, animal feed mills, and large food processors typically source molasses through direct contracts with mills, refineries, or global commodity traders. These channels are characterized by long-term offtake agreements, dedicated logistics (including tank storage and bulk liquid transport), and customized quality specifications for different end uses. Retail and supermarket channels play a secondary role, primarily serving small-pack molasses for household baking and cooking, with modest volumes relative to industrial uses.

The online channel is the fastest-growing distribution route, particularly for niche segments such as organic molasses, blackstrap molasses, and specialty grades targeted at home bakers, small food businesses, and craft beverage producers. E-commerce platforms and direct-to-consumer websites enable producers and brand owners to reach dispersed customer bases, provide detailed product information, and position molasses within broader natural and health-oriented product portfolios. This shift is most visible in developed markets where online grocery penetration is high, and consumers actively search for alternative sweeteners and functional ingredients.

Regional Insights

North America Cane Molasses Market Trends and Insights

North America leads the global cane molasses market with an estimated 37% share in 2025, anchored by a large and sophisticated animal feed sector, an established food processing industry, and a growing base of biofuel and distillery users. The United States is the principal market, with official trade statistics showing molasses imports valued at close to US$ 300 million in recent years, reflecting both structural dependence on imports and steady domestic demand. Domestic cane sugar production in states such as Florida and Louisiana contributes additional molasses supplies, with recent outlooks indicating record or near-record cane sugar output in some seasons. Feed formulators in the U.S. and Canada rely on molasses for dairy, beef, and mixed livestock rations, using it as an energy source and pellet binder in compound feeds.

Regulatory and quality frameworks support continued use of molasses in both food and feed. The U.S. Food and Drug Administration (FDA) recognizes molasses as Generally Recognized as Safe (GRAS) for specified uses, while feed regulations define quality parameters and labeling requirements for molasses-based feed products. The region also hosts a vibrant craft spirits industry, where molasses is a central raw material for rum and specialty spirits, and a growing organic and natural foods segment that drives demand for organic and non-GMO molasses. Innovation in feed-grade liquid supplements and molasses-enriched blocks, as well as wider availability through specialty retailers and online channels, further underpin the region’s leadership position.

Asia Pacific Cane Molasses Market Trends and Insights

Asia Pacific is the fastest-growing cane molasses market, supported by abundant sugarcane cultivation, expanding ethanol programs, and a large and diversifying livestock sector. India stands out as both a major producer and user of molasses, underpinned by extensive sugarcane acreage and policy-driven ethanol blending targets. Recent official outlooks show India’s ethanol production and blending ratios increasing markedly, with molasses-based ethanol contributing significantly alongside grain and juice routes. Policy decisions, such as export duties and prioritization of domestic feedstock for ethanol supply, underscore molasses’ strategic role in the country’s energy and agriculture nexus. India’s large dairy and ruminant livestock populations further underpin the use of feed-grade molasses in rural and commercial feed systems.

Competitive Landscape

The cane molasses market is moderately fragmented, featuring a mix of large integrated sugar producers, global commodity traders, and numerous regional mills supplying domestic demand. Competition is shaped by sugarcane availability, production scale, pricing volatility, logistics networks, and access to downstream ethanol, feed, and food-processing customers. Players focus on cost efficiency, long-term supply contracts, and diversification into biofuel and industrial fermentation markets to stabilize revenues. Sustainability initiatives, waste-to-value strategies, and traceability programs are gaining importance as buyers seek environmentally responsible sourcing. Regional dominance depends heavily on local sugar production volumes and government policies supporting ethanol blending and livestock nutrition.

Key Market Developments:

- In September 2025, Fermpro partnered with Universiti Malaysia Perlis (UniMAP) to conduct a three-year study starting in December 2025 to evaluate the use of spent sugarcane molasses as a soil ameliorant for high-value crops. The research aimed to assess the chemical properties and agronomic benefits of spent and treated molasses to improve soil quality, building on earlier rice field trials that had shown enhanced plant growth and yields.

Companies Covered in Cane Molasses Market

- Bunge Limited

- Cargill, Incorporated

- Louis Dreyfus Company

- Wilmar International Ltd

- ED&F Man Holdings

- Associated British Foods

- Tereos Group

- Südzucker AG

- Mitr Phol Group

- Guangxi Guitang Group

- Raízen Energia

- Shree Renuka Sugars Ltd

- Other

Frequently Asked Questions

The global cane molasses market is expected to be valued at US$ 3.3 billion in 2026, with projections indicating it could reach around US$ 4.5 billion by 2033, reflecting a forecast CAGR of 4.5% over 2026-2033.

Key demand drivers include the acceleration of biofuel and ethanol programs that rely on molasses as a core feedstock, and the expanding global animal feed industry where molasses provides cost-effective energy and enhances feed palatability, supported by rising compound feed production in major livestock-producing regions.

North America is currently the leading regional market, accounting for around 37% share in 2025, underpinned by strong animal feed demand, a large food processing base, stable molasses import flows, and domestic cane sugar and molasses production in states such as Florida and Louisiana.

High‑growth opportunities include the development of organic and certified sustainable molasses targeting premium food and feed segments, and the use of cane molasses in advanced biofuels and bio-based chemicals, where biorefinery projects and circular economy policies promote its valorization as a renewable, low‑carbon feedstock.

Leading market participants include global agribusiness and sugar groups such as Bunge Limited, Cargill, Incorporated, Louis Dreyfus Company, Wilmar International Ltd, ED&F Man Holdings, Associated British Foods, Tereos Group, Südzucker AG, Mitr Phol Group, Guangxi Guitang Group, Raízen Energia, and Shree Renuka Sugars Ltd, complemented by regional and specialty players in feed, food ingredients, and molasses trading.