- Medical Devices

- C-Reactive Protein Testing Market

C-Reactive Protein Testing Market Size, Share, and Growth Forecast, 2025 - 2032

C-Reactive Protein Testing Market By Test Type (High-Sensitivity CRP (hs-CRP), Standard CRP), Assay Technology (Immunoturbidimetry, Enzyme-Linked Immunosorbent Assay), Sample Type, Application, and Regional Analysis for 2025 - 2032

C-Reactive Protein Testing Market Size and Trends Analysis

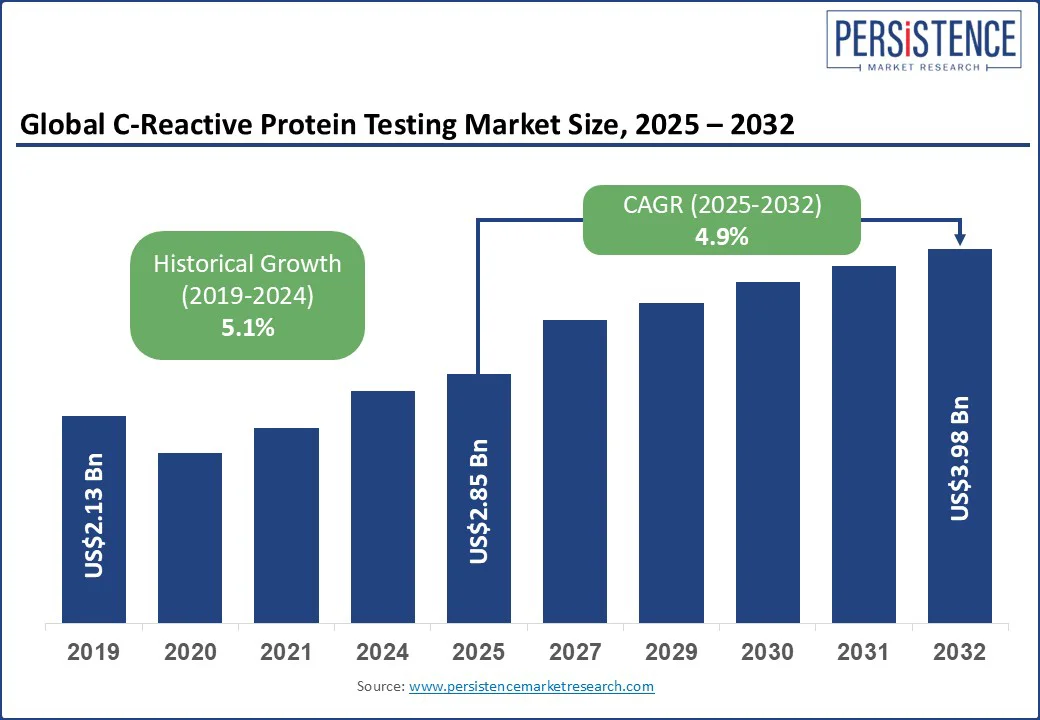

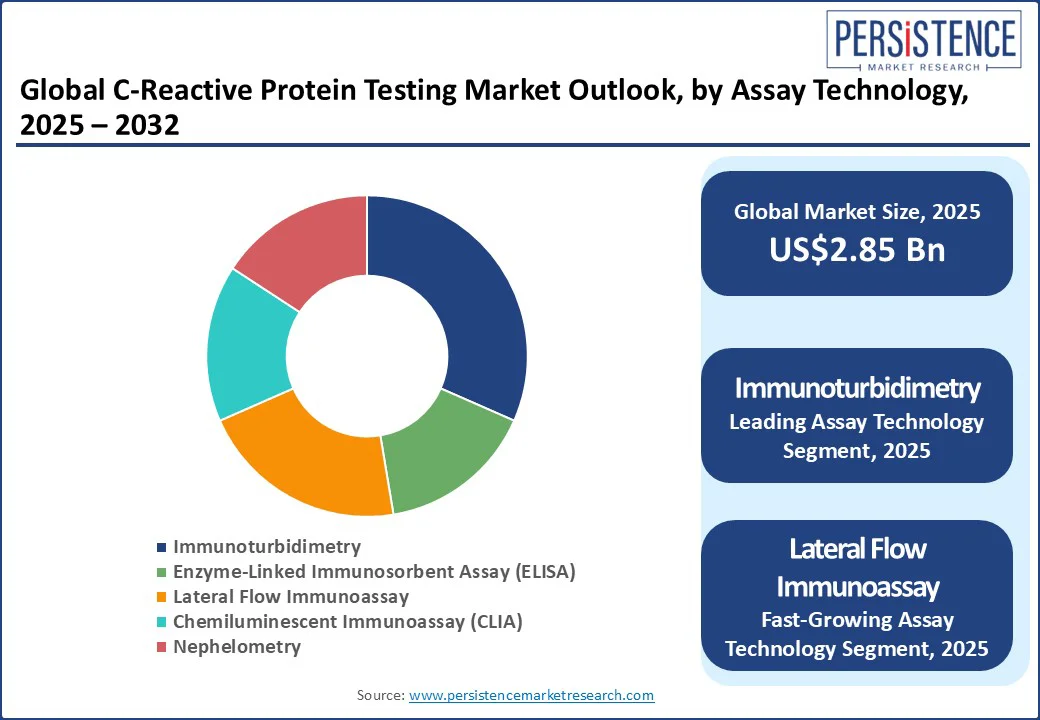

The global C-reactive protein testing market size is projected to rise from US$2.85 Bn in 2025 to US$3.98 Bn by 2032. It is anticipated to witness a CAGR of 4.9% during the forecast period from 2025 to 2032.

The C-Reactive Protein (CRP) testing market plays a critical role in diagnosing and monitoring inflammatory conditions, cardiovascular risks, and infections by measuring CRP levels in blood.

The growing prevalence of chronic diseases, rising demand for rapid and point-of-care (POC) diagnostics, and advancements in immunoassay technologies are driving market expansion. Increasing awareness about preventive healthcare, coupled with the integration of CRP testing in routine health check-ups, is further supporting growth, while ongoing innovations are enhancing the accuracy, speed, and accessibility of testing solutions worldwide.

Key Industry Highlights

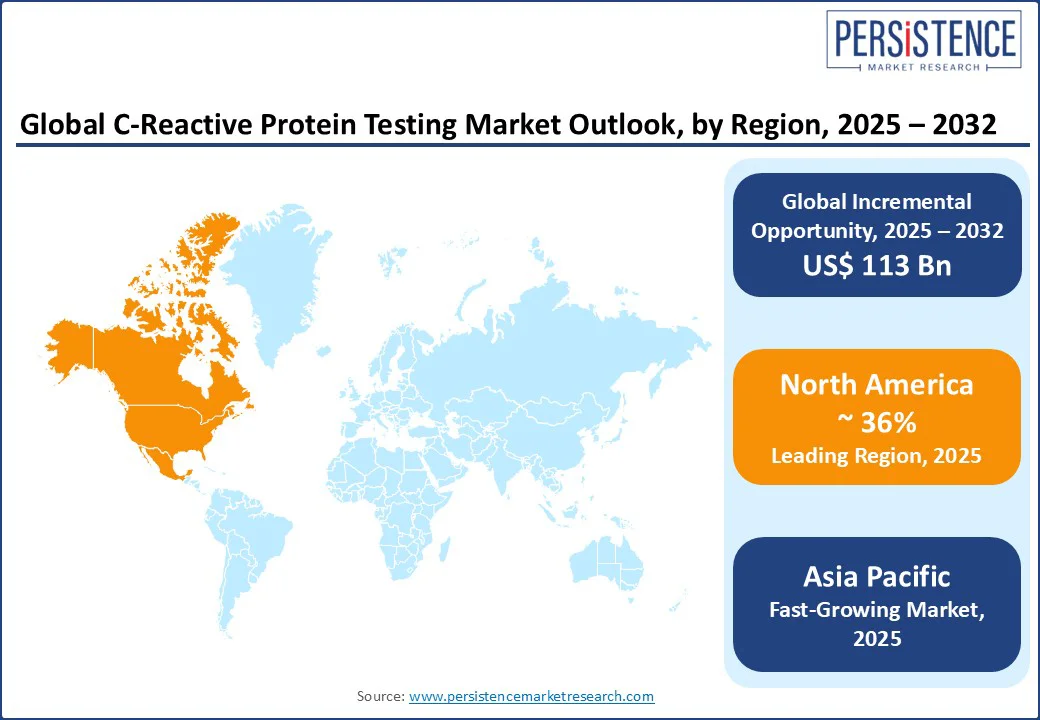

- Leading Region: North America is anticipated to hold over 36% of the market share in 2025, driven by the high prevalence of cardiovascular and inflammatory diseases, strong diagnostic infrastructure, and rapid adoption of high-sensitivity CRP testing in preventive care programs.

- Fastest-growing Region: Asia Pacific is projected to grow at a high CAGR over the forecast period, fueled by expanding healthcare access, government-backed infectious disease screening initiatives, and increasing point-of-care testing adoption.

- Dominant Test Type: The high-sensitivity CRP (hs-CRP) test is anticipated to account for 42.5% of the global market share in 2025, supported by its crucial role in early cardiovascular disease detection and risk stratification.

- Leading Assay Technology: The Immunoturbidimetry segment is expected to lead, holding around 30% of the market share in 2025, due to its cost-effectiveness, high throughput capability, and widespread adoption in both hospital laboratories and large diagnostic centers for routine CRP and hs-CRP testing.

|

Global Market Attribute |

Key Insights |

|

C-Reactive Protein Testing Market Size (2025E) |

US$2.85 Bn |

|

Market Value Forecast (2032F) |

US$3.98 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.1% |

Market Dynamics

Driver - Rising Adoption of Advanced CRP Testing for Targeted Diagnosis and Preventive Care

The adoption of point-of-care C-reactive protein tests for antibiotic stewardship in primary care is accelerating, as these tools reduce diagnostic uncertainty and help curb unnecessary antibiotic prescriptions. The integration of high-sensitivity CRP assays for cardiovascular risk stratification enables targeted risk reclassification and preventive interventions.

Rising incidence of chronic inflammatory disorders and cardiovascular diseases is driving the need for repeat CRP monitoring, while payer initiatives supporting precision-medicine workflows and updated clinical guidelines are fostering the broader use of quantitative and hs-CRP testing.

Manufacturers are introducing CRP rapid lateral flow immunoassay kits and compact microfluidic platforms that support fast, on-site diagnostics. The emergence of CRP duplex lateral flow tests for sepsis detection, combining CRP with procalcitonin (PCT), is improving triage speed in emergency departments and resource-limited settings.

Expanding at-home CRP testing and remote monitoring support the rising home healthcare trend, especially for managing chronic conditions. Lower-cost POC devices are reducing turnaround times and encouraging adoption in emerging markets, while regulatory approvals tied to antibiotic stewardship programs are further boosting the deployment of CRP point-of-care testing.

Restraint - Limited Specificity and Performance Variability in CRP Testing Across Settings

CRP shows limited clinical specificity for distinguishing bacterial from viral infections at low-to-moderate concentrations. Single, point-in-time CRP readings mislead clinicians when they ignore symptom onset and CRP kinetics (CRP velocity).

High-sensitivity assays reveal ethnic and socio-demographic variability in CRP reference ranges, which complicates universal cut-offs. Immunoassay interference from heterophile and anti-animal antibodies can produce false CRP values. These factors together reduce confidence in standalone CRP-guided antibiotic algorithms, prompting clinicians to rely on combined clinical assessment.

Analytical performance differs across POC CRP brands, leading to poor comparability of results across devices. Many lateral-flow and semi-quantitative CRP tests struggle to meet precision at the clinical decision thresholds used for stewardship.

Pre-analytical instability and transport issues limit the accuracy of self-collected and remote CRP testing. Most CRP POCT (point-of-care testing) programs lack seamless electronic health record (EHR) integration and decision-support, weakening real-time stewardship workflows. Variable quality assurance and lot-to-lot differences also contribute to inconsistent results, particularly in decentralized and emerging-market deployments.

Opportunity - Expanding CRP Integration in Telehealth, Point-of-Care, and Remote Monitoring Models

The integration of CRP testing into telehealth and remote-patient-monitoring workflows presents significant growth potential. At-home CRP self-collection kits can enhance chronic disease management and help optimize biologic therapy dosing. Using high-sensitivity CRP for cardiovascular risk reclassification enables targeted preventive interventions, such as personalized statin or anti-inflammatory therapy.

The deployment of CRP-procalcitonin duplex lateral-flow tests for sepsis triage in emergency departments can shorten antibiotic decision timelines, while embedding serial CRP measurements and CRP velocity analytics into EHR dashboards can help detect early relapse in conditions such as inflammatory bowel disease and autoimmune disorders.

Advancements in microfluidic CRP rapid quantitative point-of-care analyzers create opportunities for use in primary-care outreach and mobile health clinics. The rise of smartphone-enabled lateral-flow CRP quantification offers scalable solutions for community screening in low-resource settings. Integrating EHR-based CRP decision-support modules into antibiotic stewardship programs can improve the link between diagnostic results and treatment decisions.

The expansion of portable high-sensitivity CRP analyzers with field quality-assurance frameworks in emerging markets, alongside the introduction of CRP-as-a-service models via telehealth and remote monitoring, can significantly accelerate market penetration.

Category-wise analysis

Test Type Insights

The high-sensitivity CRP (hs-CRP) test segment is anticipated to account for approximately 42.5% of the global market share in 2025, making it the largest test type. Its dominance is driven by its established role in cardiovascular risk reclassification, where precise low-level CRP measurements guide preventive interventions and statin therapy decisions. The widespread adoption in central laboratories, compatibility with automated platforms, and inclusion in preventive care guidelines reinforce its leadership position.

The point-of-care (POC) CRP test segment is the fastest-growing. Growth is propelled by the rising need for rapid decision-making in antibiotic stewardship programs, increased use in urgent and primary care settings, and expanding availability of compact microfluidic analyzers and smartphone-enabled readers. The ability to deliver accurate, same-visit results without centralized infrastructure is accelerating uptake, particularly in emerging markets and home healthcare models.

Assay Technology Insights

Immunoturbidimetry is projected to hold the largest market share of approximately 30% in 2025, reflecting its status as the preferred method for high-throughput CRP testing in hospital and reference laboratories. Its leadership is underpinned by the existing installed base of automated clinical chemistry analyzers, robust precision across a broad dynamic range, and seamless integration with laboratory information systems, which ensure consistent and cost-efficient operations.

Lateral flow immunoassay (LFIA) represents the fastest-growing assay technology, with adoption rates rising sharply due to advancements in quantitative readouts, multiplex formats such as CRP-PCT for sepsis triage, and improved portability for low-resource settings.

These assays address the growing demand for rapid, on-site diagnostics, enabling decentralized testing in community health programs, mobile clinics, and point-of-care facilities, where immediate results directly impact treatment decisions.

Regional Insights

North America C-Reactive Protein Testing Market Trends - Strong Diagnostic Infrastructure and Rapid Technological Advancements

North America is expected to dominate with an estimated market share of 36% in 2025, underpinned by high per-capita diagnostic spending, early adoption of automated immunoassay platforms in centralized laboratories, and strong uptake of POC solutions in primary and urgent care networks.

A well-established policy and clinical guideline framework, including recognition of hs-CRP’s role in cardiovascular risk assessment by organizations such as the American College of Cardiology (ACC) and the American Heart Association (AHA), further strengthens market demand.

This combination of structural infrastructure, regulatory alignment, and evolving clinical needs ensures North America retains its leadership position, while POC expansion continues to complement centralized workflows.

In the U.S., the integration of hs-CRP into cardiology practice has been reinforced through ACC/AHA guidelines, driving consistent demand for high-precision assays on automated analyzers. Recent product updates, such as Roche’s Tina-quant series and Siemens’ hs-CRP assays, have improved assay sensitivity and throughput, enabling broader preventive care applications. Major IVD companies have expanded both CRP assay menus and POC offerings, for example Abbott’s Afinion CRP cartridge and Roche’s cobas-family solutions, supporting a dual strategy of centralized and decentralized testing.

Asia Pacific C-Reactive Protein Testing Market Trends - Expanding Healthcare Access and Rising Chronic Disease Burden

Asia Pacific presents a mix of mature laboratory-based CRP testing environments and fast-growing opportunities for decentralized POC testing. Developed markets such as Japan and Australia maintain stable demand for hs-CRP and immunoturbidimetric assays, while emerging economies, particularly China, India, and parts of Southeast Asia, are witnessing accelerated adoption of portable, low-cost CRP testing solutions.

Governments’ focus on strengthening primary care infrastructure and implementing antimicrobial resistance (AMR) control programs is generating sustained interest in rapid diagnostics. Rising domestic manufacturing capacity for lateral-flow and immunoassay kits also contributes to market expansion, although growth trajectories vary.

China’s large hospital laboratory market is constrained by pricing pressures, although followed with steady growth. Whereas India’s fragmented primary-care network creates fertile ground for scalable, cost-efficient POC technologies.

CRP testing demand remains anchored in immunoturbidimetric assays performed in centralized hospital laboratories, supported by ongoing investments in automated analyzers. While POC deployment in community clinics and secondary care is increasing, pricing sensitivity and entrenched lab infrastructure temper growth rates. Local reagent manufacturers compete alongside global suppliers, focusing on throughput optimization and affordability.

Europe C-Reactive Protein Testing Market Trends - Stringent Healthcare Guidelines and Adoption of High-Sensitivity Assays

Europe’s CRP testing market is heavily shaped by robust antibiotic stewardship policies, mature primary-care POCT pilots, and widespread automation in laboratory testing. Countries such as the U.K. and the Netherlands have pioneered the use of CRP POC testing in primary care as part of AMR reduction strategies, with strong guidance from clinical societies and external quality assurance (EQA) bodies.

While immunoturbidimetric and hs-CRP assays remain routine in hospital and reference laboratories, growing evidence from national programs supports the expansion of validated POCT devices in primary care to reduce inappropriate antibiotic prescribing. However, challenges persist in harmonizing assay performance across platforms and integrating POC results seamlessly into electronic health records.

In the U.K., NHS-backed pilot projects and practical guidance from the Primary Care Respiratory Society (PCRS) have driven the broader adoption of CRP POCT for respiratory tract infection management. Trials consistently demonstrate reduced antibiotic prescribing and cost-effectiveness when CRP POCT is applied to targeted patient groups.

Private suppliers such as Abbott (Afinion) and Roche (cobas B 101) are actively promoting devices to primary care and urgent care providers, with several regional rollouts underway.

Competitive Landscape

The global C-reactive protein testing market is highly competitive, dominated by a handful of global players who leverage strong R&D capabilities and broad product portfolios.

Key companies such as Roche Diagnostics, Abbott Laboratories, Siemens Healthineers, and Beckman Coulter lead the market with advanced automated immunoassay platforms, high-sensitivity CRP tests, and innovative point-of-care solutions. These players continuously invest in enhancing assay sensitivity, throughput, and integration with laboratory information systems to maintain their competitive edge and meet evolving clinical demands.

In addition to established multinationals, a growing number of regional and emerging-market manufacturers are expanding their presence by offering cost-effective lateral flow and rapid CRP testing kits. This influx intensifies competition in the point-of-care segment, particularly in the Asia Pacific and emerging economies.

Strategic collaborations, product launches, and expansion into telehealth-compatible CRP testing solutions further characterize the competitive landscape, as companies aim to capture a larger share of decentralized diagnostics markets while strengthening their foothold in centralized laboratory testing.

Key Industry Developments:

- In May 2024, Radiometer launched the AQT90 FLEX immunoassay analyzer with CRP testing, delivering results in under 13 minutes. Its closed-tube design minimized exposure and supported both whole blood and plasma, ideal for emergency and bedside use.

- In January 2024, Siemens HealthCare Diagnostics Inc. received FDA 510(k) clearance for its Atellica CH High Sensitivity CRP 2 (hCRP2) assay, enabling quantitative CRP testing in serum and plasma using the Atellica CH Analyzer.

Companies Covered in C-Reactive Protein Testing Market

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers AG

- Beckman Coulter, Inc. (Danaher Corporation)

- Thermo Fisher Scientific Inc.

- Randox Laboratories Ltd.

- Ortho Clinical Diagnostics

- Quest Diagnostics Incorporated

- Bio-Rad Laboratories, Inc.

- Horiba, Ltd.

- Sysmex Corporation

- Tosoh Corporation

- DiaSorin S.p.A.

- Merck KGaA

- Becton, Dickinson and Company (BD)

- Abaxis, Inc. (Zoetis)

- Biosystems S.A.

- Genrui Biotech Inc.

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Helena Laboratories Corporation

Frequently Asked Questions

The C-reactive protein testing market is estimated to be valued at US$ 2.85 Bn in 2025.

By 2032, the C-reactive protein testing market is expected to reach US$ 3.98 Bn, reflecting the rising adoption of CRP testing in preventive healthcare and chronic disease monitoring.

Key trends include increasing adoption of point-of-care CRP testing devices, integration of CRP testing in multi-analyte panels, growing demand for high-sensitivity CRP (hs-CRP) assays for cardiovascular risk prediction, and expanded use in pediatric infection diagnostics.

The high-sensitivity CRP testing segment dominates the market due to its critical role in early detection and management of cardiovascular diseases.

The C-reactive protein testing market is projected to grow at a CAGR of 4.9% from 2025 to 2032, supported by advancements in immunoassay technology and the increasing emphasis on preventive healthcare.

Prominent companies include Siemens Healthineers AG, Abbott Laboratories, F. Hoffmann-La Roche Ltd., Thermo Fisher Scientific Inc., and Danaher Corporation.