- Metals & Minerals

- Bonded Magnets Market

Bonded Magnets Market Size, Share, Trends, Forecasts 2025 - 2032

Bonded Magnets Market By Product (Rare Earth Bonded, Ferrite Bonded, SmFeN Hybrid), Form (Rigid, Flexible), Process (Injection Molding, Extrusion, Compression, Calendering), End-user (Consumer Electronics, Office Equipment, Others), Regional Analysis from 2025 to 2032

Bonded Magnets Market Share and Trends Analysis

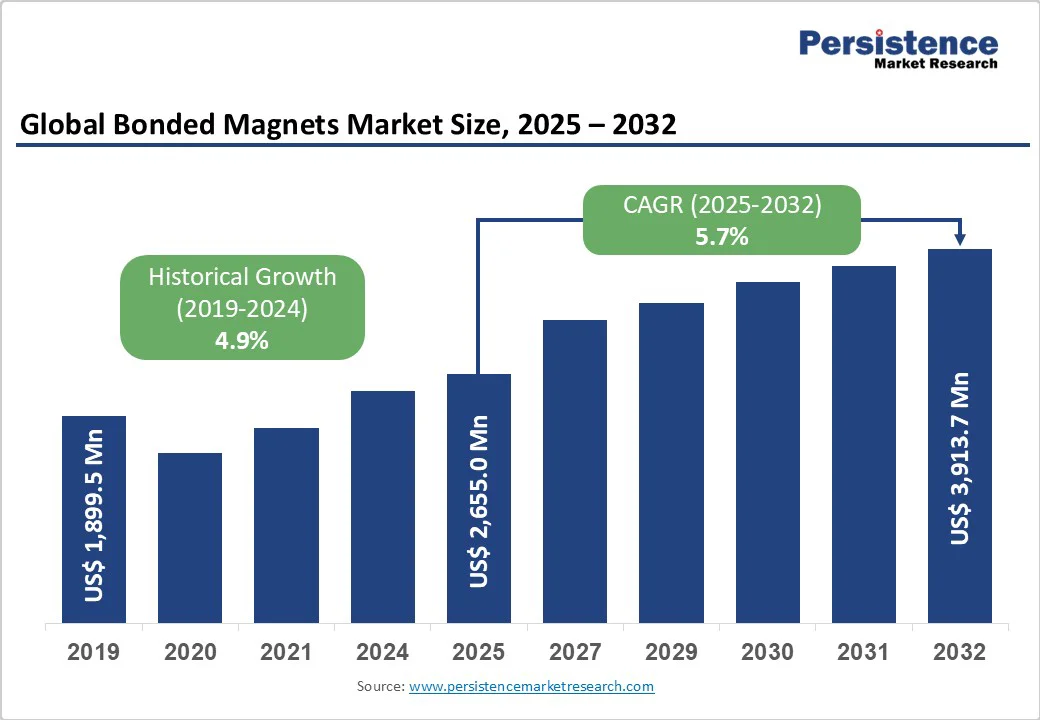

The global bonded magnets market size was valued at US$2,655.0 million in 2025 and is projected to reach US$3,913.7 million by 2032, growing at a CAGR of 5.7% between 2025 and 2032.

The rising demand for energy-efficient motors in the automotive sector, and miniaturization trends in consumer electronics, and ongoing innovations in rare earth magnet technologies are among the key factors driving market growth.

Key Industry Highlights:

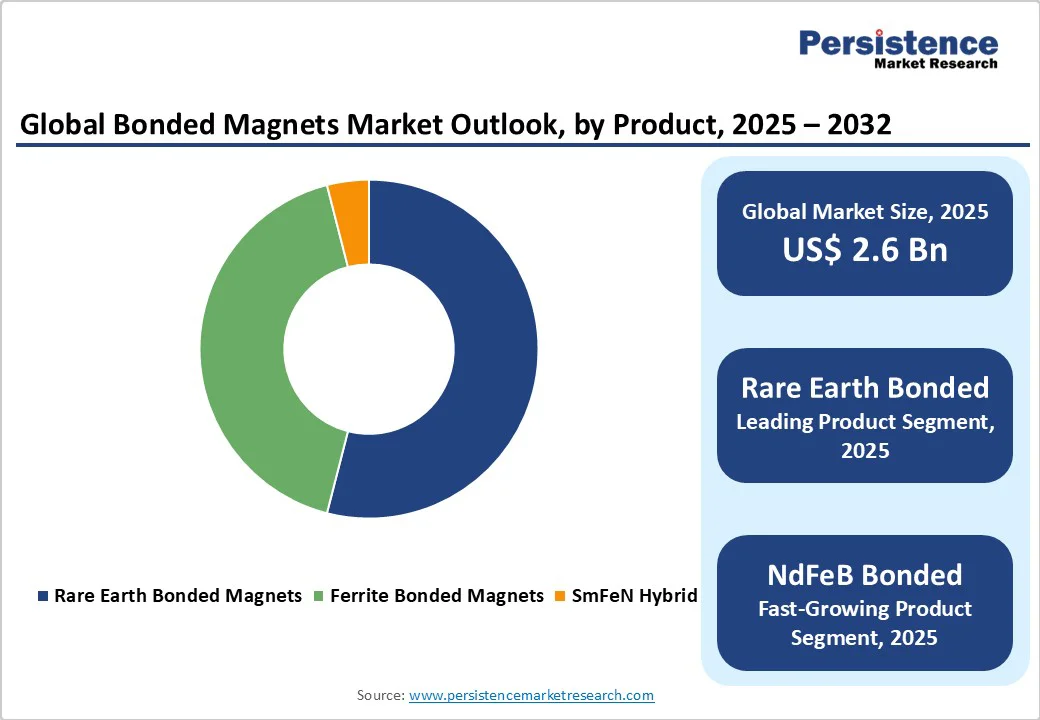

- Rare Earth bonded magnets dominate with over 50% share, with NdFeB bonded magnets representing the fast-growing product category due to superior performance in automotive traction motors and electronic applications.

- Compression molding holds over 30% of the process segment share, while additive manufacturing, enabled by 3D printing technologies, is the fastest-growing process, enabling customization and reduced lead times.

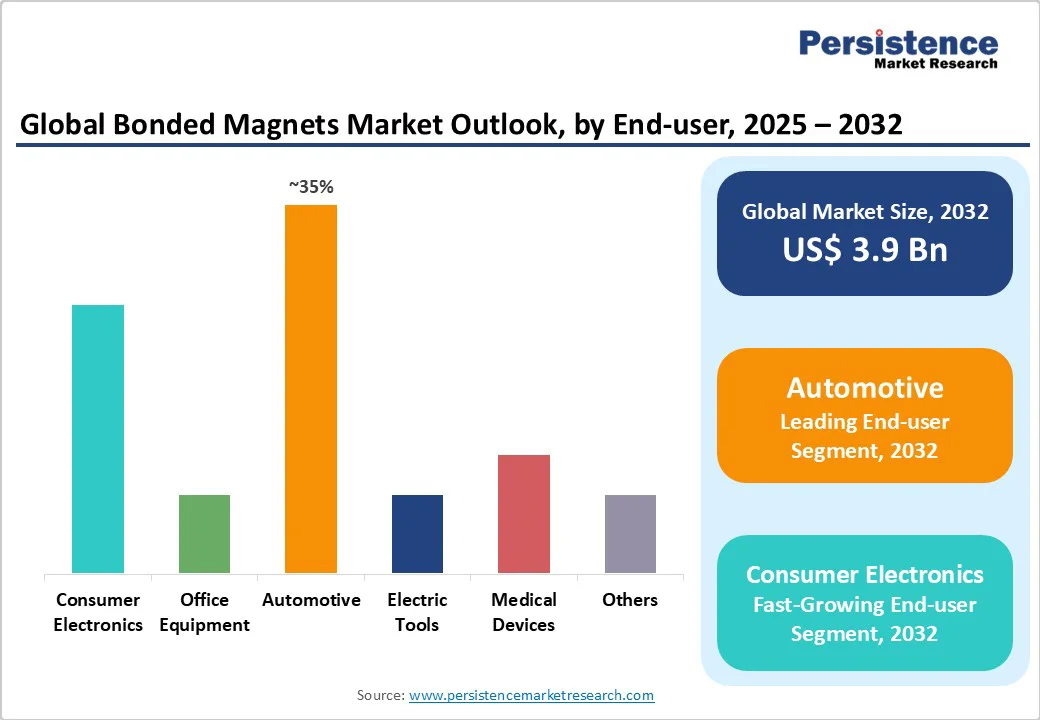

- Automotive end-use holds over 35% market share, with the electric vehicle sub-segment exhibiting exceptional growth at a positive CAGR through 2032.

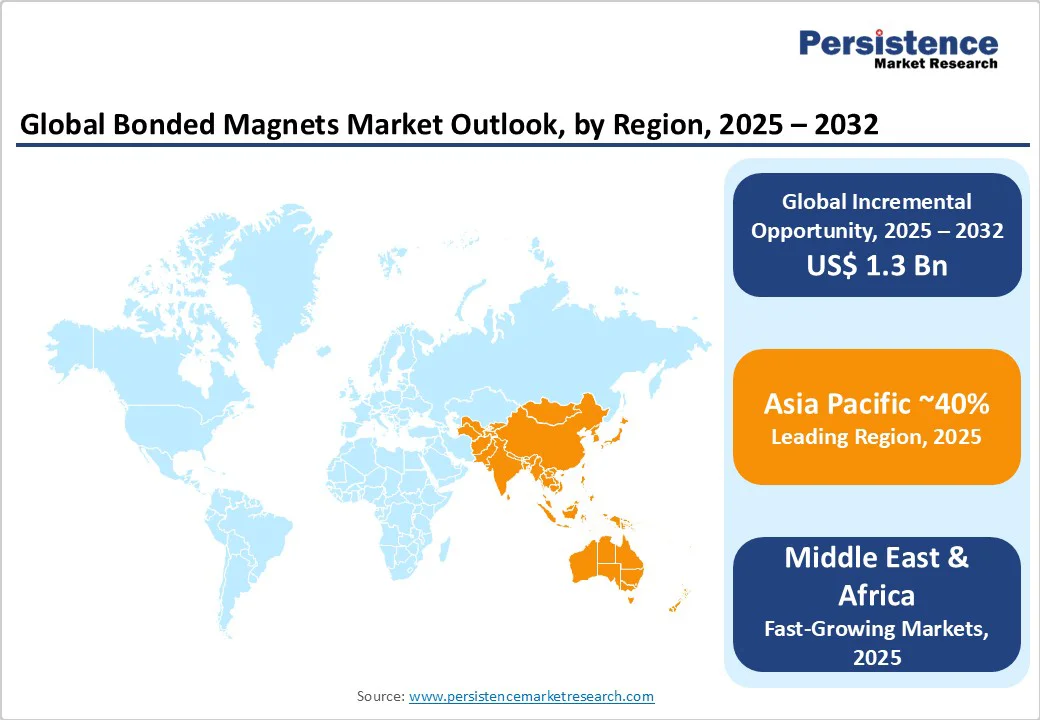

- Asia Pacific controls over 40% of global consumption, with China as the largest contributor and India demonstrating the fastest regional growth at 7.5% CAGR between 2025 and 2032.

- Rigid bonded magnets maintain leadership with more than 60% share in 2025, with conventional applications such as automotive components, industrial motors, and consumer electronics driving the growth.

- Consumer electronics represent the fastest-growing end-use segment, driven by smartphone production scaling, gaming console adoption, and smart home device proliferation in a trillion-dollar global consumer electronics market.

| Key Insights | Details |

|---|---|

| Global Bonded Magnets Market Size (2025) | US$2,655.0 million |

| Projected Market Value (2032F) | US$3,913.7 million |

| Global Market Growth Rate (CAGR 2025 to 2032) | 5.7% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 4.9% |

Market Dynamics

Driver - Booming Growth in Electric Vehicles and Automotive Electrification

The global electric vehicle market has emerged as the primary growth catalyst for bonded magnets, with EV sales forecasted to exceed 20 million units by 2025, representing a 35% year-over-year increase according to the International Energy Agency (IEA). Electric vehicle traction motors extensively use bonded NdFeB magnets due to their superior magnetic strength-to-weight ratio, enabling greater energy efficiency and longer driving range.

A surge in electric vehicle (EV) manufacturing and the increasing global penetration of smart electronics are major catalysts, as bonded magnets are essential for lightweight, miniaturized motors and actuators.

For instance, EV production is forecasted to grow at over 18% annually through 2030, supported by government targets and incentives across China, Europe, and North America (IEA, 2024). The demand for NdFeB bonded magnets in EV drivetrains and advanced infotainment systems directly translates to robust volume growth, with the automotive segment expected to command over 35% market share in 2025.

Consumer Electronics Expansion and Miniaturization Trends

The global consumer electronics market, valued at over US$950 billion in 2025 and projected to surpass US$1.25 trillion by 2035 at a CAGR of 3%, is a significant driver of bonded magnet demand. The proliferation of smartphones, personal computers, wearable devices, and smart home technologies requires compact magnetic components for motors, sensors, and actuators.

Modern devices, including smartphones, tablets, wearables, and smart home appliances, increasingly rely on bonded magnets for audio systems, haptic feedback, magnetic charging, and sensor applications. Industry miniaturization trends demand smaller yet more powerful magnetic components, creating opportunities for injection molding and compression bonding technologies that enable complex geometries and enhanced performance characteristics.

Advances in Magnetic Processing and Manufacturing Technologies

Technological progress in injection molding, additive manufacturing, and hybrid material processing has expanded the market’s application breadth. The integration of additive manufacturing is expected to expand bonded magnet production capacity, enabling complex, custom geometries and rapid prototyping while minimizing material waste.

3D printing of bonded permanent magnets is likely to reduce reliance on scarce rare-earth elements, lower energy and labor requirements, and enable endless design possibilities for magnet shapes. This enhances design flexibility for electronics, medical devices, and niche industrial applications, thereby fueling growth in high-margin end-user segments.

Restraint - Raw Material Price Volatility and Supply Chain Disruptions

The market is susceptible to fluctuations in the supply and pricing of rare earth elements (REEs), notably neodymium and samarium, which are concentrated in select countries, notably China (which accounts for more than 60% of global output, USGS, 2024). China imposed stringent rare-earth and magnet export controls in September 2025, restricting exports of products containing even trace amounts of Chinese content, which threatens defense and technology supply chains in the U.S. and Europe.

China's rare-earth magnet exports declined 6.1% in September 2025 from August 2025, ending three months of consecutive gains and raising supply security concerns among international manufacturers. Disruptions, trade restrictions, and mining regulations pose risks, driving up procurement costs for manufacturers and potentially compressing margins, especially for NdFeB and SmCo bonded magnets.

Cost Competitiveness and Manufacturing Complexity

Bonded magnet production requires sophisticated manufacturing processes, including injection molding, compression bonding, and emerging additive manufacturing techniques, each of which demands specialized equipment and technical expertise.

While bonded magnets offer design flexibility and complex geometries, their magnetic performance characteristics remain inferior to those of sintered magnets, limiting their use in high-performance applications. Volatile battery metal prices, high inflation, and the phase-out of purchase incentives in certain markets have put pressure on magnet manufacturers' margins.

The transition from early adopter markets to mass-market applications requires cost optimization while maintaining quality standards, particularly challenging in price-sensitive consumer electronics segments. Manufacturing localization initiatives in India, Europe, and North America face technology-transfer barriers and require substantial capital investment to establish competitive production capabilities.

Opportunity - Additive Manufacturing and Advanced Processing Technologies

Additive manufacturing offers a transformative opportunity for bonded magnet production, enabling near-net-shape fabrication without tooling and facilitating rapid prototyping. Research demonstrates that Big Area Additive Manufacturing (BAAM) can produce isotropic bonded magnets with efficient rare-earth material utilization, reducing waste and manufacturing costs.

Polymer-bonded magnet composites offer greater feasibility than sintered magnets due to their lower density, corrosion resistance, and suitability for additive manufacturing.

The additive manufacturing segment is rapidly growing, with the potential to capture a significant market share by 2032 through cost reductions, customization capabilities, and shortened production cycles. Integration of automated production technologies and advanced manufacturing processes addresses supply chain resilience while enabling local production capabilities in a strategic market.

SmFeN Bonded Magnets Offering Cost-Effectiveness and Supply Chain Advantages

SmFeN magnets offer substantial cost benefits compared to traditional NdFeB magnets, with raw material costs approximately 50% lower than those of bonded neodymium magnets. This pricing advantage stems from SmFeN's composition, which uses abundant samarium rather than the expensive rare-earth elements neodymium, dysprosium, and terbium. The U.S. Department of Energy has classified NdFeB magnets as critical materials that require supply diversification, creating opportunities for the adoption of SmFeN in domestic manufacturing.

High-temperature stability emerges as SmFeN's most significant performance advantage, with Curie temperatures reaching 476°C compared to 312°C for standard NdFeB magnets. Corrosion and oxidation resistance demonstrates s2-3 times better performance than comparable NdFeB materials, reducing or eliminating expensive protective coatings required for traditional rare earth magnets.

Category-wise Insights

Product Analysis

Leading Segment: Rare Earth Bonded Magnets

Rare Earth Bonded Magnets represent the dominating segment with over 50% market share in 2025. Within this category, NdFeB (neodymium-iron-boron) bonded magnets constitute the most popular product and fastest-growing segment, driven by superior magnetic properties and expanding electric mobility applications.

Superior magnetic properties and high adoption in advanced electric motors, sensors, and consumer electronics are among the chief drivers propelling the demand for NdFeB bonded magnets. Product innovation around temperature stability and demagnetization resistance strengthens their competitive positioning, particularly in developing high-performance EV powertrains and data storage devices.

Bonded NdFeB magnets deliver high performance and design flexibility, making them ideal magnets for sensors, actuators, brushless motors, automotive instrumentation, and electronic gas pedals.

Fastest-Growing Segment: NdFeB Bonded Magnets

NdFeB bonded magnets represent both the most popular and fastest-growing sub-segment, as demand for miniaturized and energy-efficient solutions surges in e-mobility, household appliances, and wearables. The segment is projected to outpace market averages, reflecting robust consumption growth and sustained R&D investment in custom and hybrid formulations.

Previously, automotive micromotors served limited applications, primarily powering essential components such as wipers, windshield washers, electric oil pumps, and automatic antennas. However, contemporary vehicle architecture demands significantly broader micromotor integration.

Modern passenger vehicles now require micromotors across a range of systems, including skylight mechanisms, seat belt pretensioners, seat adjustment assemblies, interior lighting, climate control units, electric antennas, starter motors, cooling fans, fog lamps with steering linkage, audio speakers, and various sensor applications.

The intensity of micromotor deployment varies considerably across vehicle segments, correlating directly with feature sophistication and price positioning. Luxury vehicles typically incorporate over 90 micromotors per unit, while mid-tier vehicles require 40-50, and economy segment vehicles utilize a minimum of 20. As automobiles evolve towards greater comfort, energy efficiency, and automation, the demand for bonded NdFeB magnets in automobile motors is expected to increase.

Ferrite Bonded Magnets dominate the segment in terms of volume consumption due to their cost-effectiveness and widespread availability, though rare-earth magnets lead in value terms. Ferrite magnets serve cost-sensitive applications, including household appliances, office automation equipment, small motors, magnetic couplings, and fuel filters.

Form Analysis

Leading Segment: Rigid Bonded Magnets

Rigid bonded magnets maintain market leadership with more than 60% market share in 2025, serving traditional applications in automotive components, industrial motors, and consumer electronics. Rigid forms enable higher magnetic loading and superior mechanical strength, making them suitable for structural applications in electric motors, sensors, and actuators requiring dimensional stability.

Injection molding and compression bonding processes primarily produce rigid bonded magnets with complex three-dimensional geometries that support automotive and industrial equipment requirements.

Fastest-Growing Segment: Flexible Bonded Magnets

Flexible bonded magnets represent the fastest-growing form segment with projected CAGR exceeding 7% through 2032, driven by emerging applications in wearable devices, conformable sensors, wireless charging systems, and flexible electronics. Flexible formulations utilize thermoplastic binders, including thermoplastic polyurethane (TPU) and nylon (PA12) blends that enable bending and conformability while maintaining magnetic properties.

Applications include refrigerator door seals, magnetic strips, flexible signage, and emerging uses in Internet of Things devices requiring conformable magnetic field sources. The growth is anticipated to exceed overall market averages, supported by ongoing adoption in complex, miniaturized device assemblies and easy customization.

Process Analysis

Dominating Segment: Compression Molding

Compression molding is the dominant process segment, accounting for over 30% of the market in 2025, favored for producing high-performance bonded magnets with maximum magnetic loading.

Compression bonding encapsulates neodymium-iron-boron powder with minimal resin content and compresses it under high pressure (approximately 6 tonnes/cm²), achieving superior magnetic properties compared to other processes. This technique serves automotive, aerospace, and industrial applications requiring optimized magnetic performance characteristics.

Injection molding enables high-volume production through multi-cavity tooling, supporting consumer electronics, office equipment, and automotive component manufacturers requiring cost-effective mass production. Injection molding processes molten, highly filled thermoplastic compounds into complex geometries, facilitating multicomponent assemblies through insert and over-molding techniques. Ferrite and neodymium-iron-boron powders serve as the primary magnetic materials in injection-molded bonded magnets.

Regional Market Insights

North America Bonded Magnets Market Trends

The North American bonded magnets market is mature, underpinned by significant adoption across the electronics, automotive, and medical device sectors. The U.S. comprises over 90% of the regional market share, with the U.S. bonded magnets market size to reach US$1,141.8 million by 2032.

Innovation-centric business culture, rapid electrification of vehicle fleets, and robust R&D investments drive growth. U.S. policies supporting domestic manufacturing of critical technologies and rare-earth independence shape competitive positioning, while regulatory alignment with energy-efficiency standards (DOE, EPA) propels market expansion.

Canada contributes to regional market growth through automotive component manufacturing and natural resource processing capabilities. Investment trends prioritize strategic partnerships with Japanese and European technology providers, government-supported expansion of manufacturing capacity, and the development of non-Chinese rare-earth supply chains.

Europe Bonded Magnets Market Trends

Europe presents a mature, highly regulated bonded magnets market, valued at US$605.7 million in 2025. Germany, France, and the U.K. drive demand, particularly in automotive, robotics, and industrial machinery sectors, with long-standing magnet-intensive manufacturing traditions. The German market is a bellwether for advanced magnet adoption in the region, with continuous investment in Industry 4.0 and automotive electrification.

The European regulatory framework, harmonized under the REACH and EcoDesign directives, creates a level playing field and encourages investments in sustainable materials and processes. Companies in the region are investing in recycling facilities to develop a stable supply of rare earth materials.

Strategic focus on localizing magnetic material sourcing and recycling supports resilience, while leading players invest in both vertical integration and collaborative R&D platforms. The competitive field is moderately fragmented, with differentiation favoring high-performance, compliance-ready products.

In 2024, Heraeus Remloy launched a recycling facility in Germany with the capability to produce nanocrystalline rare-earth magnetic materials from recycled End-of-Life electronic devices. The recovered materials can be sourced as a key raw material for bonded NdFeB magnets.

Asia Pacific Bonded Magnets Market Trends

Asia Pacific commands over 40% of global bonded magnet consumption in 2025, with China as the largest user and producer. China accounts for over 55% of the regional market share, holding a dominant position owing to its robust automotive and electronics sectors. Aggressive government funding for e-mobility, consumer electronics, and industrial automation underpins demand in the region.

India’s market is projected to grow at a 7.5% CAGR between 2025 and 2032, driven by robust electronics and automotive manufacturing growth, as well as increasing EV penetration. According to the Automotive Component Manufacturers Association (ACMA), India’s automotive components sector is valued at over US$80 billion in 2025 and is projected to surpass US$100 billion by 2030. Bonded magnets are widely deployed in cars’ digital speedometers, instrument clusters, and sensors.

Competitive Landscape

The bonded magnets market is characterized by moderate consolidation at the top, with the top five players accounting for approximately 40% of global revenues.

Regional players and diversified conglomerates compete with specialist suppliers, leveraging scale, R&D, and supply chain integration as key differentiators. The landscape rewards innovation-focused business models and cost optimization, with barriers defined by intellectual property, supplier relationships, and compliance with end-user standards.

Companies Covered in Bonded Magnets Market

- Daido Electronics Co. Ltd.

- Nichia Corporation

- Toda Kogyo Corp.

- Neo Performance Materials (Magnequench)

- Arnold Magnetic Technologies

- Alliance Magnetics

- Magnet Applications Inc.

- Zhejiang Innuovo Magnetics Co., Ltd.

- MGM Magnetics

- Ashvini Magnets

- AIM Magnet

- ABM Magnetics Co. Ltd.

- Ningbo Tongchuang Magnetic Materials Co., Ltd.

- Ningbo Yunsheng Co., Ltd.

- Dexter Magnetic Technologies

- Newland Magnetics

- Proterial Ltd

Frequently Asked Questions

The global bonded magnets market was valued at US$2,655.0 million in 2025 and is projected to reach US$3,913.7 million by 2032, growing at a CAGR of 5.7% from 2025 to 2032.

Rare earth bonded magnets are expected to dominate the market with an over 50% market share in 2025, with NdFeB (neodymium-iron-boron) bonded magnets representing the fast-growing product category due to their superior magnetic properties and extensive use in EV traction motors, sensors, and consumer electronics.

Automotive leads with over 35% market share (US$900+ million in 2025), driven by EVs, while consumer electronics represents the fast-growing segment, fueled by smartphones, PCs, wearables, and smart home devices in a trillion-dollar global market.

Asia Pacific controls over 40% of global consumption, with China as the largest contributor. Meanwhile, India demonstrates the fastest regional growth.

Additive manufacturing (3D printing) emerges as the fastest-growing process enabling customization and reduced waste, while SmFeN bonded magnets offer raw material costs approximately 50% lower than NdFeB magnets with superior high-temperature stability and corrosion resistance.