- Construction & Engineering

- Temporary Storage Buildings/Sheds Market

Temporary Storage Buildings/Sheds Market Size, Share, and Growth Forecast 2025 - 2032

Temporary Storage Buildings/Sheds Market by Building Material (Timber, Steel), Application (Storage Space, Workspace, Open Categories, Education, Sports Facilities, Others) Regional Analysis 2025 - 2032

Temporary Storage Buildings/Sheds Market Share and Trends Analysis

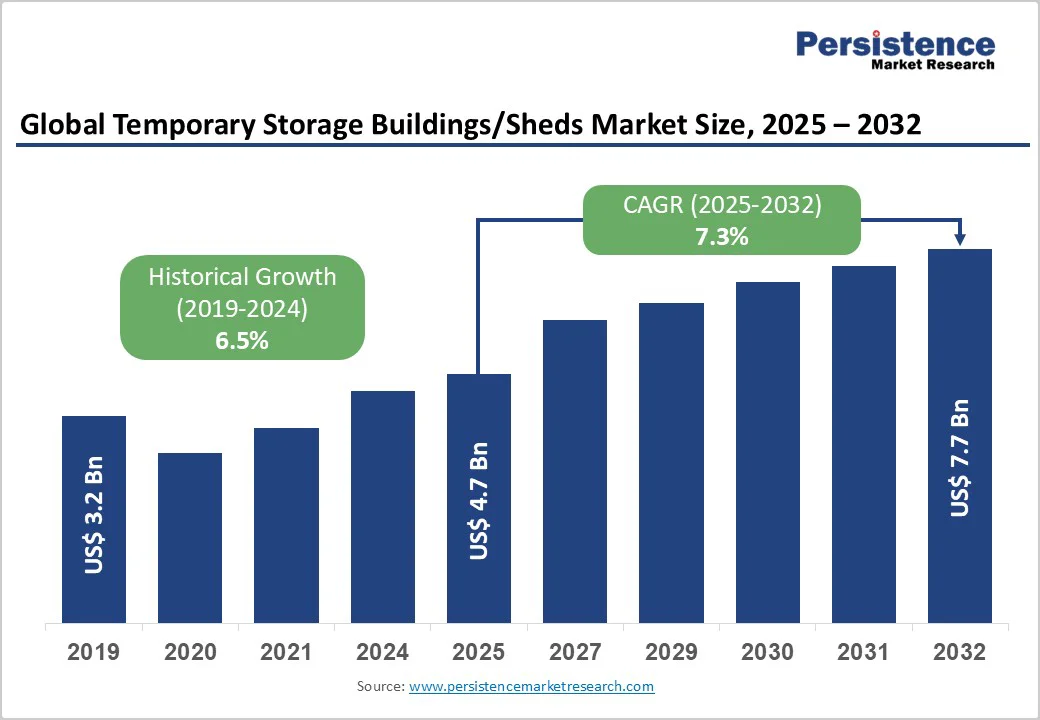

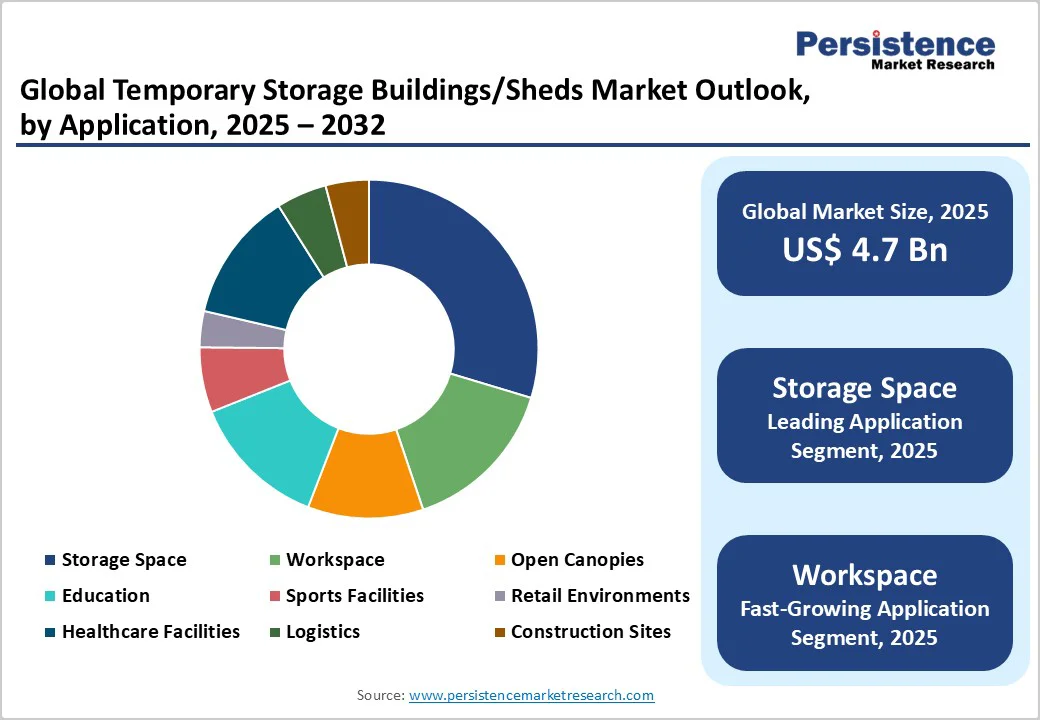

The global temporary storage buildings/sheds market size is likely to be valued at US$4.7 billion in 2025 and is projected to reach US$7.7 billion by 2032, growing at a CAGR of 7.3% between 2025 and 2032.

The expansion is driven by a surge in e-commerce activities requiring flexible warehousing solutions, rapid industrialization across emerging economies necessitating quick-deployment storage infrastructure, and increasing adoption of modular construction methodologies that reduce project timelines by 30-50% compared to traditional building approaches. Rising infrastructure development expenditure and growing preference for cost-effective, relocatable structures further accelerate market momentum.

Key Market Highlights:

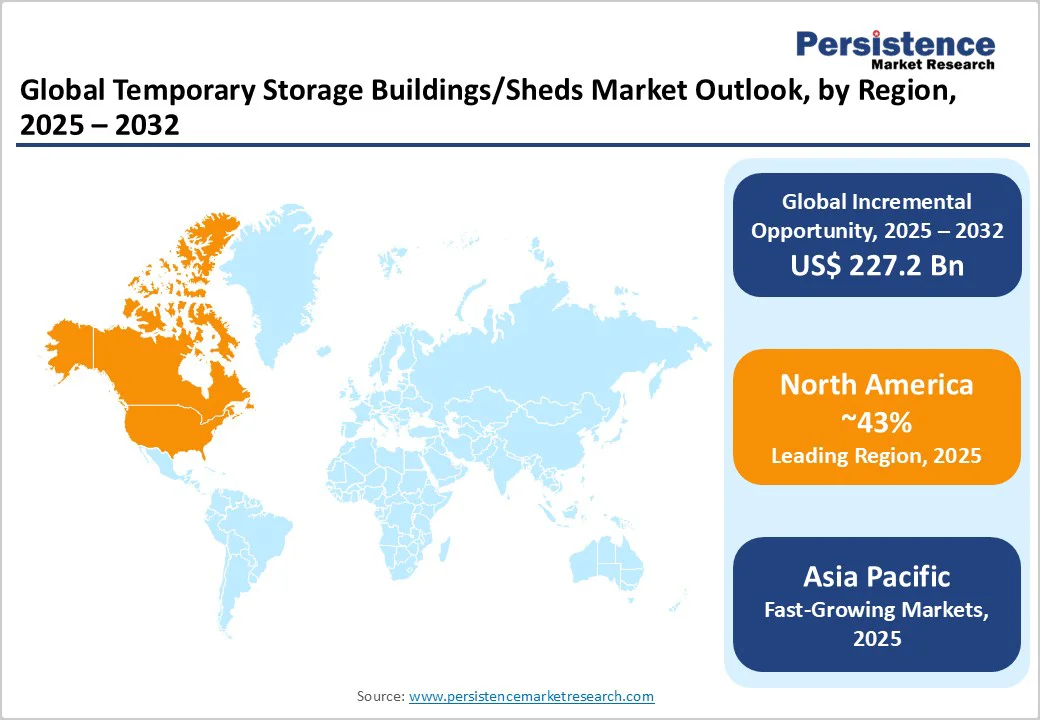

- Leading Region: North America leads the global temporary storage buildings market, supported by US$600 million in federal housing investments and a mature e-commerce infrastructure that requires flexible warehousing solutions across industrial corridors.

- Fastest-Growing Region: Asia Pacific leads with an 8% CAGR in warehousing growth, driven by China's industrial expansion and India's emergence as the preferred expansion destination for international occupiers.

- Leding Application Segment: Storage Space applications dominate with 43% market share, reflecting diverse end-user adoption across e-commerce, manufacturing, agriculture, and retail sectors requiring flexible capacity management solutions.

- Leading Build Material Segment: Steel building materials represent the fastest-growing segment due to superior structural integrity, weather resistance, and suitability for large-span industrial applications with minimal maintenance requirements.

- Key Market Opportunity: Smart technology integration presents the key market opportunity, with IoT sensors, BIM, and digital monitoring systems creating value-added services for logistics and industrial clients.

| Key Insights | Details |

|---|---|

|

Temporary Storage Buildings/Sheds Size (2025E) |

US$ 4.7 Billion |

|

Market Value Forecast (2032F) |

US$ 7.7 Billion |

|

Projected Growth CAGR (2025-2032) |

7.3% |

|

Historical Market Growth (2019-2024) |

6.5% |

Market Dynamics

Drivers - Exponential E-commerce Growth and Warehousing Demand Surge

The rapid expansion of the global e-commerce sector is driving strong demand for temporary storage buildings and sheds. Retailers and logistics providers increasingly require flexible, quick-to-deploy storage solutions to manage fluctuating inventory during peak seasons and promotional events. In the Asia Pacific, the warehousing market reached US$300 billion in 2024 and is projected to grow at an 8% CAGR through 2032, directly boosting temporary storage demand.

Just-in-time inventory strategies and supply chain diversification following global disruptions have intensified the need for scalable storage solutions. Third-party logistics (3PL) providers are significant adopters, with around 70% of APAC occupiers planning warehouse expansions in the coming years. Temporary storage facilities offer a cost-effective and rapid means to accommodate seasonal surges and dynamic inventory requirements, reinforcing their role in modern logistics networks.

Rapid Industrialization and Infrastructure Development in Emerging Markets

Emerging economies in the Asia Pacific, Latin America, and Africa are witnessing accelerated industrialization, creating high demand for flexible storage infrastructure. India alone plans to add 30 million square feet of warehouse space, contributing to a broader APAC expansion of 86 million square feet. Government initiatives, such as modular housing funding in Canada, illustrate public-sector support that indirectly drives the adoption of temporary buildings.

Temporary storage solutions are increasingly used in manufacturing and construction sectors to house raw materials, finished goods, and equipment. With global infrastructure investments projected to reach US$4 trillion annually, these buildings serve as critical interim solutions during large-scale projects. The growing need for adaptable, rapid-deployment storage reflects broader industrial and urban development trends in emerging markets.

Restraint - Transportation and Logistics Constraints for Volumetric Modules

The temporary storage building market faces notable restraints due to transportation and logistics challenges, especially for large volumetric modules. Oversized shipments often require special permits, escort vehicles, and specialized equipment, driving transport costs and fees to exceed 15% of total project expenses when modules are shipped over 500 miles.

Varying road traffic regulations, including height, width, and length limitations across jurisdictions, create design constraints that can limit optimal building configurations. These factors increase deployment timelines and reduce the speed advantages of prefabricated solutions. As a result, logistical complexities can limit market penetration in remote areas and negatively affect the overall cost-effectiveness of temporary storage solutions.

Regulatory Complexity and Building Code Variations

Temporary storage buildings face challenges from diverse building codes, zoning laws, and permitting requirements across regions. Although many structures are designed to comply with standards like EN 1090, EN 13782, and Structural Eurocodes, local adaptations often require design modifications and prolonged approval processes.

Differences in temporary building classifications affect allowed usage durations, foundation types, and compliance costs. Certain jurisdictions may restrict installation in specific zones, mandate permanent foundations, or require fire safety and environmental assessments. These regulatory variations increase project timelines and expenses, reducing the cost and time advantages of temporary storage buildings and posing a significant barrier to widespread adoption.

Opportunities - Integration of Smart Technologies and Digital Construction Methods

The temporary storage building sector is increasingly leveraging smart technologies and digital construction methods to enhance efficiency, security, and value. IoT sensors, Building Information Modeling (BIM), and smart monitoring systems enable real-time tracking of environmental conditions, access control, and inventory management, providing significant benefits for logistics, retail, and industrial clients. Digital Product Passports, introduced under the EU Construction Products Regulation 2024, enhance transparency and traceability of modular components, supporting circular economy initiatives.

Advances in automation and 3D printing are transforming modular production, enabling consistent quality, reduced labor requirements, and faster manufacturing cycles. By integrating these technologies, temporary storage buildings evolve from simple shelters into sophisticated, data-driven solutions. Real-time monitoring, predictive maintenance, and digital asset management further increase operational value, creating new revenue streams and positioning these structures as smart, adaptable assets within modern supply chains and construction ecosystems.

Sustainable Construction and Circular Economy Applications

Growing sustainability awareness is driving demand for eco-friendly temporary storage buildings that align with circular economy principles. Modular construction reduces material waste by 10–15% during production, while prefabricated units can be disassembled, reconfigured, and repurposed at end of life, extending asset utility. Factory-built solutions are particularly advantageous under carbon-neutral and net-zero energy codes, as controlled production environments enable precise compliance with efficiency requirements.

Temporary buildings increasingly incorporate bio-based materials, renewable energy integration, and recyclable components, enabling them to serve as showcase projects for sustainable construction practices. Government incentives, green building regulations, and corporate sustainability commitments further support adoption across logistics, retail, industrial, and construction sectors. These trends position temporary storage buildings as environmentally responsible, flexible infrastructure solutions that meet evolving regulatory and corporate ESG requirements.

Category-wise Insights

Building Material Analysis

Steel dominates the temporary storage buildings market with approximately 74% market share in 2025, primarily due to its superior structural integrity, weather resistance, and suitability for large-span applications. Steel-framed structures offer exceptional strength-to-weight ratios enabling clear-span widths up to 200 feet for warehouse applications while maintaining rapid assembly capabilities. The material's fire resistance, pest immunity, and minimal maintenance requirements make it particularly attractive for industrial and commercial storage applications.

Galvanized steel components resist corrosion effectively, ensuring extended service life even in challenging environmental conditions. However, Timber construction is gaining momentum as a sustainable alternative, particularly for smaller-scale storage applications and regions emphasizing environmental responsibility. Engineered wood products such as cross-laminated timber (CLT) and glue-laminated beams provide adequate structural performance while offering superior insulation properties and lower carbon footprint compared to steel alternatives.

Application Analysis

Storage Space applications command the largest market segment with approximately 43% share, driven by e-commerce expansion, retail inventory management needs, and industrial equipment storage requirements. The segment benefits from diverse end-user adoption across logistics, manufacturing, agriculture, and retail sectors, requiring flexible capacity management solutions.

Workspace applications represent the second-largest segment witha 22% share, encompassing site offices, temporary facilities during renovations, and remote work installations. The COVID-19 pandemic accelerated the adoption of modular workspace solutions as organizations required rapid capacity adjustments and safe working environments.

Healthcare Facilities emerged as a rapidly growing application during the pandemic, with temporary hospitals, testing centers, and vaccination sites demonstrating the critical role of deployable medical infrastructure. Education applications, including portable classrooms and temporary school buildings, address enrollment fluctuations and facility renovations, while Sports Facilities and Retail Environments serve seasonal and event-based requirements.

Regional Insights

North America Temporary Storage Buildings/Sheds Trends

North America maintains market leadership with the United States controlling 72% of regional market share, supported by US$ 600 million in HUD research investments and federal housing policy initiatives targeting tribal and rural development. The region's mature e-commerce infrastructure drives consistent demand for temporary warehousing solutions, with logistics corridors experiencing sustained growth in modular storage deployment. Regulatory frameworks favor modular construction through updated energy codes like IECC-2024 and ASHRAE-90.1-2022 that establish efficiency thresholds more easily met by factory-built structures.

The North American modular construction market is projected to reached US$ 30 billion by 2032, representing 5.1% of total construction activity across key segments. Skilled labor shortages contribute +1.8% impact on market CAGR, while net-zero energy codes add +1.0% growth momentum. Mexico emerges as the fastest-growing market within the region at 7.6% CAGR, driven by nearshoring trends boosting demand for industrial modules and worker housing, creating additional opportunities for temporary storage solutions.

Europe Temporary Storage Buildings/Sheds Trends

Europe demonstrates strong regulatory support for modular construction through the new EU Construction Products Regulation (2024/3110) that harmonizes standards across member states and introduces Digital Product Passports for construction components. The regulation explicitly supports offsite construction methods, recognizing their potential to reduce costs, improve project timelines, and enhance sustainability performance. Germany, United Kingdom, France, and Spain lead regional adoption with established modular construction industries and supportive policy frameworks.

Regulatory harmonization across EU member states simplifies trade and market access for modular manufacturers while reducing administrative costs and streamlining compliance processes. The regulation's emphasis on circular economy principles aligns with temporary building capabilities for disassembly, reconfiguration, and material reuse. European focus on sustainability drives innovation in eco-friendly materials and energy-efficient designs, positioning the region as a leader in green modular construction technologies and sustainable temporary storage solutions.

Asia Pacific Temporary Storage Buildings/Sheds Trends

Asia Pacific represents the fastest-growing regional market with China dominating production capacity and consumption patterns while India emerges as a key expansion destination for international occupiers. China's rapid industrialization and e-commerce growth create massive demand for flexible storage infrastructure, supported by government policies promoting urbanization and manufacturing development. The region benefits from competitive labor costs, integrated supply chains, and established manufacturing expertise in steel and modular construction.

India's warehousing sector demonstrates exceptional dynamism with high absorption rates within the country over the next few years. ASEAN nations including Vietnam, Indonesia, and Thailand experience robust manufacturing growth requiring immediate storage solutions for raw materials and finished goods. The region's young demographics, rising disposable incomes, and improving digital connectivity support sustained demand for retail and logistics infrastructure, creating substantial opportunities for temporary storage building deployment across diverse applications and industries.

Competitive Landscape

The global temporary storage buildings market exhibits moderate fragmentation with numerous regional players competing alongside established global manufacturers. Market leaders differentiate through vertical integration, proprietary building systems, and comprehensive service offerings encompassing design, manufacturing, installation, and maintenance. Companies employ diverse strategies, including rental/lease models, turnkey solutions, and technology licensing to capture market opportunities across different customer segments.

Innovation focuses on rapid deployment capabilities, sustainable materials, digital integration, and customizable designs that address specific industry requirements. Strategic partnerships between manufacturers and end-user industries facilitate product development and market penetration, while merger and acquisition activities target capacity expansion, geographic reach, and technology capabilities.

Key Market Developments

- In September 2024, GP Portable Buildings LLC, a manufacturer of outdoor storage buildings, announced a US$ 7.4 million investments to establish a new manufacturing facility in Marston, Richmond County, North Carolina. This expansion is expected to create 51 new jobs and enhance the company's production capacity for portable storage solutions.

- In December 2023, Storefriendly, a leading self-storage provider in Asia, announced the acquisition of a self-storage building in Hong Kong. The facility features advanced technologies, including robotic storage systems and AI-powered facilities, enhancing operational efficiency and customer experience.

Companies Covered in Temporary Storage Buildings/Sheds Market

- Skanska

- Clayton Homes

- GNB Global

- Shield Structures

- Spaciotempo

- Mar-Key Group

- Derksen Portable Buildings

- Countryside Barns

- Modulaire Group

- Bouygues Construction

- Lendlease Corporation

- Cavco Industries

- Red Sea Housing

- Champion Homes

- Z Modular

- Fleetwood

- Horizon North

Frequently Asked Questions

The global temporary storage buildings/sheds market is projected to reach US$ 7.7 billion by 2032, growing from US$ 4.7 billion in 2025 at a CAGR of 7.3%.

Exponential e-commerce growth requiring flexible warehousing solutions and rapid industrialization in emerging markets necessitating quick-deployment storage infrastructure are the primary demand drivers accelerating market expansion.

Steel dominates with approximately 74% market share due to superior structural integrity, weather resistance, and suitability for large-span applications with minimal maintenance requirements.

North America leads the global market, with the United States controlling 72% of the regional share, supported by federal investments and a mature e-commerce infrastructure.

Smart technology integration including IoT sensors, BIM, and digital monitoring systems presents the primary opportunity, creating value-added services for logistics and industrial clients.

Leading companies include Skanska, Clayton Homes, GNB Global, Shield Structures, Modulaire Group, and Bouygues Construction, among others, with market leadership determined by manufacturing capabilities, service offerings, and geographical presence.