- Medical Devices

- Biopsy Devices Market

Biopsy Devices Market Size, Share, and Growth Forecast 2026 - 2033

Biopsy Devices Market by Product Type (Needle-based Biopsy Guns, Biopsy Guns, Biopsy Forceps), Application (Breast Biopsy, Skin Biopsy, Kidney Biopsy, Others), End-user (Imaging Centers, Hospitals, Others), and Regional Analysis, 2026 - 2033

Biopsy Devices Market Size and Trend Analysis

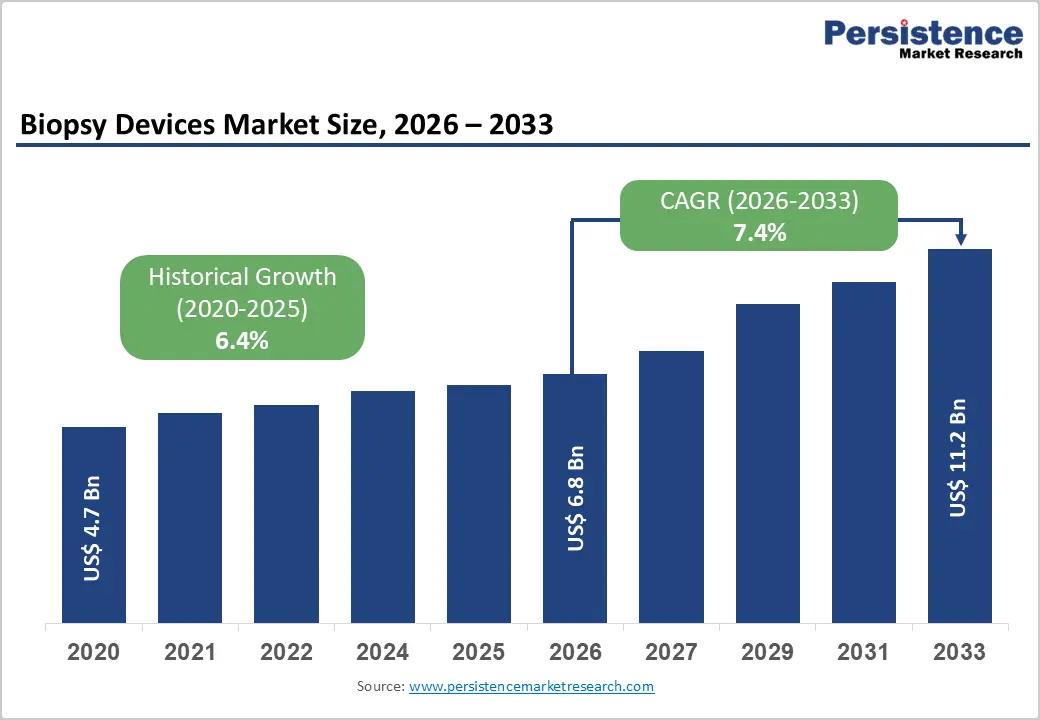

The global biopsy devices market size is expected to be valued at US$ 6.8 billion in 2026 and projected to reach US$ 11.2 billion by 2033, growing at a CAGR of 7.4% between 2026 and 2033. This is primarly driven primarily by the rise in cancer cases across the globe as the International Agency for Research on Cancer (IARC) projects nearly 35 million new cancer cases by 2050, a 77% increase from the estimated 20 million cases recorded in 2022, making early and accurate tissue diagnosis more critical than ever.

Minimally invasive biopsy systems, including needle-based platforms and vacuum-assisted devices, are increasingly preferred across hospitals and imaging centers. In contrast, the integration of artificial intelligence and real-time imaging guidance continues to enhance diagnostic precision and clinical throughput globally.

Key Industry Highlights:

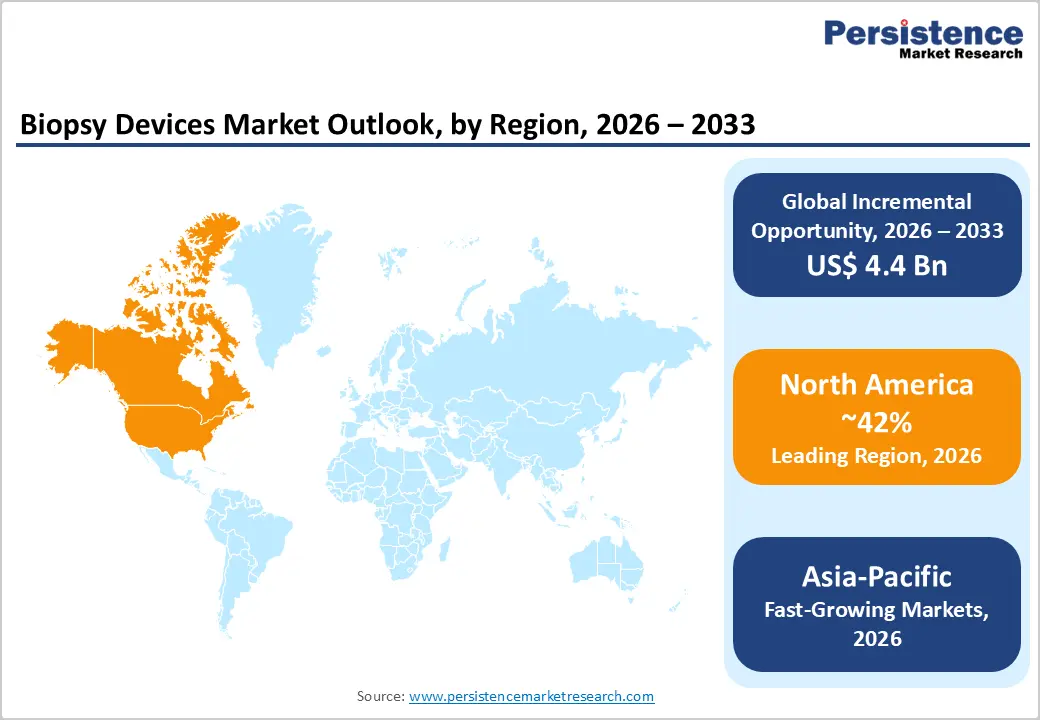

- Leading Region – North America: North America held approximately 42% of the global biopsy devices market in 2025, driven by high cancer incidence, advanced healthcare infrastructure, favorable FDA regulatory frameworks, and the presence of leading manufacturers, including Hologic, Inc. and Danaher Corporation.

- Fastest Growing Market – Asia Pacific is the fastest-growing regional market, fueled by an increase in cancer cases across China and India, government-led early detection initiatives such as the Healthy China 2030 program, and rapid expansion of hospital-based oncology diagnostic infrastructure.

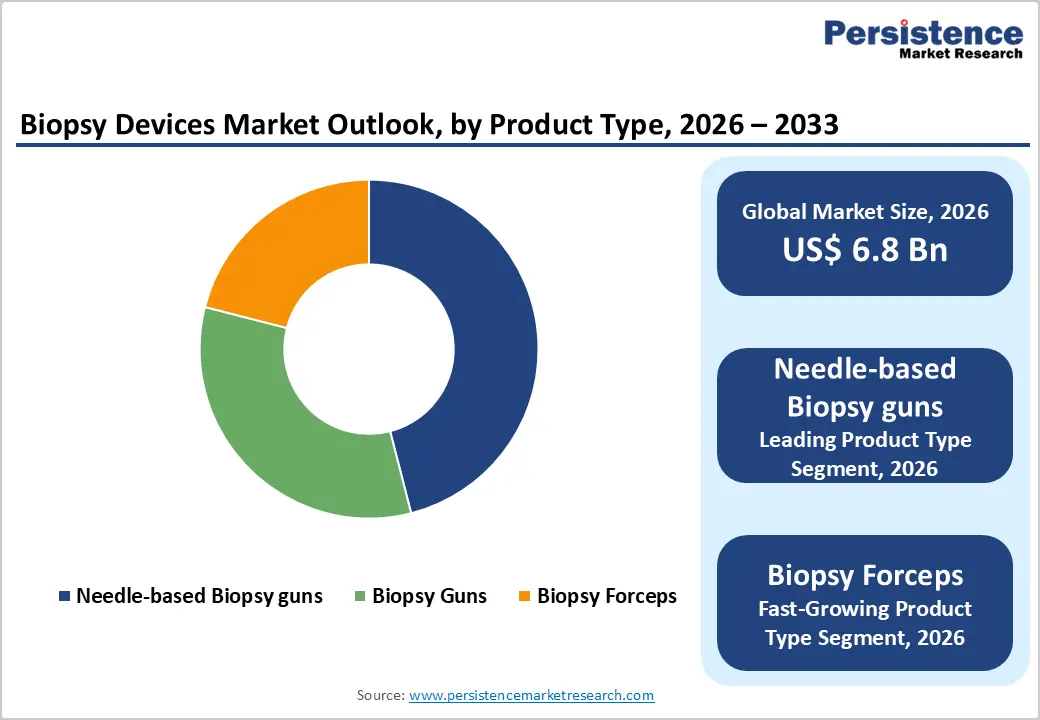

- Dominant Segment – Needle-based biopsy guns account for approximately 46% of global market share in 2025, reflecting widespread clinical adoption across breast, prostate, and kidney biopsy applications, supported by continuous innovation exemplified by Mammotome AutoCore's 2024 commercial launch.

- Fastest Growing Product Segment – Biopsy forceps represent the fastest-growing product segment, driven by expanding endoscopic biopsy procedures in gastroenterology and pulmonology and the growing adoption of minimally invasive tissue sampling across emerging markets.

- Key Opportunity – AI-Powered Biopsy Diagnostics: Integration of AI-powered pathology tools and robotic-assisted biopsy systems presents the most significant near-term market opportunity, with Ibex Medical Analytics and Biobot Surgical receiving key regulatory approvals in 2025, enabling enhanced diagnostic precision and greater clinical efficiency.

Market Dynamics

Drivers - Rising Global Cancer Burden Intensifying Diagnostic Demand

The rise in global incidences of cancer encourages the need for biopsy devices. According to the World Health Organization (WHO)'s cancer research arm, the International Agency for Research on Cancer (IARC), global cancer cases stood at approximately 20 million in 2022 and are projected to surge to nearly 35 million by 2050, a 77% increase that dramatically amplifies the clinical need for accurate and timely tissue sampling. In the United States alone, the American Cancer Society (ACS) estimates over 2 million new cancer cases annually, with breast, lung, and prostate cancers leading diagnoses.

Biopsy remains the definitive gold standard for cancer confirmation, ensuring a direct and proportional relationship between rising global incidence rates and the demand for advanced biopsy devices. Furthermore, early detection programs promoted by agencies such as the Centers for Disease Control and Prevention (CDC) are expanding population-level screening initiatives, translating directly into greater utilization of biopsy procedures across diverse clinical settings.

Restraints - High Cost of Advanced Biopsy Systems

The high acquisition and operational costs associated with advanced biopsy systems, particularly vacuum-assisted devices, robotic platforms, and MRI-compatible guidance systems, pose a significant barrier to widespread market penetration, especially in low- and middle-income countries. Vacuum-assisted biopsy units can carry capital costs several times higher than conventional core needle devices, limiting adoption in resource-constrained healthcare environments. According to the World Bank, approximately 54% of the global population resides in lower-middle-income countries where healthcare infrastructure remains underdeveloped. These cost disparities restrict the market's ability to reach substantial patient populations in high-burden regions, dampening overall procedure volumes and constraining addressable market expansion for premium biopsy device manufacturers.

Opportunities - AI-Powered Diagnostics and Robotic Biopsy Systems

The convergence of artificial intelligence (AI), machine learning, and robotics within the biopsy devices ecosystem presents a transformative commercial opportunity for market participants. AI-powered pathology platforms demonstrate the ability to reduce diagnostic error rates, accelerate tissue analysis timelines, and enhance the interpretive precision of biopsy specimens. In February 2025, Ibex Medical Analytics secured FDA clearance for its Prostate Detect platform, enabling AI-assisted cancer detection in prostate biopsy samples, reflecting growing regulatory acceptance of AI-driven diagnostics. In January 2025, Biobot Surgical's Mona Lisa 2.0 received CE mark approval for robotic prostate biopsy and ablation procedures. Furthermore, in April 2025, ArteraAI Prostate received FDA authorization to predict long-term cancer outcomes using AI-powered digital pathology. Companies investing in AI-augmented and robot-assisted biopsy systems are well-positioned to command premium pricing and differentiate competitively in high-value developed healthcare markets.

Category-wise Analysis

Product Type Insights

Needle-based biopsy guns account for approximately 46% of the global biopsy devices market in 2025, making them the dominant product segment by a decisive margin. This leadership reflects the modality's widespread clinical adoption across tissue sampling applications, including breast, prostate, kidney, and liver biopsies, where core needle systems offer an optimal balance of sample quality, procedural safety, and cost-effectiveness. Automated and semi-automated spring-loaded needle biopsy systems enable clinicians to obtain multiple high-quality tissue cores in a single insertion, reducing the need for repeat interventions and improving workflow efficiency. The commercial launch of the Mammotome AutoCore Single Insertion Core Biopsy System by Mammotome in November 2024 the first automated spring-loaded core needle device commercially available, exemplifies the segment's innovation trajectory. Compatibility with real-time ultrasound, CT, and MRI imaging guidance further reinforces the clinical preference for needle-based systems globally.

Application Insights

Breast biopsy represents the leading application segment within the global biopsy devices market, accounting for an estimated 35% share in 2025. This dominance reflects the exceptionally high global burden of breast cancer, the most commonly diagnosed cancer worldwide. According to the International Agency for Research on Cancer (IARC), breast cancer accounted for approximately 2.3 million new cases globally in 2022, representing 11.6% of all new cancer diagnoses. Clinically, percutaneous breast biopsy including vacuum-assisted core needle and stereotactic image-guided procedures, has largely replaced open surgical biopsy as the standard of care, particularly for non-palpable lesions detected via mammography or tomosynthesis. Dense breast notification legislation enacted in the United States in September 2024 has further elevated supplemental screening demand, indirectly increasing biopsy procedure volumes across hospitals and breast care centers.

Regional Insights

North America Biopsy Devices Market Trends and Insights

North America dominates the biopsy devices market, supported by strong diagnostic infrastructure, high screening penetration, and advanced technology adoption. The region accounted for over 43% global share, driven by high biopsy procedure volumes and early cancer detection programs. Favorable reimbursement systems and continuous FDA approvals further accelerate adoption.

- United States Biopsy Devices Market Trends and Insights

The United States leads due to high cancer burden and advanced diagnostics. According to the National Cancer Institute, about 2 million new cancer cases were diagnosed in 2024, significantly driving biopsy demand . Strong reimbursement frameworks and early screening programs (breast, lung, prostate) support procedure volumes. The country is expected to reach US$ 2.4–2.6 Bn, driven by AI-integrated biopsy systems and minimally invasive adoption across hospitals and outpatient centers.

- Canada Biopsy Devices Market Trends and Insights

Canada is emerging as the fastest-growing market due to increasing cancer screening and public healthcare expansion. According to the Canadian Cancer Society, over 247,000 new cancer cases were reported in 2023, supporting demand for diagnostic procedures. Government-backed screening programs and rising adoption of image-guided biopsies are key growth factors. The market is expected to achieve ~8.2% CAGR, driven by improving access to diagnostic technologies and rising aging population.

Europe Biopsy Devices Market Trends and Insights

Europe is a critical market driven by structured cancer screening programs and universal healthcare systems. According to the World Health Organization, the region records over 3.7 million new cancer cases annually, creating sustained demand for biopsy diagnostics . Strong regulatory frameworks and standardized clinical pathways ensure high procedure adoption. Europe remains stable and innovation-driven, contributing significantly to the global biopsy devices market growth trajectory.

- Germany Biopsy Devices Market Trends and Insights

Germany leads due to advanced healthcare infrastructure and high diagnostic spending. The country has one of Europe’s highest screening participation rates, particularly in breast and colorectal cancer programs. According to OECD data, Germany spends over 12% of GDP on healthcare, supporting widespread adoption of advanced biopsy technologies. It is expected to reach US$ 1.1 billion, driven by strong hospital networks and early disease detection initiatives.

- United Kingdom Biopsy Devices Market Trends and Insights

The UK is the fastest-growing market due to aggressive screening initiatives like NHS cancer programs. The country reports ~385,000 new cancer cases annually, according to national statistics, driving biopsy demand. Government campaigns such as early diagnosis initiatives are increasing procedure volumes. The market is expected to grow at ~8% CAGR, supported by expanding diagnostic capacity and focus on early-stage cancer detection.

Asia Pacific Biopsy Devices Market Trends and Insights

Asia Pacific is the fastest-growing region due to rising cancer burden, improving healthcare infrastructure, and increasing awareness. Countries like China and India together account for a significant share of global cancer cases (China ~18%, India ~5%) . Rapid urbanization, government health programs, and expansion of diagnostic centers are accelerating biopsy adoption. The region is witnessing strong growth aligned with the global CAGR of 7.4%, with higher upside due to unmet diagnostic needs.

- China Biopsy Devices Market Trends and Insights

China dominates due to its massive patient pool and expanding healthcare system. The country accounts for over 4.8 million new cancer cases annually, according to global cancer statistics, significantly driving biopsy demand. Government investments in oncology infrastructure and diagnostic capacity are accelerating adoption. China is expected to reach US$ 1.7 billion, supported by rapid hospital expansion and increasing use of image-guided biopsy technologies.

- India Biopsy Devices Market Trends and Insights

India is the fastest-growing market due to rising awareness and expanding healthcare access. According to ICMR, India reports over 1.4 million new cancer cases annually, with increasing screening initiatives. Government programs like Ayushman Bharat are improving diagnostic accessibility. The market is expected to reach ~9% CAGR, driven by growing private hospital networks, diagnostic chains, and increasing adoption of minimally invasive biopsy procedures.

Competitive Landscape

The global biopsy devices market exhibits a moderately consolidated competitive structure, with a small number of multinational medical device corporations holding dominant positions alongside a larger cohort of regional and niche players. Companies such as Hologic, Inc., Danaher Corporation, Cardinal Health, Inc., Olympus Corporation, and Cook Medical command significant market shares through broad product portfolios, global distribution networks, and continuous R&D investment. Key competitive strategies include strategic acquisitions exemplified by Hologic's 2025 acquisition of Gynesonics to strengthen its women's health portfolio alongside AI and digital pathology integration, device miniaturization, and single-use disposable formats. Emerging subscription-based software analytics bundled with biopsy device platforms are also reshaping business model differentiation within the sector.

Key Developments

- March 2026: Mammotome secured FDA clearance for its industry-first in-room MR vacuum-assisted breast biopsy system and HydroMARK™ Plus MR biopsy site markers.The newly approved system enabled clinicians to perform MRI-guided breast biopsies directly within the MRI suite, eliminating the need to move patients between rooms and improving procedural efficiency and accuracy.

- February 2025: The software was designed to work with contrast-enhanced mammography (CEM), enabling clinicians to accurately target and biopsy lesions that are highlighted through contrast imaging but may not be visible on conventional imaging. By integrating with the Affirm® breast biopsy guidance system, it improved lesion localization, procedural confidence, and diagnostic accuracy.

Global Biopsy Devices Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 4.7 Billion |

|

Projected Market Value (2026) |

US$ 6.8 Billion |

|

Projected Market Value (2033) |

US$ 11.2 Billion |

|

CAGR (2026-2033) |

7.4% |

|

Leading Region |

North America, 42% share |

|

Dominant Product |

Needle-based Biopsy guns, 46% share |

|

Top-ranking Application |

Breast Biopsy, 41% share |

|

Incremental Opportunity |

US$ 4.4 billion |

Companies Covered in Biopsy Devices Market

- Cardinal Health, Inc.

- Hologic, Inc.

- Danaher Corporation

- CONMED Corporation

- Cook Medical

- DTR Medical Ltd.

- INRAD, Inc.

- Devicor Medical Products, Inc.

- TransMed7, LLC

- Olympus Corporation

- Others

Frequently Asked Questions

The global biopsy devices market is estimated to be valued at US$ 6.8 billion in 2026.

Rising cancer incidence, demand for early diagnosis, minimally invasive procedures, technological advancements, expanding screening programs globally.

North America is the leading regional market, accounting for approximately 42% of the global Biopsy Devices market share in 2025.

Expansion in emerging markets, liquid biopsy adoption, AI integration, outpatient settings, and personalized cancer diagnostics growth.

Cardinal Health, Inc., Hologic, Inc., Danaher Corporation, CONMED Corporation, Cook Medical, DTR Medical Ltd.