- Medical Devices

- Bioabsorbable Stents Market

Bioabsorbable Stents Market Size, Share, Trends, Growth, and Forecasts for 2025 - 2032

Bioabsorbable Stents Market by Material Type (Polymer-based, Metal-based), Product Type (Drug-eluting, Bare), Application (Coronary Artery Disease, Peripheral Artery Disease), End-use (Hospitals, Cardiology Centers), and Regional Analysis for 2025 - 2032

Bioabsorbable Stents Market Size and Trends Analysis

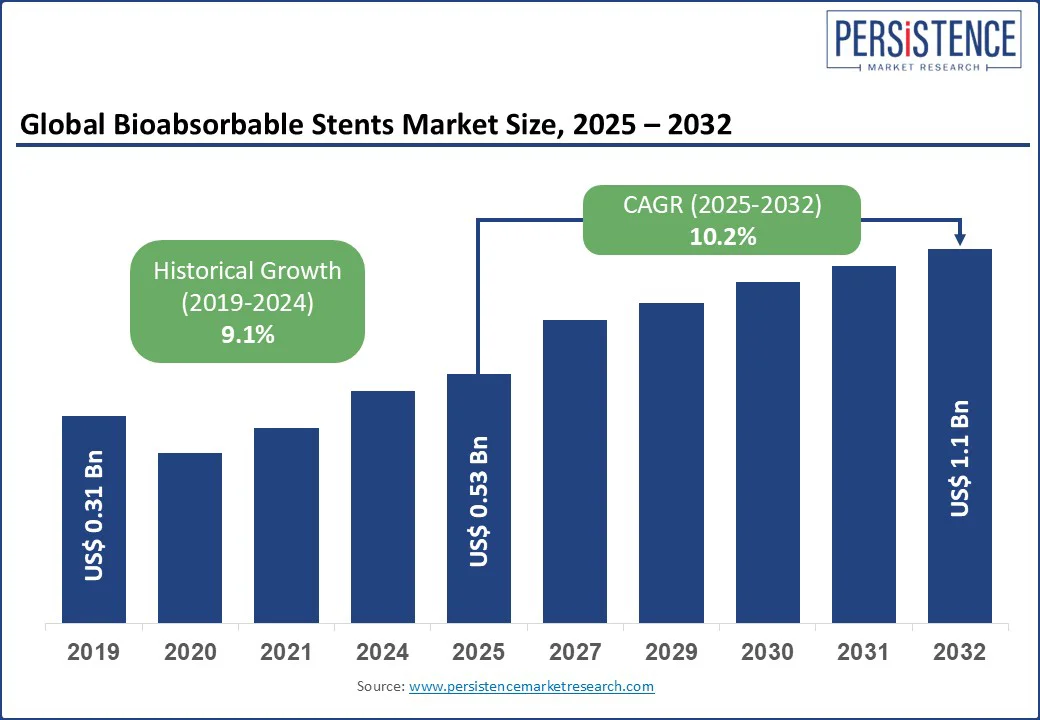

The global bioabsorbable stents market size is likely to be valued at US$ 0.53 Bn in 2025, and is estimated to reach US$ 1.1 Bn by 2032, growing at a CAGR of 10.2% during the forecast period 2025 - 2032. The bioabsorbable stents market is driven by the growing prevalence of cardiovascular disease, increasing demand for minimally invasive procedures, and adoption of next-generation stent technologies. Unlike traditional metallic stents, bioabsorbable stents naturally dissolve in the body over time, reducing long-term complications such as in-stent restenosis and thrombosis.

These devices are gaining traction across both developed and emerging markets, supported by advancements in bioresorbable materials such as polymers and magnesium alloys. Technological innovations, favorable clinical outcomes, and ongoing regulatory approvals are further accelerating adoption. Conversely, challenges related to high costs, limited availability, and device safety remain key considerations for market stakeholders.

Key Industry Highlights:

- The coronary artery disease (CAD) segment remains the most dominant with a market share of 79% in 2025, driven by the demand for temporary vascular scaffolds that dissolve naturally after vessel healing, reducing long-term complications associated with permanent stents.

- While polymer-based stents (mainly PLLA) maintain market leadership, magnesium- and zinc-based metal stents are the fastest-growing segment, offering better mechanical strength, visibility, and faster resorption.

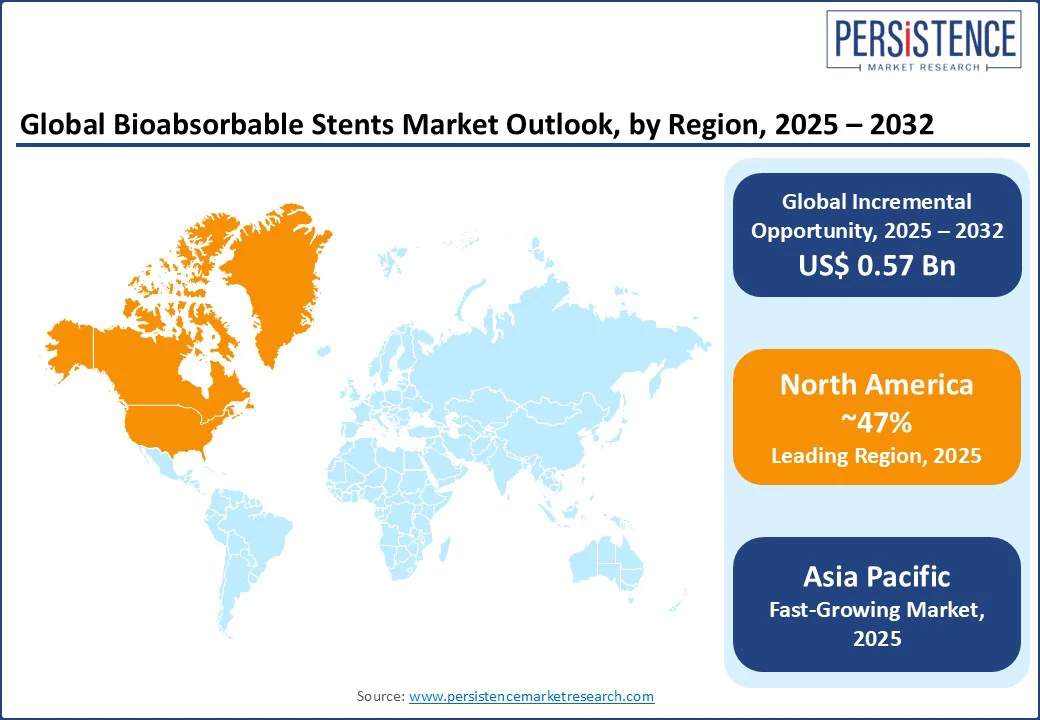

- North America leads the market, accounting for over 47% of the market share in 2025, owing to early clinical adoption, advanced regulatory frameworks, and widespread use of magnesium-based bioresorbable stents.

- Technological innovation is focused on next-generation alloy platforms, particularly magnesium and zinc-based devices, offering improved radial strength, biocompatibility, and predictable resorption rates.

- The market is witnessing rising adoption in Asia Pacific, especially in China and India, due to favorable government investments, local manufacturing initiatives, and a growing cardiovascular disease burden.

- Key players such as Biotronik, Elixir Medical, Arterius Ltd., Meril Life Sciences, and REVA Medical are accelerating clinical trials and product launches aimed at improving deployment precision, safety, and patient recovery outcomes.

|

Market Attribute |

Key Insights |

|

Bioabsorbable Stents Market Size (2025E) |

US$ 0.53 Bn |

|

Market Value Forecast (2032F) |

US$ 1.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

10.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.1% |

Market Dynamics

Driver - Increasing Demand for AI-Guided Stent Placement and Imaging-Optimized Deployment

The bioabsorbable stents market is driven by the adoption of magnesium-based bioresorbable alloy stents and next-generation devices, such as Magmaris, that exhibit controlled resorption and strong radial support. These bioresorbable metal stents leverage metallic corrosion engineering and tailored alloy composition to reduce scaffold thrombosis and vessel recoil, spurring clinical interest and elective use in precision interventional cardiology. Targeted devices are being approved through pathways such as the FDA Breakthrough Device program, expediting the first-in-the-world launches of magnesium and zinc alloy stents.

Investments in polymer-based drug-eluting bioabsorbable stents are rising due to engineered coatings combining everolimus with biodegradable PLA frameworks. These next-gen polymer-based BVS devices deliver anti-restenosis therapy while enabling vessel restoration after dissolution, making them attractive for younger CAD patients and outpatient PCI procedures. Simultaneously, the growing demand for AI-guided personalized stent placement and imaging-optimized deployment (via OCT and IVUS) is improving procedural precision and driving the adoption of smart bioabsorbable stent platforms by clinicians in leading catheterization labs worldwide.

Restraint - Magnesium Alloy Degradation Undermines Stent Stability

Polymer-based PLLA scaffold limitations hinder the adoption of polymer-based, drug-eluting bioabsorbable stents. These devices require thick struts to compensate for weak radial strength in vivo, which leads to vessel injury and elevated risk of scaffold fracture and late thrombosis during degradation. Asymmetric strut degradation causes malapposition and mechanical discontinuity, heightening restenosis in long-term follow-up. These performance issues limit use to very specific lesion types and restrict broader clinical uptake.

Magnesium alloy degradation inconsistencies hinder stability and structural reliability of magnesium-based bioresorbable metal stents. Rapid corrosion in chloride-rich body fluids can cause early loss of radial support before vessel healing, sometimes within weeks rather than months. This accelerated degradation may lead to hydrogen gas formation, local alkalinity shifts, inflammation, and neointimal proliferation. Mechanical fatigue and early strut fracture under vessel deformation remain concerns, especially considering the current limitations in magnesium alloy strength and flexibility.

Opportunity - AI-Driven Hybrid Stents & Robotic Delivery to Revolutionize Coronary Care

The rise in hybrid polymer-metal composite stent development offers a unique growth path. These hybrid stents blend magnesium alloy frameworks with polymer-drug-eluting layers to deliver faster vessel healing and controlled degradation. Early studies show enhanced mechanical support and smoother absorption of magnesium-based WE43 alloy combined with everolimus-coated PLA. This synergy opens doors in personalized coronary scaffolding, enabling tailored device selection for different lesion complexities.

AI-optimized magnesium alloy stent design and robotic-assisted catheter deployment are unlocking precise, next-level procedural outcomes. Machine learning algorithms now predict ideal alloy compositions for strength and corrosion control, while robotic systems with real-time vessel segmentation enable more precise navigation during stent deployment. The integration of these innovations enables the placement of intelligent bioresorbable scaffolds in complex anatomies, enabling wider adoption in advanced catheter labs and academic medical centers.

Category-wise Insights

Material Type Insights

Polymer-based bioabsorbable stents, particularly those made from poly-L-lactic acid (PLLA), are projected to lead the market with a share of around 58%. Their leadership stems from earlier regulatory approvals and extensive clinical usage, especially in drug-eluting formats that help reduce restenosis. These stents are widely used in CAD cases due to their compatibility with pharmacological coatings and proven biocompatibility. However, limitations such as thicker strut profiles, lower radial strength, and delayed resorption timelines (two–three years) hinder long-term performance and physician confidence.

Metal-based bioabsorbable stents, particularly those made from magnesium and zinc alloys, represent the fastest-growing material segment. These alloys offer superior mechanical strength, thin-strut design, and significantly shorter degradation times (6–12 months), making them more appealing for younger and active patients who require temporary support with minimal long-term risks. These stents minimize late scaffold thrombosis risks and offer improved visibility, encouraging their inclusion in next-gen scaffold trials.

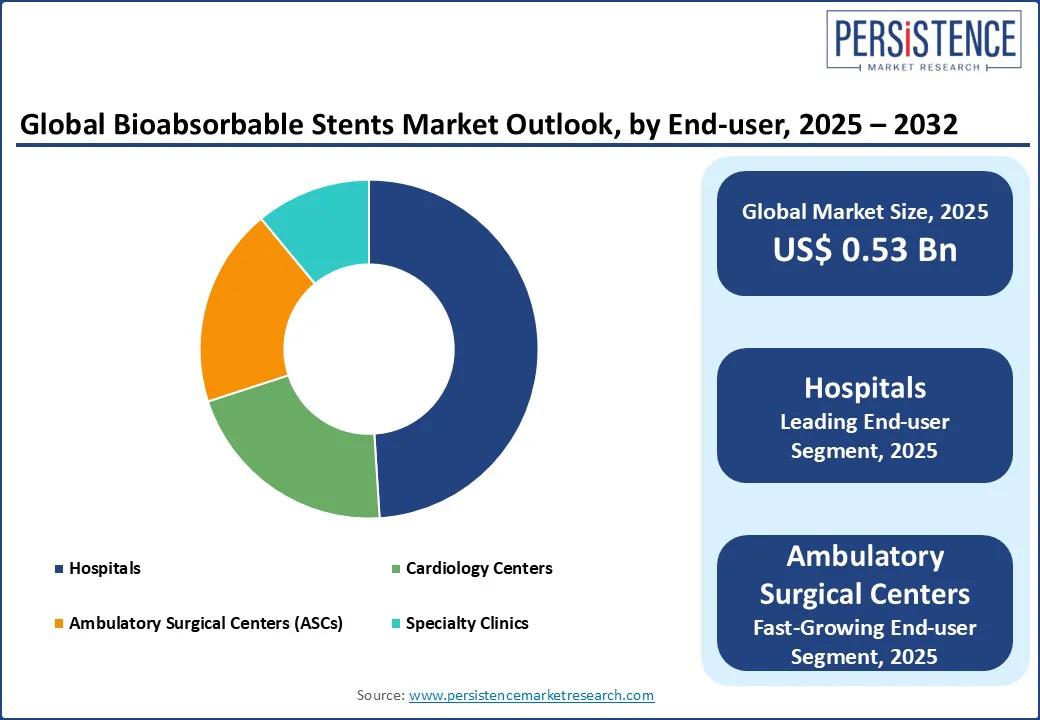

End-use Insights

By end-use, the hospitals segment is anticipated to be the largest end-use segment, capturing approximately 49% of the total market share in 2025. Its dominance is driven by access to catheterization labs, interventional cardiologists, and advanced imaging modalities such as intravascular ultrasound (IVUS) and optical coherence tomography (OCT). Hospitals are the preferred centers for complex angioplasty procedures and post-operative monitoring, particularly in Europe and North America, where reimbursement structures and patient care protocols support in-patient interventions.

Ambulatory Surgical Centers (ASCs) are emerging as the fastest-growing end-use segment, especially in regions such as the U.S., Germany, and the U.K. ASCs are increasingly adopting same-day PCI models, reducing hospitalization costs and improving patient turnover. The rise of minimally invasive techniques, combined with the improved safety profile of newer bioabsorbable stents, is accelerating their adoption in outpatient settings. ASCs also benefit from regulatory support in value-based healthcare systems and growing confidence in low-risk PCI cases, particularly for single-vessel disease in stable patients.

Regional Insights

North America Bioabsorbable Stents Market Trends

North America remains the largest contributor, accounting for 47% of the global bioabsorbable stents market. The U.S. leads due to a high prevalence of CAD, with over 800,000 percutaneous coronary interventions (PCI) performed annually. The region's advanced cardiovascular care ecosystem has facilitated early adoption of AI-guided imaging platforms such as IVUS and OCT for stent optimization.

Clinical trials such as ABSORB III and IV, both U.S.-centric, laid the foundation for bioresorbable scaffolds. Despite initial setbacks (Abbott’s Absorb GT1 withdrawal in 2017), renewed interest has surged with magnesium-based scaffolds such as the BIOTRONIK Magmaris, supported by recent FDA Breakthrough Device Designations. In 2024, Amaranth Medical re-initiated clinical trials for its Fortitude bioresorbable scaffold, citing improved material properties and faster endothelialization. Additionally, value-based care models and CMS reimbursement shifts are aligning incentives toward long-term cost reduction, favoring temporary implants such as bioabsorbable stents.

Europe Bioabsorbable Stents Market Trends

Europe remains at the forefront of clinical innovation in bioabsorbable stents, with countries including Germany, France, and the U.K. leading adoption. Germany stands out for investing in thinner strut design and polymer coatings, with clinical data from the DAEDALUS and BIOSOLVE programs showing up to 78% reduction in scaffold thrombosis. In 2023, the BIOSOLVE-IV registry (with >2,000 patients) reported encouraging long-term outcomes for Dreams 2G magnesium scaffolds.

France’s National Agency for Medicines and Health Products Safety (ANSM) has streamlined post-market evaluation processes, encouraging new trials and faster approvals for European-made devices. The U.K.'s NHS is trialing bioresorbable options for younger STEMI patients in collaboration with research institutes such as Imperial College London, particularly in patients undergoing hybrid stenting (metal + bioabsorbable) approaches.

Furthermore, Europe’s Horizon Europe Program (2021–2027) is co-funding R&D for bioresorbable composite materials, while public stent registries in Sweden and the Netherlands ensure better safety tracking and real-world validation.

Asia Pacific Bioabsorbable Stents Market Trends

Asia Pacific is the fastest-growing regional market, with a forecasted CAGR of 5.5% through 2030. China is rapidly scaling up adoption in Tier 1 and Tier 2 hospitals, especially for patients under 50 with single-vessel disease. In 2024, MicroPort Scientific launched a domestically developed BVS platform, which received conditional approval under China’s Green Channel policy. Furthermore, partnerships between Shanghai Jiao Tong University and private manufacturers are developing next-gen zinc-magnesium alloy scaffolds with shorter degradation cycles.

India is also witnessing robust growth through public-private cardiovascular health programs such as Ayushman Bharat, enabling coverage for high-risk PCI procedures. Startups such as Sahajanand Medical Technologies (SMT) have expanded trials for their MeRes100™ bioresorbable scaffold in urban heart centers. Several hospitals in Mumbai, Bengaluru, and Ahmedabad are now using polymer BVS kits in elective angioplasties, supported by government-backed skill training programs for interventional cardiologists.

Competitive Landscape

The global bioabsorbable stents market is currently moderately consolidated, led by a mix of established medical device manufacturers and emerging cardiovascular innovators. Companies are shifting focus from first-generation polymer-only scaffolds to magnesium-based and hybrid alloy stents with better radial strength, bio-compatibility, and predictable degradation profiles. These innovations aim to reduce late scaffold thrombosis and provide more effective vascular support, especially in younger CAD patients. Strategic investments in thin-strut technology, controlled drug elution, and fast endothelialization are now central to maintaining competitive advantage.

Biotronik SE & Co. KG remains a global frontrunner with its Magmaris magnesium scaffold, which has shown promising outcomes in European patients. The company is now expanding its CE-mark trials to new markets. Similarly, Elixir Medical Corporation is making headlines with its DREAMS 3G platform, currently under clinical evaluation in the U.S. and India through the BIOADAPT trial. Meanwhile, Arterius Ltd. has accelerated the development of ArterioSorb™, a polymer-based bioresorbable stent with ultra-thin struts, aimed at reducing healing time and improving patient recovery.

Key Industry Developments

- In February 2025, Lepu Medical (China) received approval for its self-developed bioabsorbable coronary stent under China’s priority review channel, aiming to serve the rising domestic CAD population.

- In May 2024, Abbott Laboratories confirmed its return to the bioresorbable space with early-stage R&D on next-gen ultra-thin strut BVS platforms with improved resorption timelines (under 18 months) and targeted drug delivery coatings.

Frequently Asked Questions

The global bioabsorbable stents market is expected to be valued at US$ 0.53 Bn in 2025, driven by increasing adoption in coronary artery disease treatment.

By the end of the forecast period (2032), the market is estimated to reach approximately US$ 1.1 Bn.

Key trends include a shift toward magnesium-based scaffolds, robotic-assisted stent delivery systems, AI-guided imaging, and rising demand for ultra-thin strut bioresorbable platforms with faster resorption profiles.

The coronary artery disease (CAD) segment dominates the market due to high PCI volumes and demand for minimally invasive solutions that eliminate long-term implant risks.

The bioabsorbable stents market is projected to grow at a CAGR of 10.2%.

Leading companies include Biotronik SE & Co. KG, Elixir Medical Corporation, Arterius Ltd., REVA Medical, LLC, and Abbott Laboratories.