- Home Care & Utilities

- Bio-Furnishing Market

Bio-Furnishing Market Size, Trends, Share, and Growth Forecast 2025 - 2032

Bio-Furnishing Market by Product Type (Furniture Components, Soft Furnishing & Textiles, Decorative Accessories), Application (Residential, Commercial), Distribution Channel (Online, Hypermarket/Supermarket, Specialty Stores, Other), and Regional Analysis for 2025 - 2032

Bio-Furnishing Market Size and Trend Analysis

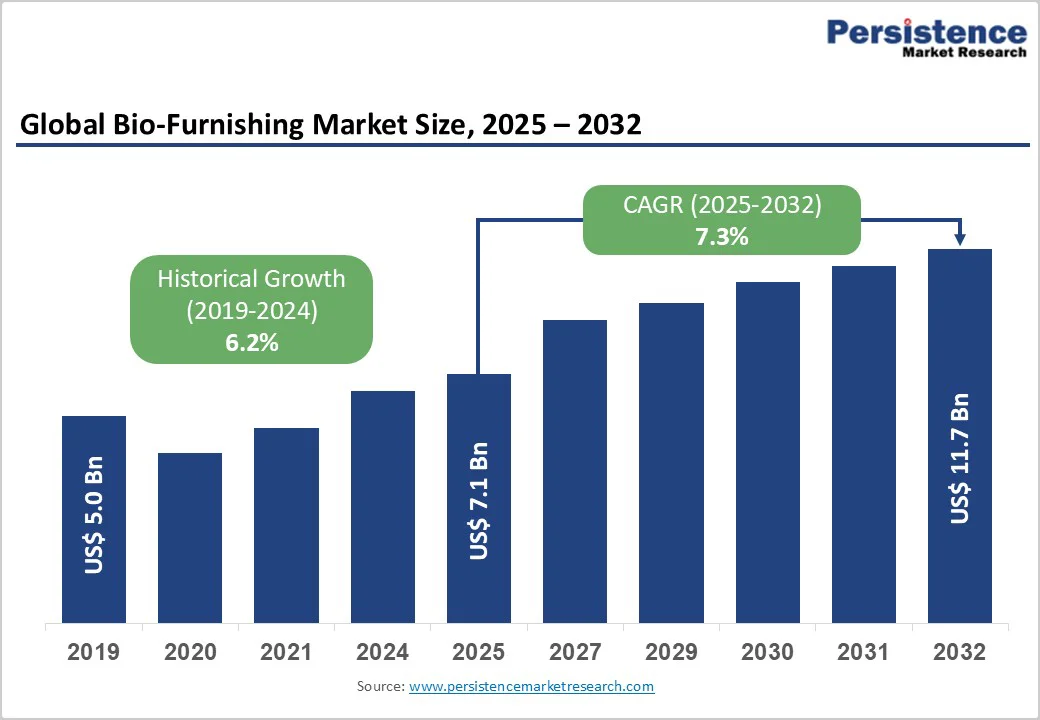

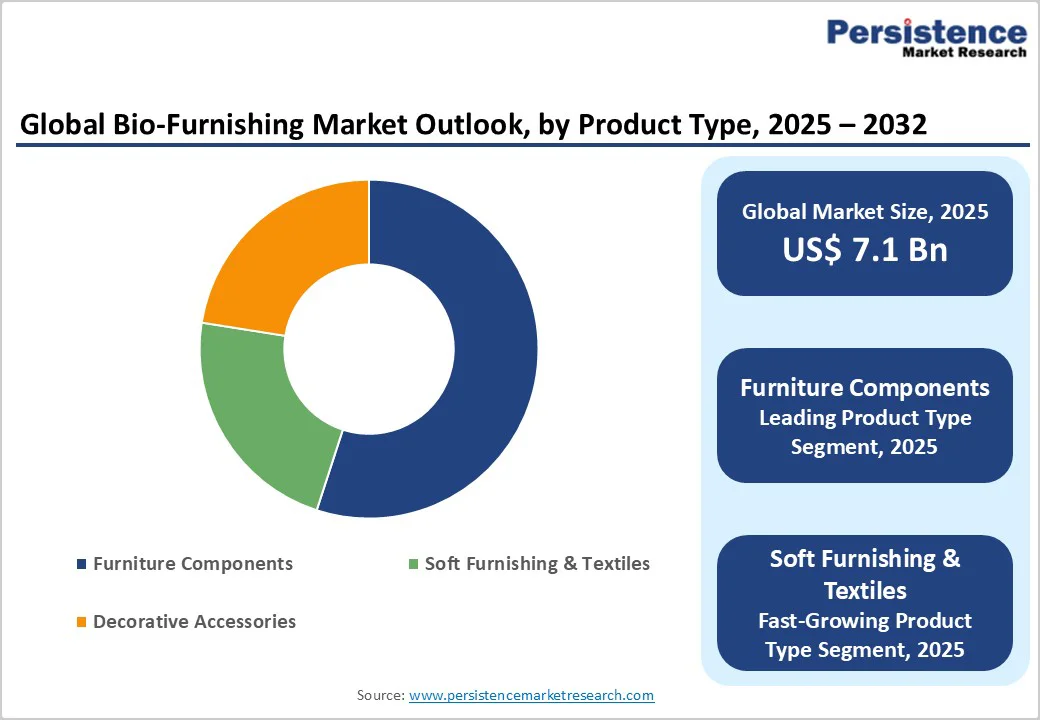

The global bio-furnishing market size is valued at US$7.1 billion in 2025 and is projected to reach US$11.7 billion, growing at a CAGR of 7.3% between 2025 and 2032. The primary drivers include heightened consumer awareness of environmental sustainability and the health risks posed by conventional furniture, leading to increased demand for bio-based alternatives made from renewable resources such as bamboo and recycled wood.

Key Market Highlights

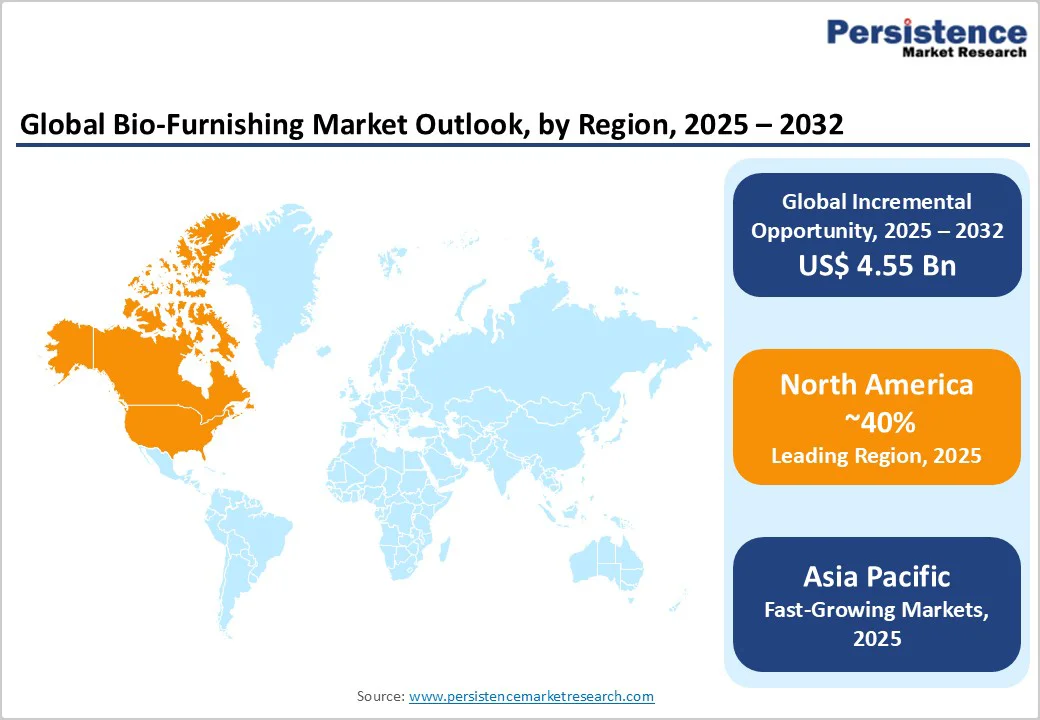

- Regional Leader: North America leads the Bio-Furnishing Market due to stringent EPA regulations and innovation in recycled materials, capturing over 35% global share with robust consumer demand for LEED-certified products.

- Fastest Growing Region: Asia Pacific emerges as the fastest-growing region, driven by manufacturing hubs in China and India, through resource abundance and urbanization fueling eco-furniture adoption.

- Leading Segment: Residential dominates applications with 70% share, as homeowners prioritize non-toxic, sustainable options like bamboo beds to support healthy living amid rising environmental awareness.

- Fastest Growing Segment: Online channels grow fastest at 40% share, enabled by e-commerce platforms offering customization and certifications, appealing to tech-savvy millennials seeking convenient bio-product access.

- Key Opportunities: Advancements in bio-materials like mycelium offer key opportunities, enabling companies to tap premium residential demand with low-impact innovations that reduce carbon footprints by 50%.

| Key Insights | Details |

|---|---|

|

Bio-Furnishing Market Size (2025E) |

US$7.1 Bn |

|

Market Value Forecast (2032F) |

US$11.7 Bn |

|

Projected Growth CAGR (2025-2032) |

7.3% |

|

Historical Market Growth (2019-2024) |

6.2% |

Market Dynamics

Drivers - Rising Consumer Awareness of Sustainability and Health Risks

Consumers are increasingly prioritizing eco-friendly products due to growing concerns about environmental degradation and the health hazards posed by traditional furniture, such as emissions of Volatile Organic Compounds (VOCs) that can cause allergies, migraines, and asthma. Research conducted by the National Institute of Health Sciences in Japan revealed that emissions from furniture products significantly influence indoor air quality, with toluene and alpha-pinene being the most dominant components emitted. The study found that VOC concentrations in interior settings are substantially higher than outdoor environments, with some furniture pieces exceeding the provisional target value of 400 microg/m3 for total VOC in residential spaces.

This trend is evidenced by the rising demand in residential settings, where families seek durable, low-emission options. For instance, the Environmental Protection Agency (EPA) highlights that 8.5 million tons of office furniture end up in landfills annually, fueling interest in sustainable alternatives that extend product lifecycles and reduce waste. Such awareness not only drives sales but also encourages manufacturers to innovate with biodegradable finishes, positively impacting market expansion by aligning with global sustainability goals.

Government Initiatives and Regulatory Support for Green Manufacturing

Governments worldwide are implementing policies and incentives to promote sustainable practices, significantly boosting the bio-furnishing sector by facilitating the use of renewable materials and reducing reliance on virgin resources. For example, the UK Government announced £440 million in funding for green construction projects, including certifications and incentives for eco-friendly furniture, thereby directly stimulating demand across both residential and commercial applications.

The European Union's Ecodesign for Sustainable Products Regulation (ESPR), which became effective in July 2024, establishes stringent sustainability requirements for products, including furniture, focusing on durability, recyclability, and environmental impact disclosure. Supporting such regulations, IKEA Group has committed to reducing its carbon footprint by 50% by 2030 and reported in its FY24 Sustainability Report that 97% of its wood is now FSC-certified or recycled, with VOC emissions reduced by 8%. By providing financial and legal backing, such initiatives lower barriers for companies to scale sustainable operations, thereby convincing stakeholders of the long-term viability and profitability of investing in bio-furnishings that comply with evolving standards such as the EU Deforestation Regulation (EUDR).

Restraints - Higher Production Costs of Bio-Based Materials

The elevated costs associated with sourcing and processing renewable materials like reclaimed wood and bio-resins pose a significant barrier, making bio-furnishings 20-30% more expensive than conventional options, which deters price-sensitive consumers and small manufacturers. This premium arises from limited supply chains for certified sustainable inputs, such as FSC-verified timber, and energy-intensive extraction processes for natural fibers, leading to higher upfront investments that strain budgets in emerging markets. As a result, market penetration slows in regions without subsidies, with data showing that cost concerns contribute to only 62% adoption rates among budget-conscious households, ultimately hindering overall growth by favoring cheaper, non-eco alternatives despite long-term environmental benefits.

Stringent Regulatory Compliance and Certification Challenges

Navigating diverse and rigorous regulations for bio-based products, including VOC limits and deforestation-free sourcing under frameworks such as EUDR, creates compliance hurdles that increase operational complexities and costs for producers. Lack of uniform global certifications leads to fragmentation, where varying standards across regions, such as California's flammability codes differing from national norms, delay product launches and raise testing expenses by up to 15%. This regulatory variability not only burdens smaller players but also confuses consumers, slowing market uptake. The non-compliance risks fines or market exclusion, convincing industry observers that without harmonization.

Market Opportunities - Advancements in Bio-Material Innovations for Residential Applications

Innovations in bio-based materials, such as mycelium composites and algae-derived foams, offer substantial opportunities for companies targeting the residential segment, where demand for customizable, low-impact furnishings is surging amid urbanization and eco-conscious millennials. These technologies enable lighter, compostable products that outperform traditional materials in durability while cutting carbon footprints by 50%, as seen in trials of hemp-based boards matching standard laminates with 70% less energy use.

Supported by developments such as 3D printing for waste-free production, this opportunity aligns with the Hometech Textiles Market's growth in sustainable home solutions, enabling firms to capture premium pricing in this segment. By investing in R&D, companies can differentiate via certifications like LEED, convincing investors of the potential to generate significant revenue from health-focused, planet-positive homes that appeal to most of Gen Z buyers willing to pay more for eco-products.

Expansion in the Commercial Sector Driven by Corporate Sustainability Policies

The commercial application offers key growth for bio-furnishings as corporations adopt green workspaces to meet ESG goals, with modular, recyclable designs like rattan office suites addressing the 8.5 million tons of annual furniture waste reported by the EPA. Policies mandating low-VOC interiors in public buildings, combined with trends in co-working spaces, create demand for scalable solutions. For instance, hotels increasingly use bio-materials to attract eco-travelers, boosting segment growth. News of expansions in sustainable procurement, such as Boston's textile recovery programs, further supports this by reducing material costs through circular models. Companies leveraging these policies can secure large contracts, as evidenced by rising adoption in hospitality, positioning bio-furnishings as a high-potential avenue for revenue diversification and leadership in the evolving corporate landscape.

Category-wise Insights

Product Type Analysis

The Furniture Components segment leads the Product Type category with an estimated 55% market share, driven by its essential role in both residential and commercial setups where durability and versatility are paramount. Items like tables, chairs, and beds made from renewable sources such as bamboo and reclaimed wood dominate due to their high everyday utility and alignment with sustainability trends.

For instance, tables alone account for 31% of product demand, supported by data showing increased adoption in home offices post-pandemic. Bamboo's rapid growth rate, structural strength comparable to hardwood, and minimal environmental impact make it an ideal bio-based material for furniture components. Greenington Fine Bamboo Furniture has pioneered sustainable harvesting techniques, selecting and hand-harvesting each bamboo stick while leaving roots intact, ensuring forest regeneration without clear-cutting. Additionally, IKEA Group reported that 97% of its wood sourcing is now FSC-certified or recycled, demonstrating industry-wide commitment to sustainable furniture component production.

Application Analysis

In the Application category, the Residential segment holds a commanding 70% market share, fueled by growing homeowner preferences for non-toxic, aesthetically pleasing furnishings that support sustainable living amid rising urbanization. Families prioritize beds and storage units made from bio-materials to minimize health risks from VOCs, with statistics indicating a projected 83.5% demand by 2034 in this area due to eco-conscious millennials renovating spaces. This dominance is validated by government incentives for green homes, such as those in the U.S., where 97% of buyers favor certified products, making residential applications a stable, high-volume opportunity that drives overall category growth through personalized, health-focused solutions.

Distribution Channel Analysis

The online segment commands 40% of the Distribution Channel category, propelled by the convenience of e-commerce platforms that enable global access to customized bio-furnishings and detailed sustainability info. Digital marketplaces facilitate comparisons of eco-certifications, with sales surging 34.94% through online channels in related home sectors, as consumers research VOC-free options from home. This lead is backed by post-2020 digital shifts, where platforms like company websites offer virtual try-ons for items like curtains and desks, enhancing purchase confidence and reducing returns; authentic data from retail trends confirms online's edge in reaching urban, tech-savvy buyers, solidifying its position as the primary channel for bio-product dissemination.

Regional Insights

North America Bio-Furnishing Market Trends

North America, led by the US, dominates the bio-furnishing landscape through robust regulatory frameworks and a mature innovation ecosystem that prioritizes sustainable sourcing. The US Environmental Protection Agency (EPA) enforces strict guidelines on waste reduction, diverting 8.5 million tons of furniture from landfills annually through recycling programs, thereby fostering demand for bio-based alternatives such as FSC-certified wood in residential renovations. Innovations in mycelium and recycled plastics thrive here, supported by certifications such as LEED for green buildings, and 73.6% of regional sales stem from eco-initiatives in coastal states.

Corporate commitments further accelerate trends, as seen in expansions of greenhouse businesses promoting ocean-bound plastic furnishings, aligning with millennial preferences for low-VOC products. This ecosystem not only drives the market in sustainable segments but also positions North America as a hub for R&D, ensuring compliance and market leadership through verifiable, health-oriented designs.

Europe Bio-Furnishing Market Trends

Europe's bio-furnishing market excels in regulatory harmonization, with Germany and the U.K. leading performance through stringent eco-standards that mandate deforestation-free materials under the EU Deforestation Regulation (EUDR), effective from 2025. Germany's export dominance, with high regional shares, stems from recycled-material mandates in Blue Angel-certified products, which reduce environmental impacts by 50% in manufacturing. Recent developments include £440 million UK funding for green projects, boosting adoption in France and Spain, where VOC limits cap emissions at 5% for coatings.

The EU Ecolabel criteria for textiles and foams ensure durability and recyclability, supporting a 7.3% CAGR in Germany through biogenic innovations such as hemp panels. Harmonized policies across the U.K., France, and Spain facilitate cross-border trade, with news of extended producer responsibility schemes encouraging circular models that minimize waste, convincing stakeholders of Europe's role in setting global sustainability benchmarks.

Asia Pacific Bio-Furnishing Market Trends

Asia Pacific's bio-furnishing growth is propelled by manufacturing advantages in China and India, where abundant resources like bamboo drive the market, supported by skilled labor and domestic demand. China's dominance leverages scale in rattan and recycled wood production and exports to global markets, while urbanizing populations in ASEAN countries fuel residential uptake. Government subsidies in India enhance the use of local bio-materials, reducing reliance on imports.

Japan and India's dynamics highlight resource efficiency, with Vietnam's USD 16 billion wood exports incorporating sustainable practices amid rising incomes. Manufacturing hubs in China and Thailand utilize rubberwood for cost-effective, eco-panels, supported by production-linked incentives that cut emissions, positioning the region for rapid expansion through affordable, high-volume supply chains.

Competitive Landscape

The global bio-furnishing market exhibits a moderately consolidated structure, with a few leaders such as IKEA Group and Herman Miller controlling significant shares through vertical integration and sustainable supply chains, while smaller innovators add fragmentation via niche bio-materials. Companies pursue expansion via R&D in recycled plastics and circular models, such as modular designs for reuse, differentiating through certifications like FSC and low-VOC commitments that enhance brand loyalty. Emerging trends include AI-driven customization and B2B partnerships for commercial green procurements, fostering growth in a landscape where top players invest 5-10% of revenues in eco-innovations to capture premium segments and navigate regulatory pressures effectively.

Key Market Developments

- February 2024: Herman Miller updates its iconic Aeron chair with recycled ocean-bound plastic across its entire portfolio, advancing its 50% recycled-content goal by 2030.

- April 2025: Steelcase launches Flex Perch using Cycling technology from electronics waste, marking the first fully recyclable bio-furniture in commercial lines.

- October 2025: IKEA expands its 2030 sustainability strategy with zero-emission deliveries and 100% renewable materials in new bio-furnishing collections.

Top Companies in the Bio-Furnishing Market

IKEA Group (Sweden), a global leader with strong portfolio in affordable sustainable designs, influences the market through circular initiatives like buy-back programs, generating high revenues from FSC-certified bamboo products and driving 2030 net-zero goals via resource regeneration.

Herman Miller, Inc. (USA), renowned for ergonomic innovations, excels in maturity, with 50% recycled-content pledges, leveraging R&D in bio-resins for office furnishings that secure corporate contracts and emphasize durability, contributing to influential eco-leadership.

Steelcase Inc. (USA), dominant in commercial segments, boasts revenue strength from modular systems using reclaimed materials, with FSC-sourced wood and waste-reduction strategies enhancing its portfolio and market position through global sustainability certifications.

Companies Covered in Bio-Furnishing Market

- IKEA Group

- Herman Miller, Inc.

- Steelcase Inc.

- Williams-Sonoma, Inc.

- La-Z-Boy Incorporated

- Greenington Fine Bamboo Furniture

- Vermont Woods Studios

- Cisco Bros. Corp.

- Manchester Woodcraft

- Ashley Furniture Industries, Inc.

- Pottery Barn

- Nitori Co.

Frequently Asked Questions

The Bio-Furnishing Market is valued at US$ 7.1 Bn in 2025 and expected to reach US$ 11.7 Bn by 2032, growing at a 7.3% CAGR, driven by sustainable material adoption.

Key drivers include health concerns from VOC emissions and environmental initiatives such as EPA waste reduction programs, prompting shifts to non-toxic, renewable bio-materials for healthier interiors.

The Residential segment leads with 70% share, as consumers favor eco-friendly furnishings like bamboo beds for sustainable home living, supported by millennial renovation trends.

North America leads, holding over 35% share through US regulations like LEED certifications and innovations in recycled plastics, fostering strong eco-product demand.

Innovations in bio-materials like mycelium offer opportunities in residential applications, reducing carbon by 50% and aligning with circular economy goals for premium growth.

Leading players include IKEA Group, Herman Miller, Inc., and Steelcase Inc., recognized for sustainable initiatives like recycled content pledges and FSC-certified portfolios.