- Technology

- Big Data as a Service (BDaaS) Market

Big Data as a Service (BDaaS) Market Size, Trends, Share, and Growth Forecast, 2025 - 2032

Big Data as a Service (BDaaS) Market by Service Type (Hadoop-as-a-Service (HaaS), Data-as-a-Service (DaaS), Analytics-as-a-Service (AaaS).), Large (20–100 L), and Industrial/Bulk (>100 L)), Deployment Mode (Public Cloud, Hybrid Cloud, Private Cloud.), Organization Size (Small & Medium Enterprises (SMEs), Large Enterprises), End-user, and Regional Analysis for 2025 - 2032

Big Data as a Service (BDaaS) Market Size and Trends Analysis

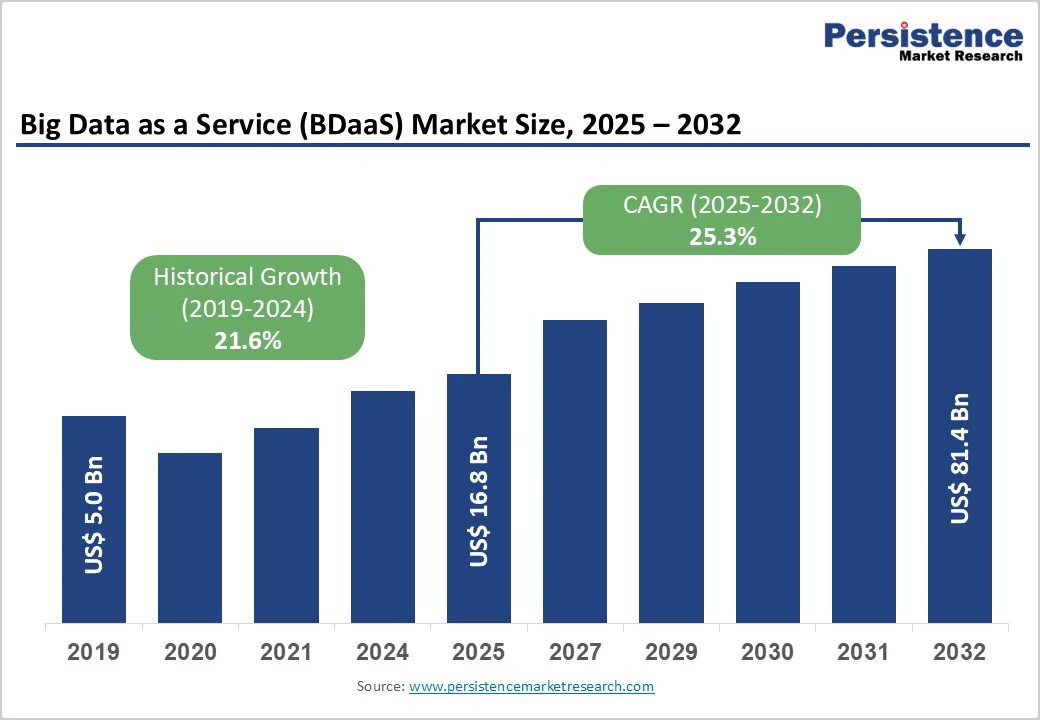

The global big data as a service (BDaaS) market size is valued at US$16.8 billion in 2025 and is projected to reach US$81.4 billion, growing at a CAGR of 25.3% between 2025 and 2032.

This accelerated expansion reflects the convergence of three critical market catalysts: the exponential proliferation of structured and unstructured data generated through IoT infrastructure and digital channels; the widespread organisational adoption of cloud-native architecture enabling real-time analytics capabilities; and the intensifying regulatory mandates requiring sophisticated data governance frameworks. Enterprise organisations are transitioning from capital-intensive on-premises data infrastructure to operationally efficient, scalable cloud-based analytics platforms, fundamentally reshaping data management economics across BFSI, healthcare, retail, and manufacturing sectors.

Key Industry Highlights:

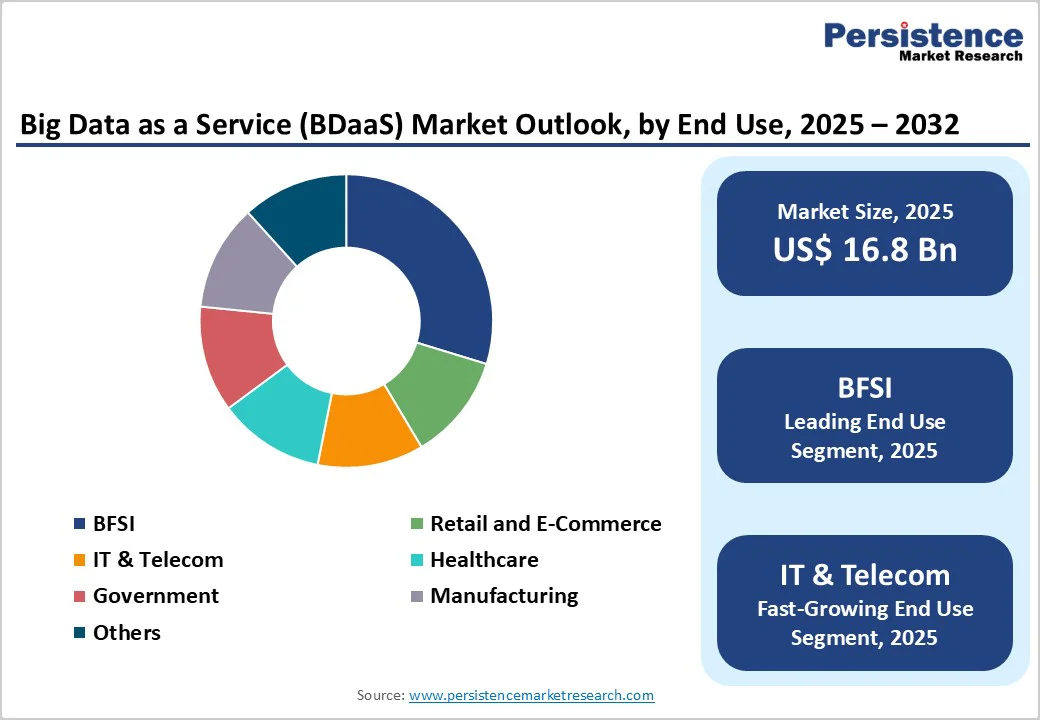

- Analytics-as-a-Service (AaaS) leads the market in 2025, accounting for 53.4% of the global BDaaS share due to widespread adoption across finance, healthcare, and telecom sectors.

- Data-as-a-Service (DaaS) is the fastest-growing segment, driven by real-time access to structured and unstructured datasets for retail and manufacturing applications.

- Public Cloud remains the dominant deployment model with 64.3% market share, offering cost-effective scalability and regulatory compliance for enterprises.

- Hybrid Cloud is the fastest-growing deployment mode, providing flexible, secure, and optimised environments for multinational and regulated organisations.

- BFSI continues to be the largest end-use sector with 28.3% market share, leveraging BDaaS for fraud detection, customer experience, and regulatory reporting.

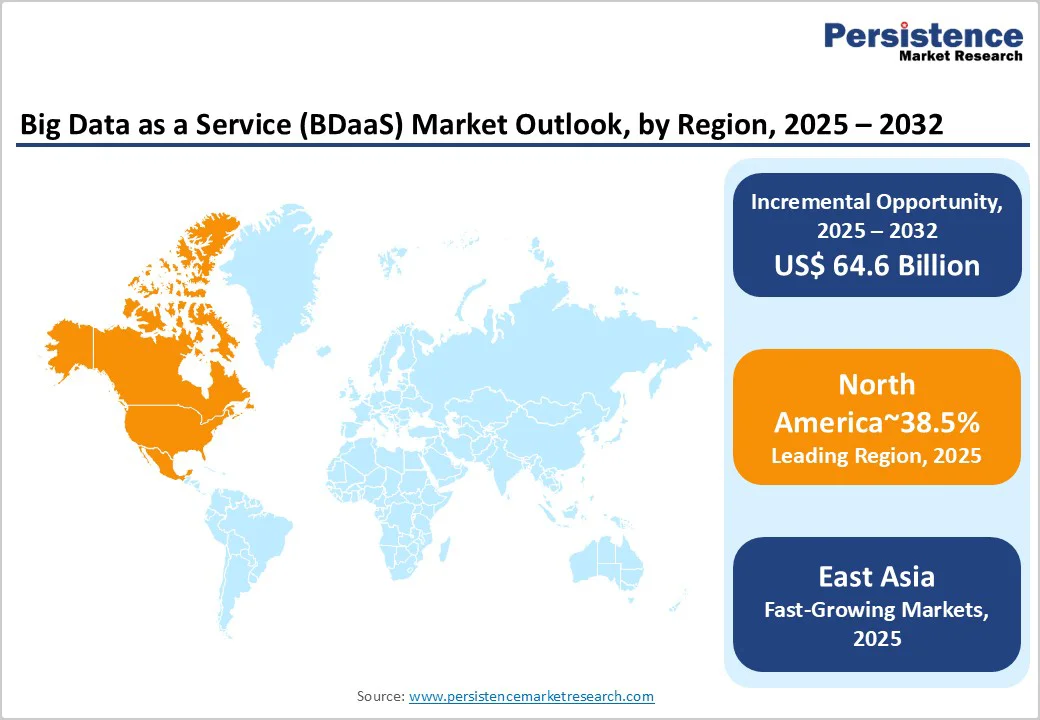

- North America commands the largest regional share at 38.5%, driven by enterprise cloud investments, AI adoption, and regulatory compliance frameworks.

- East Asia and Europe hold 21.3% and 22.5% of the market, respectively, supported by government-led digital transformation, hybrid cloud infrastructure, and strict data governance policies.

| Key Insights | Details |

|---|---|

|

Big Data as a Service (BDaaS) Market Size (2025E) |

US$ 16.8 Bn |

|

Market Value Forecast (2032F) |

US$ 81.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

25.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

21.6% |

Market Dynamics

Drivers - Exponential Data Generation and Digital Transformation Acceleration

The Global Big Data as a Service (BDaaS) Market is fundamentally driven by unprecedented data volume expansion stemming from pervasive IoT deployments, mobile application proliferation, and enterprise digitalization initiatives.

According to industry assessments, connected device installations exceeded 15.1 billion units globally by 2024, generating approximately 120 zettabytes of annual data production. This exponential data proliferation has created an operational imperative for organisations to deploy scalable analytics infrastructure capable of processing heterogeneous data streams in real-time without requiring substantial capital expenditure on physical infrastructure.

Manufacturing enterprises, healthcare institutions, retail organisations, and telecommunications providers face mounting pressure to extract actionable business intelligence from increasingly complex datasets spanning multiple geographic jurisdictions and technology platforms.

The Big Data as a Service (BDaaS) Market addresses this critical capability gap by abstracting infrastructure complexity, enabling organisations to scale analytics operations elastically while maintaining cost predictability through consumption-based pricing models.

Real-world implementation patterns demonstrate that enterprises adopting BDaaS solutions achieve data processing acceleration of 3.5x to 4.2x compared to legacy on-premises data warehousing architectures, directly translating to competitive advantage through accelerated business decision cycles and enhanced operational responsiveness.

Cloud Computing Maturation and Multi-Cloud Architecture Adoption

Cloud computing infrastructure maturation represents the fundamental enabler of BDaaS market expansion, with public cloud service providers Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform collectively commanding 63% of enterprise cloud workload distribution as of 2025. The Global Big Data as a Service (BDaaS) Market has achieved operational viability through the convergence of cloud provider service proliferation, standardised data management interfaces, and proven security compliance certifications spanning GDPR, HIPAA, and SOC 2 Type II frameworks.

Enterprise architecture teams increasingly mandate multi-cloud deployment strategies to minimise vendor lock-in risks, requiring data analytics platforms capable of seamless cross-cloud data mobility and consistent performance optimisation.

The economic model underlying cloud-native BDaaS platforms demonstrates superior total cost of ownership calculations: organisations report 40% to 50% infrastructure cost reductions compared to hybrid data centre models while simultaneously achieving 60% acceleration in analytics query performance through serverless architectures and intelligent query optimisation.

Leading enterprises across financial services, healthcare, and e-commerce sectors have established strategic partnerships with multiple BDaaS providers to ensure operational redundancy while leveraging competitive pricing pressures to achieve sustained infrastructure cost optimisation.

Regulatory Compliance Complexity and Data Governance Imperatives

Regulatory compliance frameworks have evolved into a primary market driver for Global Big Data as a Service (BDaaS) Market adoption, with the California Privacy Rights Act (CPRA), General Data Protection Regulation (GDPR), and emerging sector-specific regulations across healthcare, financial services, and government creating organisational mandates for enterprise-grade data governance infrastructure.

The CPRA enforcement in 2024 introduced "data minimization" requirements obligating organizations to collect and retain only data strictly necessary for specified business purposes, fundamentally reshaping data management methodologies. Non-compliance penalties have escalated dramatically, with organisations facing fines exceeding 4% of annual revenue or €20 million, whichever is greater, incentivizing rapid adoption of centralized, audit-capable analytics platforms.

The Big Data as a Service (BDaaS) market provides built-in compliance automation features, including data lineage tracking, access control auditing, encryption key management, and automated retention policy enforcement capabilities, requiring significant engineering investment when implemented on legacy infrastructure. BFSI institutions and healthcare providers report that BDaaS platform adoption reduced compliance audit preparation time by 65% to 70% while simultaneously reducing regulatory violation risk exposure by enabling real-time compliance monitoring and automated incident reporting capabilities.

Government agencies across North America and Europe have formally mandated BDaaS adoption for citizen data management applications, recognising that cloud-native architectures provide superior privacy protection and audit transparency compared to traditional government data centre operations.

Restraint - Data Security and Privacy Risk Perception Among Legacy Organisations

Despite substantial progress in cloud security maturity, significant organisational segments, particularly government agencies, healthcare institutions, and legacy financial services organisations, maintain structural concerns regarding data security risks associated with third-party cloud infrastructure management.

Organisations managing highly sensitive datasets, including personally identifiable information, genomic data, or national security intelligence, continue requiring on-premises data processing capabilities to satisfy organisational risk governance frameworks and regulatory mandates. Implementation of hybrid BDaaS architectures designed to address these security concerns introduces operational complexity, increased management overhead, and erosion of cost advantages that constitute the primary economic rationale for cloud adoption.

Small and mid-sized organisations lacking dedicated security infrastructure and expertise demonstrate measurable hesitation regarding cloud-based analytics platform adoption, with 34% of SME decision-makers citing security concerns as the primary barrier to BDaaS evaluation.

Legacy organisations required to maintain technical compatibility with decades-old enterprise data systems encounter substantial engineering expenses to establish data integration pathways between existing infrastructure and cloud-based BDaaS platforms, dampening adoption momentum among cost-sensitive operational units.

Opportunities - Healthcare and Life Sciences Precision Analytics Convergence

The healthcare and life sciences industry represents an emerging high-value opportunity domain for Global Big Data as a Service (BDaaS) Market expansion, driven by the convergence of genomic sequencing cost reductions, electronic health record digitalisation, and regulatory mandates requiring evidence-based clinical decision support systems.

Healthcare institutions currently generate approximately 30 petabytes of cumulative data annually through electronic medical records, medical imaging systems, genomic sequencing platforms, and patient monitoring devices.

Precision medicine initiatives, including genetic profiling, biomarker identification, and personalized treatment protocols, require analytics platforms capable of processing multi-modal genomic, proteomics, and phenotype datasets simultaneously, generating computational requirements that fundamentally exceed the capabilities of legacy healthcare IT infrastructure.

The Global Big Data as a Service (BDaaS) Market has emerged as the primary enabler of precision medicine analytics at scale, with leading healthcare systems including Mayo Clinic, Cleveland Clinic, and Mount Sinai Health System deploying enterprise BDaaS implementations to accelerate drug discovery timelines, optimise clinical trial enrollment, and implement predictive analytics for population health management.

Regulatory agencies, including the FDA and EMA, have explicitly endorsed cloud-based analytics platforms for clinical research applications, creating accelerated adoption momentum. Pharmaceutical companies and contract research organisations are competing aggressively to establish clinical trial capability advantages through BDaaS platform investments, with implementation partnerships generating average contract values of $8 million to $15 million across 18-to-24-month engagement cycles.

Healthcare BDaaS implementations demonstrate 2.3x faster time-to-insight compared to legacy data warehouse architectures, enabling healthcare delivery organisations to achieve measurable improvements in patient outcomes and operational cost efficiency.

Government healthcare programs, including the National Institutes of Health and the European Medicines Agency, have allocated substantial research funding to BDaaS platform pilot projects, creating additional expansion vectors for market participants targeting the healthcare vertical.

Artificial Intelligence and Machine Learning Infrastructure Convergence

The integration of Artificial Intelligence (AI) and Machine Learning (ML) capabilities into Global Big Data as a Service (BDaaS) Market platforms represents a substantial value expansion opportunity as organisations recognise that traditional analytics methodologies provide insufficient competitive advantage in digital markets.

Machine learning model training requires substantial computational resources and iterative data experimentation cycles, capabilities that BDaaS platforms provide through elastically scaled compute resources and integrated data pipeline frameworks.

Enterprises deploying AI/ML-driven applications, including fraud detection systems, customer churn prediction models, demand forecasting algorithms, and anomaly detection frameworks, require BDaaS platforms capable of managing model training datasets containing hundreds of millions to billions of training examples, necessitating infrastructure that only cloud-scale providers can practically operate.

The global big data as a service (BDaaS) market has catalysed enterprise AI/ML adoption by reducing the infrastructure complexity, cost barriers, and specialised engineering expertise previously required for machine learning operations. Organisations relying on BDaaS platforms for AI/ML workloads report reducing model development cycles by 50% to 60% compared to organizations managing self-hosted ML infrastructure. Government agencies and enterprise technology leaders have established formal AI/ML competency centres leveraging BDaaS platforms as foundational infrastructure, creating sustained demand for advanced analytics and ML capabilities.

The convergence of generative AI technologies with BDaaS platforms is anticipated to accelerate enterprise adoption substantially through 2026-2027, as organisations recognise that LLM training, fine-tuning, and inference operations require infrastructure capabilities exclusively available within cloud-scale environments.

Category-wise Analysis

Service Type Insights

In 2025, Analytics-as-a-Service (AaaS) constitutes the dominant segment within the BDaaS Market, accounting for53.4% of overall sector share. AaaS enables organisations to access advanced analytical capabilities without the need for in-house infrastructure, supporting a range of enterprise applications from customer behaviour modelling to operational optimisation. Its prominence is attributed to rapid organisational adoption across finance, healthcare, and telecom, reflecting the sector’s commitment to outcome-driven analytics and predictive data science.

Data-as-a-Service (DaaS) emerges as the quickest-growing offering, with robust integration across dynamic business environments. DaaS platforms facilitate real-time access to structured and unstructured datasets, supporting decision-making and regulatory reporting. Industry feedback points to increased adoption by retail and manufacturing sectors aiming to leverage distributed data streams, driving new business models and enhancing competitive agility within the global BDaaS Market landscape.

Deployment Mode Insights

Public Cloud maintains its leadership position, representing 64.3% of the BDaaS Market share in 2025. Public Cloud solutions provide cost-effective scalability, security compliance, and enhanced interoperability for enterprises worldwide, underscored by widespread use in regulated domains such as BFSI and healthcare. The resilience and flexibility of public cloud architecture meet diverse operational requirements, establishing it as the foundational deployment mode for BDaaS providers.

Hybrid Cloud is identified as the fastest-growing deployment mode, reflecting preferences for customised risk management and operational optimisation. Hybrid Cloud BDaaS solutions combine private security controls with public elasticity, offering configurable environments for multinational corporations and regulatory-driven organisations. Strategic alliances and technical advancements within this segment drive accelerated adoption, positioning hybrid cloud as critical to organisational transformation initiatives in the sector.

End-user Insights

The BFSI sector remains at the forefront of BDaaS Market implementation, contributing 28.3% of the overall industry share in 2025. Financial institutions leverage analytics-as-a-service and data-as-a-service to address core challenges in fraud detection, customer experience management, and regulatory reporting. The segment’s adoption trajectory is supported by digital banking initiatives, fintech integration, and government-mandated security protocols.

Retail & E-Commerce exhibits the highest adoption velocity, underpinned by transformative shifts towards data-centric customer engagement, omnichannel distribution, and real-time inventory management. The sector’s investment in analytics platforms enhances personalisation, forecasting accuracy, and supply chain transparency. Case studies from trade associations emphasise the market opportunity for BDaaS providers to deliver tailored solutions serving evolving business needs and regulatory expectations.

Regional Insights and Trends

North America Big Data as a Service (BDaaS) Market Trends

North America commands 38.5% of the global share, driven by sustained investment in enterprise data infrastructure and cloud innovation. U.S. federal agency reports, such as those from the Department of Commerce and the National Institute of Standards and Technology, highlight robust integration of BDaaS platforms into critical sectors, particularly BFSI, healthcare, and government operations. Strategic priorities include digitisation of public services, defence sector modernisation, and implementation of AI-guided analytics engines.

From 2022 through 2025, increased expenditure in public cloud infrastructure and analytics-as-service deployments has generated marked improvements in data-driven service delivery, process optimisation, and regulatory compliance.

North America’s regulatory environment, shaped by data privacy frameworks such as CCPA and HIPAA, reinforces organisational demand for secure, flexible BDaaS solutions. The competitive landscape reflects strong participation by established technology leaders and niche solution vendors, favouring a hybrid market structure with significant opportunities for new entrants. Investment flows continue to target the adoption of emerging technologies, workforce upskilling, and collaborative innovation.

East Asia Big Data as a Service (BDaaS) Market Trends

East Asia accounts for 21.3% of the sector’s global share, supported by government-led digital transformation and enterprise deployment of advanced analytics solutions between 2023 and 2025. Ministries of digital economy and information technology in regional markets, including China, Japan, and South Korea, cite aggressive policy support for cloud adoption and data science initiatives.

Notably, Chinese government directives and Japanese industrial policy documents from 2024-2025 recognise BDaaS as a catalyst for smart manufacturing, e-government, and fintech expansion.

Infrastructure investments in hybrid cloud environments accelerate market access for enterprise clients, with local providers partnering internationally to deliver tailored analytics and compliance solutions. Regulatory emphasis on data sovereignty and cybersecurity underpins East Asia’s market evolution, while active engagement by regional technology platforms and startups introduces innovative service models. The region maintains strong growth potential through investment in education, cross-border technology transfers, and expansion into emerging submarkets.

Europe Big Data as a Service (BDaaS) Market Trends

Europe maintains an industry share of 22.5% (2025), reflecting a highly regulated, innovation-driven BDaaS Market environment. Policy emphasis is placed on data privacy, operational transparency, and cross-border data governance embodied within the GDPR and related digital single market frameworks.

European government funding initiatives from 2022-2025 prioritise integration of analytics-as-a-service into healthcare, manufacturing, and public administration, driving widespread adoption and capacity building.

Performance metrics indicate enhanced enterprise spending on hybrid and public cloud platforms, fostering a competitive blend of global incumbents and domestic solution providers. The region leverages technology partnerships and R&D networks to implement next-generation BDaaS Market capabilities, such as predictive modelling and edge analytics. Investment strategies centre on regulatory compliance automation, digital talent development, and the establishment of cross-border intelligence sharing consortia.

Competitive Landscape

The global big data as a service (BDaaS) market exhibits a moderately consolidated and competitive landscape, dominated by a mix of global tech giants and specialised providers. Leading players such as Amazon Web Services (AWS), Microsoft Corporation, IBM Corporation, Oracle Corporation, SAP SE, and Snowflake Inc. capture significant market share through their extensive cloud platforms, advanced analytics capabilities, and enterprise-grade solutions. These companies leverage strong R&D, global service networks, and strategic partnerships to maintain competitive advantage, while smaller vendors and regional players contribute to market fragmentation at the niche level.

The market’s nature encourages continuous innovation in AI, machine learning, and real-time analytics to differentiate offerings and secure client adoption. Overall, the BDaaS market reflects a competitive yet consolidated environment with high entry barriers due to technology complexity and cloud infrastructure investments.

Key Industry Developments:

- On Nov 18, 2025, Microsoft Corporation: Microsoft announced the general availability of Managed Instance General Purpose "NextGen" and rebranded Azure Cosmos DB for MongoDB as Azure DocumentDB, introducing AI-ready capabilities for vector and hybrid search. These enhancements improve performance, cost predictability, and cross-cloud migration, strengthening Microsoft’s Big Data as a Service (BDaaS) offerings and driving adoption among enterprises seeking scalable, AI-integrated data platforms.

- Jan 11, 2024, Microsoft announced new generative AI and data solutions for retailers via Microsoft Fabric and Azure OpenAI Service, enabling personalized shopping experiences and unified retail data management. These capabilities enhance analytics, support store operations, and help retailers leverage data-driven insights, reflecting the growing role of cloud-based Big Data as a Service (BDaaS) solutions in optimizing customer engagement and operational efficiency globally.

Companies Covered in Big Data as a Service (BDaaS) Market

- Amazon Web Services (AWS)

- Hewlett Packard Enterprise

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- SAP SE

- Wipro Limited

- Snowflake Inc.

- SAS Institute Inc.

- Alteryx Ltd.

Frequently Asked Questions

The global Big Data as a Service (BDaaS) Market is projected to be valued at US$ 16.8 Bn in 2025.

The Analytics-as-a-Service (AaaS) segment is expected to account for approximately 53.4% of the global Big Data as a Service (BDaaS) Market by End-user Industry in 2025.

The big data as a service (BDaaS) market is expected to witness a CAGR of 25.3% from 2025 to 2032.

Exponential data generation from IoT, digital transformation initiatives, cloud computing maturation, multi-cloud adoption, and stringent regulatory compliance are driving the growth of the Global Big Data as a Service (BDaaS) Market.

Expanding adoption in healthcare precision analytics and AI/ML infrastructure integration presents key growth opportunities for the Global Big Data as a Service (BDaaS) Market.