- Advanced Materials

- Bentonite Market

Bentonite Market Size, Share, and Growth Forecast for 2025 - 2032

Bentonite Market by Product Type (Sodium Bentonite, Calcium Bentonite, and Others), Application (Drilling Mud, Foundry Sands, Iron Ore Pelletizing, Cat Litter, and Others), Industry (Oil & Gas, Foundry & Metal Casting, Construction, and Others), Regional Analysis from 2025 to 2032

Bentonite Market Size and Share Analysis

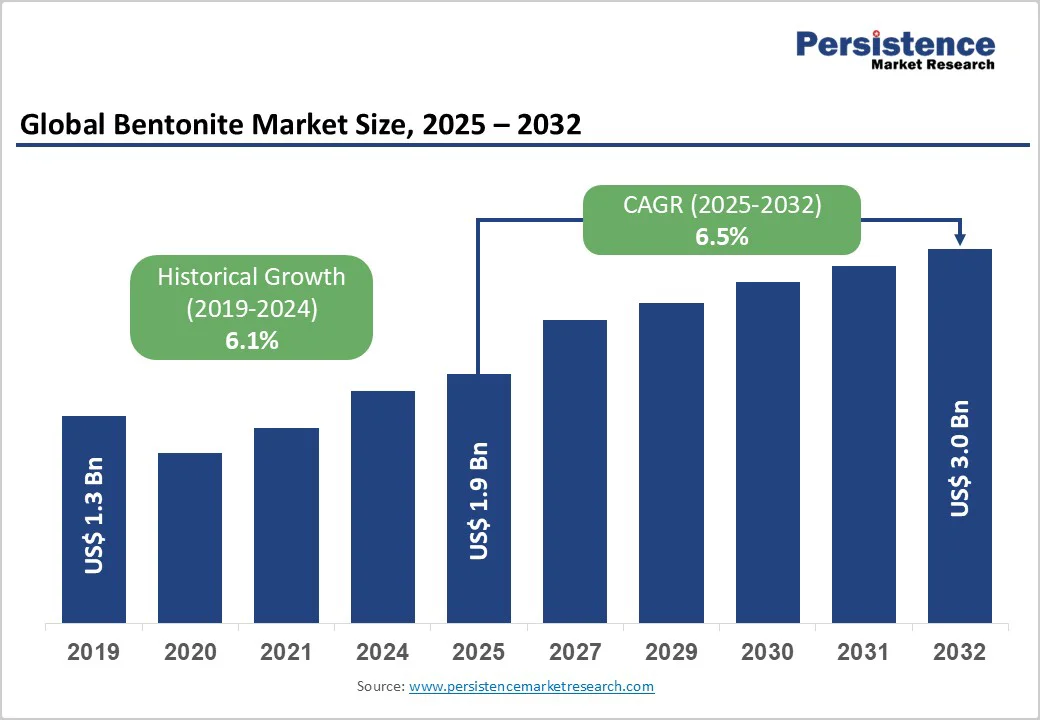

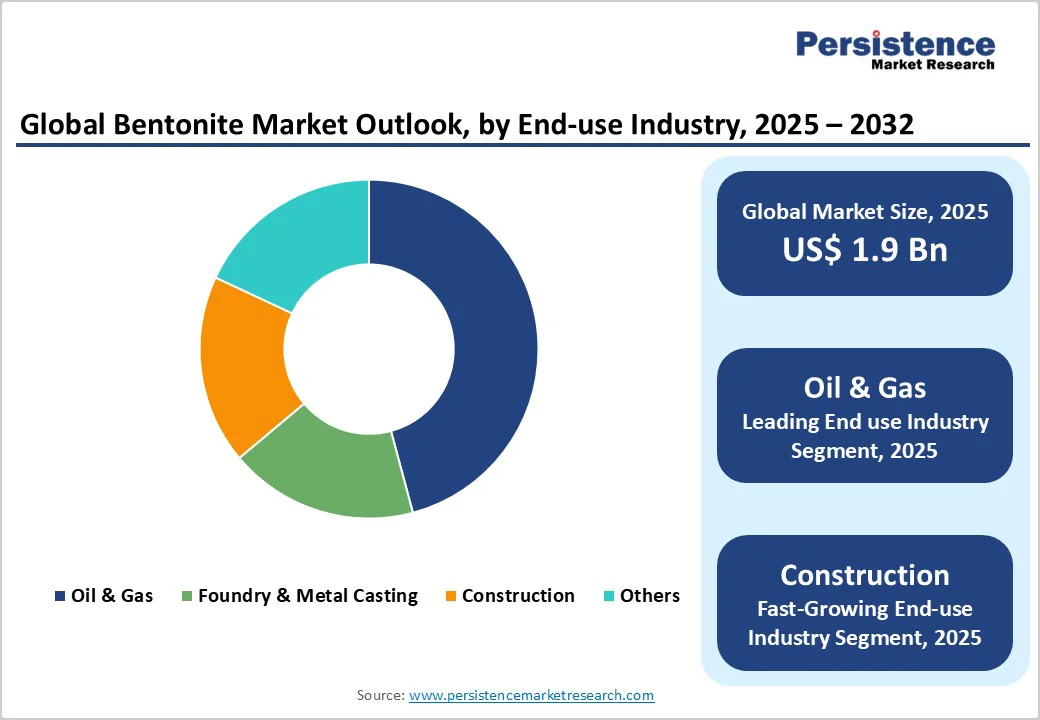

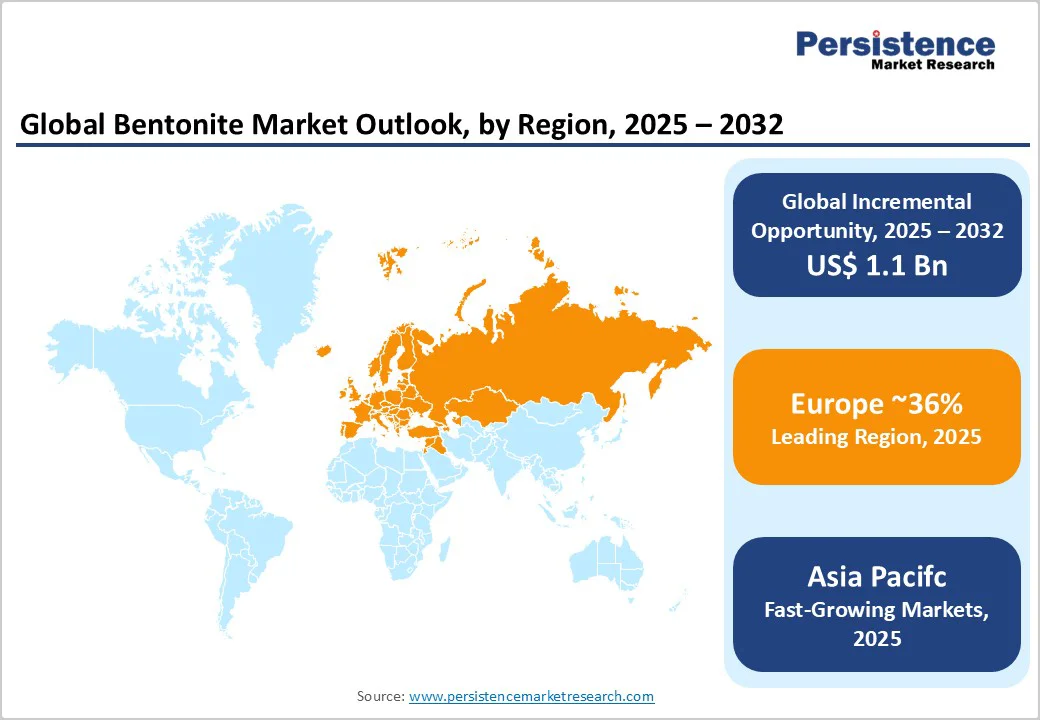

The global bentonite market size is likely to value at US$ 1.9 billion in 2025 and is projected to reach US$ 3.0 billion by 2032, expanding at a CAGR of 6.5% between 2025 and 2032.

The market growth is primarily driven by the rapid industrialization, rising infrastructural projects worldwide, and the growing use of bentonite in iron ore pelletizing and cat litter products.

Key Industry Highlights:

- Regional Leaders: Europe is the leading region, accounting for over 36% of global volume in 2025, driven by robust industrial activity, well-established foundry and construction sectors, and stringent environmental and quality regulations.

- Leading Segments: Sodium Bentonite dominates the market with approximately 60% share in 2025, owing to its superior swelling capacity, water absorption, and thixotropic properties, making it indispensable for drilling mud, foundry sands, and soil stabilization applications.

- Industry Applications: Drilling muds hold the largest application segment, accounting for around 38% share, propelled by rising oil and gas exploration and offshore drilling activities. Foundry sands follow closely, reflecting strong demand for precision metal castings in automotive, heavy machinery, and industrial sectors.

- Industry: The Oil & Gas sector leads the market, supported by sustained exploration in shale and offshore reserves, growing demand for efficient drilling muds, and technological advancements in polymer-enhanced and eco-friendly drilling solutions.

- Market Drivers: Key growth drivers include expansion of global oil & gas drilling projects, growth in foundry and metal casting industries, rising infrastructure development, and increasing applications in cat litter and environmentally friendly construction.

- Market Restraints: Stringent environmental regulations on mining and processing, coupled with high compliance costs and limitations on waste disposal from drilling and foundry operations, are constraining market flexibility and slowing entry for smaller producers.

| Key Insights | Details |

|---|---|

| Bentonite Market Size (2025E) | US$ 1.9 Bn |

| Projected Market Value (2032F) | US$ 3.0 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 6.5% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 6.1% |

Market Dynamics

Driver - Rising Demand from Oil & Gas Drilling Activities is Driving Global Bentonite Market

Bentonite’s critical role in the oil and gas sector, especially as a base component of drilling mud, remains a major growth driver. Sodium bentonite acts as a sealing and lubrication agent, facilitating borehole stability and efficient drilling operations.

Global oil exploration activities and enhanced offshore drilling projects are growing, despite fluctuating crude oil prices, driven by technological advancements in drilling and the need for unconventional resource extraction. U.S. and Middle Eastern investments in shale and deep-water drilling have increased bentonite consumption significantly

In 2025, global oil production is projected to increase by 2.7 million barrels per day (bpd), reaching 105.8 million bpd, with non-OPEC+ countries contributing 1.4 million bpd to this growth. This expansion is driven by significant investments in offshore drilling technologies and unconventional resource extraction. For instance, the U.S. Gulf of Mexico is set to boost offshore oil production, with companies like Chevron aiming to increase output by 50% by 2026.

These developments underscore the growing demand for bentonite in drilling operations, as its properties are crucial for the success of modern drilling techniques. The ongoing expansion and technological advancements in global oil and gas extraction are expected to further propel the demand for bentonite, solidifying its position as an indispensable material in the industry.

Expansion of Foundry and Metal Casting Applications

The foundry and metal casting industry heavily relies on bentonite for its use in foundry sands which require binding and thermal stability. This application holds a significant share of the bentonite market, reflecting its indispensable role in manufacturing castings with precision and dimensional stability.

With the automotive and infrastructure sectors rapidly expanding, especially in countries like China, India, Germany, and the U.S., the demand for high-quality cast metal parts is rising. Bentonite binds sand molds effectively, preventing breakdown during metal pouring and cooling, thereby ensuring higher yield and reduced defects.

The strong growth in heavy machinery, automotive OEMs, and industrial machinery sectors directly fuels foundry bentonite consumption worldwide.

Restraint - Environmental and Regulatory Constraints to Hinder Market Growth

Stringent environmental regulations related to mining, processing, and application of bentonite are creating challenges for market expansion. Many countries have implemented strict guidelines to minimize land degradation, dust emissions, and water pollution linked to bentonite extraction and processing.

Obtaining mining licenses necessitates comprehensive environmental impact assessments, and compliance costs have increased. Additionally, regulations concerning the disposal of spent drilling mud and foundry sands limit excessive waste, prompting companies to invest in treatment or recycling technologies. These restrictions raise operational costs and can cause delays in project start-up, especially for smaller producers or new entrants.

Opportunity - Growth in Bentonite Cat Litter Applications is Creating New Revenue Opportunities

The bentonite cat litter market continues to emerge as a strong opportunity for bentonite suppliers. With increasing pet ownership globally and preference for absorbent, odor-controlling cat litters, bentonite’s superior absorption and clumping properties make it highly desirable.

Growth in disposable pet products, expanding retail channels, and rising awareness about pet hygiene in emerging markets are propelling this segment. Innovations in eco-friendly and dust-free bentonite litter formulations also cater to evolving consumer preferences and strict regulatory mandates for product safety, enhancing market potential.

Advancements in Eco-Friendly Construction and Soil Stabilization

Increasing infrastructure development across developing nations and focus on sustainable construction practices underscore an opportunity for bentonite as a natural, low-impact construction material. Sodium bentonite is widely used for drilling sealants, slurry walls, and ground improvement techniques due to its impermeability and binding strength.

Governments’ emphasis on groundwater protection and erosion control has promoted its use in landfill liners and waste containment systems. Additionally, bentonite’s role in soil stabilization for road base preparation is gaining traction in regions undertaking large-scale road construction, bridging infrastructure expansion with environmental safety demands.

Category-wise Insights

Product Type Analysis

Among the product types, sodium bentonite dominates the market due to its exceptional swelling and water absorption properties, which enable diverse industrial applications. It has a high capability to expand and absorb water several times its dry volume, making it the preferred material for oil and gas drilling fluids, where borehole sealing is vital.

Its use in foundry sands and construction applications similarly capitalizes on these properties for molding and sealing purposes. The reliability and performance of sodium bentonite, coupled with increasing resource extraction from key deposits in the U.S., China, and India, facilitate its market leadership.

Application Analysis

The foundry sands segment holds a significant portion of the bentonite market, accounting for about 28% share. Bentonite’s binding ability ensures compactness and strength of sand molds, which is critical during metal casting.

Increasing demand for automotive components, heavy machinery, and Industrial hydraulic equipment globally escalates foundry output, indirectly accelerating bentonite consumption. Technological refinements in foundry operations and growing adoption of green sand molding techniques, which emphasize natural binders to reduce emissions, further highlight bentonite’s relevance in this application.

Industry Analysis

The oil and gas sector accounts for the largest end-use share, driven by continued exploration and production, especially in shale and offshore reserves. Bentonite’s application as a key component in drilling muds is unparalleled, as it conditions the drilling fluid by enhancing viscosity and lubricating drill bits, minimizing friction and borehole collapse.

This ensures efficient extraction and reduces downtime. With global energy demand rising and unconventional drilling gaining momentum, oilfield bentonite usage is expected to sustain its dominant position, further strengthened by innovations in polymer-enhanced and environmentally-friendly drilling solutions utilizing bentonite.

Regional Insights

North America Bentonite Market Trends

North America remains a crucial market with significant bentonite production, primarily in the U.S., which hosts some of the largest sodium bentonite deposits. The region leads in innovation around bentonite-enhanced drilling fluids for unconventional oil and gas development, including hydraulic fracturing operations. Additionally, regulatory frameworks aimed at environmental protection influence product formulations and mining practices, ensuring sustainable operations.

The mature foundry industry and rising construction activities, especially in infrastructure development and remediation projects, maintain steady bentonite demand. North America’s leadership also lies in adopting advanced processing and quality enhancement technologies to meet stringent industry specifications.

Europe Bentonite Market Trends

In Europe, bentonite is extensively used in foundry operations, construction sealants, and environmental applications such as landfill liners. Germany, France, the U.K., and Spain dominate the regional market, with rising infrastructural investments driving consumption growth. Regulatory harmonization under EU environment directives facilitates the adoption of bentonite as a natural alternative to synthetic binders in various applications.

Additionally, Europe’s increased focus on sustainable construction practices and growing automated foundries incorporates bentonite in advanced mold technologies. Emerging interest in bentonite for environmental remediation, particularly in water purification, enhances regional market dynamics.

Asia Pacific Bentonite Market Trends

Asia Pacific is the fastest-growing bentonite market, driven by industrial expansion and infrastructure projects in China, India, Japan, and ASEAN countries. China leads the regional market fueled by its vast foundry industry, which produces automotive and heavy machinery components extensively.

Expansion in oil and gas exploration, especially offshore fields in Southeast Asia, is another significant bentonite driver. The construction sector’s growth, coupled with governmental focus on sustainable and resilient infrastructure, boosts bentonite demand for slurry walls, soil stabilization, and sealing applications. Lower production costs and increasing mining capacities in mining hubs propel Asia Pacific as a dominant producer and consumer.

Competitive Landscape

The bentonite market exhibits a moderately consolidated structure, with a few large multinational players controlling significant production and distribution capacities, alongside several regional and local producers. Top participants focus on vertical integration, controlling mining, processing, and product formulation, and expanding geographic reach to improve supply chain resilience.

Product innovation, such as the development of specialty bentonites with enhanced purity or tailored particle size distribution, remains a key competitive differentiator. Companies are also investing in environmentally sustainable mining practices and resource recycling to align with regulatory trends. Strategic partnerships and acquisitions in emerging markets further underpin growth strategies.

Recent Industry Developments:

- In March 2025, Ashapura Group, one of the leading producers of bentonite globally, announced the expansion of its sodium bentonite production capacity at its key mining sites in India.The expansion aims to meet the growing domestic and international demand from the oil & gas sector for drilling mud applications, as well as from the foundry industry.

- In June 2025, Bentonite Performance Minerals LLC. inaugurated a state-of-the-art blending and packaging facility in the U.S. Midwest, aimed at diversifying its product portfolio with specialty bentonite blends. The new facility enhances the company's capability to produce tailor-made drilling mud formulations and foundry sands with improved performance characteristics such as higher fluid loss control and better mold strength.

- In September 2025, Clariant AG unveiled a new line of eco-friendly bentonite-based additives designed specifically for the construction industry. These additives improve water retention, enhance viscosity, and provide superior sealing properties crucial for slurry walls and groundwater barriers in civil engineering projects.

Companies Covered in Bentonite Market

- BASF SE

- NanoBioMatters Industries S.L

- RTP Company

- Milliken Chemical

- BioCote Limited

- Microban International

- Clariant AG

- PolyOne Corporation

- Momentive Performance Materials Inc.

- Life Materials Technologies Limited

- SteriTouch Limited

- Sanitized AG

- Dow Inc.

- LyondellBasell Industries Holdings B.V.

- Plastics Color Corporation

- Lonza

Frequently Asked Questions

The global bentonite market is expected to reach US$ 3.0 billion by 2032, up from US$ 1.9 billion in 2025.

Growth is primarily driven by expanding oil and gas drilling activities and increased demand for bentonite in foundry sands due to growth in automotive and industrial manufacturing.

Sodium Bentonite dominates the product segment with approximately 60% market share, favored for its swelling and absorption capabilities.

Asia Pacific leads in production and consumption, supported by rapid industrialization and infrastructure development, particularly in China and India.

Expanding applications in environmentally friendly construction and the growing Bentonite Cat Litter Market present significant opportunities for growth.

Key market players include Ashapura Group, Bentonite Performance Minerals LLC., and Clariant AG, recognized for quality production and extensive geographic reach.