- Technology

- Banking as a Service Market

Banking as a Service Market Size, Share, and Growth Forecast for 2025 - 2032

Banking as a Service Market By Component (Platform, API), Enterprise Size (Small, Large, Medium), End-user (Banking and Financial Institutions, Fintech Companies), and Regional Analysis for 2025 - 2032

Banking as a Service Market Size and Trends Analysis

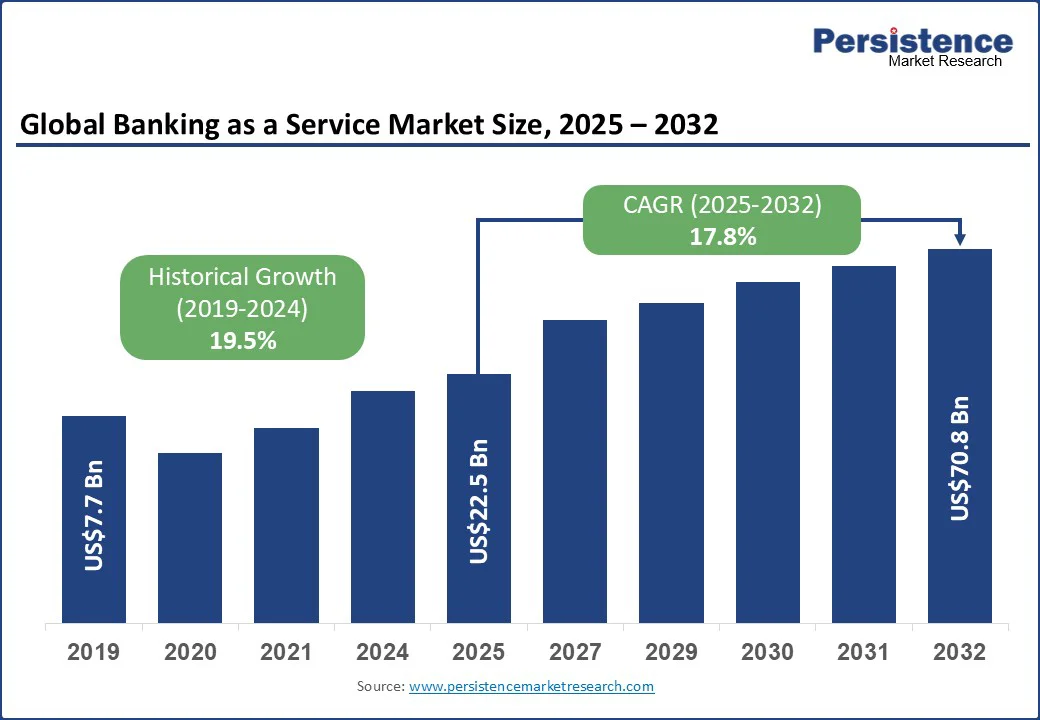

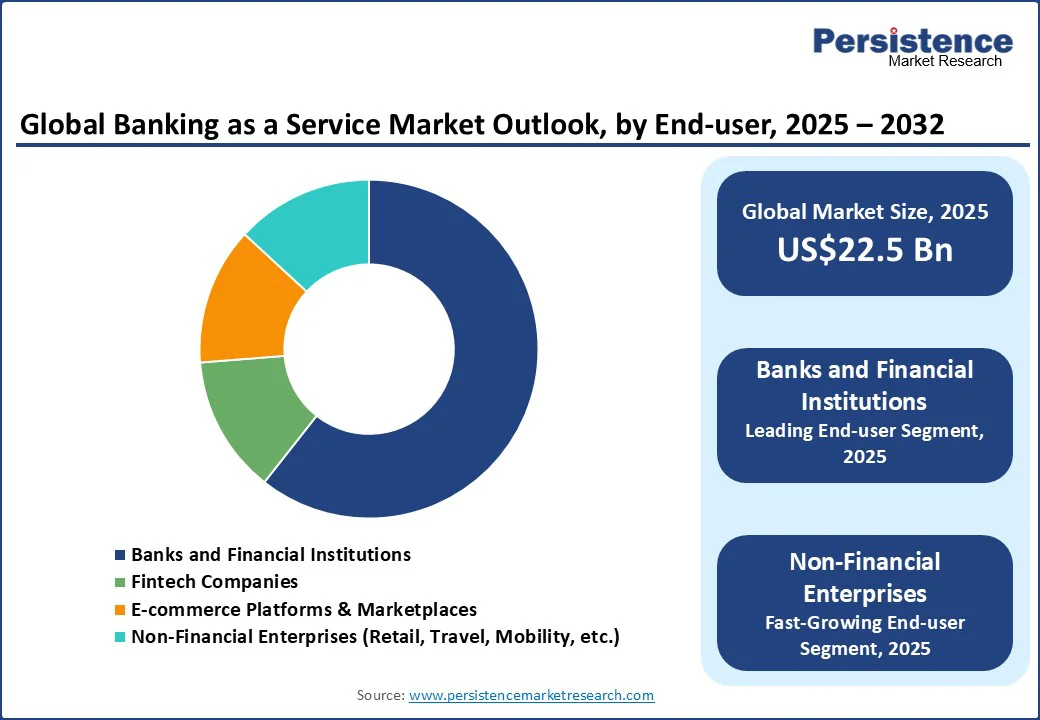

The global banking as a service market size is likely to be valued at US$22.5 Bn in 2025 and is expected to reach US$70.8 Bn by 2032, growing at a CAGR of 17.8% during the forecast period from 2025 to 2032. The rising demand for embedded finance is driving the Banking as a Service (BaaS) market growth. Similarly, the increasing integration of digital payments, lending, and financial services into non-banking platforms is accelerating long-term market adoption.

Key Industry Highlights

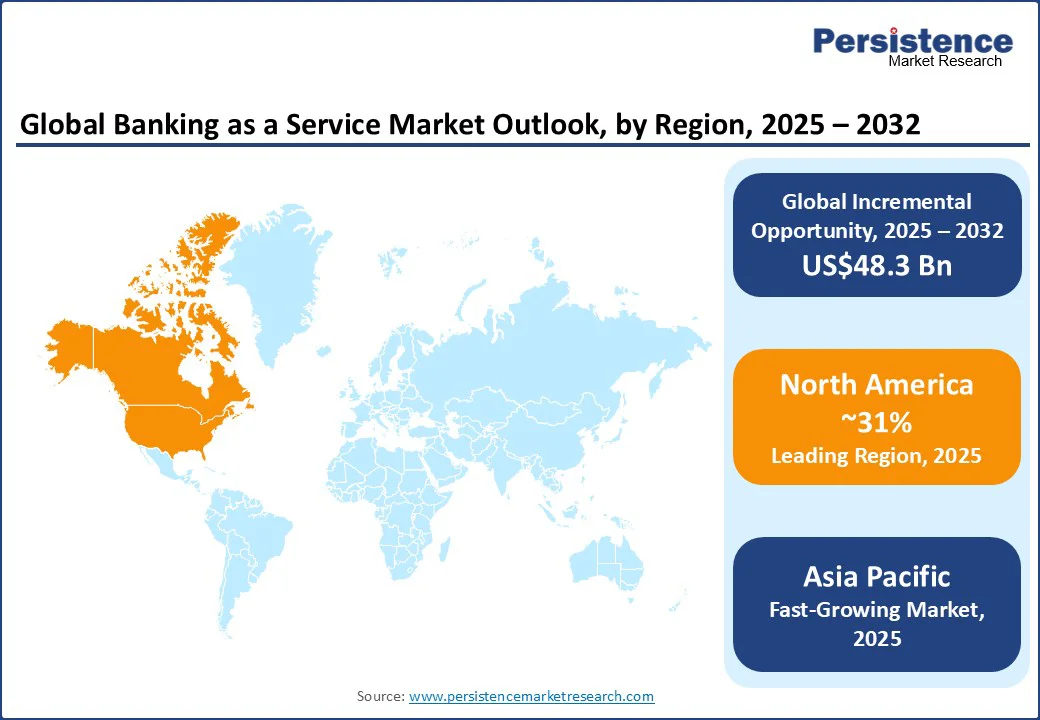

- Leading Region: North America, 31% market share in 2025, driven by strong bank-fintech collaborations, advanced API-driven infrastructure, and regulatory milestones such as Canada’s upcoming open banking framework.

- Fastest-growing Region: Asia Pacific, led by India’s explosive UPI growth with 117.6 billion transactions in 2023 and China’s 64 64 mobile payments market, supported by government-backed financial inclusion and digital currency initiatives.

- Investment Plans: Europe, emerging as a fintech innovation hub, fueled by PSD2, open banking mandates, and a 28% annual rise in fintech adoption, alongside Germany and the U.K. leading BaaS platform integration.

- Dominant Component Type: Platform/API, capturing the largest market share as over 90% of financial institutions adopt APIs, cutting costs by 30% and enabling transactions 50% faster through seamless integration of banking functions.

- Leading End-user: Fintech companies and non-bank enterprises, supported by embedded finance expanding at a 25.5% CAGR, and 96% of sponsor banks engaging in multiple fintech partnerships to meet demand from millennials and Gen Z consumers.

Market Dynamics

Driver - Digital Banking Uptick Accelerates BaaS Adoption

The global rise in digital banking is a major growth engine for the banking-as-a-service market, driven by consumer demand for seamless, mobile-first financial services. According to the World Bank, globally, 79% of adults have an account at a bank or similar financial institution, with a mobile money provider, or both, up from 74% in 2021.

Additionally, 75% of banks have accelerated their digital transformation strategies, while digital banking customer acquisition costs are up to 80% lower than traditional branch methods. With such strong momentum, banks, fintechs, and non-bank firms are increasingly leveraging BaaS platforms to swiftly integrate account services, payments, and lending into their offerings. These platforms provide efficient, API-driven deployment options that help institutions compete effectively in the digital-first economy while expanding user engagement and revenue streams.

Restraint - Cyber Risks and Regulatory Demand Challenge BaaS Expansion

Despite robust growth potential, the BaaS market is constrained by growing cybersecurity threats and a fragmented regulatory environment. In 2023, 94% of IT leaders reported significant cyberattacks, prompting heightened security budgets and compliance demands. BaaS providers operate across multiple jurisdictions, including regions with open banking regulations, such as the EU, and others with stricter licensing rules, resulting in complex compliance hurdles and higher operating costs.

However, the rapid growth of the online payment fraud detection market, growing from US$8 Bn in 2025 to US$20 Bn by 2032 with a 13.8% CAGR, is helping providers counter rising threats by strengthening identity verification, encryption, and fraud monitoring systems. This shift is enabling BaaS companies to build greater resilience, restore enterprise confidence, and mitigate the risks that could otherwise slow adoption and global expansion.

Opportunity - BaaS as a Catalyst for Financial Inclusion

A major opportunity for the Banking-as-a-Service (BaaS) market lies in serving the 1.7 billion unbanked adults worldwide through scalable, mobile-first financial offerings. According to the Global Findex Database 2025, 86% of adults own a mobile phone, with the share of smartphones steadily increasing. Although there are about 5 billion smartphone users globally, nearly one-third of the world’s population remains excluded from formal financial systems.

As the mobile payment transaction market expands, BaaS enables non-bank entities such as mobile networks, retailers, and digital platforms to embed banking functionalities such as digital accounts, payments, and micro-loans without building their own infrastructure. This approach enables rapid and cost-effective onboarding of underserved populations, particularly in emerging markets where digital money usage and mobile penetration are already high.

Category-wise Analysis

Component Insights

The platform/API segment continues to serve as the backbone of the global BaaS market, largely due to its ability to seamlessly integrate core banking functions for fintechs, non-banks, and established financial institutions. Today, over 90% of financial institutions already use or plan to use APIs to unlock new revenue streams from existing customers, while nearly three-quarters are actively pursuing client monetization strategies, reflecting a strong API-first approach.

According to CoinLaw, APIs have reduced operational costs by an average of 30% for financial institutions through automation of repetitive processes, while customers using API-driven platforms benefit from transactions that are 50% faster. Nearly half of the world’s top 100 banks have already made their APIs publicly accessible, with many others preparing to follow.

This transition from internal tools to external revenue-generating platforms underscores why Platform/API services are the most critical growth driver within the evolving API-powered BaaS ecosystem and highlights their rising influence across the broader digital commerce platform market.

End-user Insights

Among end-users, fintech companies and non-bank enterprises such as digital platforms and retailers are emerging as the fastest-growing adopters of the banking-as-a-service model. The embedded banking services market is witnessing robust momentum, fueled by the rapid rise of embedded finance, which is projected to expand at a 25.5% CAGR between 2021 and 2031. At the same time, nearly 96% of sponsor banks are engaged in more than five fintech partnerships, highlighting the ecosystem’s strong reliance on collaborative models.

Consumers, particularly millennials and Gen Z, are increasingly inclined toward brand-driven financial solutions, with over 60% favoring financing options embedded within their favorite platforms over traditional banking channels. This growing preference is also reshaping adjacent sectors such as the buy now pay later market, where seamless integration of credit services enhances customer loyalty, expands access to flexible payments, and drives innovation across industries.

Regional Insights

North America Banking as a Service Market Trends

North America continues to lead the banking-as-a-service market, representing nearly 31% of the global share in 2025. Growth in the region is supported by strong collaboration between traditional banks and fintech firms that are expanding digital banking through advanced platforms. Plaid, for instance, connects over 10,000 U.S. banks to fintech applications such as Venmo and Robinhood, which reflects the region’s strong API-driven infrastructure.

Canada is also expected to implement open banking by 2025, a regulatory milestone that will further accelerate adoption across financial services. In the U.S. private banking market, significant investments in modernization and fintech integration are enhancing digital offerings, while growing consumer demand for embedded finance is driving innovation.

As banks across North America strengthen partnerships and expand digital ecosystems, the region is well-positioned to dominate Banking-as-a-Service deployment and maintain its leadership in digital banking transformation.

Europe Banking as a Service Market Trends

In Europe, the BaaS market is gaining rapid momentum owing to the favorable regulatory framework and fintech-friendly policies such as the revised Payment Services Directive (PSD2) and open banking mandates. Europe has experienced a 28% annual increase in fintech adoption, accompanied by a 35% rise in API-based banking collaborations.

In the U.K., 64% of business decision-makers expect BaaS to reach mainstream usage within five years, demonstrating strong industry confidence. Germany is emerging as a standout market, driven by digital innovations from platforms such as Solarisbank and N26. Collectively, Europe’s regulatory clarity, combined with a mature fintech ecosystem and high digital literacy, makes the region a hotbed for BaaS growth and embedded finance innovation.

Asia Pacific Banking as a Service Market Trends

Asia Pacific is emerging as the global leader in the BaaS ecosystem, strongly influenced by rapid growth in the India fintech market and China’s dominance in digital banking.

According to the National Payments Corporation of India (NPCI), India has emerged as a key driver of digital payments, with UPI transactions surpassing 117.6 billion in 2023, registering 60% annual growth. Data from the Department of Financial Services and the Ministry of Finance show overall digital payment volumes rising from INR 2,071 crore (US$249.5 Mn) in FY 2017–18 to INR 18,737 crore (US$2.26 Bn) in FY 2023–24, reflecting a 44% CAGR, while financial inclusion initiatives such as Jan Dhan Yojana have boosted total deposits in new accounts to over INR 203,505 crore (US$24.52 Bn) by August 2023.

In parallel, China leads the world in mobile transactions, with the People’s Bank of China reporting over US$64 Tn in mobile payment value in 2022. Government-backed initiatives such as the Digital Yuan pilot and large-scale integration of digital wallets are accelerating fintech adoption. Together, India and China, along with advanced markets including Singapore and Japan, position Asia Pacific as the fastest-growing hub for embedded finance and BaaS platforms.

Competitive Landscape

The global Banking as a Service market is highly competitive, with key players such as Solaris SE, Mambu, Fidor Solutions, Green Dot Corporation, and Temenos AG focusing on strategic developments such as partnerships, acquisitions, and new product launches. For instance, Solarisbank has expanded its API-based platform across Europe through strategic collaborations with fintechs, while Mambu has been scaling its SaaS banking engine globally to strengthen its market position.

Companies are also investing in cloud-native infrastructure, AI integration, and regulatory compliance solutions to enhance platform efficiency and customer experience. For example, Temenos is advancing its AI-driven BaaS offerings to support embedded finance, while Green Dot has focused on expanding its banking partnerships with leading retailers and digital platforms. These strategies not only strengthen their global presence but also set benchmarks for scalability, compliance, and digital banking innovation, shaping future industry standards.

Key Industry Developments

- In April 2024, Mambu partnered with Visa to accelerate embedded finance solutions, enabling fintechs and traditional banks to launch innovative digital banking services faster.

- In September 2024, Solaris SE acquired Contis, strengthening its European footprint and expanding its BaaS offerings across payments and lending.

- In January 2025, Fidor Solutions announced a strategic collaboration with Microsoft Azure to enhance cloud-native BaaS solutions with advanced AI-driven compliance and fraud detection capabilities.

Companies Covered in Banking as a Service Market

- Solaris SE

- Treezor (a subsidiary of Société Générale)

- Railsr

- Sopra Banking Software

- Clearbank Ltd

- Technisys

- Marqeta, Inc.

- Bankable

- ClearBank

- Green Dot Corporation

- Treasury Prime

- Unit Finance

- SynapseFI

- Fidor Bank

- Starling Bank

- Mambu

- Q2 Holdings, Inc.

- Mbanq

- Cambr

- Galileo Financial Technologies

- Banxware

Frequently Asked Questions

The global banking-as-a-service market is projected to grow from US$22.5 Bn in 2025 to US$70.8 Bn by 2032, registering a strong CAGR of 17.8% during the forecast period.

The rapid rise in digital banking adoption, increasing demand for embedded finance, and the integration of digital payments, lending, and financial services into non-banking platforms are the key growth drivers of the global BaaS market.

The BaaS market faces challenges such as cybersecurity threats, online payment fraud risks, and complex regulatory requirements across multiple jurisdictions, which increase compliance costs for providers.

North America currently leads the BaaS market with around 31% of the market share in 2025, while Asia-Pacific is emerging as the fastest-growing region, driven by India’s fintech boom and China’s dominance in digital payments.

BaaS providers have huge opportunities in financial inclusion, with the potential to serve 1.7 billion unbanked adults worldwide through mobile-first digital banking, micro-lending, and embedded financial services.