- Non-food Packaging

- Bamboo Packaging Market

Bamboo Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Bamboo Packaging Market by Product Types (Boxes, Trays, Others), End-user (Food & Beverages, Cosmetics & Personal Care, Others), Packaging Forms, and Regional Analysis for 2026 - 2033

Bamboo Packaging Market Size and Trends Analysis

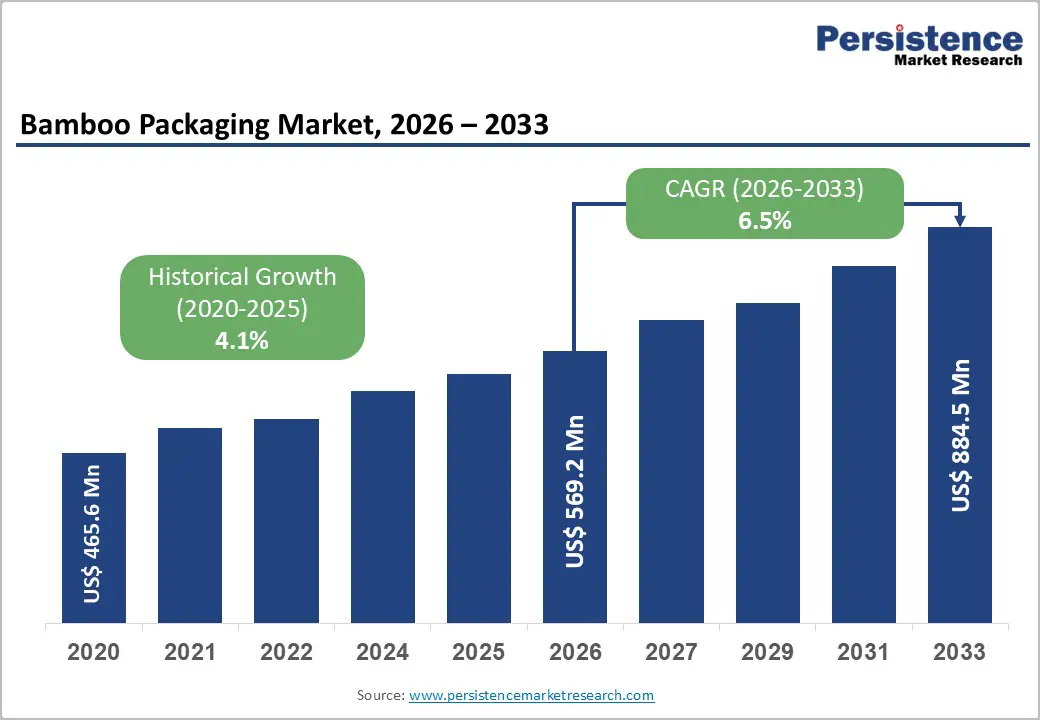

The global bamboo packaging market size is likely to be valued at US$ 569.2 million in 2026 and is expected to reach US$ 884.5 million by 2033, growing at a CAGR of 6.5% between 2026 and 2033, driven by the accelerating substitution of plastic-based packaging with renewable fiber alternatives across food and beverage, cosmetics, electronics, and select industrial applications.

Regulatory bans on single-use plastics, corporate net-zero commitments, and procurement mandates for low-impact materials are shifting purchasing behavior toward bamboo-based formats. Falling conversion costs, scale-up of bamboo pulp processing, and innovation in molded fiber and water-based barrier coatings are expanding functional use cases. Asia Pacific supply-side expansion and maturing downstream converting capacity underpin the sustained mid- to high-single-digit growth trajectory through 2033.

Key Industry Highlights

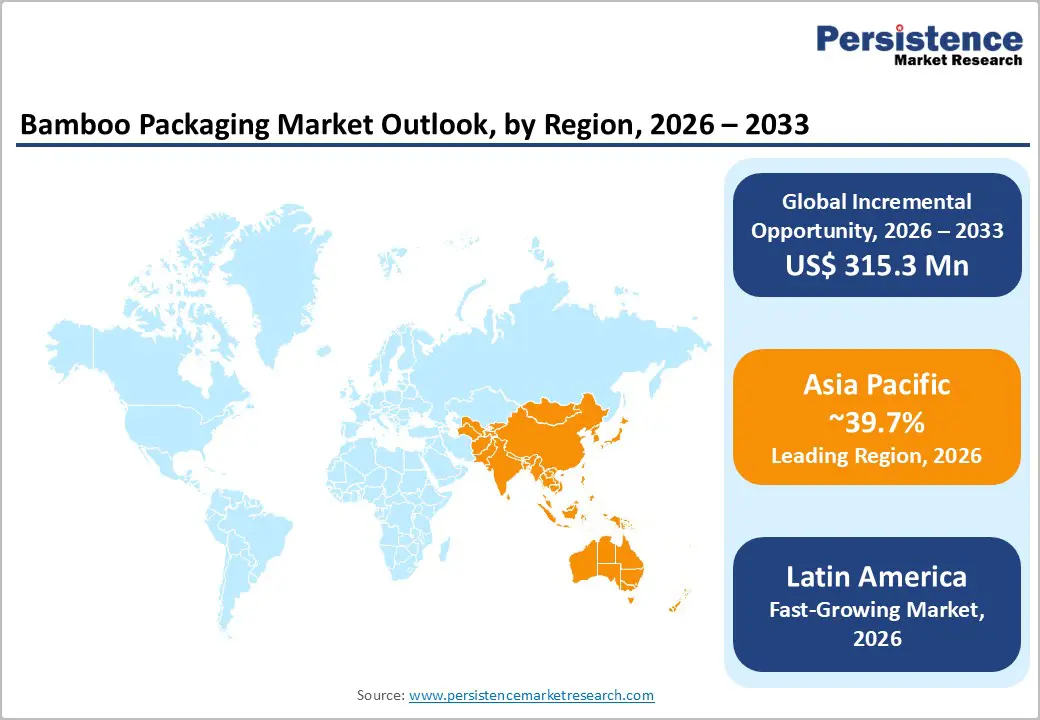

- Leading Region: Asia Pacific is projected to hold approximately 39.7% of market share, supported by abundant raw material availability, vertically integrated supply chains, and strong export-oriented converting capacity led by China and India.

- Fastest-growing Region: Latin America is projected to be the fastest-growing region, supported by expanding bamboo cultivation in Brazil and Colombia, increasing export demand from North America, and policy-backed rural development programs promoting bamboo-based value chains.

- Investment Plans: Ongoing investments focus on mechanical and chemical pulp capacity expansion, water-based barrier coating technologies, and supply-chain localization initiatives. Several regional converters in Asia Pacific and North America are expanding molded fiber production lines to support the anticipated 6.5% CAGR through 2033.

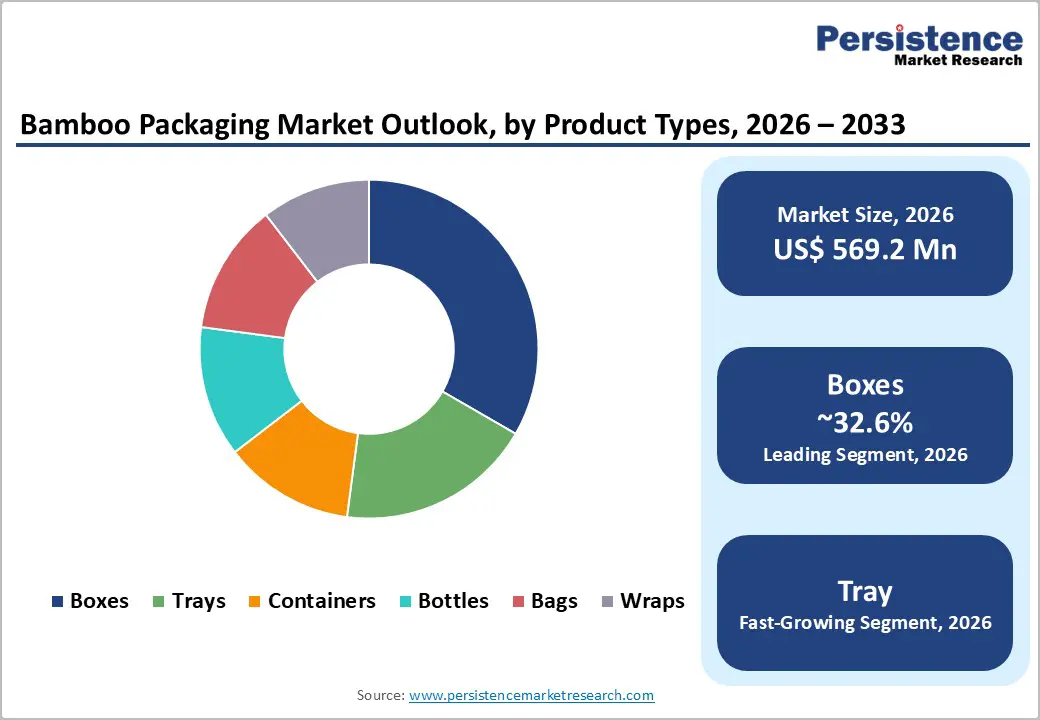

- Dominant Product Types: Boxes are anticipated to account for approximately 32.6% of market share, maintaining leadership due to versatility across cosmetics, electronics, retail, and food packaging applications.

- Leading End-user: The food and beverages segment is estimated to represent around 33.7% of the market share, driven by regulatory substitution of single-use plastics and high-volume procurement from quick-service restaurants and packaged food brands.

| Key Insights | Details |

|---|---|

| Bamboo Packaging Market Size (2026E) | US$569.2 Mn |

| Market Value Forecast (2033F) | US$884.5 Mn |

| Projected Growth (CAGR 2026 to 2033) | 6.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Substitution and Policy Acceleration

Global regulatory frameworks targeting single-use plastics are materially increasing demand for biodegradable and recyclable packaging solutions. Extended producer responsibility schemes, plastic bans in foodservice packaging, and mandated recycling targets across Europe, parts of North America, and Asia Pacific are converting sustainability preferences into procurement requirements. These regulations elevate demand for tree-free fiber materials that demonstrate favorable life-cycle emissions and compostability profiles. Bamboo packaging aligns with these requirements by offering rapid renewability and reduced land-use pressure compared with wood pulp. As compliance costs for plastics rise, bamboo-based formats gain structural cost competitiveness in regulated packaging categories.

Material Performance Improvements and Processing Scale

Technological advancements in bamboo fiber processing are expanding the functional performance envelope of bamboo packaging. Improvements in mechanical pulping, thermoforming, and fiber refining have enhanced tensile strength, dimensional stability, and surface smoothness. Water-based barrier coatings now deliver improved moisture and grease resistance without compromising compostability. Scale investments in bamboo pulp capacity and downstream converting are lowering unit costs and improving consistency. These developments support adoption in packaging segments such as electronics, cosmetics, and premium food applications, where durability and appearance are critical. Commercial-scale production has increased since 2024, moving bamboo packaging from pilot-stage validation into mainstream deployment.

Brand and Consumer Alignment with Circular Materials

Brand sustainability strategies increasingly prioritize packaging materials with verifiable circular credentials. Bamboo packaging offers both functional sustainability and visible differentiation, supporting brand equity in premium categories. Consumer research consistently indicates willingness to pay modest premiums for packaging that demonstrates environmental responsibility, particularly in cosmetics and specialty foods. Corporate commitments to reduce scope-3 emissions further reinforce demand for low-impact materials. High-profile adoption by multinational electronics and consumer brands has validated bamboo packaging at scale, accelerating confidence across adjacent sectors and shortening procurement decision cycles.

Barrier Analysis - Cost Structure and Supply Variability

Despite high yield per hectare, bamboo supply chains remain regionally concentrated, creating exposure to localized harvest cycles, logistics constraints, and price volatility. Conversion from existing paper or plastic lines requires capital investment and technical adjustments, raising near-term costs. In high-performance applications, bamboo pulp solutions can carry cost premiums of approximately 5-20% compared with recycled paperboard, depending on scale and specification. These factors limit adoption in highly price-sensitive packaging segments and slow penetration outside premium or regulated use cases.

Compliance Complexity and End-Of-Life Limitations

Food-contact compliance, compostability certification, and regional end-of-life infrastructure present technical and regulatory challenges. Bamboo packaging intended for primary food use requires barrier treatments and curing processes that must meet stringent safety standards. In regions lacking industrial composting or fiber recovery infrastructure, environmental claims are harder to substantiate, weakening value propositions. Certification timelines and testing costs increase time-to-market, particularly for smaller converters with limited regulatory resources.

Opportunity Analysis - Premium Cosmetics and Personal Care Packaging

Cosmetics and personal care represent a high-margin opportunity where material aesthetics and sustainability credentials directly influence purchasing decisions. Bamboo packaging supports clean-beauty positioning, refill-ready systems, and premium shelf presence. Even modest shifts in packaging spend toward sustainable materials in premium beauty markets can translate into meaningful incremental revenue. Bamboo jars, closures, and secondary cartons are increasingly used to signal authenticity and environmental responsibility, creating scalable demand in high-value segments.

Consumer Electronics Packaging

Electronics manufacturers seek durable packaging that reduces plastic content without compromising protection. Bamboo molded pulp inserts, rigid presentation boxes, and secondary packaging formats are demonstrating technical viability. Electronics packaging carries a higher per-unit spend, allowing bamboo solutions to absorb material premiums. Early adoption by large OEMs establishes reference cases that de-risk broader category adoption. Incremental substitution within electronics packaging can contribute disproportionately to revenue growth.

Asia Pacific Capacity Expansion and Localization

Asia Pacific offers structural advantages through abundant bamboo resources, established processing expertise, and proximity to major consumer markets. Vertical integration across cultivation, pulping, and converting reduces logistics costs and enhances pricing competitiveness. With continued investment in quality control and barrier technologies, the region is positioned to capture over 39.7% of global bamboo packaging value. Government-backed bamboo commercialization programs further support expansion and export competitiveness.

Category-wise Analysis

Product Types Insights

Boxes are anticipated to account for approximately 32.6% of market share in 2026, due to their versatility across both primary and secondary packaging applications. They are widely used in cosmetics, consumer electronics, retail gift packaging, and dry food products where structural rigidity and branding surface area are critical. Bamboo-based boxes leverage converting processes adapted from conventional paperboard manufacturing, allowing manufacturers to integrate bamboo pulp with minimal disruption to established die-cutting and folding operations. In premium cosmetics, bamboo presentation boxes enhance shelf differentiation and align with clean-label positioning. In consumer electronics, rigid bamboo cartons are increasingly replacing laminated plastic board to reduce plastic content while maintaining protective strength. Their compatibility with existing automated filling lines, high-quality printability, and durability during transport sustain their dominant market position. As brands prioritize scalable, sustainable formats, boxes remain the most commercially deployable bamboo packaging solution.

Trays are anticipated to record the fastest growth rate during the forecast period, supported by structural demand in foodservice and e-commerce logistics. The expansion of ready-to-eat meals, takeaway services, and meal-kit delivery models increases per-order packaging intensity, directly benefiting molded bamboo trays. Thermoformed bamboo trays provide adequate compressive strength, heat tolerance, and grease resistance, meeting performance standards for quick-service restaurants and supermarket deli sections. Urban markets with single-use plastic bans are accelerating tray substitution, particularly in regions enforcing compostable or fiber-based food-contact packaging. For example, bamboo trays are being adopted in airline catering and institutional dining where compostability supports corporate sustainability targets. E-commerce grocery platforms also use bamboo trays for fresh produce packaging to reduce plastic punnets. These diversified applications underpin trays’ superior growth momentum compared with more mature box formats.

End-user Insights

Food and beverage applications dominate, anticipated to hold approximately 33.7% of market share in 2026, due to regulatory pressure on plastic packaging and consistently high consumption volumes. Government-imposed restrictions on single-use plastics in foodservice, coupled with extended producer responsibility frameworks, are compelling restaurants, food manufacturers, and retailers to adopt fiber-based alternatives. Bamboo packaging supports regulatory compliance while aligning with consumer preferences for biodegradable and compostable materials. Quick-service restaurant chains and food delivery platforms represent major procurement drivers, particularly for trays, clamshell boxes, and takeaway containers. Supermarkets are also incorporating bamboo-based produce packaging and bakery cartons to reduce plastic intensity in fresh food aisles. High-volume usage and recurring replenishment cycles ensure steady demand, making food and beverage the structural anchor segment of the bamboo packaging market.

Cosmetics and personal care are projected to expand at the fastest rate during the forecast period, driven by clean-beauty positioning and premium sustainability narratives. Packaging in this sector plays a central role in brand perception, allowing bamboo materials to serve both functional and marketing purposes. Bamboo jars, compacts, outer cartons, and caps are increasingly used for skincare, haircare, and fragrance products. Premium beauty brands are integrating bamboo packaging into refillable systems, reducing lifecycle material intensity while reinforcing environmental claims. The higher packaging value per unit in cosmetics, compared with food packaging, accelerates revenue growth once adoption scales. As consumer scrutiny of ingredient sourcing extends to packaging materials, bamboo’s renewable and natural origin strengthens its competitive position within high-margin personal care segments.

Regional Insights

North America Bamboo Packaging Market Trends - Regulation-Driven Adoption and Premium Brand Integration

North America represents a structurally expanding demand market for bamboo packaging, driven by regulatory tightening, corporate sustainability mandates, and premium consumer positioning. The U.S. leads regional demand due to high per-capita packaging consumption and binding state-level plastic reduction measures. States such as California, New York, and Washington have enacted extended producer responsibility legislation and restrictions on single-use plastics in foodservice, directly accelerating the shift toward compostable fiber-based alternatives. These regulatory developments create procurement certainty for bamboo packaging suppliers.

Corporate adoption further strengthens market momentum. Large consumer goods companies operating in the U.S. market have publicly committed to reducing virgin plastic use and increasing renewable material content in packaging portfolios. Electronics brands such as Dell Technologies have expanded the use of molded fiber packaging across product lines, replacing foam-based inserts with renewable fiber materials, including bamboo blends. This move has influenced supplier ecosystems and validated fiber performance in protective packaging applications. In cosmetics, brands such as Estée Lauder and Aveda have incorporated bamboo components into secondary packaging and closures to reinforce sustainability narratives, stimulating demand for higher-grade bamboo pulp formats.

Investment activity in North America increasingly centers on local converting capacity and advanced barrier technologies. Packaging converters are investing in water-based coatings to meet food-contact standards while preserving compostability. Supply-chain localization has gained strategic importance as companies seek to reduce reliance on imported molded fiber components from Asia. These developments collectively enhance technical capability within the region, positioning North America as a high-value consumption market with growing domestic processing capacity.

Latin America Bamboo Packaging Market Trends - Feedstock-Led Growth Supported by Policy and Export Demand

Latin America is expected to be the fastest-growing region for bamboo packaging, combining upstream resource availability with expanding sustainability policy frameworks. Countries such as Brazil, Colombia, and Ecuador possess substantial native bamboo resources, particularly Guadua species, which are increasingly commercialized for industrial applications. Government-supported rural development initiatives in Colombia have promoted bamboo cultivation as both an environmental restoration tool and an economic diversification strategy, strengthening feedstock availability for packaging applications.

Brazil has advanced waste management and packaging recovery regulations under its National Solid Waste Policy, encouraging companies to integrate recyclable and biodegradable materials into packaging portfolios. This policy environment creates favorable conditions for bamboo packaging substitution, particularly in foodservice and retail. Regional exporters also benefit from demand in North America and Europe, where buyers seek certified sustainable materials with traceable supply chains.

Private sector developments are reinforcing regional capabilities. Latin American packaging manufacturers are partnering with agricultural cooperatives to secure bamboo feedstock and integrate pulping operations closer to cultivation zones. This vertical alignment reduces raw material volatility and enhances export competitiveness. However, scaling remains dependent on harmonizing food-contact compliance standards with international requirements. Investments in testing laboratories and certification processes are gradually strengthening the region’s credibility in higher-value packaging categories, positioning Latin America as both a supply base and an emerging domestic consumption market.

Asia Pacific Bamboo Packaging Market Trends - Resource Abundance and Vertically Integrated Production Leadership

Asia Pacific is estimated to be the leading region in the bamboo packaging market, holding approximately 39.7% of global market share in 2026. The region’s leadership stems from abundant bamboo resources, established processing expertise, integrated manufacturing ecosystems, and strong domestic consumption growth. China and India dominate upstream bamboo cultivation and pulp processing, while Japan and several ASEAN economies focus on high-value converting and premium packaging applications. China maintains the world’s largest bamboo resource base and has implemented national strategies promoting bamboo as a sustainable industrial material.

Government-backed initiatives supporting bamboo industrialization have accelerated investment in pulping, fiber molding, and export-oriented packaging production. Chinese molded fiber manufacturers supply global electronics and consumer goods brands, reinforcing Asia Pacific’s role as a production hub. India has similarly expanded bamboo commercialization through national missions focused on increasing cultivated area and improving value-chain efficiency. Indian packaging firms are integrating bamboo pulp into foodservice containers and retail cartons to comply with domestic single-use plastic restrictions implemented across multiple states. These regulatory measures have stimulated rapid substitution in quick-service restaurant packaging and institutional catering sectors.

Japan represents a premium innovation center within the region. Companies such as Muji have introduced packaging formats incorporating natural fiber materials to align with minimalistic and sustainability-focused brand positioning. ASEAN countries, including Vietnam and Thailand, are scaling bamboo processing capacity to serve both domestic foodservice markets and export demand. The region’s vertically integrated supply chains provide cost advantages and reduce lead times, reinforcing Asia Pacific’s structural dominance. Increasing domestic demand for sustainable packaging in urban centers supports internal market expansion, balancing export dependency. Continued investment in mechanical and chemical pulp refinement technologies is expected to further enhance product quality and global competitiveness.

Competitive Landscape

The global bamboo packaging market is moderately fragmented, comprising specialist bamboo converters, diversified packaging groups, and regional suppliers. Competition centers on scale, certification, and the ability to meet multinational brand requirements. Consolidation is increasing as larger players acquire fiber capabilities and integrate bamboo into broader packaging portfolios.

Key strategies include vertical integration, premium positioning in cosmetics and electronics, and cost leadership through scale in Asia Pacific. Differentiation is achieved through certification, co-development with brand owners, and innovation in barrier performance.

Key Industry Developments:

- In August 2025, Earthmade introduced Bamboo-O, a patented, eco-friendly material made from bamboo fiber and plant starch, with applications including rigid coffee packaging (Aromabox) and sustainable cups (Aromacup) at the Responsible Packaging Expo 2025.

- In September 2025, G-COVE Group debuted its pure plant-based bamboo fiber packaging series at the World Manufacturing Conference, featuring microwave-heatable tableware, oil-proof containers, and cushioning/outer packaging for electronics, all made from bamboo and agricultural waste.

Companies Covered in Bamboo Packaging Market

- Smurfit Kappa Group

- International Paper Company

- Amcor plc

- WestRock Company

- DS Smith plc

- Stora Enso Oyj

- Mondi plc

- Huhtamaki Oyj

- ProAmpac

- Sonoco Products Company

- Billerud AB

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Georgia-Pacific LLC

- Nine Dragons Paper Holdings Limited

- MOSO International B.V.

- Bambrew

- EcoPlanet Bamboo

Frequently Asked Questions

The global bamboo packaging market size is anticipated to be US$569.2 million in 2026.

The bamboo packaging market is expected to reach US$884.5 million by 2033.

Key trends include regulatory substitution of plastics, rising demand for sustainable and biodegradable materials, adoption of bamboo packaging in electronics and premium cosmetics, growth in e-commerce and foodservice applications, and technological innovations in pulp processing and water-based barrier coatings.

Boxes are the leading product type, accounting for approximately 32.6% of market share, due to their versatility across food, cosmetics, electronics, and retail applications.

The market is projected to grow at a CAGR of 6.5% between 2026 and 2033.

Major players include Smurfit Kappa, International Paper, Amcor, ProAmpac, and Moso International.