- Home Appliances

- Bamboo and Bamboo Products Market

Bamboo and Bamboo Products Market Size, Share, and Growth Forecast 2026 - 2033

Bamboo and Bamboo Products Market by Product Type (Raw Bamboo, Engineered Bamboo Products, Bamboo Furniture, Bamboo Construction Materials, Bamboo Household & Lifestyle Products, Bamboo Textile & Fiber Products, Bamboo Packaging Products, Bamboo Charcoal & Energy Products, Bamboo Handicrafts), Processing Type, Distribution Channel, End-Use, by Regional Analysis, 2026 - 2033

Bamboo and Bamboo Products Market Size and Trend Analysis

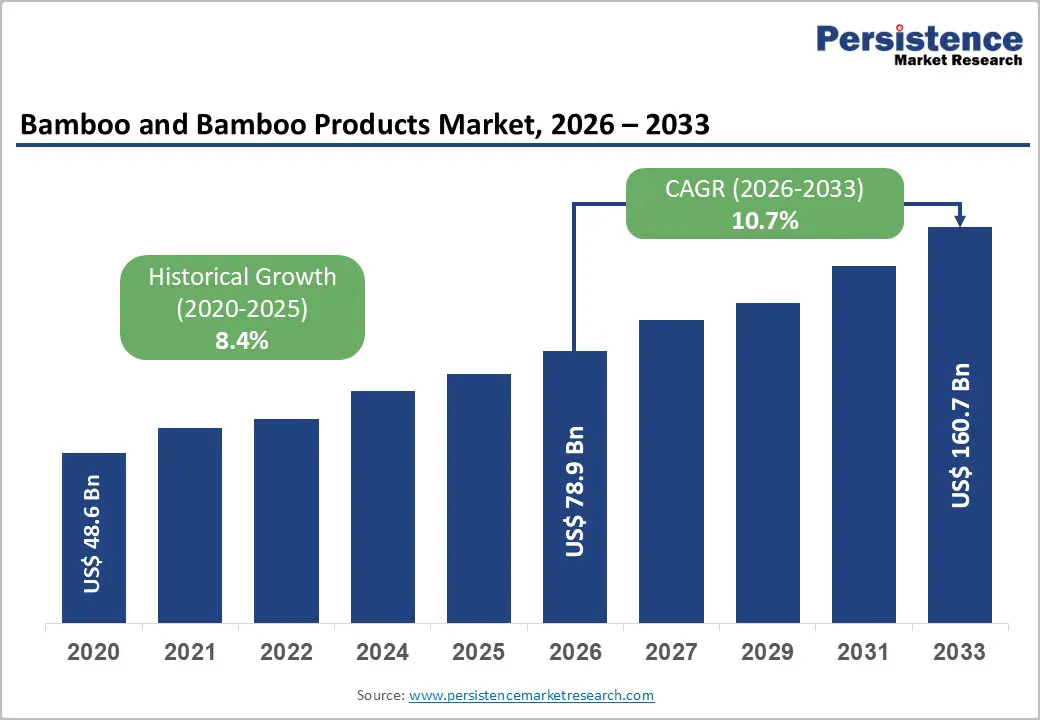

The global bamboo and bamboo products market size is likely to be valued at US$ 78.9 Billion in 2026 and is expected to reach US$ 160.7 Billion by 2033, growing at a CAGR of 10.7% during the forecast period from 2026 to 2033.

The market's exceptional and accelerating growth trajectory is rooted in the global economy's structural pivot toward sustainable, renewable, and low-carbon materials, where bamboo's unique combination of rapid regeneration, exceptional mechanical strength, and multi-sectoral applicability positions it as the preeminent natural material of the 21st century's green industrial revolution.

Key Industry Highlights:

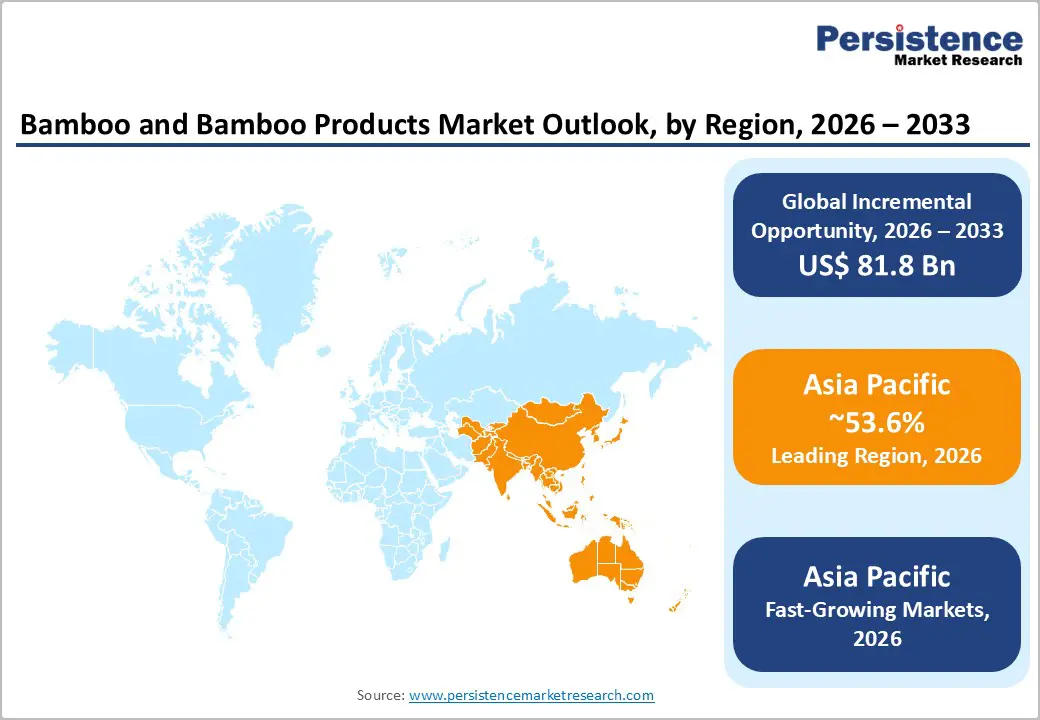

- Leading Region: Asia Pacific leads the global Bamboo and Bamboo Products market with approximately 53.6% revenue share in 2024, anchored by China's contribution of approximately 70% of world bamboo output as documented by the FAO, and supported by the region's vast cultivation base, industrial processing infrastructure, and multi-sector domestic demand.

- Fastest-Growing Region: Asia Pacific is the fastest-growing national bamboo market globally, especially India expanding at a projected CAGR of 11.7%, the highest of any country, driven by the National Bamboo Mission, PM Aawas Yojana housing demand, and a 21% year-on-year growth in bamboo exports to 40 countries in 2024.

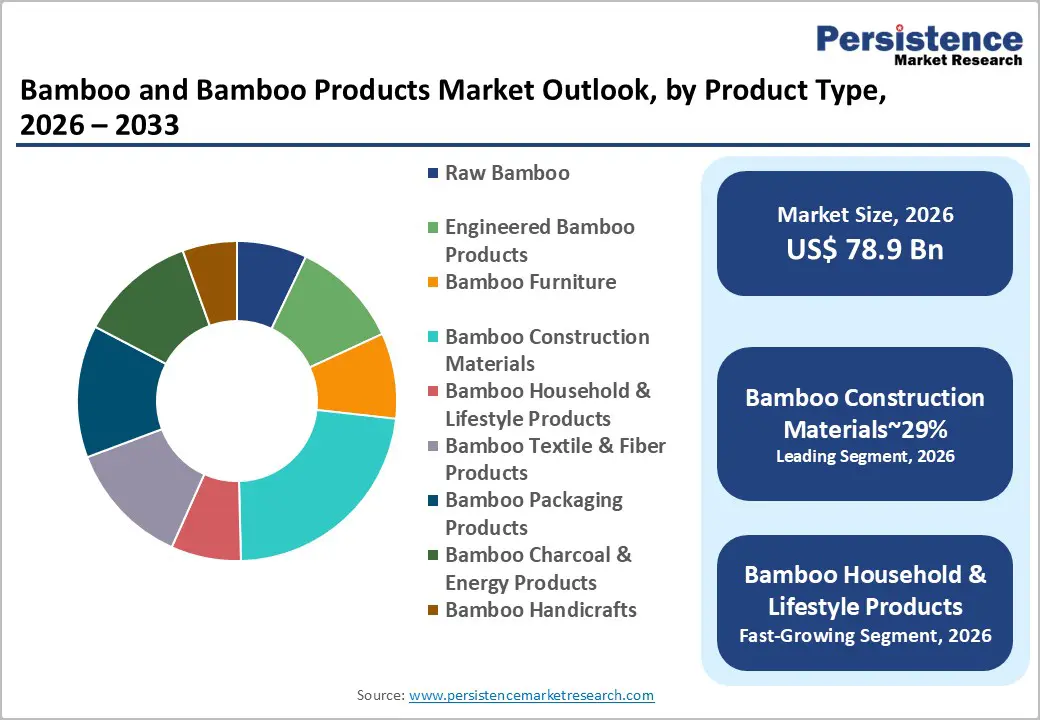

- Leading Segment: Bamboo Construction Materials dominate the Product Type segment with approximately 29% revenue share in 2026, anchored by the global bamboo engineered wood market's valuation of US$ 26.7 Billion in 2024 and accelerating LEED and BREEAM green building specification mandates across North America and Europe.

- Fastest-Growing Segment: Bamboo Textile & Fiber Products are the fastest-growing product type, with bamboo fiber demand projected to grow from US$ 5.4 Billion in 2024 to US$ 15.6 Billion by 2034 at a CAGR of 11.2%, fueled by the global sustainable fashion movement, performance activewear demand, and superior antibacterial and biodegradable fiber properties.

- Key Opportunity: Bamboo packaging represents the key market opportunity, with the EU Single-Use Plastics Directive and California's SB 54 creating regulatory-mandated plastic replacement demand across the world's two largest consumer markets, while the Ellen MacArthur Foundation's 100+ corporate packaging pledges ensure sustained institutional procurement pipelines for biodegradable bamboo packaging solutions.

| Key Insights | Details |

|---|---|

| Bamboo and Bamboo Products Market Size (2026E) | US$ 78.9 Billion |

| Market Value Forecast (2033F) | US$ 160.7 Billion |

| Projected Growth CAGR (2026 - 2033) | 10.7% |

| Historical Market Growth (2020 - 2025) | 8.4% |

Market Dynamics

Drivers - Global Sustainability Megatrend and Green Construction Mandates Accelerating Bamboo Material Adoption

The rapid transition toward sustainable, low-carbon, and circular economy materials in global construction and manufacturing industries is one of the most powerful drivers increasing demand for bamboo and bamboo products across major end-use sectors. The United Nations Environment Programme (UNEP) estimates that the construction sector contributes nearly 38% of global CO2 emissions, creating strong regulatory and environmental pressure for developers, architects, and construction companies to adopt renewable building materials. Engineered bamboo products such as Cross-Laminated Bamboo (CLB), Laminated Bamboo Lumber (LBL), and Bamboo Strand Woven (BSW) panels provide compressive and tensile strength comparable to hardwoods and structural steel while maintaining a significantly lower carbon footprint.

These materials qualify for green building certification programs such as LEED, BREEAM, and EDGE. In addition, the International Bamboo and Rattan Organization (INBAR), working with 48 member countries, actively promotes bamboo as a climate-friendly material aligned with UNFCCC Paris Agreement commitments. Advancements in carbonization, high-pressure lamination, and precision CNC fabrication have further enhanced bamboo’s structural performance, expanding its application across modern construction projects worldwide.

Rising Consumer Preference for Eco-Friendly Products Driving Bamboo Textiles, Packaging, and Consumer Goods Demand

Growing consumer awareness about sustainability and environmentally responsible consumption is creating strong demand for bamboo across textiles, packaging, and consumer goods industries. Bamboo fiber, produced from bamboo pulp through mechanical or chemical processing, offers several natural advantages including antibacterial properties, excellent moisture-wicking capability, UV protection, and superior biodegradability compared with synthetic fibers like polyester and nylon. These benefits make bamboo an increasingly popular material in clothing, personal care products, and household items.

According to the World Bamboo Organization’s 2024 Global Bamboo Resource Report, which surveyed 393 respondents across 68 countries, awareness of bamboo’s environmental benefits is rapidly increasing in key markets such as North America, Europe, and East Asia. This growing awareness is translating into higher purchasing demand for bamboo-based lifestyle products. In October 2024, India exported 502 shipments of bamboo products to 205 buyers across 40 countries, reflecting a 21% year-on-year growth rate. The United States accounted for 53% of these imports, highlighting strong Western demand for sustainable bamboo alternatives.

Restraints - Quality Standardization and Inconsistent Product Certification Constraining Institutional Market Penetration

Although bamboo offers strong environmental and structural benefits, the lack of globally harmonized quality and safety standards remains a major barrier to large-scale adoption, particularly in regulated Western markets. Unlike timber and engineered wood products that follow well-established grading systems under organizations such as the International Organization for Standardization (ISO) and ASTM International, bamboo products still lack universally accepted certification frameworks. This creates uncertainty for architects, structural engineers, and procurement authorities when specifying bamboo materials for infrastructure or commercial construction projects.

While the ISO Technical Committee TC 296 on Bamboo and Rattan is actively working to develop international standards, the process of adoption and industry implementation remains slow. In addition, inconsistent certification practices among smaller manufacturers in major producing countries often raise concerns about product quality and safety. These challenges reduce buyer confidence and slow institutional procurement, particularly in high-value construction, engineering, and industrial applications in North America and Europe where regulatory compliance and material standardization are critical purchasing requirements.

Susceptibility to Moisture, Pests, and Durability Concerns Limiting Untreated Bamboo Applications

Despite its versatility, untreated or minimally processed bamboo continues to face durability challenges that limit its wider application in certain construction and infrastructure projects. Natural bamboo materials are vulnerable to moisture absorption, fungal decay, insect infestation, and dimensional instability when exposed to fluctuating humidity levels. These issues are particularly significant in tropical and subtropical climates where environmental conditions accelerate degradation.

Reports from the Food and Agriculture Organization (FAO) and the International Bamboo and Rattan Organization (INBAR) indicate that untreated bamboo structures may deteriorate within three to five years if appropriate preservation treatments are not applied. As a result, bamboo used in outdoor structures, roofing, and flooring applications often requires chemical or thermal treatment to enhance durability. However, these treatment processes can increase production costs by approximately 25%, reducing bamboo’s price competitiveness compared with alternative materials such as treated timber, plastic composites, or metal structures in cost-sensitive consumer and mid-range construction markets.

Opportunities - Bamboo Packaging Capturing Growing Plastic Replacement Demand Across Global Consumer Markets

The global shift away from single-use plastics is creating a major growth opportunity for bamboo-based packaging products, which are emerging as one of the fastest-growing segments within the bamboo industry. Increasing regulatory restrictions on plastic waste and growing consumer demand for biodegradable alternatives are encouraging companies to adopt plant-based packaging solutions. Policies such as the European Union’s Single-Use Plastics Directive, which banned several disposable plastic products across EU member states beginning in July 2021, have significantly accelerated the transition toward sustainable materials.

Bamboo packaging products including biodegradable food containers, bamboo pulp molded packaging, compostable straws, and bamboo fiber composite bottles are gaining strong market acceptance across Europe, North America, and premium Asian markets. According to the Ellen MacArthur Foundation, more than 100 global corporations have pledged to make all packaging reusable, recyclable, or compostable by 2025. These commitments are creating structured procurement demand for bamboo packaging suppliers. Companies such as Pappco Greenware have already established scalable bamboo packaging solutions serving global foodservice, e-commerce, and personal care brands.

Bamboo-Based Bio-Refinery and Energy Products Creating High-Value Industrial Diversification Opportunities

The development of bamboo-based bio-refineries represents a major industrial diversification opportunity that can significantly expand the commercial value of bamboo biomass. Bio-refinery models process bamboo sequentially into multiple high-value products including bamboo charcoal, bamboo bioethanol, bamboo-derived chemicals, and advanced composite materials. This integrated approach maximizes resource utilization while creating multiple revenue streams within the bamboo value chain. In 2024, India’s largest power producer NTPC partnered with Numaligarh Refinery Limited (NRL) to establish a bamboo-based bio-refinery project, marking a significant step toward industrial-scale bamboo energy utilization.

Under India’s National Bamboo Mission, bamboo charcoal and bamboo biogas have been identified as priority applications, with approximately 12.8 million metric tonnes of bamboo biomass available annually for potential energy production. Additionally, the International Bamboo and Rattan Organization promotes bamboo bio-charcoal as a carbon-sequestering soil amendment that improves agricultural productivity while generating carbon credit opportunities. This dual environmental and economic value proposition is attracting growing climate finance investment into bamboo-based energy and bio-material development globally.

Category-wise Insights

By Product Type

Bamboo construction materials lead the global bamboo and bamboo products market by product type, accounting for approximately 29% of total product type segment revenue in 2026. This leadership is driven by bamboo’s increasing recognition as a strong, sustainable, and low-carbon alternative to traditional timber and composite materials used in residential, commercial, and infrastructure construction worldwide.

The engineered bamboo sub-category, covering glued laminated bamboo (Glulam), cross-laminated bamboo (CLB), and bamboo strand woven (BSW) panels, is experiencing rapid adoption due to growing demand for green building materials and certification incentives such as LEED and BREEAM. Residential construction accounts for around 40% of engineered bamboo applications, supported by green housing initiatives in China, India, and Europe.

By Processing Type

The engineered bamboo segment leads the global Bamboo and Bamboo Products market by processing type, accounting for approximately 38% of total processing segment revenue in 2026. These products are created through advanced industrial processes such as high-pressure lamination, heat carbonization, chemical stabilization, and CNC precision fabrication, which improve bamboo’s durability, stability, and structural strength. These technologies help overcome the natural variability of raw bamboo, enabling manufacturers to produce standardized, high-performance materials suitable for construction and industrial applications.

Advancements in cross-lamination, improved resin systems, and heat treatment technologies have significantly enhanced engineered bamboo’s resistance to humidity, insects, and warping, making it suitable for demanding structural uses where untreated bamboo was previously limited. Growth is driven by increasing demand for moisture-resistant bamboo decking, cladding, and automotive interior panels, which offer sustainable alternatives to tropical hardwood and plastic composites.

Distribution Channel Analysis

The offline distribution channel dominates the global Bamboo and Bamboo Products market, accounting for approximately 71% of total distribution channel revenue in 2026. Traditional offline networks, such as building material distributors, specialty furniture retailers, timber merchants, textile wholesalers, and direct manufacturer-to-project sales, continue to play a major role in product distribution. These channels remain essential because many high-value bamboo products, particularly construction materials and furniture, require physical inspection before purchase.

In addition, bulk transportation requirements for raw and semi-processed bamboo products make traditional supply chains more practical for large-scale transactions. Government procurement programs and major construction project tenders also typically operate through established offline channels, reinforcing their dominance in revenue-generating market segments. However, the Online distribution channel is the fastest-growing segment, supported by the rapid expansion of global e-commerce platforms. Online marketplaces such as Amazon, Alibaba, and direct-to-consumer brand websites are enabling bamboo product manufacturers to reach environmentally conscious consumers across North America and Europe more efficiently.

By End-user

The construction & infrastructure segment leads the global bamboo and bamboo products market by end-user, representing approximately 35% of total segment revenue in 2026. This leadership reflects the enormous scale of global construction activities, particularly across the Asia Pacific region, along with the growing transition toward sustainable and eco-friendly building materials. Bamboo construction products are increasingly viewed as practical alternatives to conventional materials such as concrete and steel in green building projects. According to INBAR, bamboo-based construction can reduce a building’s carbon footprint by up to 30%, making it an attractive option for developers and governments pursuing climate-focused infrastructure programs. Meanwhile, the Textile & Apparel segment is the fastest-growing end-use category, supported by increasing demand for sustainable fabrics worldwide.

Regional Insights

North America Bamboo and Bamboo Products Trends

North America represents a high-value growth market for bamboo products, largely driven by the United States’ position as the world’s largest importer of bamboo-based goods and one of the most mature consumer markets for premium eco-certified products. The U.S. Green Building Council’s LEED certification program, which includes more than 100,000 certified buildings across North America, recognizes rapidly renewable materials such as bamboo as contributors to sustainable building credits.

This policy framework is encouraging architects and developers to increasingly adopt bamboo flooring, panels, and furniture in both residential and commercial projects. In October 2024, the United States accounted for 53% of India’s bamboo product exports, highlighting the region’s strong role as a premium import destination for processed bamboo goods from Asian manufacturing hubs. Additionally, policy initiatives such as California’s Plastic Pollution Prevention and Packaging Producer Responsibility Act (SB 54) are accelerating demand for biodegradable bamboo packaging solutions, encouraging retailers and foodservice companies to shift toward sustainable packaging alternatives.

Europe Bamboo and Bamboo Products Trends

Europe is widely recognized as the most policy-driven demand market for bamboo products, supported by regulatory initiatives such as the European Green Deal, the EU Single-Use Plastics Directive, and the EU Renovation Wave Strategy. These policies collectively encourage the adoption of sustainable materials across construction, packaging, textiles, and consumer goods industries. Germany, the largest economy in Europe, is the region’s leading importer and consumer of bamboo engineered wood and flooring products, supported by its strong green construction sector and energy-efficient building renovation programs.

Companies such as MOSO International BV, headquartered in the Netherlands, have established a strong market presence by supplying FSC-certified bamboo flooring, decking, and structural panels to high-end construction projects across Germany, France, the United Kingdom, and Scandinavia. In addition, regulations such as France’s AGEC Anti-Waste Law and the UK Environment Act 2021 are pushing businesses to reduce non-biodegradable packaging, increasing demand for bamboo pulp packaging solutions across European consumer goods supply chains.

Asia Pacific Bamboo and Bamboo Products Trends

Asia Pacific remains the global center of bamboo production and consumption, accounting for approximately 53.6% of global bamboo market revenue in 2024. This dominance is supported by the region’s vast bamboo resources, established industrial processing infrastructure, and long cultural tradition of bamboo utilization across multiple industries. China is the world’s largest bamboo producer and manufacturer, contributing nearly 70% of global bamboo output, according to the FAO. The country has built a comprehensive bamboo industrial ecosystem that includes raw bamboo cultivation, chemical pulping, engineered panel manufacturing, furniture production, and bamboo charcoal processing.

The National Forestry and Grassland Administration (NFGA) has also introduced policy targets aimed at significantly expanding China’s bamboo industry value by 2035, focusing on high-value processing and export development. India is emerging as the fastest-growing bamboo market in the region, supported by the National Bamboo Mission, affordable housing initiatives under PM Aawas Yojana, and increasing adoption of bamboo fiber in the textile industry.

Competitive Landscape

The global bamboo and bamboo products market is highly fragmented, reflecting the wide range of products, applications, and regional production clusters within the industry. Thousands of small and medium-scale producers across China, India, and Southeast Asia operate alongside a smaller group of internationally recognized specialty companies. Premium market leaders such as MOSO International BV in Europe and Smith and Fong Company in North America differentiate themselves through FSC and PEFC certification, consistent product quality, and design-focused product portfolios.

At the same time, large Chinese manufacturers, including Xiamen HBD Industries and Huayu Group compete primarily on cost efficiency and high production scale. Emerging industry trends include blockchain-based supply chain transparency, carbon credit monetization through bamboo plantation programs, and vertically integrated business models that control the value chain from cultivation to finished consumer products. Additionally, many regional brands are increasingly adopting B2C e-commerce strategies to directly target environmentally conscious consumers in premium markets such as North America and Europe.

Key Developments:

- In January 2024: NTPC Limited and Numaligarh Refinery Limited signed a strategic MoU to explore opportunities in bamboo-based bio-refinery projects at NTPC Bongaigaon, focusing on producing biofuels and green chemicals while supporting India’s net-zero goals and sustainable industrial development in the Northeast region.

- In October 2024: India’s bamboo export sector recorded strong growth, with 502 shipments delivered to 205 buyers across 40 countries, reflecting a 21% year-on-year increase. The United States emerged as the largest importer, absorbing 53% of exports, highlighting rising North American demand for sustainable bamboo products.

- In March 2024: Grasim Industries Limited announced investments to expand its sustainable fiber portfolio, including bamboo-based textiles. The move strengthens production capacity for eco-friendly fibers and supports the company’s strategy to meet rising global demand for sustainable fabrics in both domestic and international textile markets.

Companies Covered in Bamboo and Bamboo Products Market

- MOSO International BV

- Bamboo Village Company

- Kerala State Bamboo Corporation

- Shanghai Tenbro Bamboo Textile Company

- Smith and Fong Company

- Huayu Group

- Pappco Greenware

- Xiamen HBD Industries and Trade Company

- Bamboo Master

- Meysher Industrial Group

- Jiangxi Bamboo Technology Development Company Ltd.

- Ganzhou Sentai Bamboo Wood Co., Ltd.

- Mesun Bamboo

- Yi Bamboo

- Takemoku Co., Ltd.

- EcoPlanet Bamboo Group

- Tong Siang Co., Ltd.

- Bamboo Australia

- BamCore

- Anji Tianzhen Bamboo Flooring Co., Ltd.

Frequently Asked Questions

The global Bamboo and Bamboo Products market is estimated to be valued at US$ 78.9 Billion in 2026 and is projected to reach US$ 160.7 Billion by 2033, registering a forecast CAGR of 10.7% over the period 2026 to 2033. The market recorded a historical growth rate of 8.4% CAGR between 2020 and 2025, driven by sustainable materials adoption and construction demand.

The primary growth drivers are the global construction sector's decarbonization mandate, with UNEP attributing 38% of global CO₂ emissions to construction, driving specification of engineered bamboo as a low-carbon structural material, and the dramatic rise in consumer demand for eco-certified bamboo textiles and packaging, evidenced by India's 21% year-on-year bamboo export growth in 2024 reaching 205 buyers across 40 countries.

Bamboo Construction Materials lead the Product Type category with approximately 29% revenue share in 2026, underpinned by the global bamboo engineered wood market's valuation of US$ 26.7 Billion in 2024 and accelerating adoption under LEED, BREEAM, and EDGE green building certification programs. Residential construction accounts for approximately 40% of engineered bamboo applications, driven by rising green housing initiatives in China, India, and Europe.

Asia Pacific leads the global Bamboo and Bamboo Products market with approximately 53.6% revenue share in 2024, anchored by China's dominant contribution of approximately 70% of world bamboo production as documented by the FAO. The region's established industrial processing ecosystem, vast cultivation base, and multi-sector application depth across construction, textiles, packaging, and consumer goods collectively reinforce its sustained global market leadership.

The most significant growth opportunity lies in bamboo packaging as a plastic replacement solution. The EU Single-Use Plastics Directive and California's SB 54 are creating regulatory-mandated demand for biodegradable bamboo packaging alternatives, while the Ellen MacArthur Foundation's documentation of over 100 global corporations pledging fully circular packaging by 2025 ensures structured and growing institutional procurement pipelines for scalable bamboo packaging manufacturers.

The leading companies include MOSO International BV, Smith and Fong Company, Shanghai Tenbro Bamboo Textile Company, Huayu Group, Xiamen HBD Industries and Trade Company, Pappco Greenware, Kerala State Bamboo Corporation, Jiangxi Bamboo Technology Development Company Ltd., Ganzhou Sentai Bamboo Wood Co., Ltd., Takemoku Co., Ltd., BamCore, Yi Bamboo, Mesun Bamboo, EcoPlanet Bamboo Group, and Anji Tianzhen Bamboo Flooring Co., Ltd., among other prominent participants globally.